Headline CPI 0.9%qtr/2.4%yr; Trimmed Mean 0.7%qtr/2.9%yr; Weighted Median 0.7%qtr/2.9%yr. Momentum in core inflation at the bottom of the band.

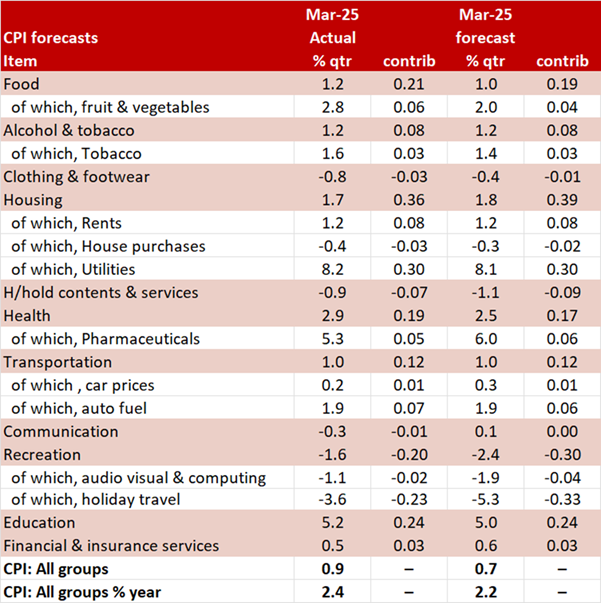

The CPI gained 0.9% in the March quarter, stronger than market consensus (0.8%) and Westpac’s expectation (0.7%) but we did highlight upside risk to our estimate. The annual pace of headline inflation, at 2.4%yr now definitively below the mid-point of the RBA’s inflation target band.

The more important measure of core inflation, the Trimmed Mean, rose 0.7% taking the annual pace down into the RBA’s target band at 2.9%yr with the two-quarter annualised pace dropping down to 2.4%yr. Westpac and the market had been looking for a 0.6% increase while we did see the risk to the upside of our estimate.

With the momentum in core inflation definitively at the bottom of the target band inflationary pressures have moderated, and the door is open for a rate cut in May. Our Chief Economist, Luci Ellis, had already locked in a rate cut for May “Lock it in: RBA to cut 25bps in May” and today’s data provides no reason to question that view.

The Monthly CPI Indicator came in 2.4%yr, the market was expecting 2.2%yr, Westpac was at 2.0%yr. Most of the variation to our estimate was due to stronger than expected increases in food, electricity, health, travel and education.

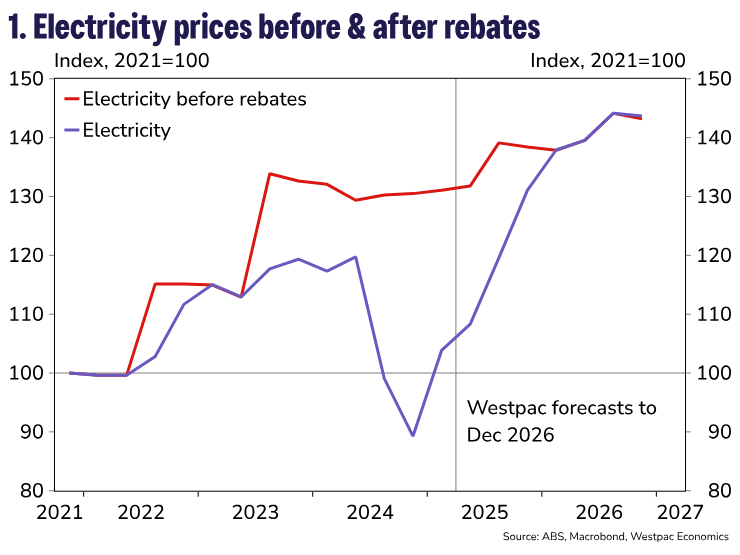

Headline inflation has been significantly reduced by various cost-of-living measures, but this is now being reversed as the energy rebates are being unwound, particularly the large $1,000 lump sum rebate in Qld. This quarter we saw a 16.3% increase in electricity prices which was stronger than our 14.5% estimate (worth an additional 0.05ppt on the CPI).

We estimated that these measures have shaved 0.5% off inflation in the year to March 2025. However, in the quarter with electricity prices rising we found that the rebates added 0.1ppt to the CPI. However, impact of these cost-of-living measures have had a limited impact on core inflation. As such the Trimmed Mean remains a reliable measure of core inflationary pressures and thus presents no hinderance to a rate cut by the RBA.

Core inflation is being held down by the moderation in housing inflation due to the moderation in rents and dwellings. Rents did rise a robust 1.2% in the quarter, but this is a step down from the 1.6% increase last September, 2.0% last June and 2.1% last March. The 0.6% increase last December was due to the maximum assistance from the Commonwealth Rent Assistance being increased by 10% on 20 September 2024. The annual pace of rental inflation is now down to 5.5%yr from 6.4%yr in December and a March 2024 peak of 7.8%yr.

This also has an impact on services inflation as the slower pace of services inflation in the March quarter was driven by moderating price growth for insurance and rents. Services inflation was 3.7%yr in March, down from 4.3%yr in December and a recent peak of 4.6%yr at September 2024. Market sector services, which is our preferred measure of domestic inflationary pressure, fell –0.1% in the March quarter, the first quarterly decline since June 2020. This took the annual pace down to 3.3%yr from 4.2%yr in December. This is the slowest pace of market services ex volatile inflation since March 2022. We had been expecting this measure to moderate as wages undershot expectations through 2024.

Dwelling prices fell –0.4% in March following a –0.2% fall in December taking the annual pace of dwellings inflation to 1.4%yr. Dwellings inflation peaked at 20.7yr in September 2022. The ABS notes that the moderation in dwellings inflation reflects project home builders increasing incentives and promotional offers to entice new business in a subdued new home market.

Compared to our expectations the main variations in the components of the CPI were:

- Food increased 1.2% vs 1.0% expected (+0.02ppt). The main contributors to the rise were fruit & vegetables (+2.8%), meals out & take away foods (+0.6%), non-alcoholic beverages (+3.2%) and food products n.e.c (+1.6%). Most of our error was with fruit & vegetables.

- Clothing footwear fell –0.8% vs –0.4% expected (–0.01ppt). The main contributors to the fall were garments (-1.1%) and footwear (-3.7%), driven by post-Christmas and back to school sales.

- Household contents & services fell –0.9% vs –1.1% expected (+0.01ppt). Furniture (-5.5%) was the main contributor to the fall, driven by post-Christmas sales on bedroom furniture. There was a partial offset from child care (+2.4%).

- Health rose +2.9% vs 2.5% expected (+0.03ppt). Medical & hospital services (+2.7%) and pharmaceutical products (+5.3%) rose because of the cyclical reduction in the proportion of consumers who qualify for subsidies under the Medicare Safety Net and Pharmaceutical Benefits Scheme (PBS). The safety net thresholds for both the PBS and Medicare are reset on 1 January each year.

- The most significant variation to our estimate was in recreation which recorded a –1.6% fall compared to –2.4 fall expected (0.10ppt) of which most was due to a smaller than expected fall in holiday travel: –3.6% vs –5.3% expected (0.11ppt). International holiday travel & accommodation (-7.6%) was the main contributor to the fall due to lower demand following the peak December holiday period.

- Education was a touch stronger at 5.2% vs 5.0% expected (0.01ppt). Secondary education (+6.4%) and preschool & primary education (+5.6%) rose reflecting fee increases at the start of the school year. The rises were driven by higher operating costs that were passed through as higher school fees. Tertiary education rose 3.6% due to the annual CPI indexation being applied to university course fees at the start of the year. This was partly offset by soft growth in TAFE fees as the federal government, in partnership with state and territory governments, continued fee-free TAFE places in 2025.

and Westpac’s expectation (0.7%) but we did highlight upside risk to our estimate. The annual pace of headline inflation, at 2.4%yr now definitively below the mid-point of the RBA’s inflation target band.){kind=link}