Summary

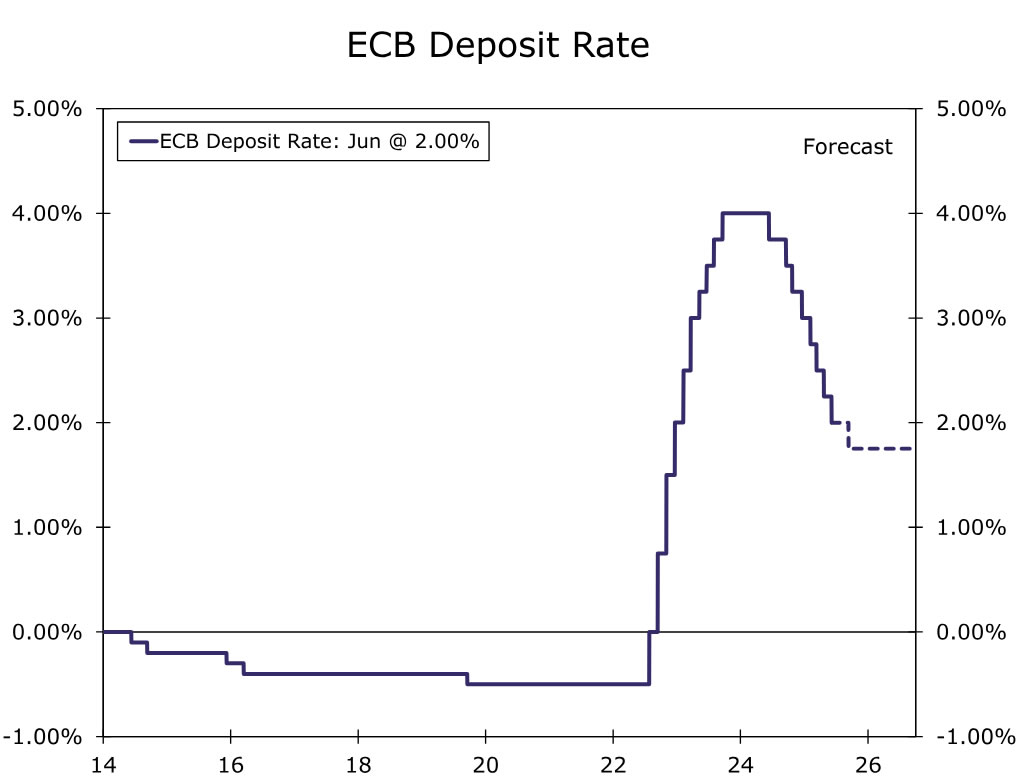

- The European Central Bank (ECB), in a widely expected decision, lowered its Deposit Rate by 25 bps to 2.00% at today’s announcement, while its accompanying statement contained both dovish elements and some more constructive elements.

- The ECB noted that current conditions were exceptionally uncertain, while also observing a deceleration in underlying inflation pressures and wage growth. While the ECB offered limited policy guidance for the meetings ahead, ECB President Lagarde did say the central bank was “getting to the end of a monetary policy cycle.”

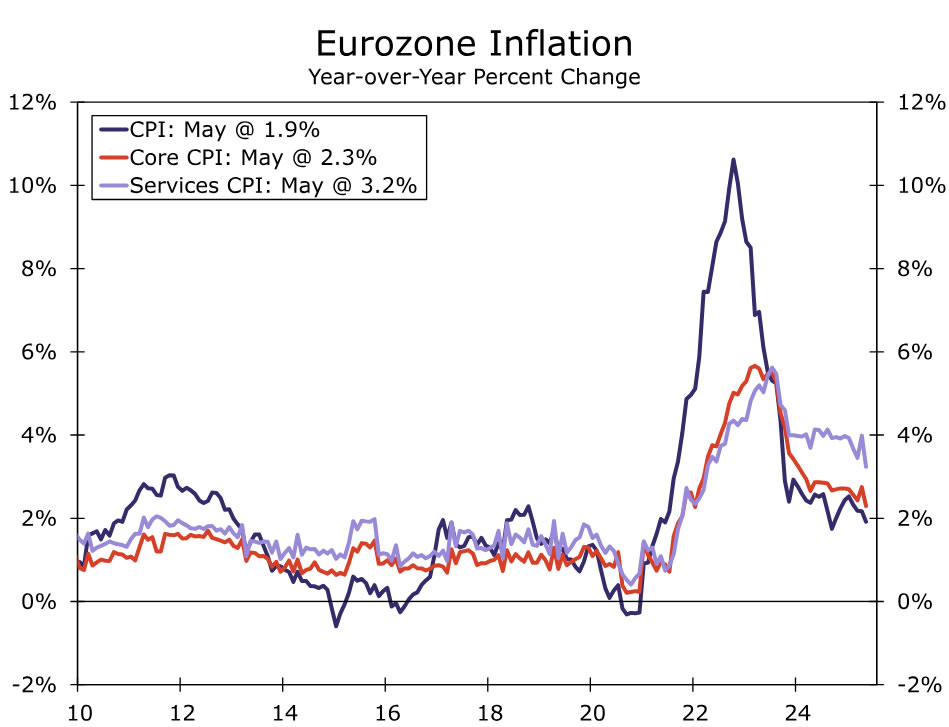

- The ECB also provided updated economic projections. The central bank’s GDP growth forecasts were little changed. Regarding prices, the forecasts for headline inflation were lowered on the back of reduced oil prices and a stronger euro. There was little change to the ECB’s underlying (CPI ex food and energy) forecasts, although a projection of 1.9% for both 2026 and 2027 suggests, in our view, the ECB maintains a modest easing bias.

- We think today’s monetary policy announcement supports further monetary easing, though it does not alter our view on the likely pace of ECB rate cuts. We expect a pause from the ECB at its July meeting and a 25 bps rate cut by the ECB in September, which would take the Deposit Rate to 1.75%. While we think the risks are likely tilted toward a more pronounced easing cycle, we do not yet see compelling enough evidence for the ECB to hasten or add to its rate cut cycle.

European Central Bank Cuts Rates, Leaves Door Open For Further Easing

The European Central Bank (ECB) cut its Deposit Rate by 25 bps to 2.00% at today’s monetary policy announcement in a widely expected decision, bringing the cumulative easing during the current cycle to 200 bps. The accompanying announcement was careful to provide only limited guidance on the path for future monetary policy, though, in our view, the ECB’s comments and updated economic projections keep the door open for further monetary easing. Among the key elements of today’s announcement, the ECB said:

- Current conditions were that of “exceptional uncertainty.”

- Most measures of underlying inflation suggest inflation will settle around 2% on a sustained basis.

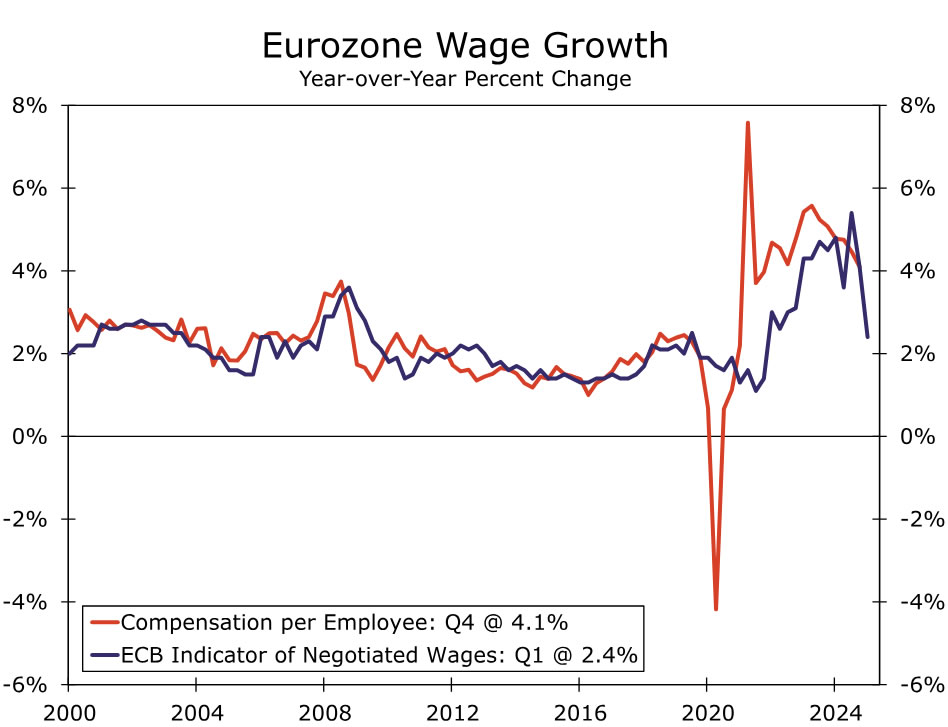

- Wage growth is still elevated but continues to moderate visibly, and profits are partially buffering its impact on inflation.

While acknowledging near-term headwinds to growth, on a somewhat more constructive note, the ECB also said “rising government investment in defense and infrastructure will increasingly support growth over the medium term. Higher real incomes and a robust labor market will allow households to spend more. Together with more favorable financing conditions, this should make the economy more resilient to global shocks.”

As has typically been the case recently, the ECB offered limited future guidance. The central bank said “it will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance” and that it is “not pre-committing to a particular rate path.” Importantly however, in the post-meeting press conference, ECB President Lagarde said the central bank was “getting to the end of a monetary policy cycle.”

Regarding the ECB’s updated economic projections, the central bank’s GDP growth forecasts were little changed at 0.9% for 2025, 1.1% for 2026 and 1.3% for 2027. We, along with the ECB, assess the risks around these growth forecasts as likely tilted to the downside. The forecasts for headline inflation were reduced, reflecting lower oil prices and in part a stronger euro, at 2.0% for 2025, 1.6% for 2026 and 2.0% for 2027. However, forecasts for underlying inflation trends (the CPI excluding food and energy) were actually revised higher to 2.4% for 2025, slightly lower to 1.9% for 2026 and unchanged at 1.9% for 2027. The fact that the underlying inflation forecasts for 2026 and 2027 are slightly below the ECB’s 2% inflation suggests, in our view, that the ECB maintains a modest easing bias.

Finally, the ECB outlined some scenario analysis related to differing potential paths for the evolution of global trade tensions. Under these scenarios, “a further escalation of trade tensions over the coming months would result in growth and inflation being below the baseline projections. By contrast, if trade tensions were resolved with a benign outcome, growth and, to a lesser extent, inflation would be higher than in the baseline projections.”

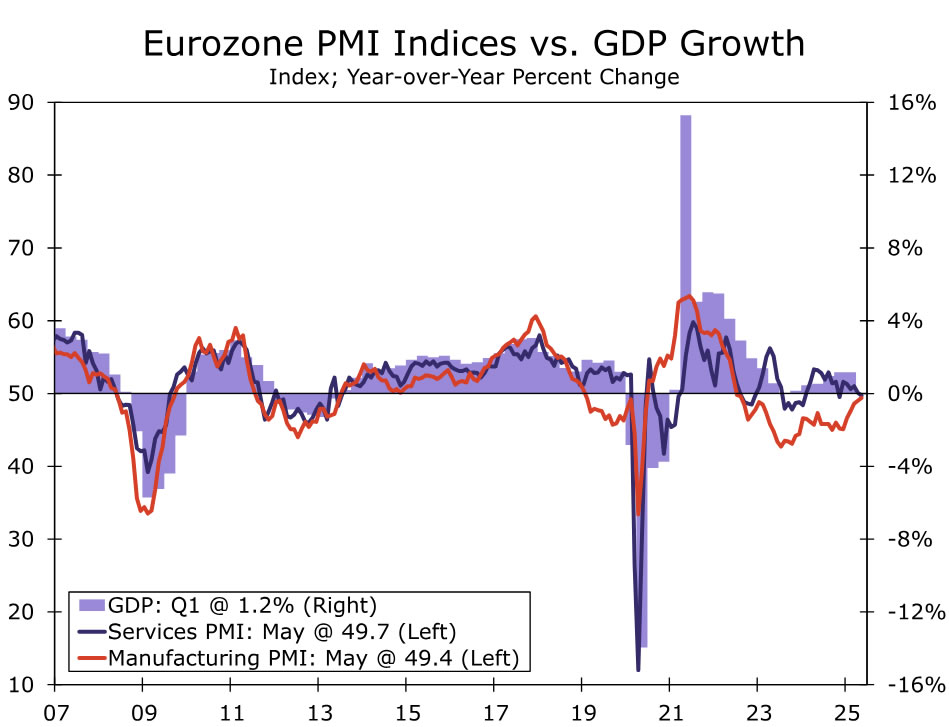

Overall we view the ECB’s ongoing, albeit modest, easing bias as well-founded. Both headline and core inflation slowed in May, to 1.9% year-over-year and 2.3% year-over-year respectively. The ECB’s Indicator of Negotiated Wages slowed to 2.4% year-over-year in Q1, and other wage growth measures are also moderating. Meanwhile, sentiment surveys remain downbeat, suggesting that growth is likely to underwhelm in the immediate months ahead. That said, while we think today’s monetary policy announcement supports the view of further monetary easing, it does not alter our view on the likely pace of ECB rate cuts, especially considering Lagarde’s comments regarding where we are in the easing cycle. We expect a pause from the ECB at its July meeting, and a 25 bps rate cut by the ECB in September, which would take the Deposit Rate to 1.75%. To be sure, the risks still appear somewhat tilted toward faster or more pronounced ECB rate cuts, with CPI inflation, GDP growth, sentiment surveys, and the evolution of trade tensions all having the potential to disappoint to the downside in the coming months. That said, we also remain “data-dependent” and do not yet see compelling enough evidence to suggest a more extended ECB easing cycle, given the ECB’s policy rate is already in a neutral zone. Against that backdrop, at this time our base case remains for the ECB to deliver its final rate cut of the current easing cycle in September.

cut its Deposit Rate by 25 bps to 2.00% at today's monetary policy announcement in a widely expected decision, bringing the cumulative easing during the current cycle to 200 bps. The accompanying announcement was careful to provide only limited guidance on the path for future monetary policy, though, in our view, the ECB's comments and updated economic projections keep the door open for further monetary easing. Among the key elements of today's announcement, the ECB said:){kind=link}