Summary

- Despite the ongoing tumult around trade policy, the near-term outlook for monetary policy is steady-as-she-goes. We expect the FOMC will leave its target range for the fed funds rate unchanged at 4.25%-4.50% at the conclusion of its upcoming meeting on June 17-18.

- “Hard” data show economic activity continues to hold up amid elevated policy uncertainty. Consumer spending started the second quarter with strong momentum, employment continued to expand at a healthy clip in May and the unemployment rate has held steady since March at a level consistent with the FOMC’s estimate of full employment. The latest readings on consumer and producer prices point to core PCE inflation inching up to 2.6% on a year-ago basis in May, up from 2.5% in April and still above the FOMC’s target of 2%.

- Changes to trade policy have ushered in upside risks to both unemployment and inflation. But, with current data showing activity remaining resilient, we expect the post-meeting statement and Chair Powell’s press conference will convey that the Committee is still in no hurry to adjust policy. We believe the FOMC will need to see more pronounced softening in the labor market to begin cutting the fed funds rate again this year. We expect to see this softening in the coming months and look for 75 bps of easing by year end.

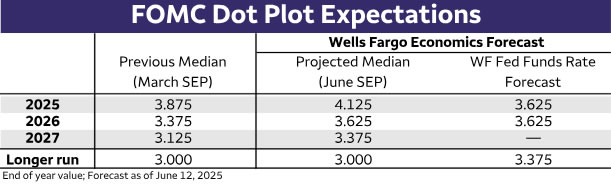

- An update to the Summary of Economic Projections (SEP) will provide a fresh look at what Committee members think lies ahead for the economy and the fed funds rate. We expect the median projection for the fed funds rate at year-end will move up 25 bps to 4.125%, although we would not be surprised if the median dot for 2025 were left unchanged at 3.875%. The same can be said for the 2026 dot moving up 25 bps to 3.625%.

- Elsewhere in the SEP, we expect to see projections for inflation at the end of 2025 move a few tenths higher in light of the changes to tariff rates since the March SEP. Estimates for GDP growth are likely to be revised down to only a little over 1% following the first quarter’s decline and lingering challenges to growth in the second half of the year. Yet, the median estimate for the unemployment rate may very well remain unchanged at 4.4%, as slower growth in the labor supply and an ongoing reluctance among businesses to cut workers keeps the jobless rate from moving up significantly this year.

The Economy Remains “Solid” While Inflation Is Still “Somewhat Elevated”

When the Federal Open Market Committee (FOMC) voted unanimously on May 7 to keep its target range for the federal funds rate unchanged at 4.25%-4.50%, the Committee noted in its post-meeting statement that “recent indicators suggest that economic activity has continued to expand at a solid pace.” It also stated that “labor market conditions remain solid.” When it releases its next post-meeting statement on June 18, we think the FOMC may note economic activity has expanded at a “moderate” pace, while continuing to characterize the labor market as “solid.”

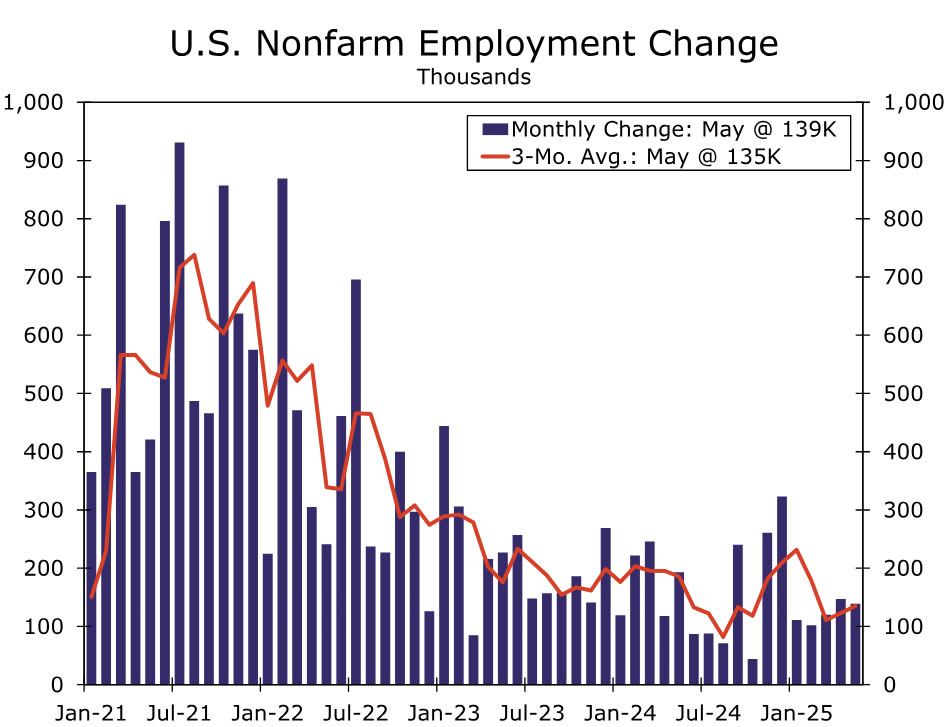

For example, recently released data show that real personal consumption expenditures (PCE) continued to grow in April. Although the 0.1% increase in real PCE is obviously not very strong, it followed a robust gain of 0.7% in March. In other words, real consumer spending started off the second quarter with strong momentum. Additionally, employment continued to expand in May. Factoring in downward revisions to March and April data, nonfarm payrolls increased an average of 135K the past three months, while the unemployment rate has held steady at 4.2% since March (Figure 1).

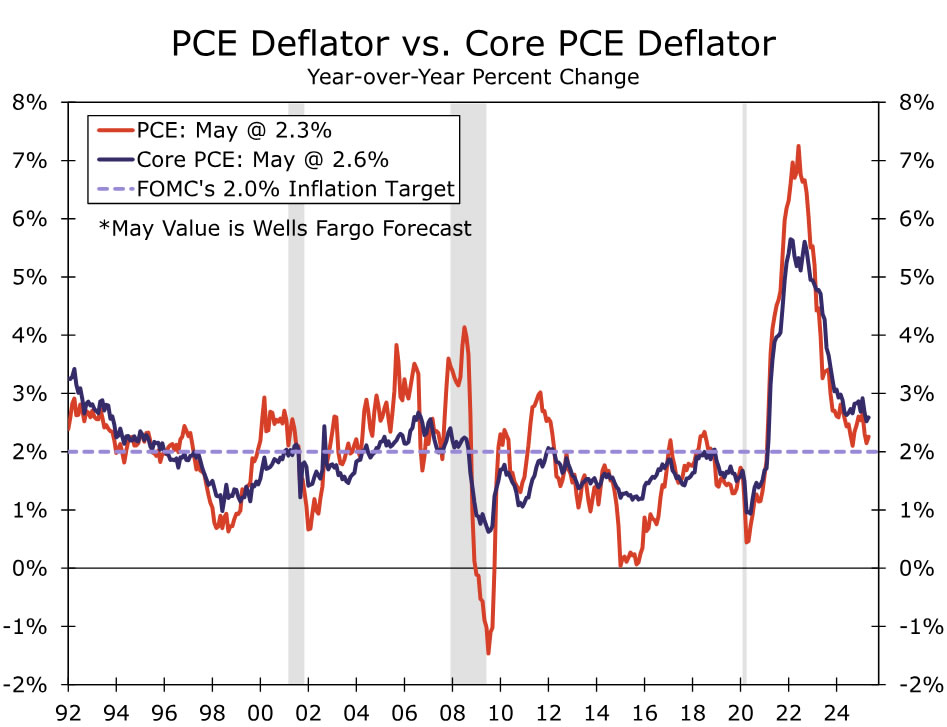

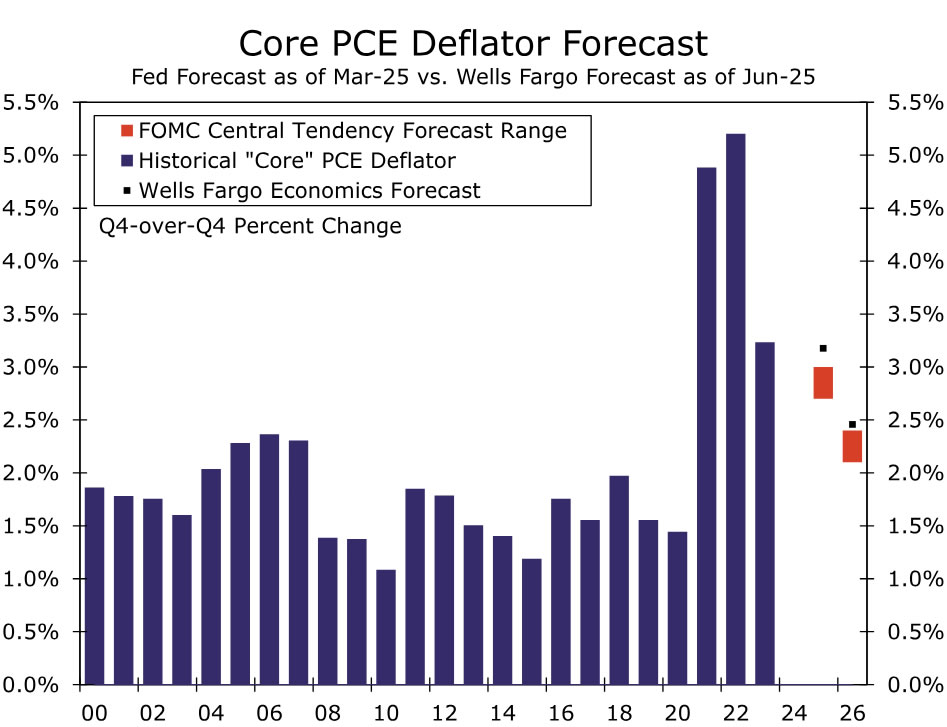

Turning to the other side of its dual mandate, the FOMC noted in its last statement that “inflation remains somewhat elevated.” The most recent reading on the year-over-year change in the core PCE deflator, which most Fed officials consider to be the best measure of the underlying rate of consumer price inflation, came in at 2.5% in April. The May CPI report came in softer-than-expected and was welcome news for the FOMC. That said, we believe it is too early for the FOMC to declare victory and say that the significant increase in tariffs over the past few months will have no material impact on consumer price growth. Most of the tariff increases occurred over the March-May period, and we doubt enough time has elapsed for the full effects of these policy changes to be felt on pricing. Furthermore, based on the May CPI and PPI reports, we expect core PCE inched up to 2.6% in May, still above the FOMC’s target of 2% (Figure 2). Given these crosscurrents, we see little reason for the FOMC to make a change to the current stance of monetary policy at this time.

Recent comments by Fed officials seem to indicate the Committee is content with the current stance of monetary policy. For example, Chair Powell said in his May 7 press conference that “we don’t think we need to be in a hurry. We think we can be patient.” More recently, Chicago Fed President Austan Goolsbee noted that the bar for a near-term rate cut is “a little higher.” Goolsbee’s sentiment is instructive. Not only is he a voting member of the FOMC this year, but most observers consider Goolsbee to be “dovish.” If a dovish member of the FOMC thinks it probably would not be appropriate to ease policy at this time, it is hard to envision the hawkish members arguing for a rate cut on June 18. Most market participants seem to agree that the Committee will remain on hold at its next meeting. As of this writing, the implied probability of a 25 bps rate cut on June 18 is essentially 0%.

Uncertainty Remains Elevated

Moreover, a change in the monetary policy stance when the economic outlook remains highly uncertain, due in part to the ever-evolving outlook for U.S. trade policy, does not seem likely. At the conclusion of the FOMC meeting on March 19, which happened before President Trump announced his “Liberation Day” tariffs on April 2, the Committee said “uncertainty about the economic outlook has increased.” The FOMC’s statement on May 7 read “uncertainty about the economic outlook has increased further” (emphasis ours). Uncertainty may not have increased even more relative to the last FOMC meeting, but it clearly has not diminished by a significant degree, in our view. Therefore, we expect the statement on June 18 will note that uncertainty remains elevated.

This uncertainty is manifested in the outlooks for unemployment and inflation, the two goals of the Fed’s dual mandate. On March 19 the FOMC said, as it has in other recent statements, that it “is attentive to the risks to both sides of its dual mandate.” The Committee included that sentence in its May 7 statement but added the following clause: “and judges that the risks of higher unemployment and higher inflation have risen.” We think the FOMC will continue to note in its June 18 statement that the risks of higher unemployment and higher inflation remain elevated.

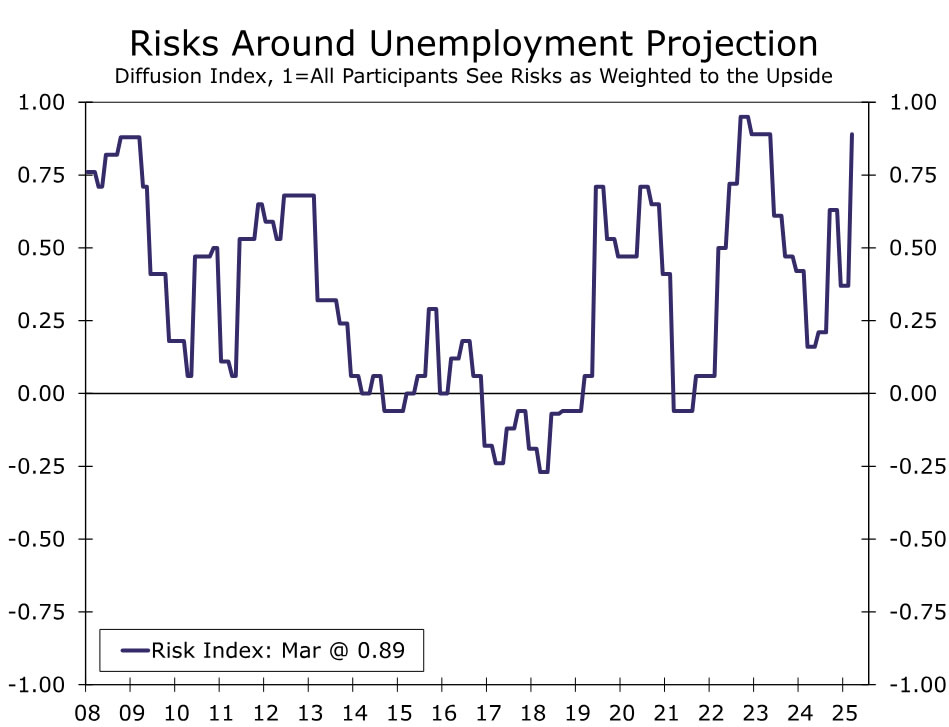

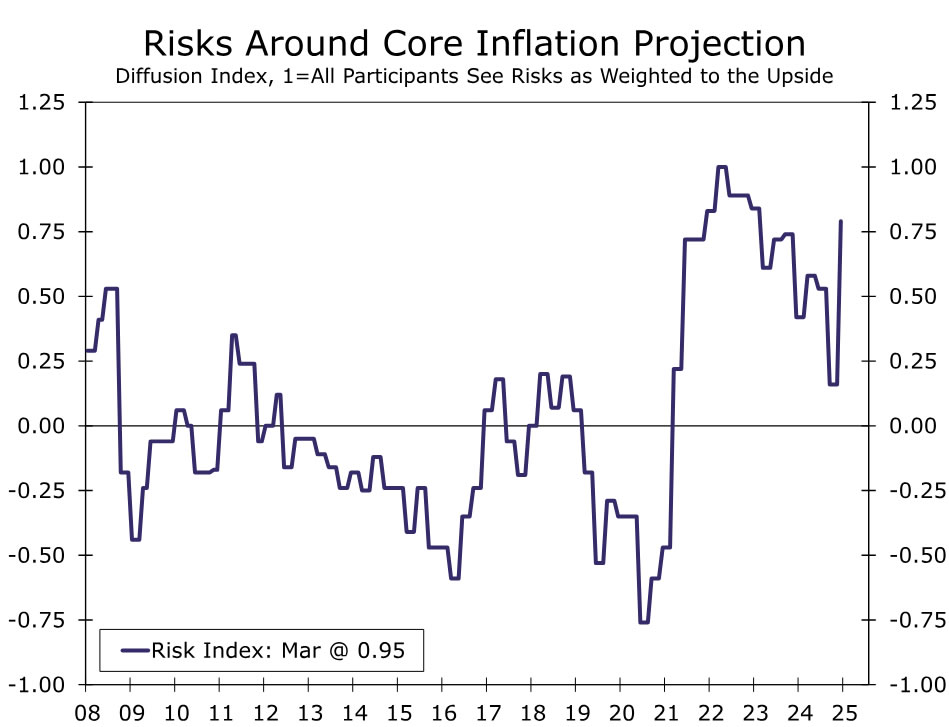

As part of its quarterly Summary of Economic Projections (SEP), the FOMC includes an assessment of the risks to its macroeconomic forecasts. When the last SEP was released on March 19, the number of FOMC members indicating that the risks to their individual unemployment rate projections were “weighted to the upside” jumped significantly relative to the December SEP (Figure 3). Additionally, the risks to the core PCE inflation forecasts were also “weighted to the upside” (Figure 4). We expect these measures of risk in the June SEP will remain elevated, if not move higher.

Upside risks to both unemployment and inflation produce a conundrum for the FOMC. On one hand, the Committee would want to respond to an upside surprise to unemployment with policy easing. On the other hand, higher-than-expected inflation would induce the FOMC to respond with policy tightening. Given the heightened level of uncertainty, the FOMC is likely to deem that the best course of action, at least at the present time, may be simply to keep the stance of policy unchanged and watch incoming data to determine if a change in policy is warranted.

Outlook for the Dots

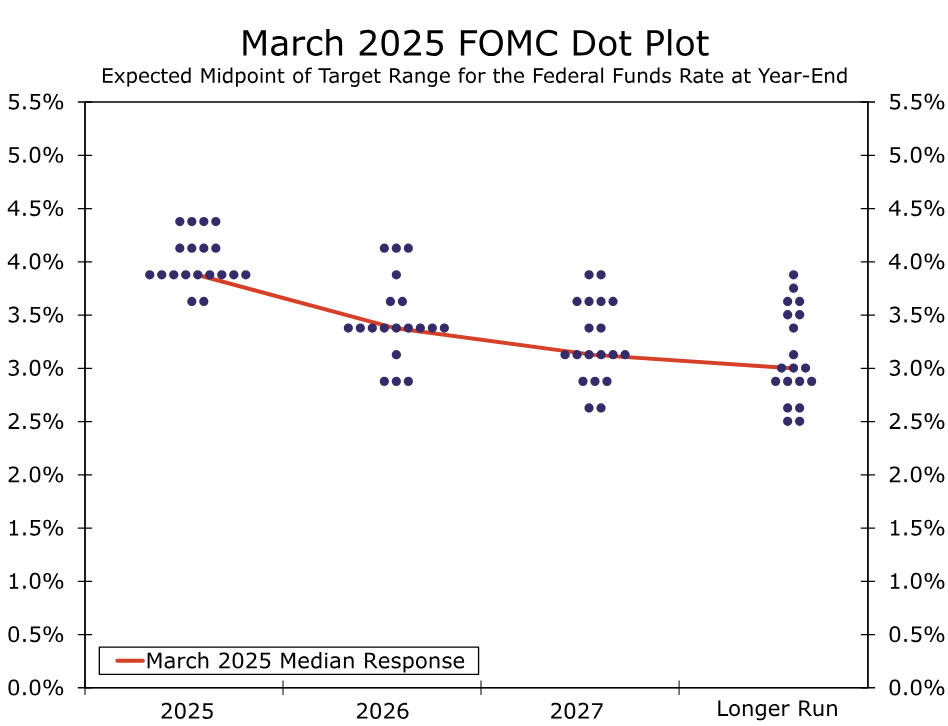

Given the uncertainty surrounding the economic outlook, we do not expect significant changes to the dot plot, which portrays the monetary policy expectations of the individual FOMC members. In March, the median FOMC member thought that 50 bps of rate cuts by the end of 2025 would be appropriate (Figure 5). While we would not be surprised to see the median dot for this year remain unchanged, we believe it is more likely that median dot will shift higher to indicate only 25 bps of easing before the end of the year. As discussed earlier, the Fed speak does not suggest the FOMC is in any hurry to cut rates at its next few meetings, and it would take only two dots moving up to change the median from 50 bps to 25 bps. That said, we think a meaningful number of members will continue to judge that 50 bps of policy easing by the end of 2025 would be appropriate. In the March dot plot, nine Committee members judged that 50 bps of rate cuts would be appropriate by the end of this year, while two members chose 75 bps of policy easing.

The dots for 2026 are more dispersed, as is typical for longer-dated forecasts. In March, nine FOMC members, which included the median, judged that a cumulative easing of 100 bps from the target range for the federal funds rate at that time would be appropriate by year-end 2026. We anticipate the median dot for next year to shift up 25 bps to 3.625%. If realized, that shift would signal 75 bps of cumulative easing by the end of next year. Like the 2025 dot, we see the risks to this view as skewed toward the 2026 median projection remaining unchanged at 3.375%.

The slightly higher expectations for the fed funds rate indicated by the dot plot are likely to come as FOMC participants see inflation deviating further from target this year. While some policymakers assumed higher tariffs in their 2025 inflation projections in the March SEP, a number of officials have noted in their public comments that changes to tariffs have generally been larger than they expected. Thus, we would expect to see the median projections for both headline and core PCE inflation in 2025 to move a few tenths higher in the June SEP, to 3.0% and 3.1%, respectively (Figure 6). In contrast, GDP projections for 2025 are likely to be revised down to just a little over 1%. Not only are the changes to trade policy and lingering uncertainty challenging for growth in the coming months, but the 0.2% annualized decline in Q1 GDP has created a tough starting point for growth this year. Yet, we expect the median estimate for the unemployment rate to remain unchanged at 4.4%, as slower growth in the labor supply and an ongoing reluctance to cut workers keeps the jobless rate from moving much beyond the Committee’s estimates for full employment.

{kind=link}