Forex markets remained trapped within yesterday’s ranges as investors struggled to find fresh conviction amid conflicting signals surrounding the US-Iran conflict. While there was some brief improvement in risk sentiment after US President Donald Trump said Washington was in the “final stages” of negotiations with Iran, optimism faded quickly as no concrete breakthrough emerged from either side officially.

But the optimism faded quickly after Reuters reported that Iran’s supreme leader Mojtaba Khamenei had directed officials to keep enriched uranium inside the country — a move likely to complicate any final agreement substantially.

The oil market remains the key macro driver. International Energy Agency Executive Director Fatih Birol warned on Thursday that global oil markets could soon enter a “red zone” during July or August if the Strait of Hormuz is not fully reopened before summer demand accelerates.

According to Birol, the IEA has already been injecting roughly 2.5 to 3 million barrels per day from strategic reserves to offset supply disruptions, but stressed that emergency stockpiles “are not endless.” With commercial inventories already declining rapidly and global demand set to rise during the northern hemisphere travel season, concerns are shifting away from pure geopolitical risk pricing toward fears of outright physical supply tightness.

Those concerns continued capping broader risk appetite across markets. Brent crude climbed back above %106 after earlier declines, while US 10-year Treasury yield rebounded to 4.60%, keeping financial conditions tight globally. Gold also softened again and drifted back toward the 4,500 area.

In currency markets, Sterling is the strongest performer of the week so far as immediate fears surrounding UK politics and fiscal instability eased. Kiwi followed, while Dollar also stayed relatively firm amid elevated yields.

On the weaker side, Yen continued suffering under the weight of rising global yields, while Aussie is pressured after weak employment data reinforced expectations that the RBA will hold rates steady in June. Euro also underperformed following weak PMI data and lingering uncertainty over whether ECB tightening will continue near term.

The market’s problem now is credibility. Traders do not appear willing to fully trust optimistic geopolitical headlines unless they are accompanied by concrete progress on reopening the Strait of Hormuz and stabilizing physical oil supply. Until then, every temporary recovery in sentiment risks running into the same structural obstacle: tightening energy markets and rising global yields.

US initial jobless claims fall to 209k, labor market remains resilient

US weekly jobless claims stayed near low levels in May, reinforcing the view that the labor market remains resilient despite broader signs of slowing economic momentum. Read More.

GBP/CHF Rebounds as UK Fiscal Worst-Case Fears Fade, Head-and-Shoulders Bottom Forming?

Sterling rebounded as markets stepped back from pricing a UK fiscal crisis after Andy Burnham reassured investors on fiscal discipline, while GBP/CHF began forming a potential bullish reversal pattern. Read More.

UK PMI Composite Falls Into Contraction as BoE Faces “Major Quandary”

UK business activity fell back into contraction in May as collapsing services demand, rising energy costs, and growing political uncertainty left the Bank of England facing a “major quandary.” Read More.

Eurozone PMI Composite Falls to 31-Month Low, Signals -0.2% Q2 GDP Contraction

Eurozone business activity deteriorated sharply in May as the Composite PMI fell to a 31-month low, with survey data signaling a potential 0.2% contraction in Q2 GDP amid deepening energy-shock pressures. Read More.

Aussie Rebound Runs Into Domestic Reality as Weak Jobs Lock In RBA June Hold

AUD/USD’s relief rally faded quickly after weak Australian jobs data effectively locked in an RBA hold for June, reinforcing concerns that cracks are forming in the domestic economy. Read More.

Australia Employment Unexpectedly Contracts as Unemployment Rate Jumps to 4.5%

Australia’s labor market weakened sharply in April as employment unexpectedly contracted and unemployment jumped to 4.5%, strengthening expectations that the RBA will stay cautious near term. Read More.

Australia PMIs Fall Back Into Contraction as Demand and Confidence Deteriorate

Australia’s private sector fell back into contraction in May as weakening demand, softer hiring, and elevated energy costs pushed business confidence toward pandemic-era lows. Read More.

BoJ’s Koeda Says Oil-Driven Inflation Risks Could Justify Further Rate Hikes

BoJ board member Junko Koeda warned the Middle East oil shock could push Japan’s underlying inflation above target, strengthening the case for further rate hikes as early as June. Read More.

Japan PMI Growth Slows as Manufacturing Strength Offsets Stagnating Services Sector

Japan’s economic expansion slowed in May as services activity stagnated and cost pressures surged, though manufacturing continued benefiting from stockpiling tied to Middle East supply disruptions. Read More.

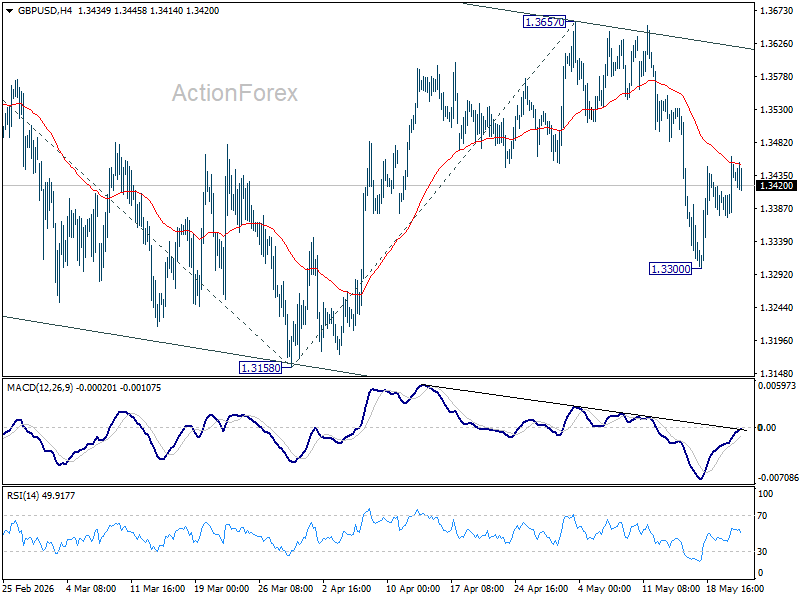

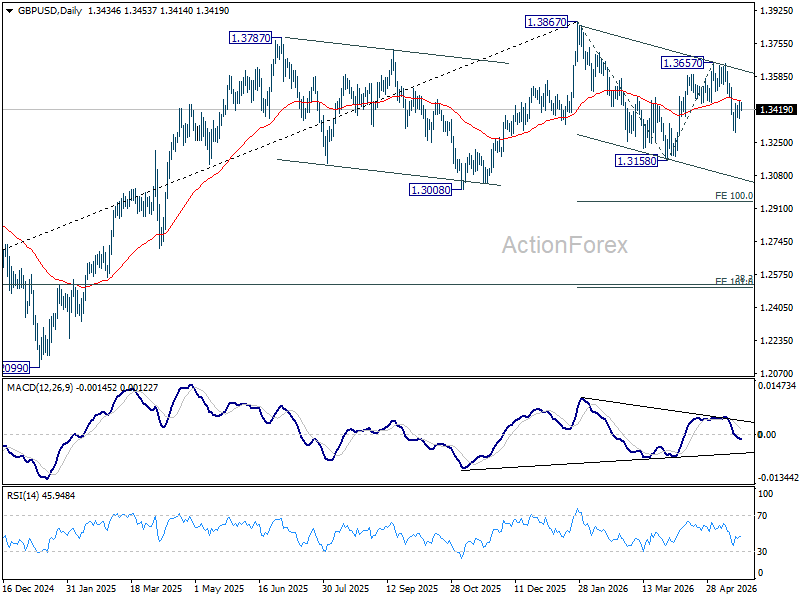

GBP/USD Daily Outlook

No change in GBP/USD’s outlook and intraday bias stays neutral. Further fall is expected as long as 55 4H EMA (now at 1.3450 holds. Below 1.3300 will target a retest on 1.3158 support first. However, sustained break of the EMA will dampen the bearish case and turn bias back to the upside for 1.3657 resistance instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

{kind=link}