Summary

- As was widely expected, the FOMC lowered the fed funds target range by 25 bps to 3.75%-4.00% at the conclusion of its October meeting. Yet, Chair Powell made clear that additional easing in December was far from assured.

- The post-meeting statement gave a nod to the more limited slate of data the FOMC was able to take into account over the past month due to the government shutdown. The Committee did, however, suggest that its concern about the labor market did not worsen over the inter-meeting period.

- October’s policy rate decision was not unanimous. Governor Miran dissented in favor of a steeper 50 bps rate cut while Kansas City Fed President Schmid dissented the opposite direction in favor of holding the fed funds rate steady.

- The divergent dissents are not wholly surprising given elevated inflation and flagging job growth have created some tension between the Committee’s price and employment objectives. But with the jobs market outlook not obviously worsening over the past month, inflation still stubbornly above target, and policy now closer to neutral, the bar to another cut in December is higher.

- Our base case remains for the FOMC to reduce the fed funds rate by another 25 bps at its December meeting. That said, with finely balanced risks around the inflation and employment objectives, a deluge of data on the other side of the shutdown could quickly shift the outlook and our expectations for the December meeting. Chair Powell does not think it is a slam dunk decision, and neither do we.

- Notably, the FOMC announced that quantitative tightening would come to an end on December 1. This was one month sooner than our long-standing forecast, although in the grand scheme of the Fed’s $6.6 trillion balance sheet, the one-month shortening of the roughly $20 billion monthly runoff will not have a material impact on longer-term yields, in our view.

FOMC Delivers October Cut, But the Bar is Higher for December

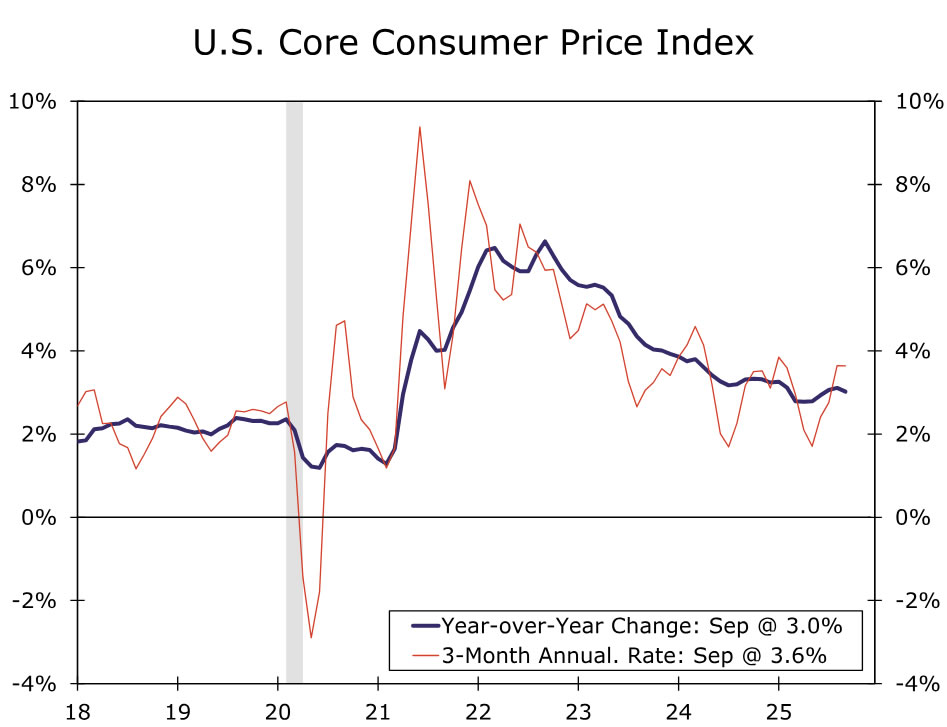

As was widely expected, the FOMC reduced the target range of the fed funds rate by 25 bps points to 3.75%-4.00% at the conclusion of its October meeting. The decision comes under odd circumstances. The ongoing government shutdown has deprived the Committee of key data used to inform its view of the economy. The belatedly-released September CPI report showed inflation still stuck around a 3% pace (chart), but the Producer Price Index has not been published, leaving a less complete picture of recent inflation than the FOMC would have ordinarily. Furthermore, while the Committee has grown more concerned about the state of the labor market the past few months, it did not receive data on nonfarm payrolls and the unemployment rate for September. What data have become available since the Committee last gathered continue to paint a picture of anemic hiring but low layoffs, keeping the jobs market in a delicate spot.

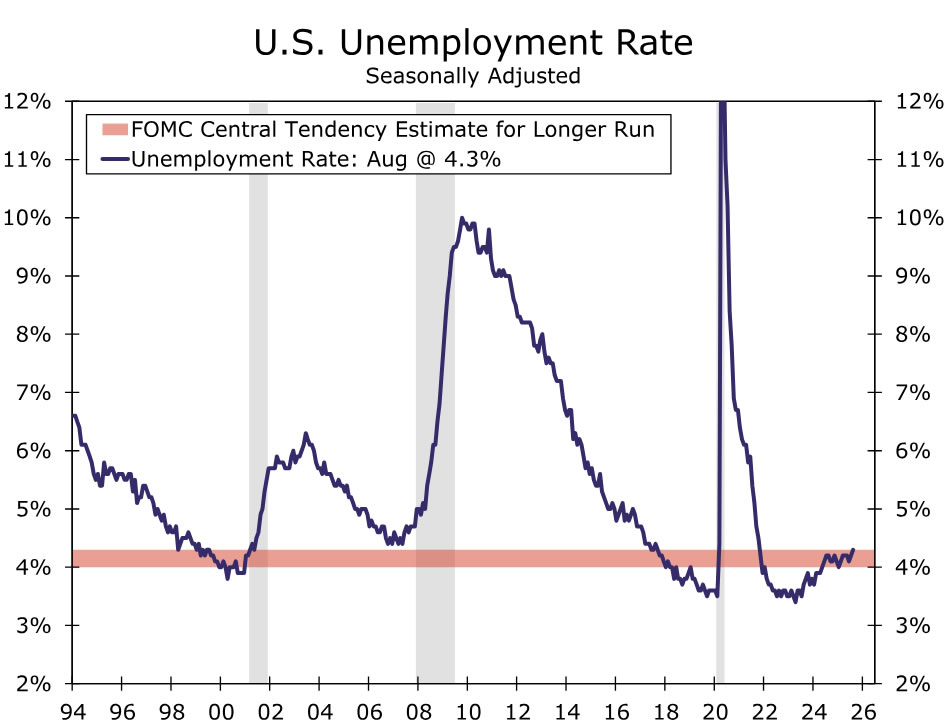

In a nod to the government shutdown affecting the data flow, the post-meeting policy statement said that “Available indicators suggest that economic activity has been expanding at a moderate pace” versus previously mentioning that activity had “moderated in the first half of the year.” It further noted that recent private sector readings on the jobs market looked consistent with the slowdown in payroll growth and uptick in unemployment since the start of the year (chart).

However, concern about the jobs market does not appear to have increased further over the inter-meeting period. In the Committee’s previous post-meeting statement, it noted that the downside risks to employment “have risen”, yet today’s statement read that those risks merely “rose in recent months.” Similarly, the statement hinted that the FOMC does not see the current state of inflation as having worsened since mid-September; it said that “inflation has moved up since earlier this year”, with the timing reference new.

Notably, today’s rate decision was not unanimous. Governor Miran once again dissented in favor of a 50 bps rate cut. At the same time, Kansas City Federal President Schmid dissented in favor of keeping the target range unchanged. Dissents in both the hawkish and dovish direction speak to the difficult position the FOMC finds itself in at this juncture. Not only has visibility on the economy become more limited with the shutdown, but elevated inflation and flagging job growth have created some tension between the Committee’s price and employment objectives.

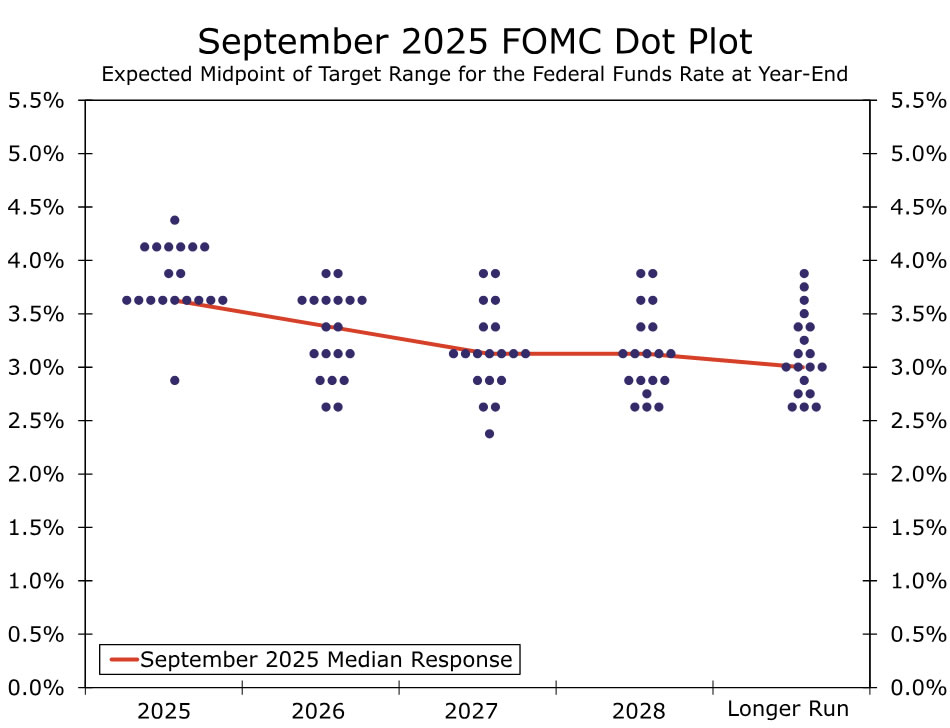

Together, the subtle statement changes and two-sided dissents suggest the bar for another cut at the December meeting is getting higher. That message was made even more clear in the post-meeting press conference. In his opening remarks, Chair Powell shared that “A further reduction in the policy rate at the December meeting is not a foregone conclusion. Far from it. Policy is not on a preset course.” The September Summary of Economic Projections already showed the Committee closely split between three 25 bps or fewer cuts this year (chart). With the policy rate closer to neutral, risks to the jobs market not obviously having worsened and inflation still stubbornly above target, the case for a third consecutive reduction in the policy rate has become less straightforward.

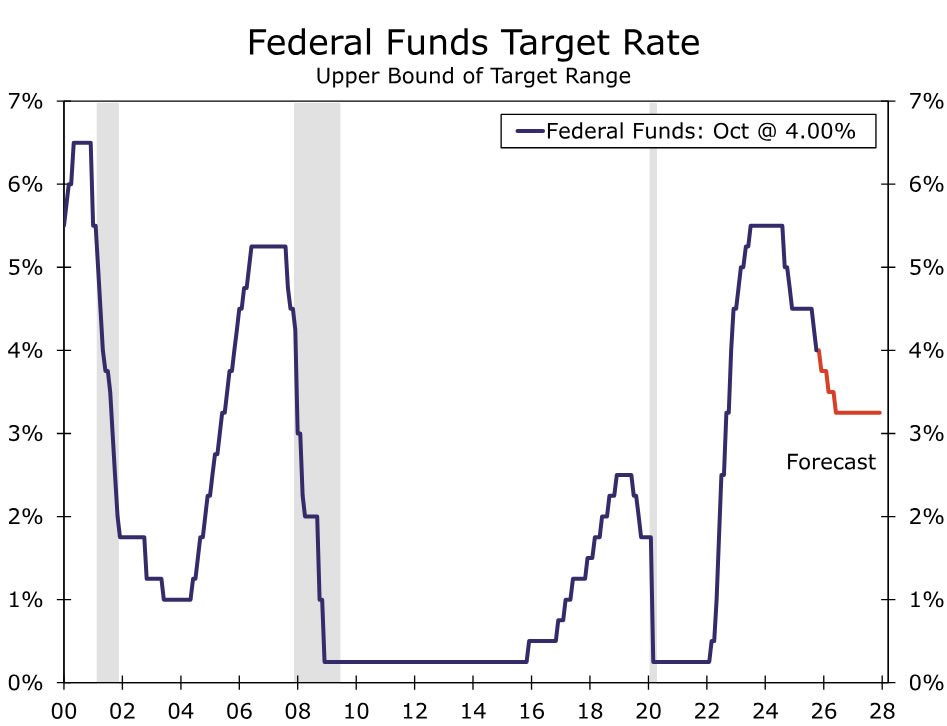

Our base case remains for the FOMC to reduce the fed funds rate by another 25 bps at its December meeting (chart). That said, with finely balanced risks around the inflation and employment objectives, a deluge of data on the other side of the shutdown could quickly shift the outlook and our expectations for the December meeting. Chair Powell does not think it is a slam dunk decision, and neither do we.

Balance Sheet Runoff to End December 1

The FOMC also announced today that its balance sheet runoff would end on December 1. This was one month sooner than our forecast, although in the grand scheme of the Fed’s $6.6 trillion balance sheet, a one month shortening of the roughly $20 billion monthly runoff will not have a material impact on longer-term yields, in our view. Runoff of mortgage-backed securities will continue indefinitely, with the proceeds plowed into Treasury bills one-for-one such that the total size of the central bank’s balance sheet is left unchanged.

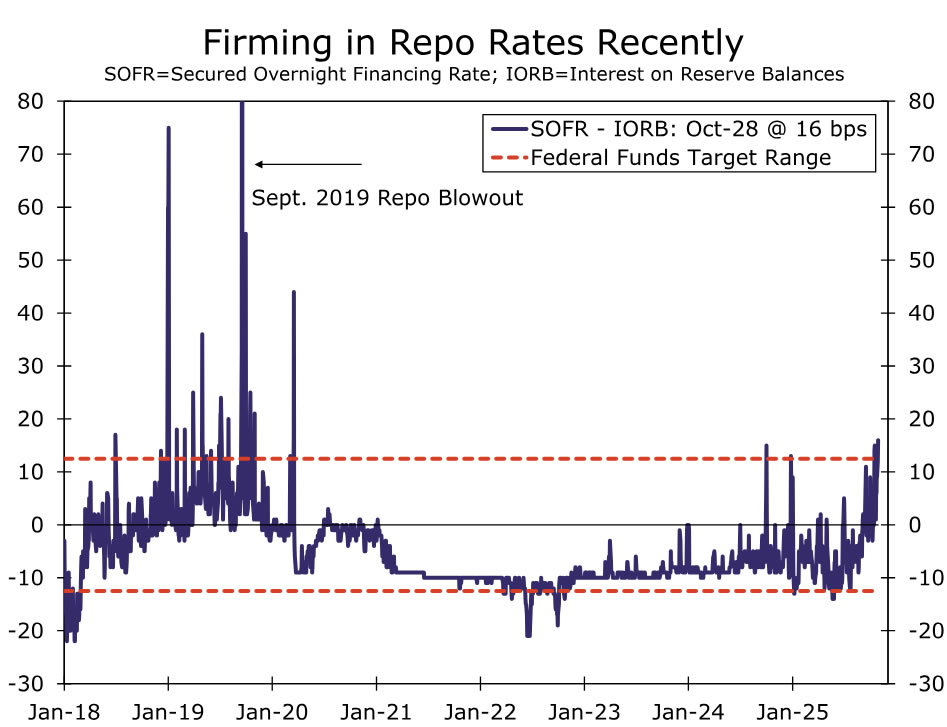

The end of runoff comes at a time when money market rates have been rising in a sign that bank reserves are becoming less abundant (chart). The next phase of the Fed’s balance sheet evolution will entail the central bank keeping its security holdings flat and monitoring carefully for the optimal equilibrium. It is important to note that even if aggregate balance sheet runoff ceases, that does not mean that balance sheet policy has shifted to neutral. If the Fed’s balance sheet is held flat for an extended period of time, then it will still be shrinking as a share of GDP. Bank reserves will continue to decline gradually and in proportion to the growth in non-reserve liabilities on the Fed’s balance sheet, such as currency in circulation.

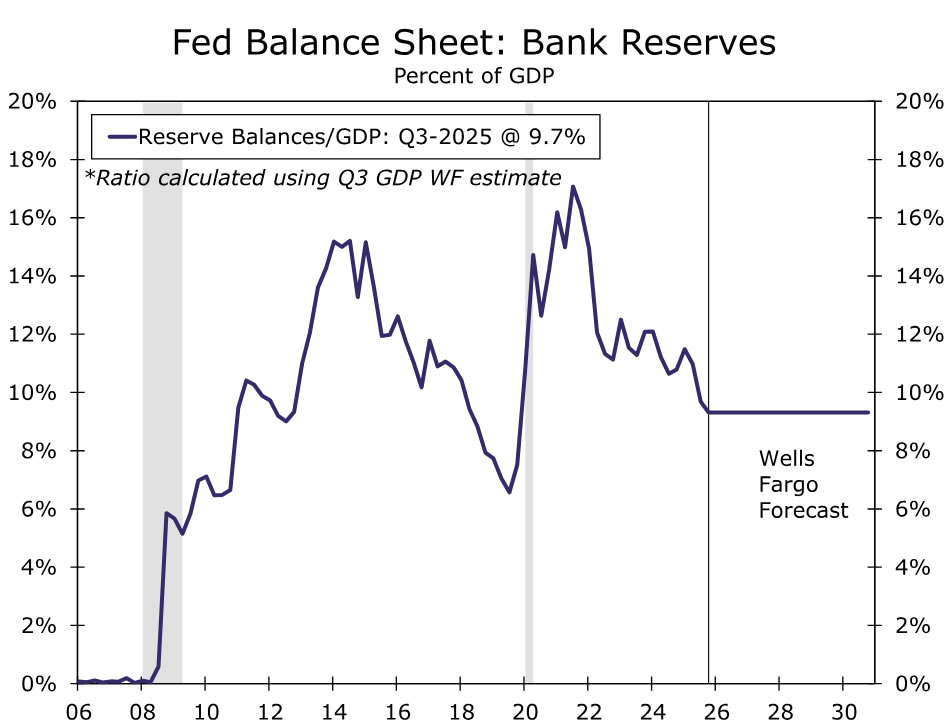

Thus, eventually the Fed’s balance sheet will need to resume growing again to prevent bank reserves from falling below the “ample” threshold. Our base case is that these reserve management purchases will begin in April 2026 and average approximately $25 billion per month, with purchases concentrated entirely in Treasury bills. If realized, this should be enough to keep the reserves-to-GDP ratio a little bit above 9%, a key threshold we and others have highlighted previously as a demarcation line between ample and abundant reserves (chart).

{kind=link}