{kind=link}

We expect the Canadian economy grew an annualized 0.5% in Q3—a partial reversal of the 1.6% decline in Q2 when international trade disruptions plunged exports lower.

Next Friday’s Q3 gross domestic product appears backloaded with (what we expect will be) a 0.3% bounce-back in September after a surprise 0.3% contraction in August. That is firmer than the 0.1% preliminary estimate from Statistics Canada, but consistent with further acceleration in growth in Q4.

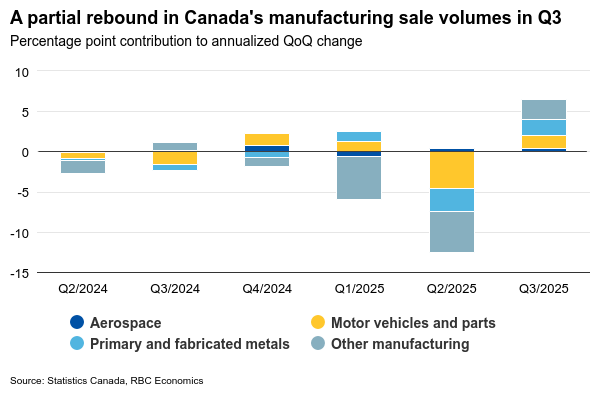

Heavily trade exposed industries continued to broadly underperform in Q3, but have shown further signs of stabilization. Manufacturing and wholesale sales volumes rebounded by an annualized 6 ½ % in Q3 to partially reverse large declines (-11.7% and -9%, respectively) in Q2.

Offsetting weakness in the trade exposed sectors is domestic Canadian demand that has remained relatively resilient so far. Business investment likely contracted in Q3, but our tracking of RBC card transactions points to further, albeit slower growth in consumer spending after a large increase in Q2. Residential investment is expected to have risen again in Q3 as well, following a gradual pick-up in home resales since March.

Net international trade data through August is on pace to add slightly to growth in Q3 after record subtraction from Q2 GDP (outside 2020 pandemic lockdowns) when exports plunged on lower shipments to the United States.

Missing September trade data could lead to revisions

Canadian international trade data for September is still missing. Statistics Canada relies on U.S. Census Bureau for information on Canadian exports to the U.S. that has been delayed by the six-week U.S. government shutdown. It’s, therefore, likely the quarterly Canadian trade data in the GDP add-up will include imputations, and could see larger-than-normal revisions in the future.

Overall, early indicators for monthly September GDP have been positive. Manufacturing sales volume jumped 2.7%—the largest one-month increase since January 2023. Oil production increased almost 3% in September by our estimates, and is on track to add positively to Q3 GDP growth after wildfires and maintenance related disruptions dampened oil sands production in Q2.

Air transportation also contributed to GDP growth in September after a strike in August temporarily weighed on output. Soft spots for growth in September include retail sales volume which pulled back 0.8%, and mining output (ex-oil & gas) that by our count edged lower for a second straight month.

Week ahead data watch:

September Survey of Employment, Payrolls and Hours data on Thursday should show moderation in declining job vacancies, following recent stabilization in timelier Indeed job openings data. Wage growth is expected to have further unwound, and the employment details will be closely watched for more signs of tariff impact among most targeted Canadian manufacturing sub-industries.

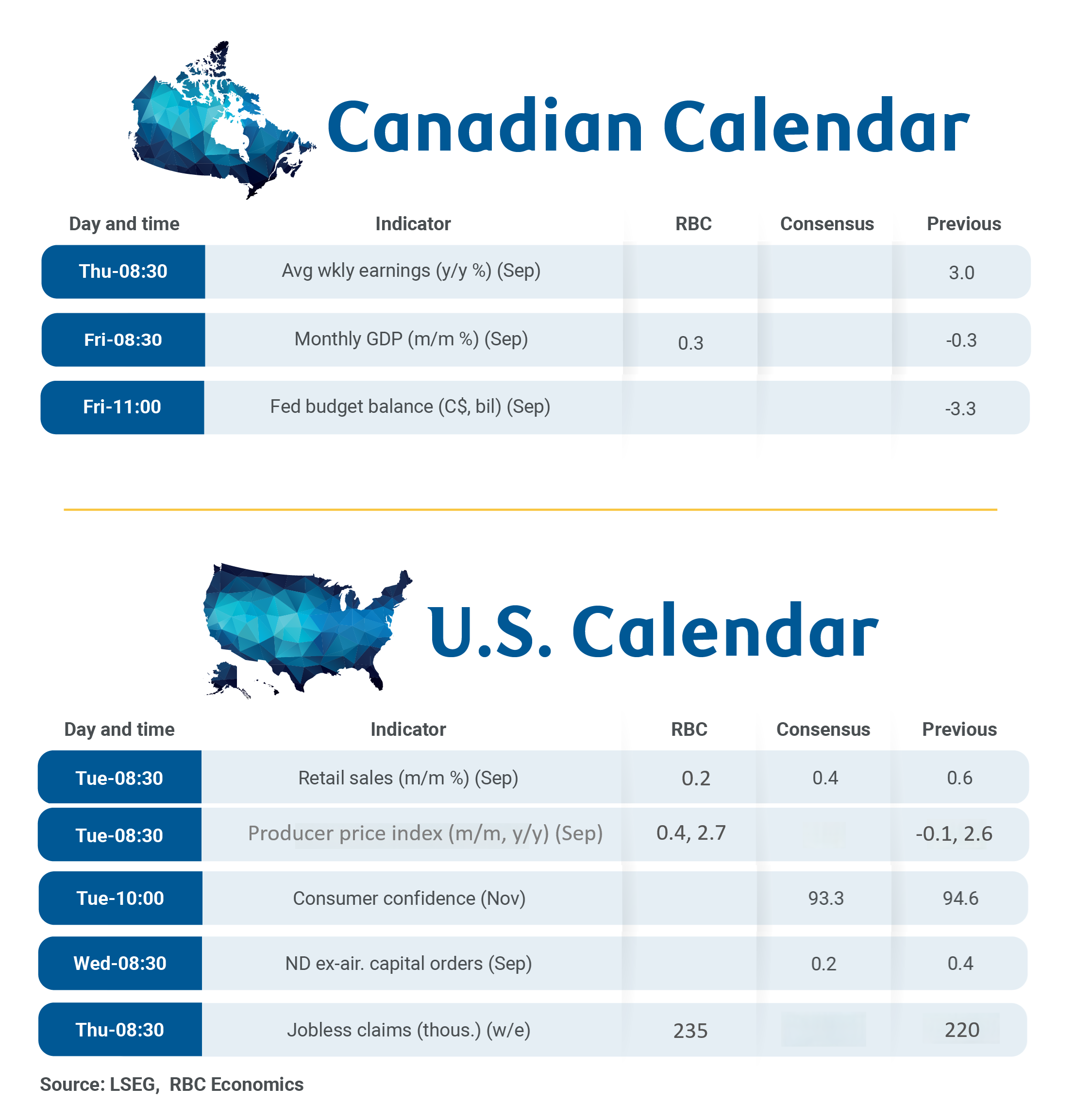

The end of the U.S. government shutdown will see a gradual return of economic data releases in the coming weeks. We expect next week’s retail sales will show a 0.2% in September and a smaller 0.1% rise in core sales. Producer price index is expected to have risen 0.4% in September, led by goods as tariff impact continue to flow through gradually. Core PPI is expected to have risen 0.3% in the same month.