{kind=link}

- Flurry of US data to test dovish Fed expectations as next meeting looms.

- ISM PMIs, ADP employment and PCE inflation may yet upset rate cut hopes.

- Eurozone CPI, Australian GDP, Canadian employment also on tap.

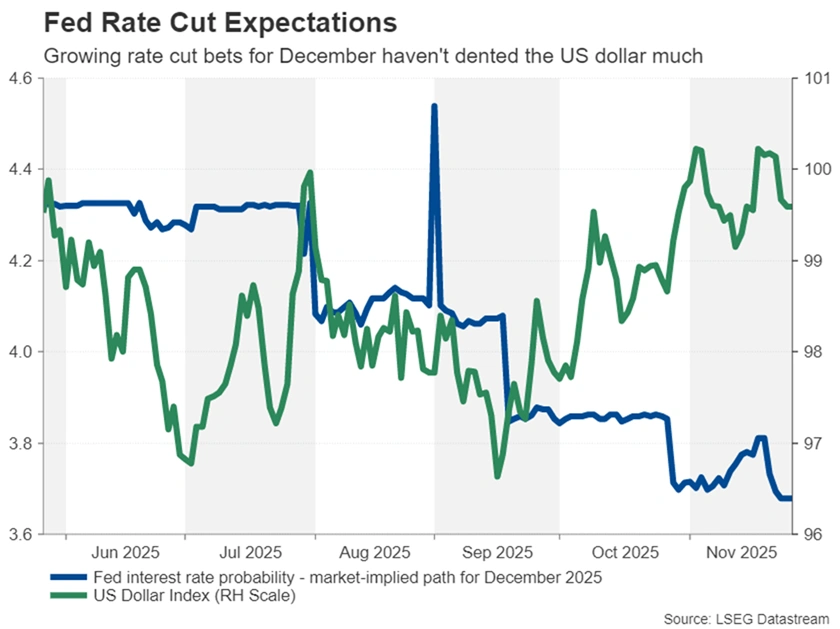

December rate cut not a done deal yet

After a string of hawkish remarks by numerous Fed speakers, the doves made a comeback during the past 10 days, putting a rate cut at the December meeting back on the table. This lifted the odds of a 25-bps reduction on December 10 from around a quarter to almost 80%, in a dramatic reversal that reverberated across financial markets. Treasury yields sank, the US dollar not so much, but risk assets were propelled higher, with Wall Street and cryptocurrencies in particular recouping a chunk of their November losses.

This sudden turnaround wasn’t just on the basis of two new doves joining the rate-cut bandwagon, most notably one of them being influential New York Fed chief John Williams. The more recent data has raised fresh question marks about the strength of the US economy.

However, Chair Powell’s argument that policymakers won’t have access to the latest labour market and inflation indicators in time for the December policy decision still stands. In light of the missing and somewhat conflicting data, next week’s releases will be monitored very closely, as there’s plenty on the calendar that could push the odds either back towards 50% or closer to 100%.

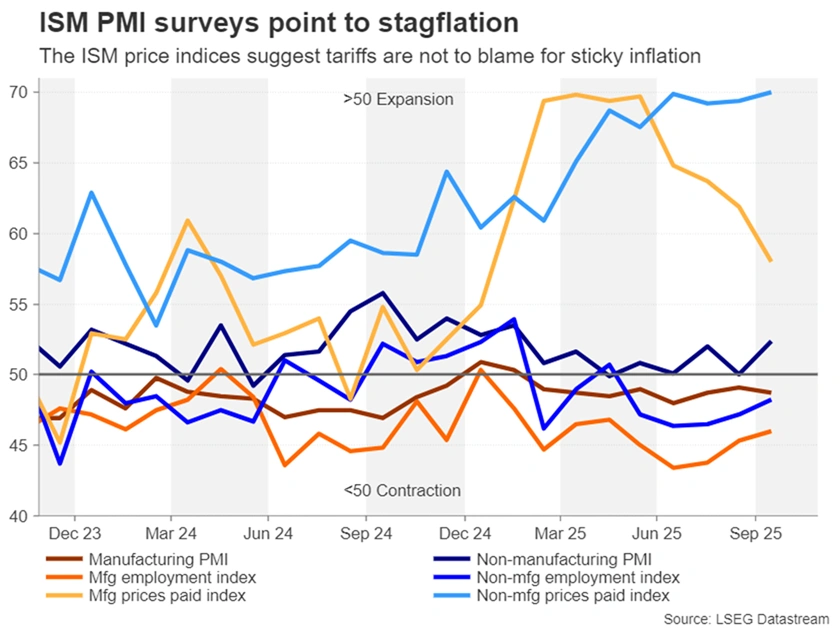

Will the ISM PMIs pose a stagflation dilemma?

First on the agenda is the ISM manufacturing PMI for November on Monday. The services PMI is released a couple of days later. The US manufacturing sector has been contracting since March according to the ISM survey, amid the tariff-related uncertainty and possible retaliatory backlash against American goods from international buyers.

Employment has also been declining, with the sub-index printing below 50 since February. However, the price index has plunged from close to 70.0 to 58.0 in October, casting doubt on the claim that tariffs have been inflationary. What’s worrying, though, is that the equivalent gauge for the services sector has stayed elevated near 70.0, suggesting that domestic price pressures are to blame for the country’s inflation rate being stuck within the 3.0% vicinity.

The overall PMI for services edged up to 52.4 in October, helped by a jump in new orders, while the manufacturing PMI declined to 48.7. Another healthy rise in services activity in November would bolster the hawks at the Fed, whereas a sudden drop to 50.0 or lower would back the case for an immediate rate cut.

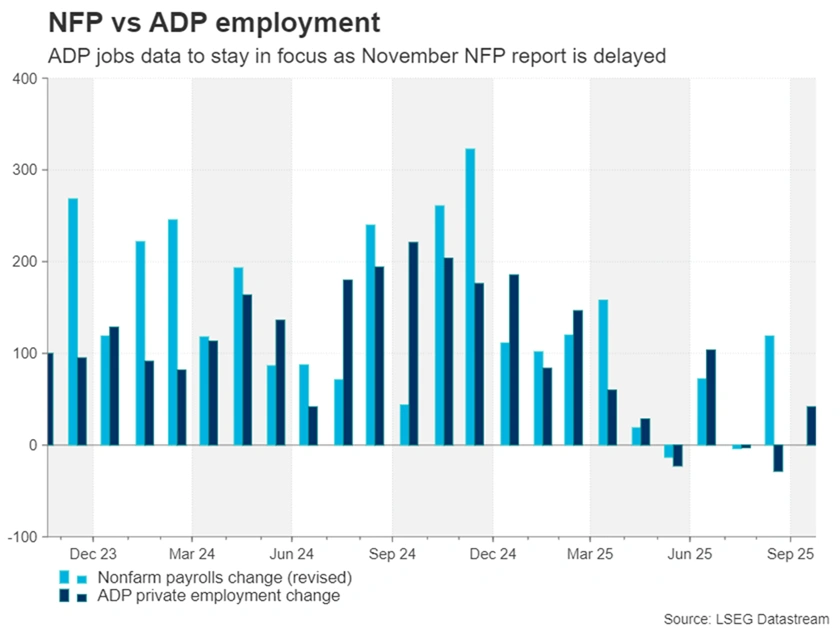

ADP in focus as November NFP delayed

Just as important will be Wednesday’s ADP employment report. The official November payrolls report isn’t due until December 16, and with the October one cancelled, the ADP’s employment survey for the private sector will offer a vital update on the labour market. In October, there were 42k jobs added, which was more than expected. As with the ISM PMIs, any surprises in either direction pose a symmetrical risk to easing expectations, as well as the US dollar.

More jobs data will follow on Thursday with the Challenger Layoffs. Even though most Fed officials haven’t sounded too worried about the recent round of job-cut announcements, any jump in layoff numbers in November could fuel concerns that the US labour market is in trouble.

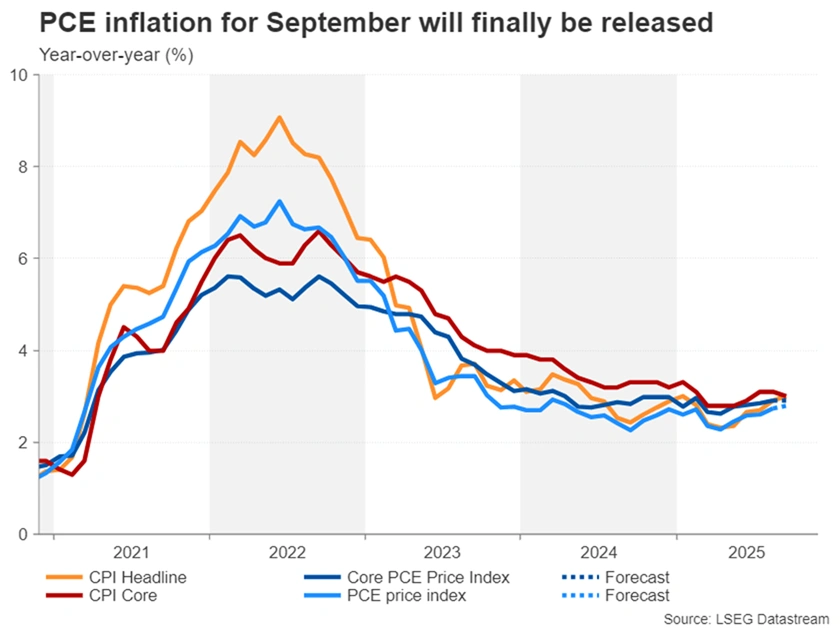

September PCE inflation might not matter

Moving to Friday, the focus will shift to the PCE inflation and personal consumption indicators for September. Although the Fed will be more eager to see the November stats, whose release date hasn’t been confirmed yet, the September report will still be watched for some guidance, especially if the incoming data continues to give mixed messages on the state of the economy.

Headline PCE is forecast to have inched up to 2.8% y/y in September from 2.7%, while the all-important core PCE price index is projected to have stayed unchanged at 2.9% y/y.

Other releases will include industrial production on Wednesday, and factory orders and the University of Michigan’s preliminary consumer sentiment survey on Friday.

Should December rate cut bets take a hit from a broadly strong set of figures, Wall Street’s rebound would be put at risk, potentially dashing hopes of a Santa rally this year, at least before the Fed meeting.

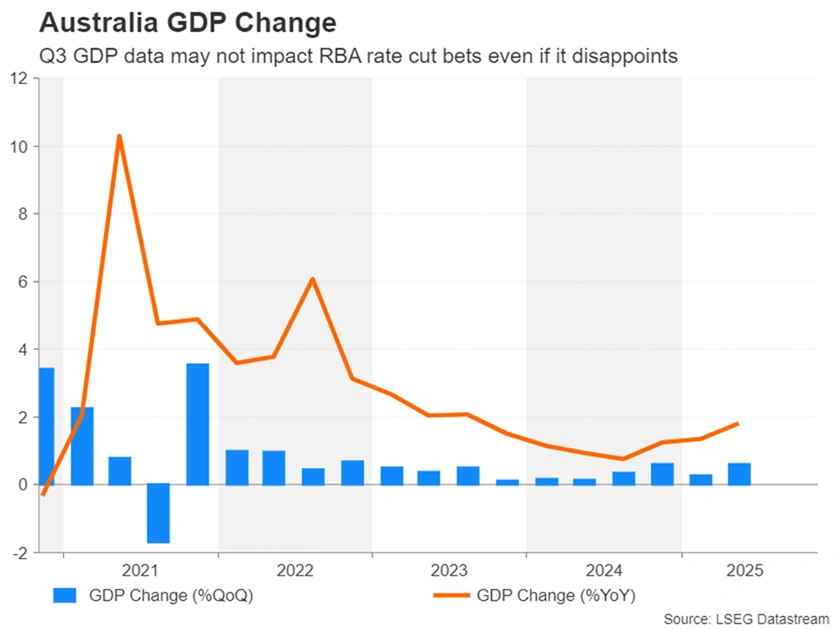

Aussie might shrug off GDP data

In Australia, the latest inflation readings couldn’t have been more decisive for the Reserve Bank of Australia where rate cut expectations have completely evaporated. The consumer price index rose by a more than-forecast 3.8% y/y in October, well above the RBA’s upper target band of 3.0%.

Combined with signs of a recovery in the labour market, there’s very little prospect of the RBA trimming rates again anytime soon. Hence, Wednesday’s GDP figures for the third quarter are unlikely to alter those expectations much even if they disappoint.

The Australian dollar will probably shrug off the growth data and will instead be driven by global risk sentiment, as well as by PMI numbers out of China on Sunday (official government), Monday (S&P Global manufacturing) and Wednesday (S&P Global services).

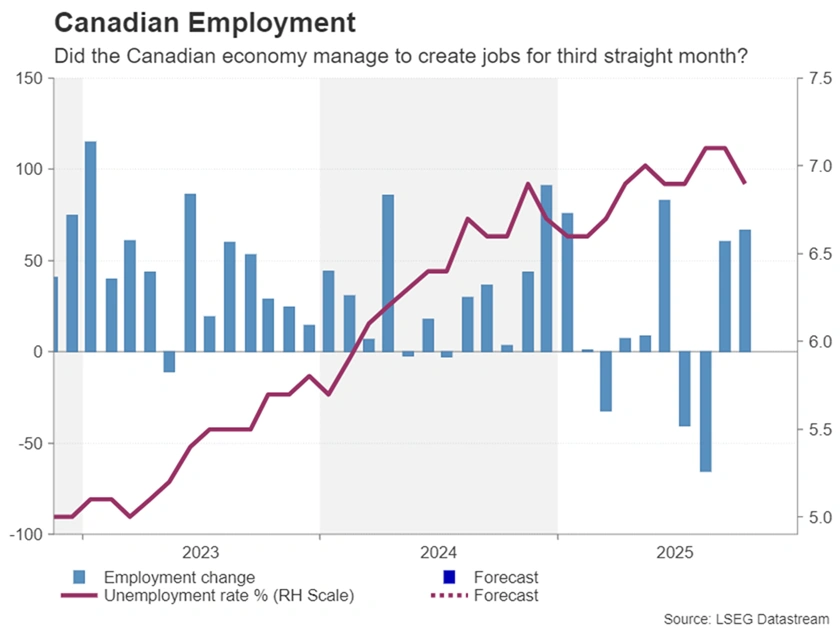

Loonie bulls hoping for jobs lift

The Bank of Canada is another central bank that’s had to adopt a more neutral tone lately. Although the Canadian economy continues to reel from President Trump’s tariffs, employment conditions appear to be stabilizing and underlying inflation measures remain sticky.

Yet, in the absence of Washington and Ottawa striking a trade agreement over the next few months, further rate cuts cannot be ruled out. But the bar is high as the BoC has already slashed rates to 2.25% so policymakers are likely preserving some firepower for a rainier day.

Along with inflation, the labour market will be key for the BoC in determining the need for additional easing. If Friday’s employment numbers show that the economy added jobs for the third month in a row, expectations of a 25-bps reduction will probably fade further, boosting the Canadian dollar.

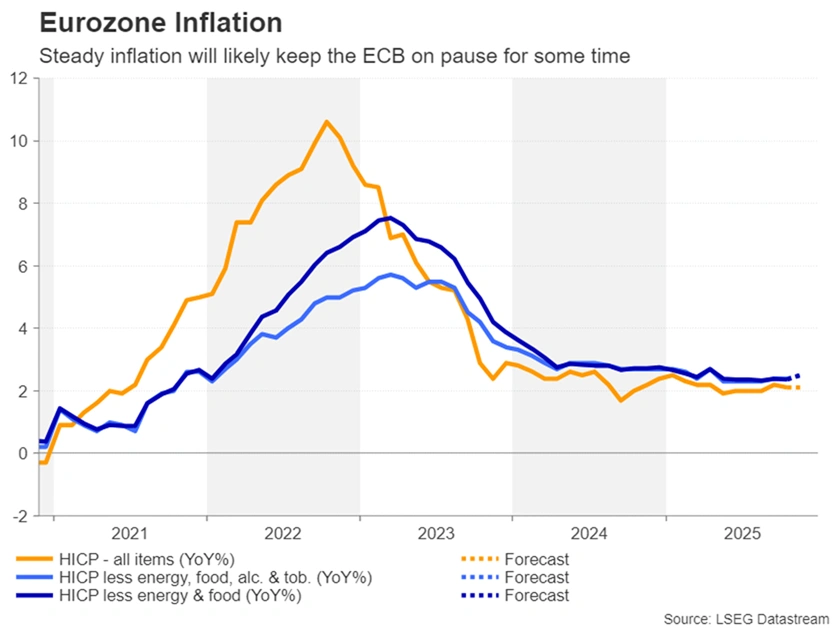

Eurozone CPI could be a non-event

Inflation is a lesser concern in the Eurozone where the European Central Bank has no plans to adjust policy anytime soon. The data backs the ECB’s firmly neutral stance.

The headline rate of CPI has been hovering around 2.0% since spring. The flash estimates for November due on Tuesday are expected to maintain the flat picture, with headline CPI holding steady at 2.1%. On Friday, no change is anticipated in revised estimates of Q3 GDP when the economy expanded by 0.2% q/q.

German industrial orders and French industrial production might also move the euro on Friday. But on the whole, Fed policy and US-EU trade relations will be a bigger driver for the single currency in the short-to-medium term.

Yen and Oil in search for a boost

In contrast, the dollar/yen pair is expected to remain somewhat more volatile, where the diverging monetary policies of the Fed and Bank of Japan are not quite having the desired effect. Although the yen has steadied over the past week following increased Fed easing bets and some unexpectedly hawkish comments from BoJ policymakers, it’s still trapped within the intervention zone.

Monday’s revised capital expenditure figures for Q3 out of Japan and Friday’s household spending numbers for October could provide some additional support to the yen if they bolster the odds of a December rate hike.

Finally, OPEC+ countries are widely anticipated to keep production quotas unchanged on Sunday, reaffirming their decision to pause output increases during the first three months of 2026. Oil traders will therefore likely be paying more attention to any updates on the Trump administration’s efforts to get Ukraine and Russia to agree to a peace plan.