{kind=link}

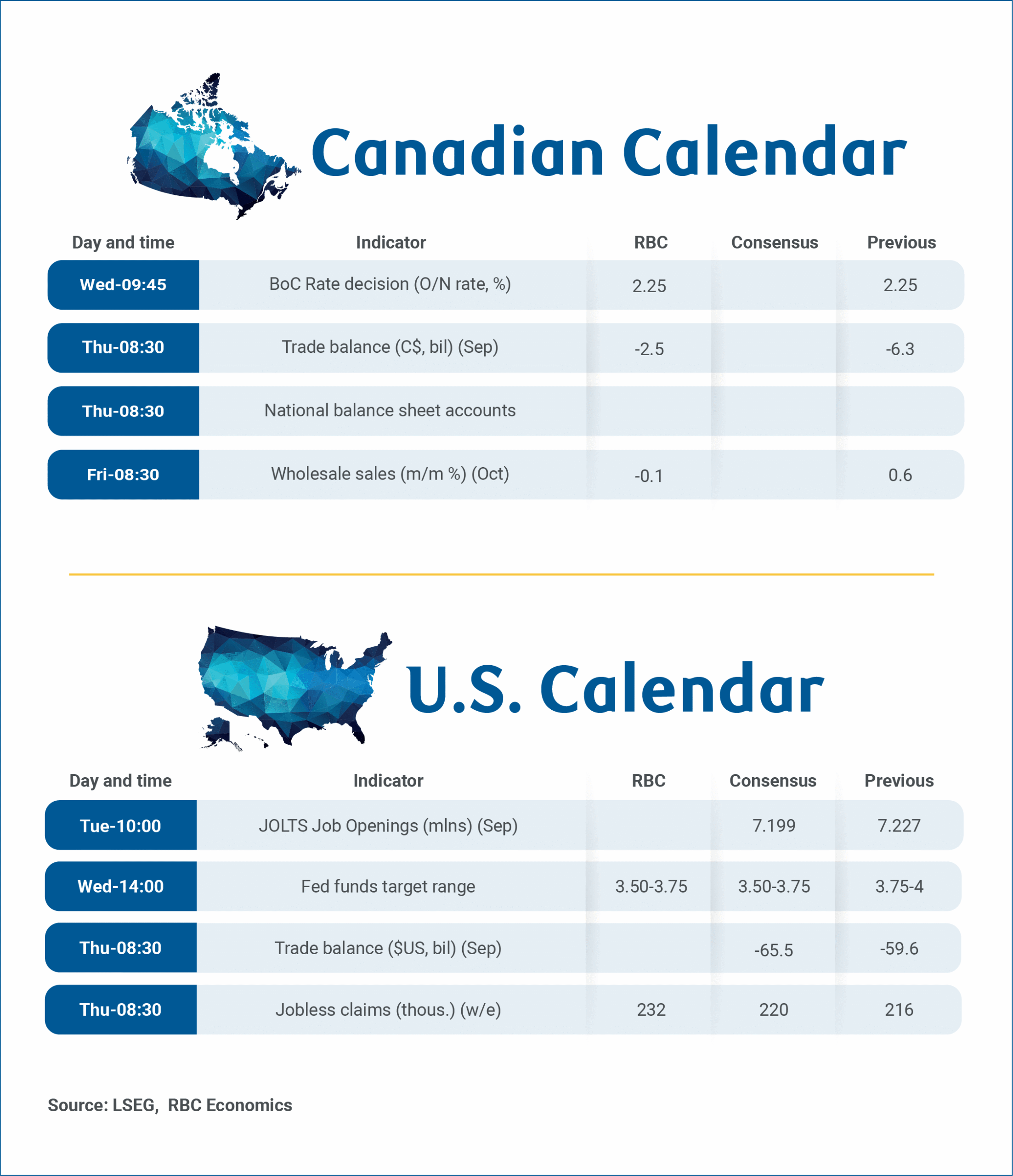

Dual central bank interest rate decisions from the U.S. Federal Reserve and the Bank of Canada on Wednesday top the week’s calendar, with the BoC expected to hold rates, while a third consecutive 25 basis point cut from the Fed looks highly likely.

Our base case forecast a month ago did not assume a December cut from the Fed, given inflation in the U.S. remains above the central bank’s 2% target, and Chair Jerome Powell’s comments at the last meeting about cautiously proceeding in a foggy environment.

However, with an unusually divided FOMC committee, next week’s decision was always going to be a very close call. Fed communication over the last few weeks has also been leaning in the direction of a cut. With some softer data during the blackout, we doubt the hawks will put up a major fight.

A hold by the BoC in comparison should be relatively uncontroversial. After October’s rate cut, policymakers signaled that “the current policy rate is about the right level” to deliver low, steady inflation while supporting growth through uncertainty.

Delayed September Canadian trade data next week would need to show a 3.4% increase in merchandize export volume from August, and a 3.1% decrease in goods import volume in order to match the details in the third quarter GDP data from last week.

More important still are the trade details from U.S. census bureau on whether CUSMA exemptions have continued to hold up to support Canadian exports to the U.S. in September.

How the labour market plays into the BoC decision

BoC’s holding bias was contingent on the central bank’s forecast for soft but positive economic growth. Gross domestic product growth in Q3 surprised on the upside with a 2.6% annualized increase versus the BoC’s 0.5 % projection, with mixed details.

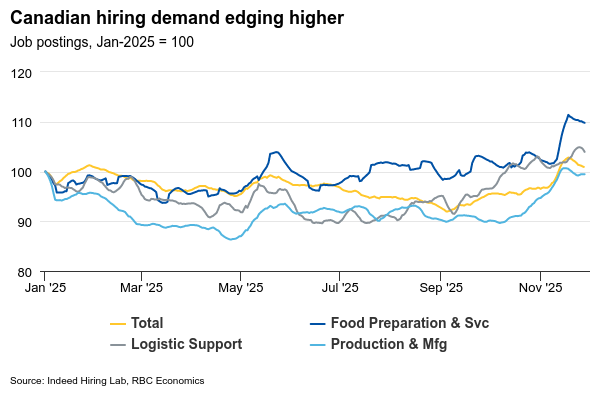

But labour markets have also shown more signs of stabilizing with employment rising 54,000 in November after already firm increases in September and October. The (less-volatile) unemployment rate dropped to 6.5% in November from 7.1% in September. Weakness still exists among tariff-exposed manufacturing sectors, but economy-wide layoffs have remained low.

As a result, household spending has broadly remained resilient this year despite a tick lower in Q3. Spending was, in part, supported by earlier BoC rate cuts that have reduced debt service pressures. Financial market gains have bolstered net worth, adding to aggregate purchasing power.

We expect those trends will have persisted in Q3, and next week’s national balance sheet data to show little changes in households’ debt service ratio from Q2 level that was already below 2019, and further gains in financial assets and net wealth.

Today, underlying inflation pressures are running above the BoC’s 2% inflation target, and could prove stickier than the central bank would like in the future thanks to stronger-than-expected consumer and government spending in 2026. Our base case assumes per-capita growth will slowly improve in 2026 with no additional interest rate cuts from the central bank.

Week ahead data watch:

The Q3 national balance sheet account details next Thursday should show rising household net worth with asset expansion outpacing growth in liabilities. Robust stock market gains in Q3 (the TSX index were up 11.8% and the S&P 500 up 10.3%) were partially offset by lower home equity given an 1.8% drop in home prices. Households’ debt service ratio is expected to remain little changed at 14.4%, as debt payments continued to rise at a similar pace as disposable income.

The release of September Canadian (and U.S.) international trade data delayed by the U.S. government shutdown should show a narrowing in the Canadian trade deficit. But the magnitude of the improvement will be watched closely after Statistics Canada needed to impose imputed placeholders on Canadian export data to compile the contribution of net trade to Canada’s Q3 GDP report. Most of a 3.1 percentage point (annualized rate) add to GDP growth in Q3 came from a pullback in imports that was not impacted by the U.S. shutdown. But the quarterly GDP data also implied a 3 1/2% increase in September merchandise export volumes.