{kind=link}

Week in review – The Debasement Trade shines again after the Fed Cut

Markets were salivating for the FOMC rate decision, and they got exactly what they wanted.

The Fed delivered a highly expected 25 bps cut on Wednesday, taking rates from the 3.75%-4.00% range down to 3.50%-3.75%, officially shutting the door on the 4% policy rate era.

While Chair Powell presented neutral remarks overall, investors interpreted them with optimism.

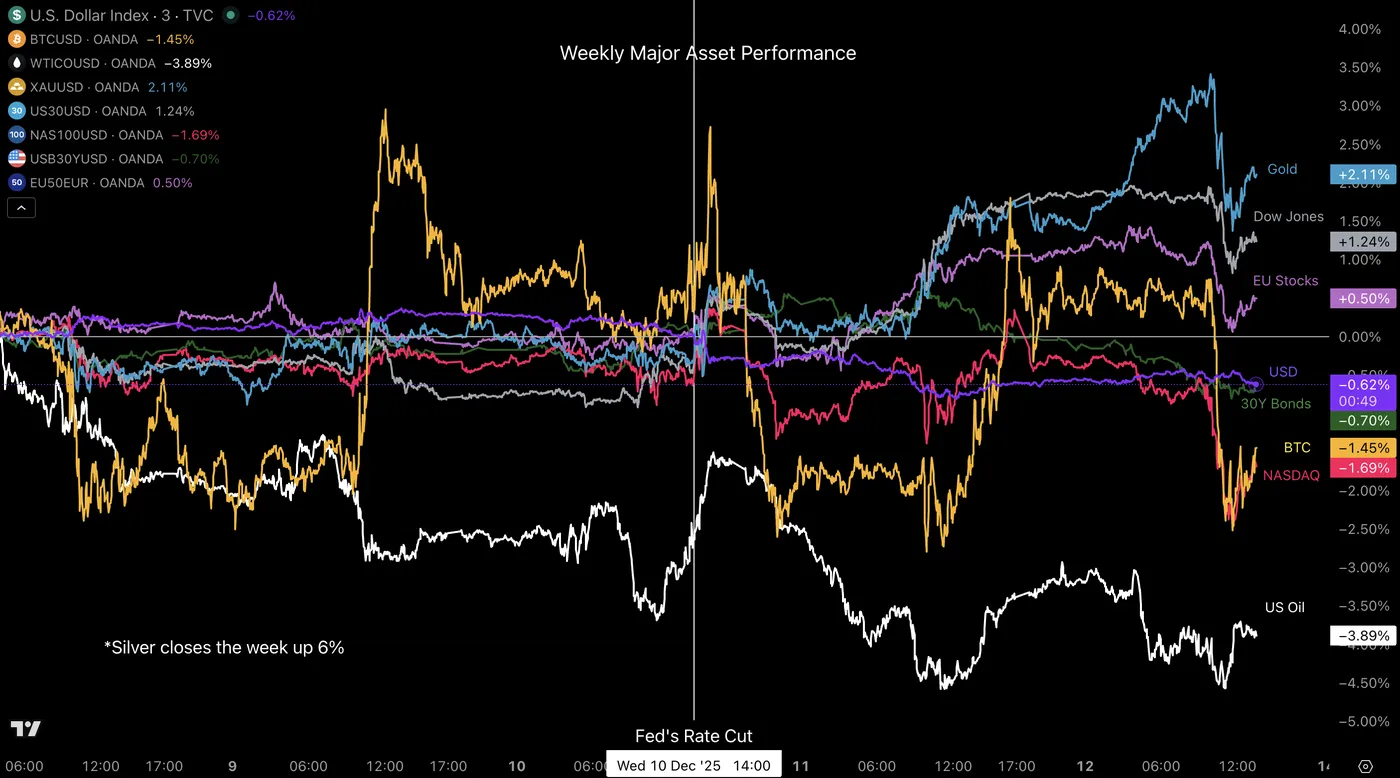

The Dow Jones traded at new all-time highs in consecutive sessions, marking a strong shift higher. Its record price is now at 48,886.

However, the rising tide did not lift all boats.

The US Dollar took a huge hit following the cut, despite the lack of explicitly dovish signals and lower projections in 2026.

Furthermore, the rotation flows that boosted the Dow came at a cost to the Nasdaq: since the cut, the tech-heavy index has dropped by 2%, with capital fleeing toward Industrial and traditional assets.

Weekly Performance across Asset Classes

Weekly Asset Performance – December 12, 2025 – Source: TradingView

But concerns remain, as seen throughout today’s session and confirmed by Chicago Fed President Austan Goolsbee. He dissented against the cut, deeming it not urgent given that the labor situation is not dire and inflation remains way too high. He argued in favor of waiting for the inflation picture to clear before cutting further—fair remarks, considering the Federal Reserve has been “driving blind” following the month-and-a-half-long Bureau of Labor Statistics shutdown.

Some profit-taking is also normal after a relentless “Everything Rally” (or Debasement Trade). The fall in the US Dollar combined with sizzling metals brings back echoes of early 2025 flows.

Strong flows but not too surprising when considering how huge next week’s data releases will be.

The question now is whether sentiment can hold after today’s reality check.

Silver fell 4% in today’s session right after reaching a record level of $65. Despite the drop, it is still closing the week up 6% and has surged 23% since the last week of November.

Silver (XAG/USD) 4H Chart. December 12, 2025 – Source: TradingView

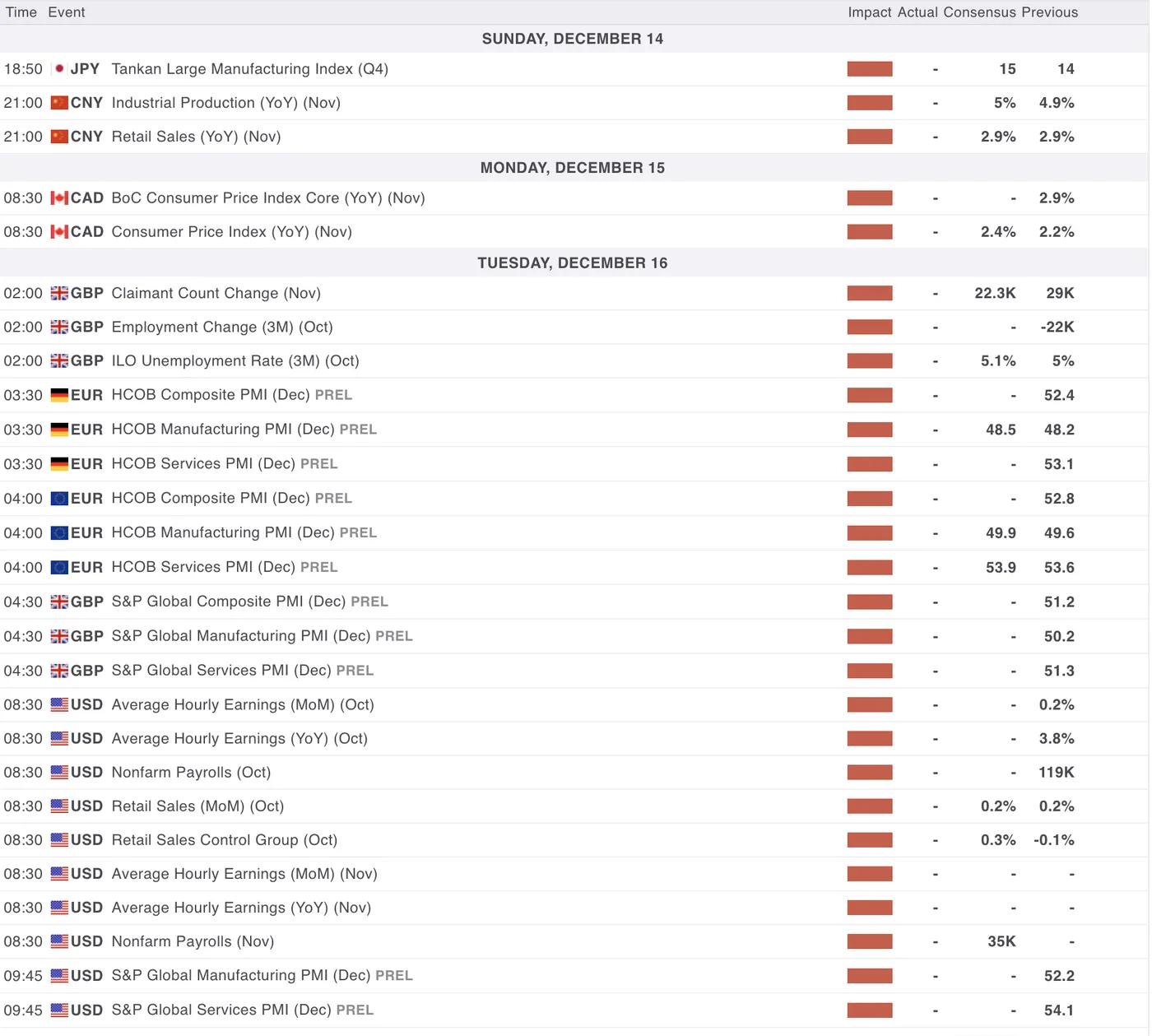

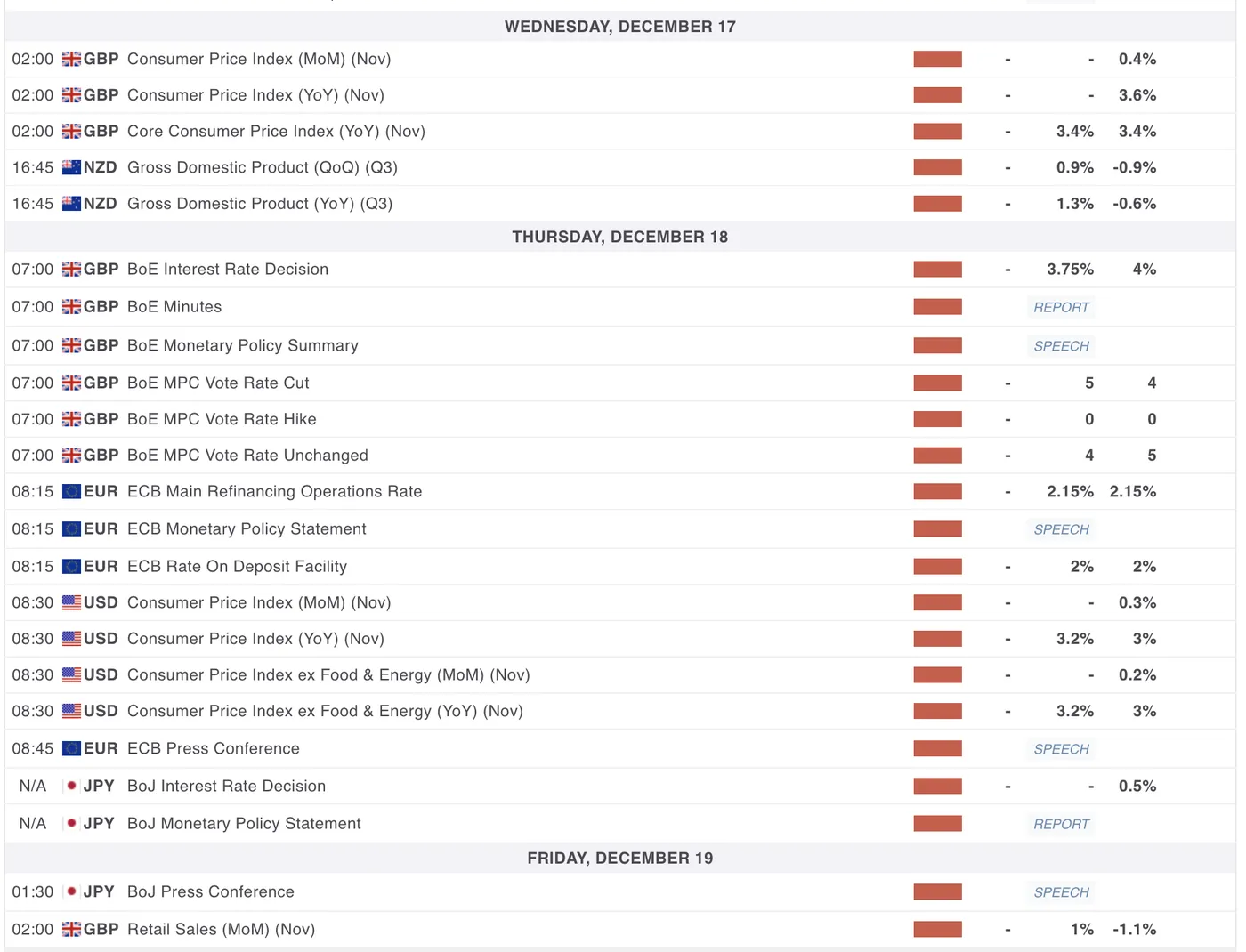

The Week Ahead – Major data is back for the US

Asia Pacific Markets – Bank of Japan in focus

Next week’s action in APAC Markets will be quite interesting.

The week will start on Sunday evening (in North America) with quite a lot of interesting economic data, between Manufacturing data from Japan, Retail Sales from Japan and a Business Survey from New Zealand.

The week then officially commences with some PMI releases for Australia, more trade data for Japan on Tuesday and the Kiwi GDP on Wednesday (very important report).

With all due respect to these (key) pieces of data, they will just be acting as Entrées for Thursday evening’s Bank of Japan rate decision.

High expectations for a hike have grown even higher in the past month, as the rout on the Yen has kept increasing despite JPY sellers taking somewhat of a breather last week.

Closing the week around 156.00 despite Dollar weakness, the Bank of Japan is facing quite an important test.

The key really will be whether the BoJ materializes some hawkish communications from their hike, if they actually provide one. The current pricing for the hike is around 75%.

Europe and UK Markets – ECB Rate Decision, UK Employment & PPI supplemented by some PMIs

Next week will also be big for Europe, particularly for the UK.

Tuesday will start with their Employment numbers expected at +22K, releasing in the Tuesday overnight session at 2:00 A.M. and facing some important tests.

The Bank of England now holds the highest interest rates of OECD nations and have about 60 bps of cuts priced in through 2026.

The Pound actually was one of the best performers against the dollar these past few weeks and may stand on top for a moment, particularly if UK data comes in strong.

Thursday will also be quite important for GBP traders as they will also get some inflation data, with the UK PPI and Retail Price Index reports. And I was about to forget the Bank of England rate decision, with a 25 bps cut largely expected.

Euro traders will also be served, between rounds of PMI releases but most importantly, the final ECB rate decision for the year, also releasing Thursday.

No change is expected, but as we conclude 2025, keep a close eye on their communication for 2026.

North American Markets – US Non-Farm Payrolls and CPI make their comeback

Nothing much for North American markets… Actually that’s false.

The US will get quite some attention after this week’s cut, transitioning towards the return of live data.

In the mix, November NFP data on December 16, CPI on December 18. Some individual reports will be released for the two quintessential releases

For Canada, they will also be releasing their inflation data on Monday to start the North American week, before only awaiting a Macklem Speech on Tuesday around noon.

Next week’s calendar in two parts. Get ready for some volatile action!

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Safe Trades and enjoy your weekend!