{kind=link}

Summary

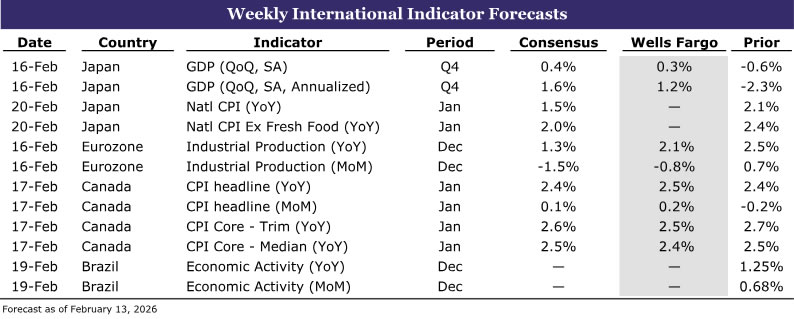

International Week Ahead

- Japan Q4 GDP: Growth Rebound to Keep BoJ Hikes in Play • (02/16)

- Canada January CPI: Noisy Headline and Cooling Core to Give BoC Breathing Room • (02/17)

- Brazil December Activity: Year-end Momentum to Influence Early ’26 BCB Policy • (02/19)

- Banxico February Meeting Minutes: Cryptic Communications, but Perhaps Minutes Clear the Smoke? • (02/19)

G10

Japan Q4 GDP • Monday

Growth Rebound to Keep BoJ Hikes in Play

While both we and consensus expect a rebound in Q4-2025 following the quarter-over-quarter annualized 2.3% contraction in Q3, we forecast a milder recovery of 1.2% versus 1.6% for consensus. The contraction in Q3 was driven largely by weaker net exports after shipments were pulled forward into Q2 ahead of anticipated U.S. tariffs. With tariffs lowered in July 2025, the drag from net exports should ease and turn supportive, while January trade data points to continued strength in global semiconductor demand, underpinning exports. Domestically, business sentiment has improved, as shown in the Bank of Japan’s (BoJ) Q4 Tankan survey, which should translate into firmer business investment. Additionally, the front-loading of construction and residential investment ahead of new environmental regulations introduced in Q2 should also have faded, supporting a broader improvement in investment. Taken together, stronger exports and higher investment should be sufficient to drive a rebound in Q4 growth. A return to growth would keep BoJ rate hikes in play, though the broader policy backdrop warrants caution. The Takaichi administration’s recent landslide victory has revived concerns around expansionary fiscal policy, contributing to upward pressure on yields and pushing 10-year JGBs to historical highs. However, if new debt issuance is avoided, as the administration has indicated, the policy rate may not need to rise as much as markets currently expect. The BoJ is likely to proceed cautiously as it assesses fiscal developments and waits for clearer evidence of wage-price firming, particularly with inflation expected to cool further in data to be released next week due to government energy subsidies and stabilizing food prices. We maintain our base case for a 25 bps rate hike by Q3-2026, bringing the policy rate to 1.00%.

Canada January CPI • Tuesday

Noisy Headline and Cooling Core to Give BoC Breathing Room

We expect headline inflation to rise in Canada to 2.5% in January from 2.4% in the previous month as base effects peak. Base effects reflect the lowering of prices between December 2024 and February 2025 because of the temporary GST/HST holiday. Elsewhere, measures of underlying inflation such as the trimmed and weighted median inflation are likely to decline to 2.5% year-over-year and 2.4%, respectively, from 2.7% and 2.5% in December. The temporary rise in year-over-year headline inflation is likely to keep the market and consensus baseline view for an on hold Bank of Canada (BoC) intact near-term. We believe these base effects are worth about 0.6-0.8 percentage points and imply a substantial stepdown in inflation as early as the February report. It’s notable that underlying inflation as suggested by the 3m average of trimmed and weighted median inflation are running at 1.45% and 1.85% respectively vs. 6m averages around 2%. We believe headline inflation is likely to step down to below 2% as soon the February report (1.8% per our nowcast). As such, the macro narrative is likely to shift from the noise of elevated headline inflation to cooling underlying core inflation. This, combined with sub-trend growth, economic slack and downside risks to growth from continued trade uncertainty with the US, we see greater room for the BoC to cut rates than hike. Current policy rate at 2.25% is within the range of neutral rate estimates (2.25-3.25) for an economy that is likely undergoing a structural transition with more to come as USMCA negotiations continue. On the flip side, a faster rollout of fiscal stimulus is likely to contain downside risks and reduce the need for deeper rate cuts.

EMs

Brazil December Activity • Thursday

Year-end Momentum to Influence Early ’26 BCB Policy

The December activity index is likely to show Brazil’s economy lost steam at the end of last year. Uber-restrictive monetary policy settings and limited fiscal stimulus as well as pre-holiday spending rolling off should push the activity index lower relative to the prior month. We will be attentive to the activity index as data will fill in the rest of the economic story for Q4 as well as how Brazil’s economy performed for all of 2025. But more importantly, the December activity index will act as the last major gauge of activity that Brazilian Central Bank (BCB) policymakers will be able to assess before meeting in March. Inflation takes precedence for the BCB, but policymakers have committed to cutting interest rates at the March Copom with the only outstanding question being how aggressive policymakers want to lower the Selic Rate. December activity could play a more influential role this time around as recent commentary from BCB policymakers leave the door open to move gradually with a 25 bps cut or remove monetary policy restriction quicker by starting with a 50 bps rate reduction. For us, we believe policymakers will opt for caution and deliver a 25 bps cut, but we could be swayed toward a 50 bps cut come March if activity is especially weak. Right now, markets lean only slightly toward the BCB lowering the Selic Rate by 50 bps, so the activity index could reinforce calls for a larger move or dial back near-term easing expectations. We hold a less dovish view on BCB monetary policy for all of 2026, which also means a more rapid pace of easing to start the year would also force us to recalibrate our YE-26 Selic Rate forecast.

Banxico February Meeting Minutes • Thursday

Cryptic Communications, but Perhaps Minutes Clear the Smoke?

Central bank meeting minutes rarely offer a ton of new insight into future interest rate decisions. Minutes are backward-looking and do not reveal which policymaker said what, a dynamic which is especially true for Banxico. As such, we do not expect anything groundbreaking to come out of February Banxico minutes, but the official statement as well as post-meeting communications are sending mixed messages and creating more smoke than clearing the fog. Maybe Banxico minutes next week will offer clarity? Again, skeptical, especially after policymakers left rates on hold earlier this month, told markets keeping rates unchanged may prove to be a “pause” in the easing cycle, all while revising their inflation forecasts sharply higher. Adding a bit more confusion to the mix are Banxico Deputy Jonathan Heath’s recent comments to a local bank. Heath appeared to shred Banxico’s inflation forecasts as unrealistic (again) this time going so far as to say “almost nobody believes that not only are we not going to meet the goal for Q2-2027, but not even in the next four, five or ten years.” He did, however, mention that if inflation evolves in line with Banxico’s inflation target, which has again been revised higher, a majority of members could opt to vote for a rate reduction at the next meeting in March. At least based on how Banxico framed its latest official statement, that appears to be the message it is sending to markets, according to Heath. If policymakers are willing to accept higher inflation, why not just cut in January? Why “pause.” Why bury any kind of guidance in a podcast? Confused? Us too. Markets seem to be pricing more Banxico easing after Heath’s comments, which we believe is a mistake. Banxico may wind up cutting in March, but for now, we are sticking with our view that Banxico will hold rates steady at its next meeting and keep rates on hold for all of 2026. Minutes may offer some insight, but either way, we expect Banxico to communicate again with markets ahead of the March meeting.