following an exceptionally strong Q3. Quarterly growth has been volatile, reflecting large swings in trade and inventories, and Q4 is likely to mark a reversal. We see a pullback in exports alongside a moderation in inventory accumulation as the key drags on activity.){kind=link}

Summary

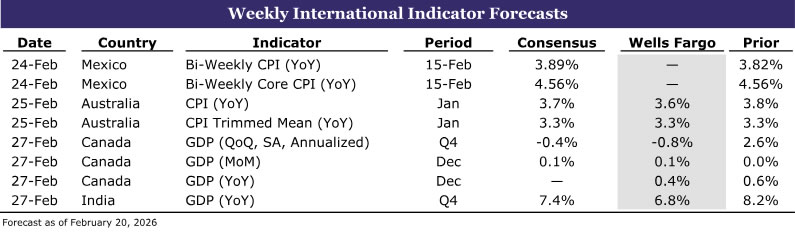

- Canada Q4 GDP: Negative Q4 GDP Sets the Stage for a BoC Cutting Restart • (02/27)

- Australia January CPI: A Soft(er) Print Ahead, Not a Green Light for March Hike • (02/25)

- India Q4 GDP: Disregard a Q4 Slowdown, Solid Growth Ahead • (02/27)

- Mexico Biweekly CPI: Banxico Flirting with Policy Error • (02/24)

G10

Canada GDP • Friday

Negative Q4 GDP Sets the Stage for a BoC Cutting Restart

We expect Q4-2025 GDP to undershoot consensus, contracting by 0.8% quarter-over-quarter (SAAR) following an exceptionally strong Q3. Quarterly growth has been volatile, reflecting large swings in trade and inventories, and Q4 is likely to mark a reversal. We see a pullback in exports alongside a moderation in inventory accumulation as the key drags on activity. On a monthly and year-on-year basis, we look for GDP growth of 0.1% and 0.4%, respectively. While growth through 2025 has proven more resilient than anticipated—supported by solid domestic demand and inventory dynamics—we expect momentum to fade in 2026. Rising trade tensions should weigh on business investment, while a softer labor market increasingly constrains household spending. Consensus expectations of 1.0%-1.5% growth in 2026 (roughly in line with potential) implicitly assume a benign outcome from USMCA renegotiations, either a muddle-through status quo or a successful renewal. More adverse scenarios, including materially higher tariffs or a USMCA withdrawal, would likely push annual growth into negative territory, depending on the severity of the shock. Against this backdrop, the balance of risks to growth remains clearly skewed to the downside. Combined with ongoing disinflation, this reinforces the asymmetry in Bank of Canada (BoC) policy toward easing. We expect the BoC to restart rate cuts in Q2, potentially as early as the April meeting, coinciding with the release of a new Monetary Policy Report and updated forecasts.

Australia CPI • Tuesday

A Soft(er) Print Ahead, Not a Green Light for March Hike

For next week’s January inflation print, we expect headline CPI to ease slightly to 3.6% year-over-year (vs. 3.7% consensus), with trimmed mean CPI holding at 3.3%, in line with consensus. Even in the event of an upside surprise, we do not see this as sufficient to raise the likelihood of a near-term RBA hike. We continue to expect the next rate increase in May to 4.10% and see greater downside risk to the hiking path. The reason for this conviction comes from the fact that inflation pressures are increasingly driven by policy-related and regulated components rather than competitively priced market goods, which should limit the RBA’s scope to tighten further. Consistent with this view, at the RBA’s most recent monetary policy meeting where they hiked rates, their forecasts showed headline and trimmed mean inflation peaking in Q2-2026, while the Cash Rate was held at 3.85%, with further hikes only anticipated beyond that point.

EMs

India Q4 GDP • Friday

Disregard a Q4 Slowdown, Solid Growth Ahead

We expect India’s economy softened at the end of last year as tariff uncertainty disrupted local activity. But now that a U.S.-India trade deal, as well as an EU-India trade agreement, has been reached, some of that uncertainty should be lifted and activity can be supported going forward. Point being, Q4 GDP data may show an economic deceleration, but we would view these data as backward-looking at this point. On a go-forward basis, India can be one of the top performing major economies in 2026. Reduced trade uncertainty helps, which combined with the lagged effects of prior Reserve Bank of India (RBI) easing, we believe India’s economy can grow ~7% this calendar year. Reduced trade and geopolitical uncertainty as well as improved growth prospects should also be an input into RBI policymakers monetary policy decisions. Policymakers opted to keep rates unchanged at the February meeting, and while the balance of risk is tilted toward additional easing later this year, we believe rates will be left unchanged for an extended period of time as growth recovers and the economy reflates. Perhaps the most interesting dynamic in India is the path of the rupee. INR has faced persistent depreciation pressure despite broad-based U.S. dollar depreciation. RBI FX intervention has done little to prevent or materially disrupt INR weakness, while constant intervention has made India’s external buffers less robust. To be clear, the RBI has adequate FX reserves, so running out of firepower is not necessarily an issue. But with inflation below target, manufacturing becoming more of a focus and FX reserves being drawn down, we often wonder why the RBI does not let INR be a more market-driven currency. For us, should current FX policy continue to be pursued, INR is likely to remain under pressure for the foreseeable future and USDINR will consistently set new all-time highs.

Mexico Biweekly CPI • Tuesday

Banxico Flirting with Policy Error

Financial markets continue to price near-term Banxico easing, and next week’s biweekly CPI may offer additional insight into whether market participants are getting ahead of themselves or accurately predicting rate decisions in Mexico. Rather than offer a view on the direction of biweekly inflation data, we wish to highlight that should data be consistent with rate cuts and Banxico indeed ease monetary policy in March and possibly again later this year, we would view those decisions as taking Banxico to the edge of a policy mistake. A few more Banxico rate reductions would make the Fed-Banxico rate spread historically narrow and not the most appealing carry profile to sustain capital flows into Mexico. Also, Banxico has limited FX reserves and, at least historically, has not opted to purchase FX reserves to build external buffers. Shock events are common, and Mexico is potentially exposed to a material shock scenario this year: USMCA negotiations. For now, we believe the USMCA re-negotiation will not cause much damage to Mexico, but the risk of an unfavorable trade agreement (or perhaps no North America trade agreement) is elevated. Additional Banxico rate cuts do not offer much room for error in Mexico and leaves MXN vulnerable to a trade-related shock, or any other external shock that may materialize. Our base case is for MXN to outperform Latam peer FX on political stability, but if political stability is upended, MXN can experience a sharp selloff that takes USDMXN back to a 20-handle quick.