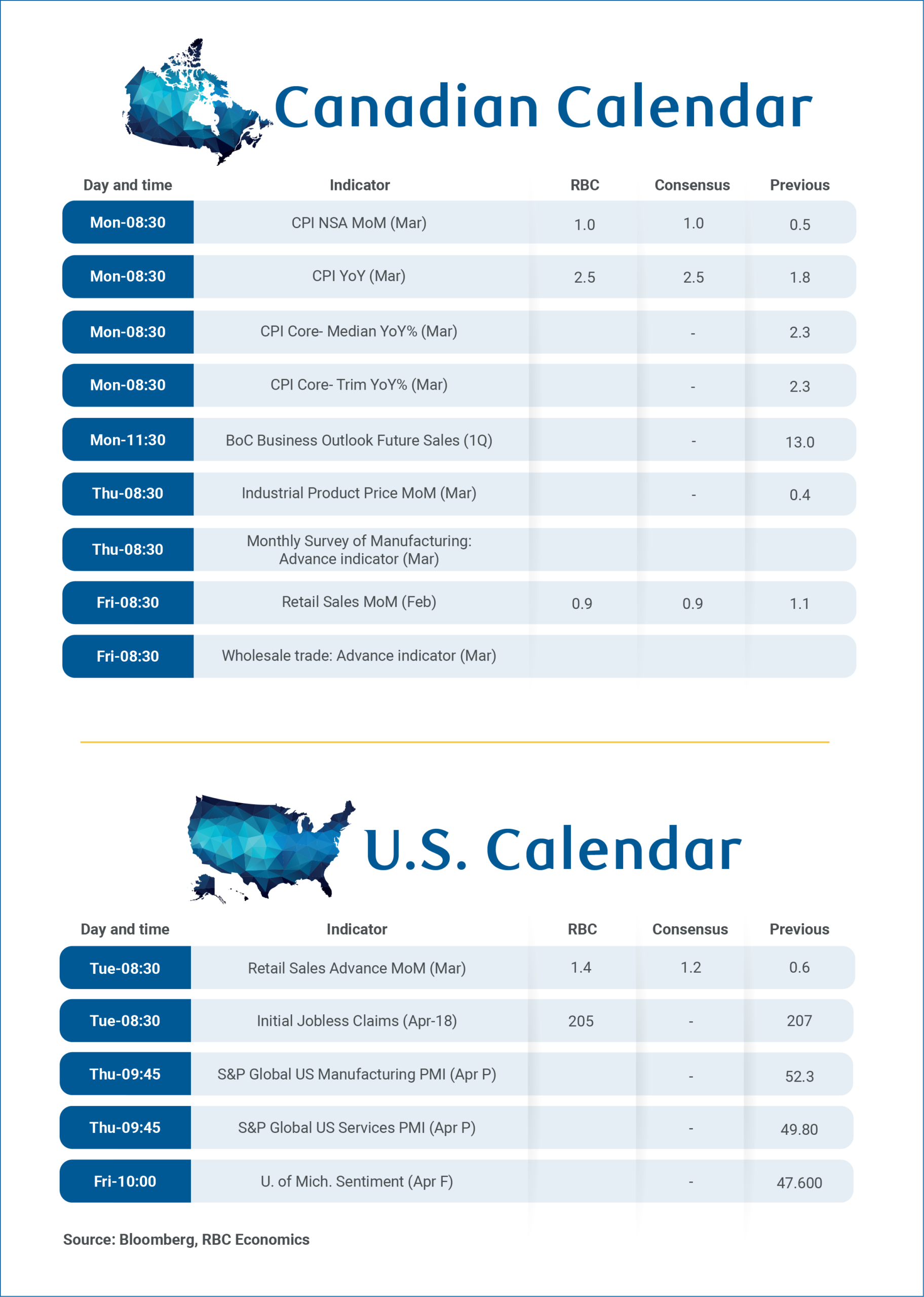

Higher gasoline prices in March in Canada —up 21% from February—are expected to push year-over-year growth in the headline Consumer Price Index up to 2.5% from 1.8% in February, while inflation excluding food and energy ticks slightly higher to 2.2%.

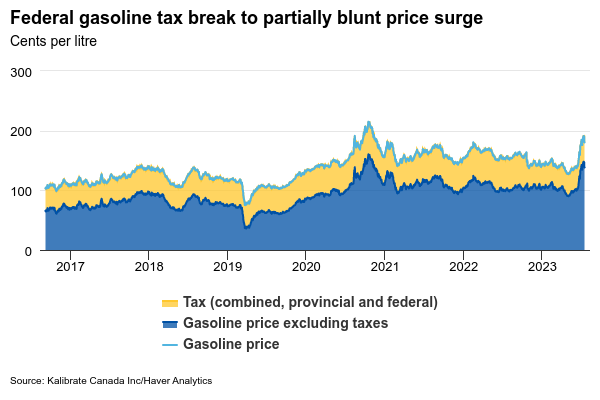

Annual energy inflation will likely rise above 0 for the first time since spring last year when the cancellation of the federal consumer carbon tax sent prices lower in April. In March, gasoline prices were up 6.8% from a year ago on average, but would have been up 23% without the impact of that tax change.

Impact from the removal of the carbon tax will fall out of the yearly comparison in April. Gasoline prices have risen further, and to-date are tracking more than 30% above a year ago. The temporary suspension of federal fuel excise tax (ten cents per litre) coming into effect on April 20 should blunt some of the impact. Still, we estimate rising energy CPI will drive headline inflation above 3% in April.

Food CPI has been biased higher by unfavourable annual comparisons in the prior months due to the federal HST/GST holiday last year and is set to ease in March, as the tax holiday in mid-February 2025.

The focus in the coming months will increasingly shift to the extent surging energy prices spread into broader inflation pressures, best gauged by the Bank of Canada’s core inflation measures that strip out more volatile components as well as effects from indirect taxes.

These core inflation measures showed significant signs of easing ahead of the Middle East conflict. CPI trim and median averaged 1% on an annualized basis from December to February.

Business survey to flag improving demand ahead of high oil prices

Easing (underlying) inflation pressures are consistent with a weak, albeit improving domestic demand flagged by businesses in the Q4 BoC Business Outlook Survey in 2025.

The Q1 update on Monday should tell a similar story, echoing other business confidence measures (eg. CFIB’s Business Barometer) that have mostly improved into early 2026 ahead of the recent oil price surge. Indeed, the survey period for BOS fell in February but likely didn’t capture much of the change in sentiment after the Middle East conflict broke out near the end of that month.

Recent softer core inflation readings should give the BoC more flexibility to look through the initial increase in energy prices from the conflict, but not if pressure broadens and persists. Risk of high oil prices seeping into core inflation, raising inflation expectations will grow the longer prices stay elevated, but are not what we currently expect in our latest base case projections.

For now, we continue to follow market pricing of oil that expects a gradual moderation in prices over the rest of this year. We see little meaningful passthrough to core CPI, and expect the BoC to hold the overnight rate steady at 2.25% for 2026.

In line with Statistics Canada’s preliminary estimate, we expect retail sales expanded 0.9% in February to build on a 1.1% increase in January. Our consumer spending tracker continues to flag resilience in core retail purchases in early 2026 that stretched into March despite sharply higher fuel prices.

In the U.S., the focus next week will be on retail sales for March, where we expect a 1.4% in nominal sales mostly due to higher gasoline prices—regular gasoline prices spiked 26% in March, and stronger light motor vehicle sales. Excluding both motor vehicles and gas, we expect retail spending was more subdued (+0.2% m/m) as discretionary goods spending softens, after sizeable pre-tariff front-running last year.

{kind=link}