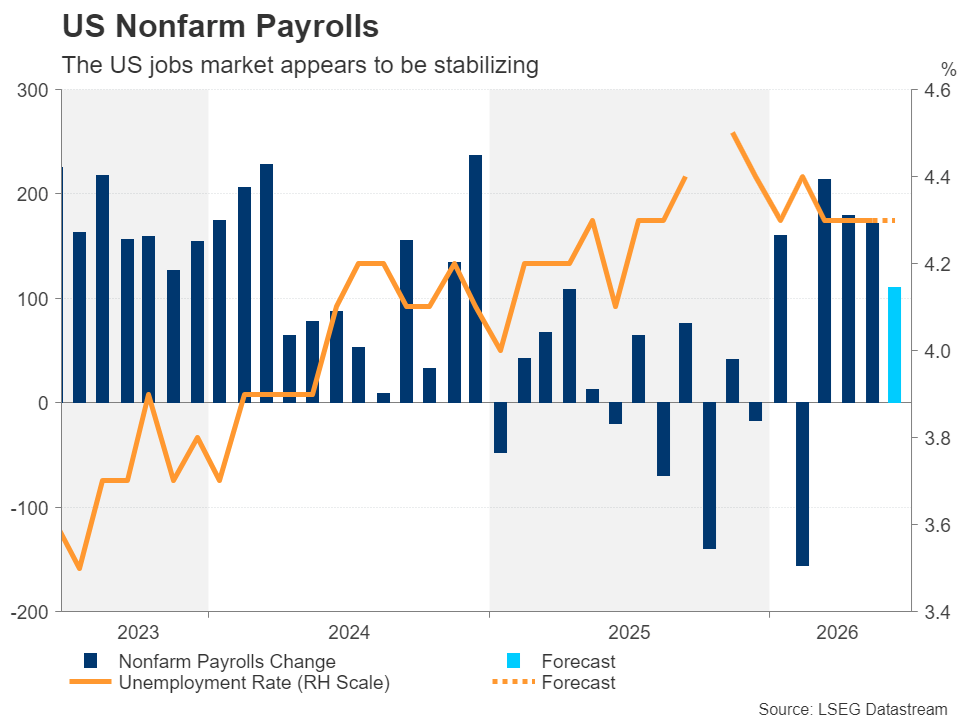

- US jobs market likely slowed in June, but World Cup may skew data.

- Warsh’s first Sintra appearance will also be crucial for the US dollar.

- But after the June FOMC surprise, will hawkish expectations be matched?

- Warsh speaks on Wednesday (13:00 GMT), NFP is due a day early on Thursday (12:30 GMT).

A Barrage of Data and Central Bank Speak

A busy week is lined up for investors, as not only is the latest jobs report set to be released a day early due to markets being shut on Friday for Independence Day celebrations, but new Fed Chair Kevin Warsh speaks for only the second time since taking over the post. If that wasn’t enough to keep traders glued to their desks, there’s also a slew of other US data on the way that could shape expectations about the Fed policy path.

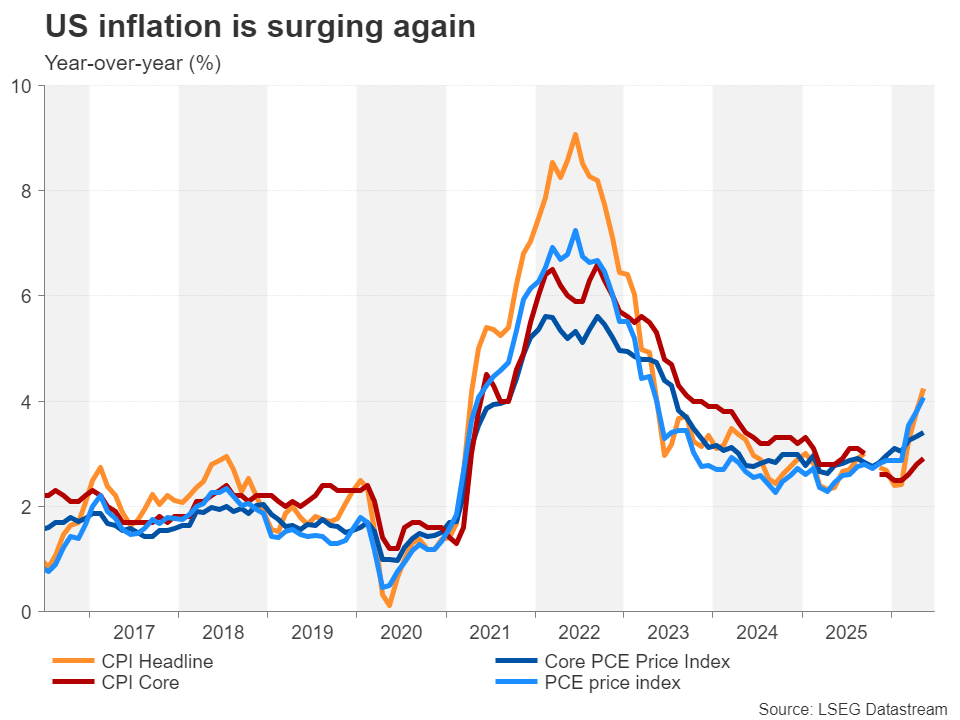

Heading into those risk events, investors are somewhat hawkishly positioned, pricing in just over three-thirds probability of a 25-basis-point rate hike in September, which represents a slight paring back from the near 100% odds in the immediate aftermath of the June policy decision. Nevertheless, markets have read Kevin Warsh’s message loud and clear – taming inflation is the Fed’s top priority right now and don’t expect much in the way of forward guidance.

Deciphering the New Fed Chair

The latter has raised the chances of greater volatility in reaction to the incoming data, not only as investors scrutinize every economic indicator but also because of the lack of clarity about which data points the Fed will focus most on under the new regime. Wednesday’s panel discussion in Sintra, Portugal, organized by the European Central Bank, presents an opportunity for Warsh to outline in more detail about how the Fed intends to bring inflation back to 2%.

However, with other central bank heads also being invited to take part in the panel, namely, the Bank of England’s Bailey and Bank of Canada’s Macklem, together of course with President Lagarde, Warsh may not reveal much more about his views than he did at his post-meeting press conference two weeks ago. If anything, there’s a risk Warsh may not come across as hawkish as he did on his FOMC debut, potentially echoing New York Fed President Williams’ recent neutral stance on the direction of interest rates.

Is Another Hot NFP Report on the Cards?

Should that turn out to be the case, the adverse reaction to any upside surprises in Thursday’s jobs report is likely to be more muted. Following May’s better-than-expected print of 172k, forecasts for June nonfarm payrolls are for a more moderate gain of 110k. The unemployment rate is projected to have held steady at 4.3% for a fourth straight month. However, growth in average hourly earnings is expected to have quickened slightly to 3.5% y/y in June.

Another stronger-than-expected headline figure would further fuel bets of a September hike, or even sooner in July. This is certainly possible as lower energy prices due to the de-escalation in the Middle East and the boost to the economy from hosting the FIFA World Cup likely led to increased hiring in June.

Choppy Times Ahead for the Dollar

For the US dollar, however, it’s going to be a tricky lead-up to Thursday’s jobs release. Aside from the ECB forum and NFP data, traders will also have to juggle the consumer sentiment gauge for June and JOLTS job openings for May on Tuesday, as well as the ISM manufacturing PMI, ADP employment change and Challenger layoffs, all for June, on Wednesday.

In the meantime, any updates on talks between the US and Iran will also test dollar bulls, not to mention remarks from other central bankers at Sintra. In particular, the euro will be almost as much in the spotlight, as Lagarde may sound a bit more optimistic about the Eurozone inflation outlook now that oil prices are almost back to pre-war levels.

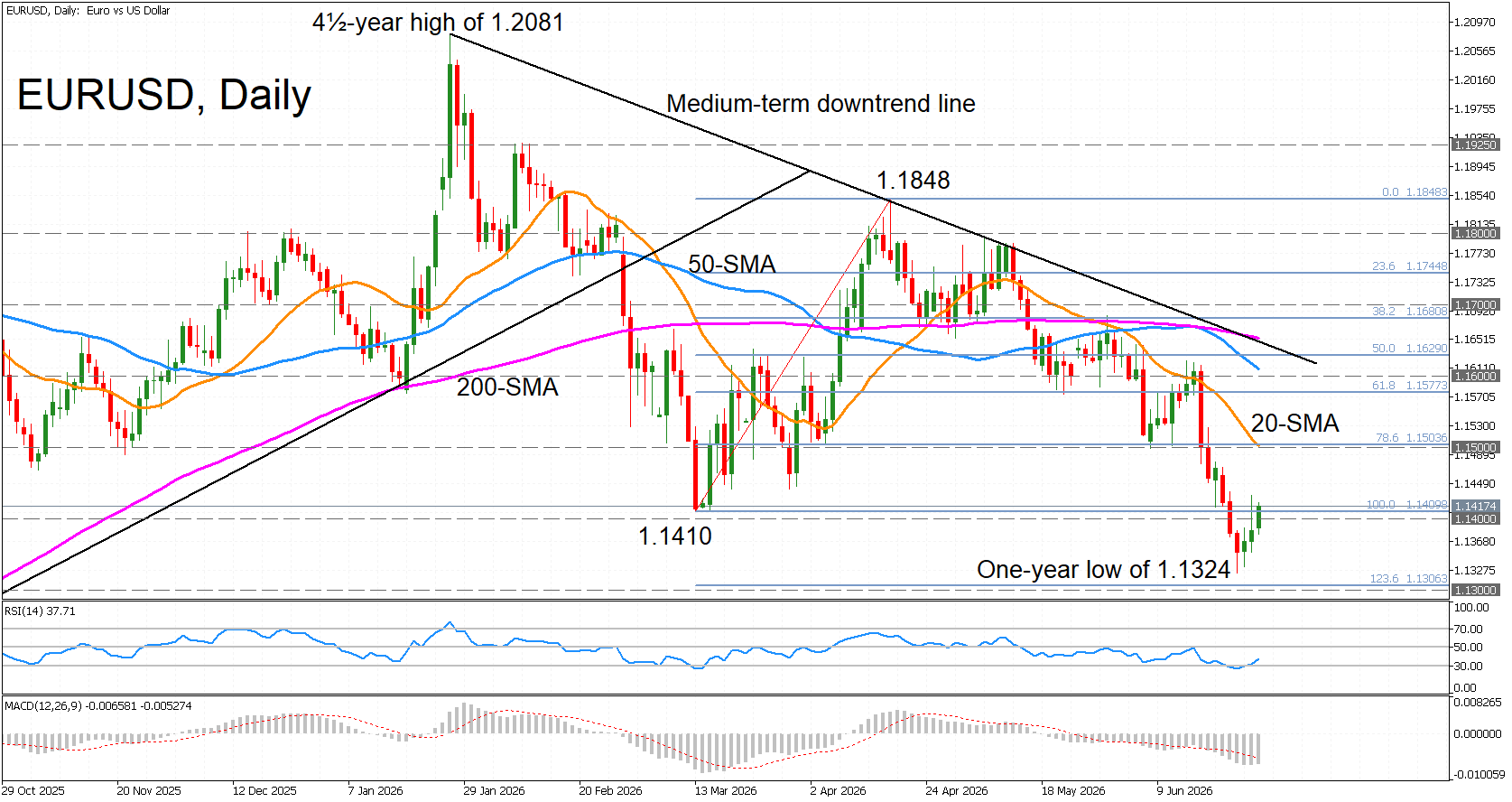

Is the Euro in Danger of Breaching $1.13?

Interestingly, the reduced geopolitical risks haven’t been able to offset the boost to the dollar from the Fed’s hawkish tilt. The euro hit one-year lows last week after tumbling below $1.1400. An upbeat set of labour market indicators out of the US would reinforce the hawkish expectations, triggering fresh selling towards $1.1300, which lies near the 123.6% Fibonacci extension of the March-April rebound.

But soft NFP numbers combined with a much more neutral sounding Warsh could buoy the euro towards its 20-day moving average just above $1.1500.

Wall Street will also be keeping a close eye on Warsh’s rhetoric and the payrolls numbers. The S&P 500’s recent lower high suggests that the AI rally is cooling off. A hot jobs report would create a major hurdle for a new all-time high as it would likely cement a September rate hike.

{kind=link}