Here are the latest developments in global markets:

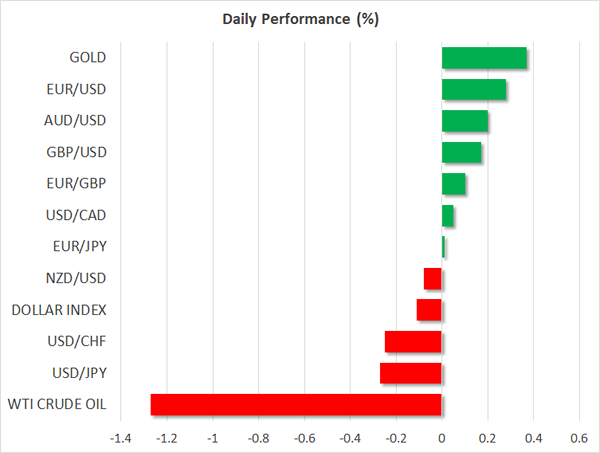

FOREX: The US dollar index was marginally lower on Friday, after also trading lower yesterday, even though yields on longer-term US Treasuries were on the rise.

STOCKS: Asian markets were in a sea of green today. Japan’s Nikkei 225 and Topix indices were up by 0.2% and 0.7% respectively, both hovering near multi-decade highs. In Hong Kong, the Hang Seng index was up 0.1% – touching its highest on record – while in Europe, futures tracking the Euro Stoxx 50 are in positive territory, albeit only marginally. Over in the US, the three major equity indices – Dow Jones, S&P 500, and Nasdaq Composite – all closed in the red yesterday, with the biggest loser out of the three being the Dow, which lost 0.37%. However, futures tracking the Dow, S&P, and Nasdaq 100 currently suggest that these indices could open slightly higher today.

COMMODITIES: Energy prices retreated on Friday, with WTI and Brent crude trading lower by 1.3% and 1.0% respectively, despite the weekly EIA inventory data yesterday showing a larger-than-anticipated drawdown in US stockpiles. The downward correction is being attributed to profit-taking by traders on prior long-oil positions, as well as concerns that US production is likely to rise rapidly in the coming months as the extremely cold weather conditions in the US recede and drillers can increase their output freely. In precious metals, dollar-denominated gold was up nearly 0.4%, with no clear fundamental trigger behind the move other than the dollar’s overall softness.

Major movers: Dollar on the defensive despite rising US yields

The US dollar index remained on the back foot on Friday, extending the losses it posted on Thursday, as the risk of a US government shutdown was seen as weighing on the currency. The House of Representatives passed a bill yesterday to fund government operations until February, but the bill has not been approved by the Senate yet.

Interestingly enough, the greenback underperformed even while the yields on longer-term US Treasuries were moving higher, something that is usually positive for the currency. This suggests that the yields on US bonds may be rising for the “wrong reasons”. Typically, rising yields signal investors’ expectations that a strengthening US economy could see the Federal Reserve accelerate its tightening pace. This is usually positive for the dollar. This time around, though, yields may be rising because major buyers of US bonds (such as China and Japan) are cutting back on their purchases, or perhaps due to markets speculating that the recent deficit-funded tax cuts could make US debt even more unsustainable. It should be noted that the 10-year Treasury yield is now above 2.64%, a level which has been widely touted recently as the “line in the sand”, after which Treasuries become attractive to hold relative to equities. This may also be a factor behind the tumble in US stocks yesterday.

Elsewhere, there was little movement in the currency market. The euro gained somewhat yesterday, after ECB Executive Board member Benoit Coeure said that the eurozone is no longer in “recovery”, but is now in expansion. His comments were seen as another hawkish sign that the ECB may be set to scale back its massive stimulus program later in the year.

The antipodeans were mixed on Friday, with aussie/dollar trading 0.2% higher, but kiwi/dollar being down nearly 0.1%. That said, both pairs are still hovering near four-month highs.

It is also notable that the Chinese currency rose to a fresh more-than-two-year high versus the greenback – equivalently dollar/yen fell to a more-than-two-year low, specifically touching 6.3870 – and is on path to recording its sixth consecutive weekly gain, the longest such stretch since January 2017.

Day ahead: UK retail sales and prospect of US government shutdown at center of attention

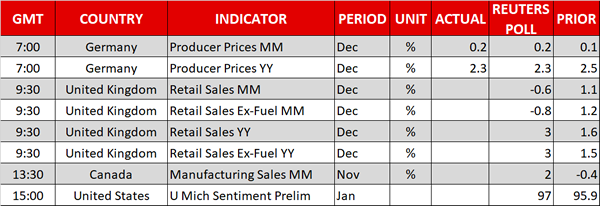

The most important release during morning European trading hours will pertain to UK retail sales for the month of December. Those are scheduled for release at 0930 GMT. A notable decline is expected on a monthly basis, but a rebound on a yearly basis. The readings are of significance because they can also show whether the squeeze in real incomes – by virtue of inflation outpacing wage growth – continues to act as a drag on consumer spending and consequently growth in the economy overall.

Canadian manufacturing sales for the month of November will be made public at 1330 GMT.

In the US, the release of the University of Michigan’s preliminary survey on January consumer sentiment due at 1500 GMT is expected to attract attention. Expectations are for the reading to reflect an improvement in consumer sentiment, following the previous month’s decline.

Market participants’ concerns for a possible US government shutdown have been acting to the detriment of the US currency – though a shutdown occurring is an unlikely scenario. The House of Representatives passed a bill funding the government through February 16 on Thursday. The bill though needs to be approved by the Senate as well; this being a tougher challenge given the slimmer Republican majority in the Senate and recent disputes between President Trump and the Democrats over the extension of funding for the Children’s Health Insurance Program. The relevant vote is anticipated to take place today, with a positive outcome likely to alleviate some uncertainty and perhaps help the dollar claw back some of its losses. Investors will be monitoring the situation.

Fed policymakers making appearances include Atlanta Fed President Raphael Bostic who is scheduled to participate in a discussion titled “Thoughts on the Economy” at 1345 GMT, Fed Vice Chair for Supervision Randal Quarles who will be speaking on bank regulation at 1800 GMT, and San Francisco Fed President John Williams who will be talking at a Bay Area forecasting conference. All three are FOMC voting members.

In oil markets, the International Energy Agency’s (IEA) monthly report is due at 0900 GMT. The report touches on issues affecting oil markets, looking at demand and supply as well. The US Baker Hughes oil rig count will be released at 1800 GMT.

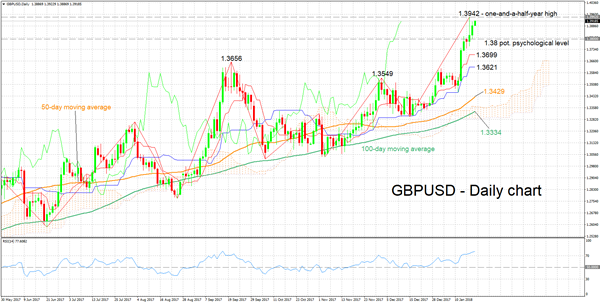

Technical Analysis: GBPUSD bullish in short-term though RSI overbought

GBPUSD has posted considerable gains in recent days and is currently trading not far below the more than one-and-a-half-year high of 1.3942 recorded on Wednesday. Technical indicators support the case for a bullish picture in the short-term: the Tenkan- and Kijun-sen lines are positively aligned and the RSI is rising; a note of caution though as RSI is in overbought territory above 70.

Stronger retail sales figures out of the UK are expected to further boost the pair with immediate resistance potentially coming around Wednesday’s high of 1.3942. As previously stated, the price is at the moment close to this level – a break above would shift focus to the 1.40 handle as an additional barrier to the upside, this being a potential psychological level.

If the data disappoint though, the pair is anticipated to head lower. In this case, support could come around another potential psychological mark, namely the 1.38 handle.

Of course, developments in the US also have the capacity to spur movements in the pair during Friday’s trading.