Sunrise Market Commentary

- Rates: German yields clear important technical resistance

The core bond sell-off accelerated yesterday. German yields copied last week’s move by US yields, breaking above key resistance levels. The sell-off might slow if the overnight risk-off correction on stock/commodity markets persists. However, German inflation data, president Trump’s state of the union and the Fed meeting are all able to start a new selling bout. - Currencies: Risk off correction to become dominant factor for FX short-term?

Yesterday, the dollar extended the bottoming out process that started end last week. Overnight risk sentiment turned further risk-off. The yen was already well bid of late and might further profit. We keep a close eye at EUR/JPY. A further rise of the yen/decline of EUR/JPY might prevent further euro gains even in case of good EMU eco data.

The Sunrise Headlines

- US stock markets corrected 0.5% to 0.7% lower yesterday. The sell-off accelerates in Asia this morning with also commodity markets and mainly base metals under pressure.

- ECB policy makers are sticking to the assumption that their bond-buying program will be wound down over about three months rather than brought to a sudden halt, according to euro-area officials familiar with the matter.

- The EU has passed Brexit transition guidelines making clear the UK will have to abide by all the bloc’s laws but have no say in the decision-making process during a two-year transition period.

- Polish central bank governor Glapinski said that he would not be surprised if interest rates, presently at 1.5%, were raised in the first half of 2019 or if they stay unchanged as inflation is benign despite fast economic growth.

- UK consumer confidence recorded its highest M/M increase in a year in January (108.2 from 107.1 vs 109.8 in January last year), according to a YouGov survey. Respondents reported a rosier outlook for household finances.

- A congressional panel voted to make public a classified Republican-authored memo that alleges surveillance abuses against an associate of President Donald Trump dating back to the 2016 campaign.

- Today’s eco calendar contains EMU Q4 GDP, EC economic confidence, German inflation, US S&P housing data and UK consumer confidence. Italy holds a BTP auction and ECB Mersch & BoE Carney are scheduled to speak

Currencies: Risk Off Correction To Become Dominant Factor For FX Short-Term?

Risk-off supportive for USD (ex USD/JPY?)

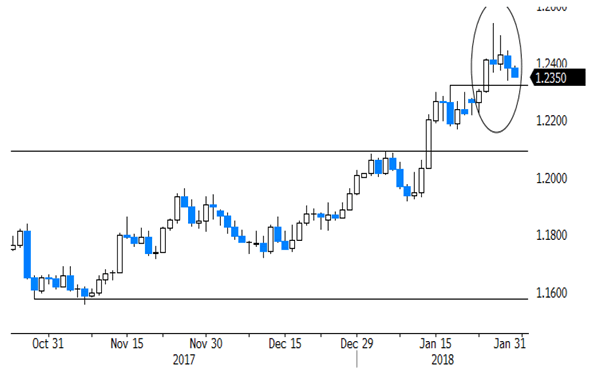

The dollar decline slowed at the end of last week and that continued yesterday. Core yields extended their break higher, but interest rate differentials were no good explanation for the USD price swings. EUR/USD drifted south in the 1.23 big figure. Remarkably, the move stalled after headlines that the ECB could consider a small tapering at the end of its APP. EUR/USD closed the session at 1.2383. The upside momentum in USD/JPY was far less strong. The pair tried to regain 109, but the move lacked momentum. USD/JPY finished at 108.96.

Asian equities join yesterday evening’s US correction. The risk-off move also weighs on commodities. The impact on the dollar is mixed. EUR/USD is losing a few ticks (1.2350). USD/JPY struggles not to return lower in the 108 area.

EMU data will be at least be as important for FX trading as US ones today. EMU Q4 growth is expected at 0.6% Q/Q and 2.7% Y/Y. German inflation is forecast to decline 0.7% M/M to stay unchanged at 1.6% Y/Y. We keep a close eye on the German inflation data. US consumer confidence is expect to rise from 122.1 to 123. Last but not least, risk sentiment might also return as a driver for FX trading. The EMU eco data will be strong. However, interest rate differentials weren’t really a good guide for FX trading of late. So, we don’t expect a resumption of the euro rally, even not on good EMU data. A risk-off correction could inspire further yen buying. USD/JPY looked already vulnerable of late and this might persist ST. Question is what it will mean for EUR/JPY and for EUR/USD. The jury is still out, but in a daily perspective, a further decline of USD/JPY and EUR/JPY might also cap the topside in EUR/USD and even cause some more downside pressure short-term. Later this week, the focus might turn to the Fed, the State of the Union and the US data.

Sterling showed some intraday gyrations yesterday. Sentiment clearly was more fragile than last week. EUR/GBP hovered in the high 0.87/low 0.88 area. EU ministers gave EU’s Barnier a mandate for the next phase of the Brexit negotiations. At the same time, the division in the UK conservative party is flaring up again. Today, UK credit data will be published and BoE’s Carney will testify before Parliament. Brexit headlines and a risk-off sentiment might continue to weigh on sterling. EUR/GBP can continue its rebound in the 0.8790/0.9033 trading range.

EUR/USD: correction continues