Higher US inflation fails to spark dollar revival

The US dollar depreciated across the board versus major pairs despite consumer prices rising more than expected. Inflation anxiety had triggered a sell-off in global stock markets with the Fed expected to ramp up their interest rate hike path yet the dollar did not benefit as higher rates have already been priced in by the market. Fiscal uncertainty driven by political factors continue to confound investors with stock indices rebounding this week and the dollar hitting a 2014 low. The paradox in consumer spending and retail sales continues as Americans remain confident in the economic outlook yet core retail sales remain flat and taking into consideration auto sales they actually dropped by 0.5 percent. The dollar showed some signs of life on Friday as it gained against a basket of major pairs, but not enough to offset the losses earlier in the week.

- Fed to release minutes of January meeting

- Kuroda renominated as Governor of Bank of Japan (BOJ)

- Lower trading activity with start of Chinese New Year celebrations and 3 day weekend in NA

Dollar Recovers on Friday But Still Underwater this Week

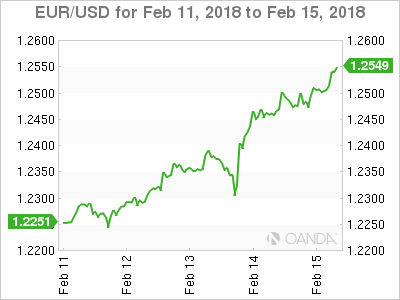

The EUR/USD gained 1.62 percent in the last five days. The single currency is trading at 1.2448 with the EUR recovering against the earlier losses versus the USD suffered earlier in the month. US inflation rose more than expected and US treasuries dropped in prices as investors sold them anticipating higher rates this year. Bond yields rose with the 10 year at four year highs (2.93 percent). The correlation between higher yields and a stronger currency is broken at the moment for the USD as the confidence in the stability of the US economy is up for debate. Fundamentals are strong and would point to a higher dollar, but political uncertainty around fiscal stimulus has made it hard to quantify the effects of actual and proposed legislation on the currency. The U.S. Federal Reserve will publish the minutes from its January Federal Open Market Committee (FOMC) meeting on Wednesday, February 21 at 2:00 pm EST. The meeting was the last presided by Chair Janet Yellen and is not expected to bring any surprises, but could prepare the market on what to expect in March when Chair Jerome Powell heads his first FOMC.

The USD went through a topsy-turvy week, with Wednesday’s release of consumer price index data providing the most volatility. The market forecasts were slightly improved with a 0.3 percent monthly gain. The employment report in February 2 was the first data point that suggested a stronger inflationary pressure. Stock markets had already suffered two difficult weeks and the dollar rose as the inflation data was released only to quickly give back all gains and end up in the red.

President’s day in the US will give some investors a much needed rest from a high octane trading week. The Lunar New Year celebrations will also affect trading volumes as Hong Kong and China markets will remain closed until Thursday. Stock markets had a positive week after stronger corporate results erased earlier losses.

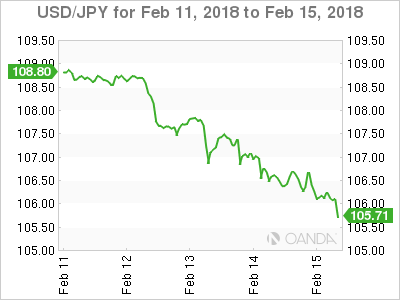

The USD/JPY lost 2.38 percent during the week. The currency pair is trading at 106.19 as the JPY keeps gaining. The government issued a statement where it was clear there is no need for intervention and the market took it as a sign to keep buying the yen. The tone changed slightly on Friday as the currency kept appreciating and there were some warning that the trade is one sided. The softness of the USD and uncertainty about how the American government will deal with growing twin deficits and political drama has boosted the JPY due to some safe haven flows.

The reappointment of BOJ Governor Haruhiko Kuroda along with other nominations of economist who favour further easing did not factor into Yen pricing in the short term, but should impact the growing gap between rates in Japan and the United States. In the short term, lack of stability in politics and fiscal uncertainty are overriding higher growth and interest rate expectations in the US.

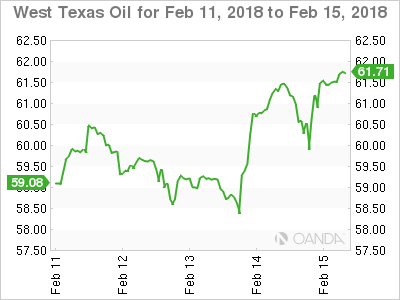

Oil prices advanced during the week. The price of West Texas Intermediate is trading at $61.21 with most of the gains in energy coming from dollar softness. Oil prices suffered losses earlier in the month as higher production in Canada, Brazil and the United States is anticipated given the high prices and producers in those nations not bound to the Organization of the Petroleum Exporting Countries (OPEC) production cut agreement. Lack of traction of the US currency is keeping prices above $60.

A small rise in oil rigs in Baker Hughes was not enough to derail energy prices specially with an underlying weak US dollar. The OPEC agreement with other major producers has stabilized oil prices after the freewill caused by overproduction. The question remains if demand for energy has recovered to the point that even after the agreement timeline runs out supply will not once again outweigh demand causing another drop in prices.

Market events to watch this week:

Monday, February 19

- 7:30pm AUD Monetary Policy Meeting Minutes

Wednesday, February 21

- 4:30am GBP Average Earnings Index 3m/y

- 9:15am GBP Inflation Report Hearings

- 2:00pm USD FOMC Meeting Minutes

Thursday, February 22

- 4:30am GBP Second Estimate GDP q/q

- 8:30am CAD Core Retail Sales m/m

- 11:00am USD Crude Oil Inventories

- 4:45pm NZD Retail Sales q/q

Friday, February 23

- 8:30am CAD CPI m/m

*All times EST