Here are the latest developments in global markets:

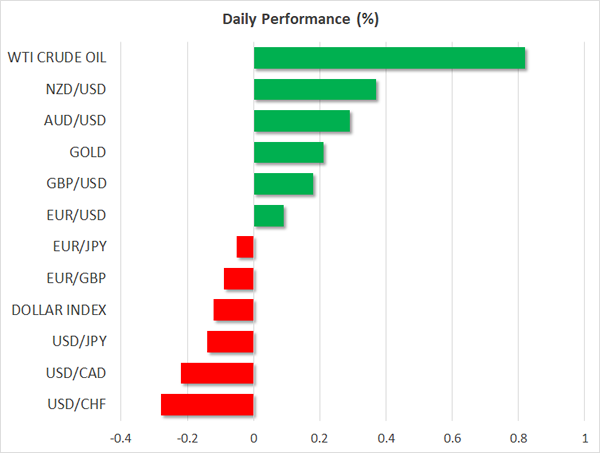

FOREX: The dollar index traded marginally lower on Thursday, extending the significant losses it posted on Wednesday. Meanwhile, the British pound skyrocketed, supported by strong jobs data and increasing optimism that Britain can secure a favorable Brexit deal.

STOCKS: Asian markets were mostly in the red. Japan’s Nikkei 225 and Topix indices fell 1.1% and 0.9% respectively, weighed on by the risk of an escalation in US-China trade tensions and a stronger JPY, which negatively affects Japanese exporting firms. In Hong Kong, the Hang Seng corrected lower by 0.8%, while in Europe, futures tracking the Euro stoxx 50 suggest the index could open slightly lower. Over in the US, the S&P 500 and Nasdaq composite closed in negative territory. Nonetheless, the Dow Jones managed to end the day slightly higher. Futures tracking the Dow, S&P and Nasdaq 100 are all currently in the red, albeit marginally.

COMMODITIES: Oil prices shot through the roof yesterday, and moved even higher today, with WTI and Brent crude trading 0.8% and 0.5% higher respectively during the Asian trading session Thursday, reaching fresh multi-year highs. The advance came after the weekly EIA inventory data showed a drawdown in US crude stockpiles for the tenth straight week. The broad USD weakness probably helped the move too, as a softer greenback makes the dollar-denominated oil appear more attractive for foreign buyers. In precious metals, gold is 0.2% higher, extending the gains it posted yesterday, also buoyed by the softer dollar.

Major movers: Cable touches 1.43; Mnuchin talks down the dollar

Sterling bulls were an unstoppable force yesterday. Sterling/dollar skyrocketed to briefly break above the 1.4300 zone, before pulling back a little during the early European morning Thursday. The move began after the publication of stronger-than-anticipated UK employment data for November, and was exacerbated by the dollar’s weakness throughout the day. Some optimistic comments from Brexit minister David Davis that he expects a transitional Brexit deal before the end of March may have played a role as well. The Brexit risk premium on the pound seems to have declined substantially, and although that may be a little premature considering the absence of major developments in the negotiations, momentum is clearly in favor of the GBP at the moment.

The collapse of the US dollar continued yesterday, with the dollar index reaching a fresh multi-year low at 89.10. The catalyst for the selloff were some comments from US Treasury Secretary Steven Mnuchin. Speaking at the World Economic Forum in Davos, he talked down the currency by indicating that “a weaker dollar is good for us”. Coming on top of concerns around protectionism and the risk of a trade war with China, Mnuchin’s comments likely gave traders another reason to trim their long-dollar positions.

Euro/dollar surged on the back of the dollar’s weakness, breaking above the 1.2400 zone. Today, investors turn their attention to the ECB policy meeting, where there is a risk that President Draghi echoes recent remarks from his colleagues and expresses discomfort with the recent strength of the euro, triggering a correction lower. However, even in that case, any dip in euro/dollar could remain relatively short-lived, considering the increasing pessimism around the dollar. For the pair to stay down, Draghi & Co may need to deliver something more than simply talking down the currency.

Elsewhere, the NZD plunged overnight before recovering somewhat, after New Zealand’s inflation surprisingly slowed in the fourth quarter. The CPI rate came 1.6% in yearly terms, notably below the forecast for staying unchanged at 1.9%. The disappointment likely scaled back expectations regarding the prospect of a rate hike from the RBNZ this year.

Day ahead: ECB decides on monetary policy; Japanese inflation pending in Asia session

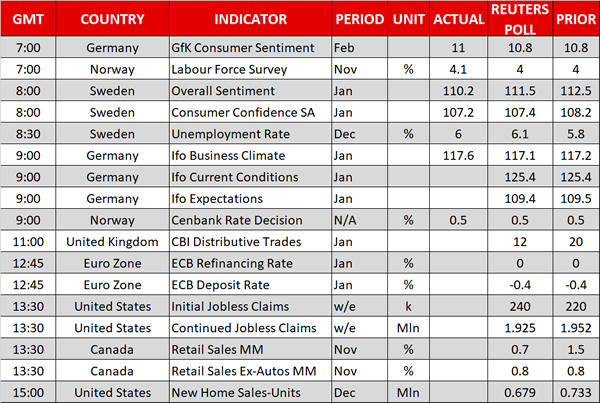

Thursday will be a relatively busy day for FX markets as several economies are expected to release economic figures, while eyes will be mainly focused in the Eurozone where the ECB will meet to decide on monetary policy.

At 1245 GMT, ECB policymakers are widely expected to keep interest rates unchanged at 0.0%. However, what could shake the euro is the press conference following the meeting at 1330 GMT where investors will be eager to hear any comments on the central bank’s quantitative easing program and its appetite to make future changes on the plan. In addition, views on the strengthening euro are also anticipated to attract attention.

Earlier, Norway’s central bank, the Norges Bank, is also projected to maintain rates at record lows of 0.5%. Still, this is likely to bring moderate volatility to the Norwegian Krona as in the previous meeting, policymakers signaled that a rate hike is likely to come only in December.

Out of Europe, monthly retail sales in Canada – due at 1330 – are said to slow down in November, growing by 0.8% compared to a rise of 1.5% seen in the previous month, while excluding automobiles the measure is forecasted to grow at October’s pace of 0.8%. Meanwhile, in the US, initial jobless claims are seen slightly higher at 240,000 in the week ending January 19, though, data on the US new home sales available at 1500 GMT might be of greater importance to the dollar. Particularly, forecasts are for a large decline of -7.9% m/m in December after the gauge posted the biggest expansion rate since 2013, jumping by 17.5% m/m in November.

Late in the day, Japan will report on inflation for the month of December at 2330 GMT, with the potential to extend or reverse the yen’s recent rally if the results deviate far from the forecasts. According to Reuters forecasts, the core CPI which is closely watched by the BoJ is projected to remain flat at 0.9% y/y.

In stock markets, Caterpillar, 3M Company and Union Pacific Corporation are among companies to report on quarterly earnings prior to the US market Open.

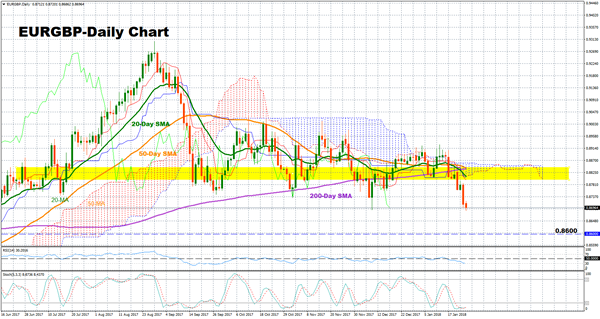

Technical analysis – EURGBP close to oversold levels; bearish in short-term

EURGBP holds a bearish bias in the short-term as prices are currently trading below the Ichimoku cloud and the simple moving average lines (SMA). However, momentum indicators suggest that the market might be oversold, hinting that a trend reversal might emerge in the near-term. The RSI is slightly above 30 and Stochastics are already well below 20 but both indicators have flattened out, meaning that the market might keep consolidating before a potential trend reversal occurs.

Should prices head down, immediate support is likely to come from the 0.8600 key level, exiting the medium-term neutral phase. Steeper declines would also target the area between 0.8400-0.8500.

On the flip side, if the pair moves higher, resistance might come first from the 0.8700 handle before the market finds a stronger barrier between the Tenkan sen (0.8800) line and the 50-day SMA (0.8844).