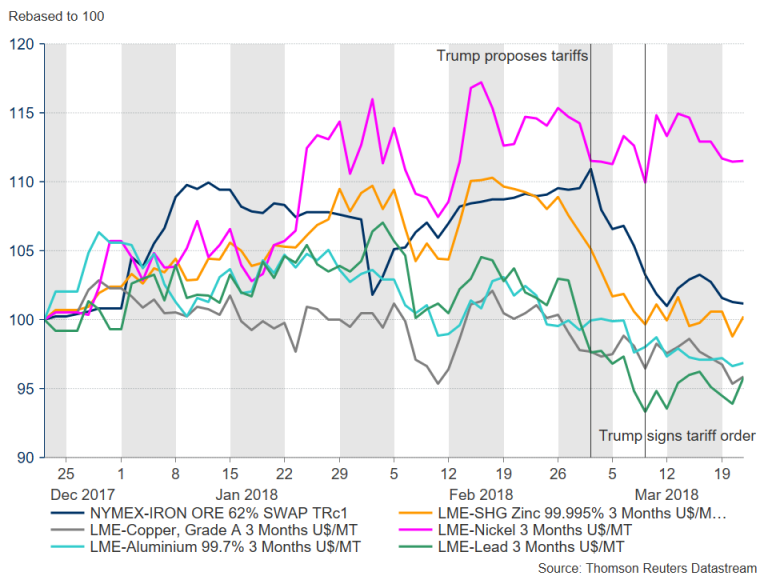

After an impressive two-year rally, industrial metal prices have been having a stormier time in 2018, being first swept over by the market turbulence caused by the sell-off in global equities and bonds, then by the announcement by US President Donald Trump that he is imposing tariffs on US imports of steel and aluminium. Commodity-linked currencies such as the Australian dollar have also been pulled lower by the market volatility and subsequent rise in risk aversion.

However, despite an international outcry by governments and industry leaders against the tariffs, which has stoked fears of a global trade war, there’s been no dramatic sell-off in industrial metals as of yet, with the declines being more attuned to a technical correction than signalling the start of a new bearish phase.

The announcement on March 8 that the United States will be slapping 25% tariffs on steel imports and 10% on aluminium was a hugely symbolic move by President Trump that he intends to see through his election campaign promises. But reaction in financial markets was far more restrained than one would have anticipated. Although the bigger sell-off actually came within the preceding days when reports of the tariffs first started circulating, events and developments after the announcement helped contain steeper declines.

Iron ore – the main alloy used in steel – has been one of the bigger casualties of the tariffs. It fell by around 7% in the days leading to the official announcement of the tariffs and has since declined by a further 2% to near three-month lows. However, iron ore’s troubles are part of a wider problem in the steel industry relating to overcapacity and rising inventories in China.

Iron ore – the main alloy used in steel – has been one of the bigger casualties of the tariffs. It fell by around 7% in the days leading to the official announcement of the tariffs and has since declined by a further 2% to near three-month lows. However, iron ore’s troubles are part of a wider problem in the steel industry relating to overcapacity and rising inventories in China.

Imports of iron ore by China fell sharply in February, contributing to the sell-off. However, China’s monthly trade figures were overall positive as exports surged by 44.5%, providing support to wider commodity prices. Other data out of China also surprised to the upside, including better-than-expected manufacturing PMI and industrial output in February, helping commodity prices stabilize. In addition, exemptions from the tariffs for some countries, including Australia, provided a further cushion for the market from a sharper sell-off.

There should be some support for iron ore prices too if the US tariffs push up steel prices in the short term. (US steel prices have already started to rise on the prospect of a higher import tax). However, longer-term gains are unlikely as higher prices would eventually start to dent demand. The impact on aluminium is expected to be even more limited given the smaller size of the tariff and the fact that US imports account for just 7% of global output.

What happens next though will not only depend on whether or not the trade tensions escalate into a more serious and wider global trade war, but on demand as well. The value of the US dollar is another factor to consider in this equation as a weaker greenback is generally positive for commodities. The weakening dollar in 2017 fuelled the rally in commodities that’s been mostly driven by the improving outlook of the global economy.

However, this bullish outlook appeared at risk even before the US tariffs came into play as rising prices have led to increased supply, with inventories of many base metals such as copper, zinc and aluminium recording strong gains at the start of the year. Even for metals like nickel where stocks have been falling, an expected supply increase and softer demand in China should curb any sharp rise in prices. While most base metals remain above their moving averages, they are at risk of entering bearish territory, and with a possible trade war hanging over the market, it may be difficult for investor sentiment to change in the near term.

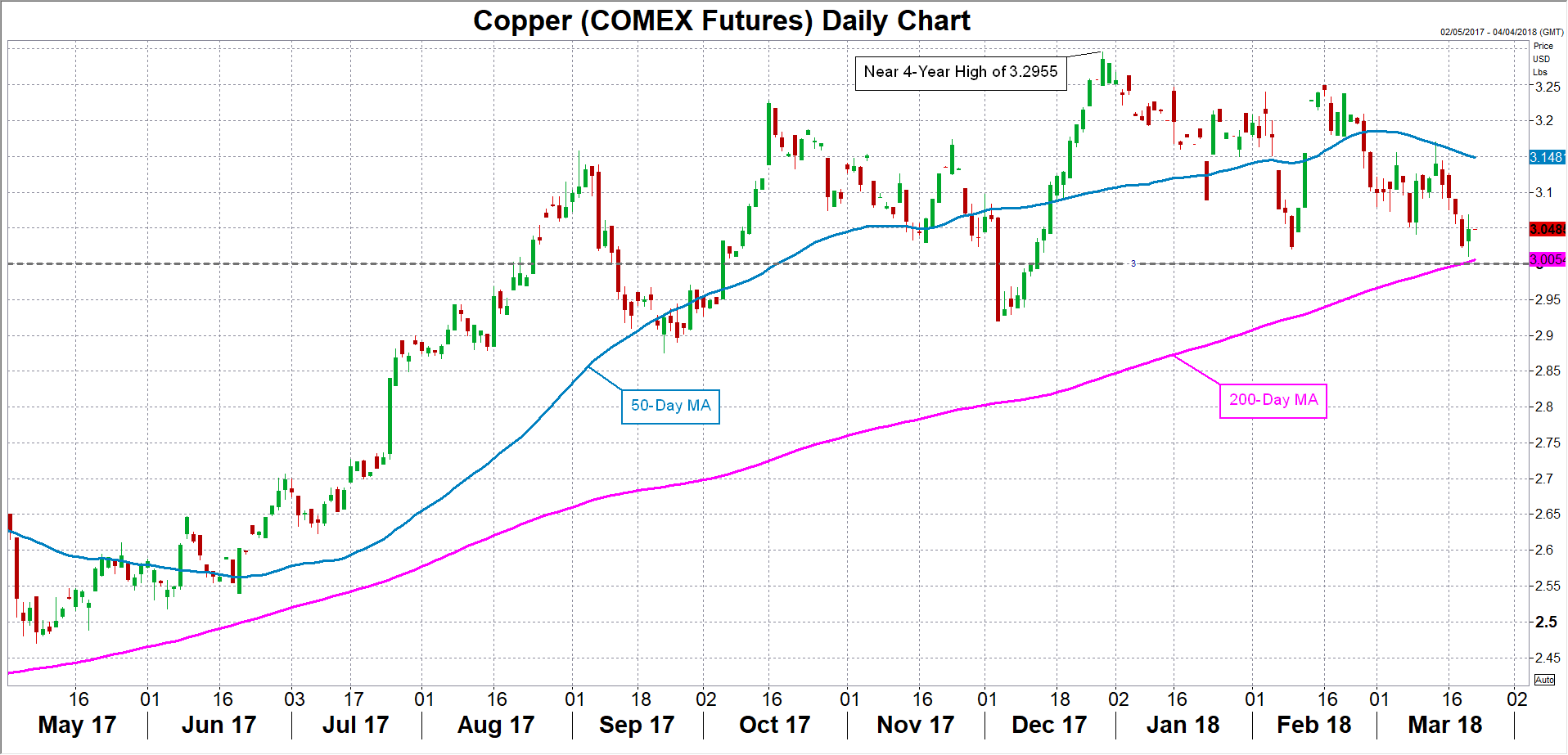

One of the most vulnerabe to a downside reversal is copper. The red metal is currently flirting with its 200-day moving average (MA). Failure to find support at the 200-MA just above the $3.00 per pound level could lead to deeper losses for copper. If the bearish sentiment was to spread to other metals, this could have a spill over effect in forex markets, particularly on the Australian dollar.

One of the most vulnerabe to a downside reversal is copper. The red metal is currently flirting with its 200-day moving average (MA). Failure to find support at the 200-MA just above the $3.00 per pound level could lead to deeper losses for copper. If the bearish sentiment was to spread to other metals, this could have a spill over effect in forex markets, particularly on the Australian dollar.

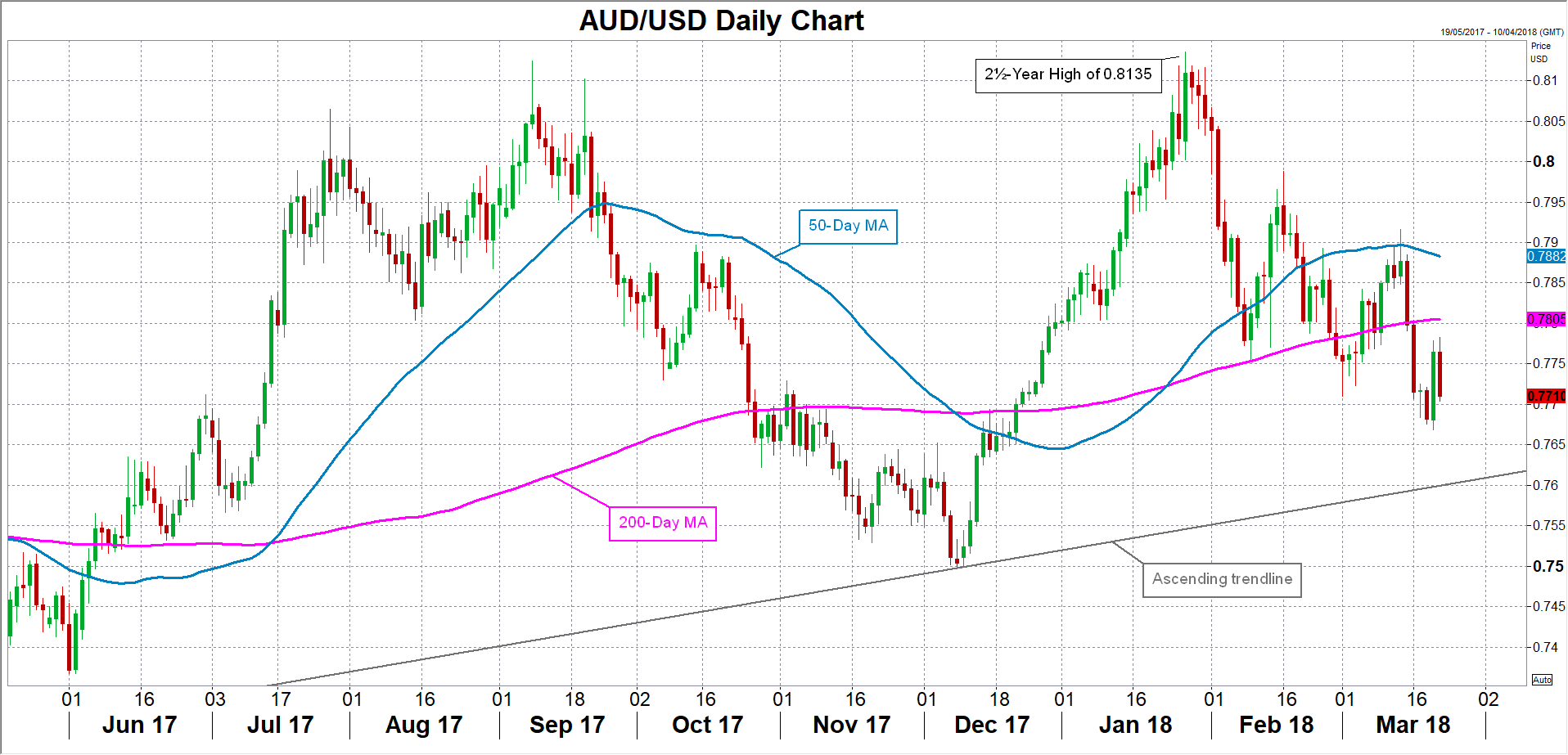

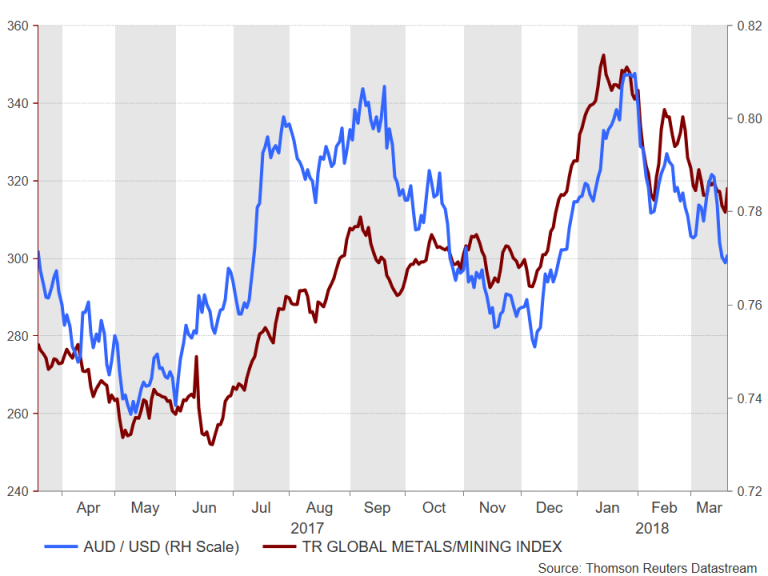

Australia is a major exporter of resources such as iron ore and copper, with China being the main destination. The demand outlook for industrial metals has already been dampened somewhat by expectations that growth in the world’s second largest economy and biggest consumer of commodities will slow in 2018. Should China engage in a trade war with the US, investors are likely to become more pessimistic about the demand outlook for metals, thus hurting the Australian currency.

The aussie has been forming lower highs and lower lows since a two-month old rally came to a halt when it hit a 2½-year high of $0.8135 versus the US dollar in January. Whether this downtrend develops to a longer-term descent could depend to a great extent on how metals perform over the coming months. The Australian dollar has a historically strong correlation with the price of metals and mining stocks. A key support to watch in the coming weeks is the ascending trendline (currently around $0.76) that’s been evolving since early 2016. A breach of this trendline would be a bearish signal for the aussie/dollar.

The aussie has been forming lower highs and lower lows since a two-month old rally came to a halt when it hit a 2½-year high of $0.8135 versus the US dollar in January. Whether this downtrend develops to a longer-term descent could depend to a great extent on how metals perform over the coming months. The Australian dollar has a historically strong correlation with the price of metals and mining stocks. A key support to watch in the coming weeks is the ascending trendline (currently around $0.76) that’s been evolving since early 2016. A breach of this trendline would be a bearish signal for the aussie/dollar.

Traders could be tempted to push the pair to such levels if President Trump, as expected, announces on Thursday, additional tariffs, this time targeting Chinese technology and telecommunications products, as well as intellectual property. The big test will be how China responds to such a move. Retaliatory measures by China and other countries have the potential to damage global trade, and thus, weaken the global economy.

Traders could be tempted to push the pair to such levels if President Trump, as expected, announces on Thursday, additional tariffs, this time targeting Chinese technology and telecommunications products, as well as intellectual property. The big test will be how China responds to such a move. Retaliatory measures by China and other countries have the potential to damage global trade, and thus, weaken the global economy.

It is of course possible that Trump’s actions have the intended effect and compel China to offer more favourable trade terms to US companies. In such a scenario, investors would likely breathe a sigh of relieve and much of the risk-off generated sell-off could be reversed. However, were Trump’s tactics to succeed in achieving a more favourable trading environment for US firms and alleviate the trade war fears, the dollar would likely appreciate under such conditions, offsetting some of the potential gains for commodity prices and commodity-linked currencies.

This only goes to highlight the many headwinds facing the commodities market in 2018. One thing traders should be able to take comfort from however is that in a worst-case scenario, the increasingly solid fundamentals of the global economy should help prevent any downtrend from spiralling out of control.

{kind=link}