Here are the latest developments in global markets:

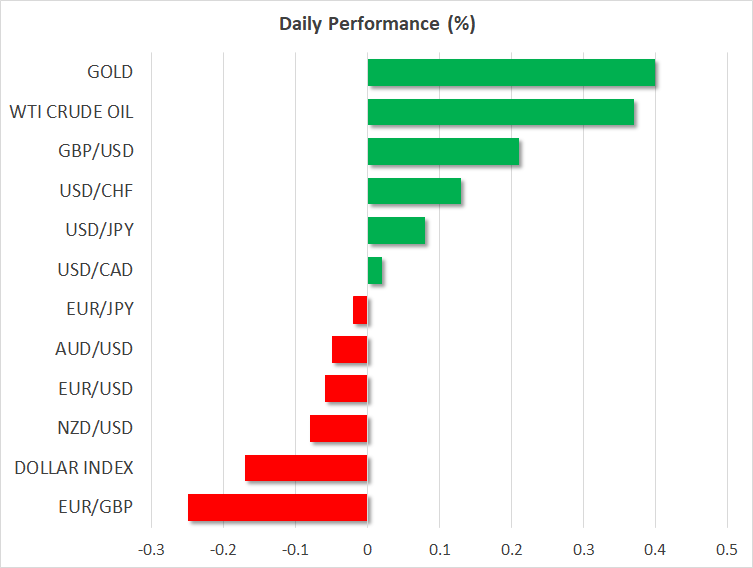

FOREX: The dollar index was nearly 0.2% lower on Monday to start the new quarter, amid continued concerns over a US-China trade dispute escalating following the latest tariffs by China, due to take effect today. The British pound was on the front foot, gaining against both the dollar and the euro, extending the significant gains it posted in the first quarter amid a reduction in Brexit uncertainties.

STOCK: US markets remained closed on Friday, in celebration of the Good Friday holiday. Trading will resume today in the US, and futures tracking the S&P 500, Dow Jones, and Nasdaq 100 are all currently in negative territory, signaling a lower open for these indices, possibly due to the announcement of new tariffs by China against the US. In Asia, Japanese indices started the quarter on a soft footing, with the Nikkei 225 and Topix declining by 0.31% and 0.44% respectively. Other Asian markets, like Hong Kong, stayed closed both on Friday and today for public holidays. Europe was a similar story, with almost all the major benchmarks set to remain shut today as well, in celebration of the Easter Monday holiday.

COMMODITIES: In energy markets, oil prices are higher to start the quarter, with WTI and Brent crude rising by nearly 0.5% and 0.6% respectively. Factors currently supporting prices include speculation that US production may be slowing down a little, following the latest Baker Hughes rig count showing a decline in active rigs, as well as expectations that the US could introduce fresh sanctions on Iran. In precious metals, gold is 0.4% higher on Monday, recouping some of the losses it posted in the prior week.

Major movers: Trade concerns back in the forefront as China slaps tariffs on the US

The US dollar index was slightly lower today, as the “trade war” saga got a new chapter. Effective today, China introduced extra tariffs of up to 25% on several US goods including food and wine, in response to the US tariffs on steel and aluminum. While the market response has not been massive so far, this is a particularly important development, as China is sending the message that it’s not hesitant to play the “tit-for-tat” game with the US.

The key question now for markets is whether, and how, the US will respond. Any announcement of fresh US countermeasures would further increase the risk of a retaliatory trade dispute escalating out of control, and could therefore take its toll on risk appetite. Such an outcome may spell more troubles for equities. Overall, risk sentiment is highly fragile at the moment and for it to recover, markets may need to see signs that this situation is simply a prelude to serious trade negotiations between the US and China, and not the beginning of something bigger.

The British pound was higher, gaining 0.20% and 0.25% against the dollar and euro respectively, with no clear fundamental catalyst behind the move.

Elsewhere, the yen remained largely unaffected by the BoJ’s Tankan survey for Q1 overnight, perhaps due to the mixed batch of data. Although most of the small-business indices beat their forecasts, most large-business prints disappointed. The results suggest that while Japan’s largest firms are still optimistic about the future, there are some signs of anxiety, particularly among big manufacturers.

Overall, there was very little to suggest any change in tone by the BoJ is imminent. As for the yen, the new Japanese fiscal year starts today. This is a period typically associated with Japanese funds moving money out of Japan, which in isolation, is a factor arguing for a weaker yen. Of course, the currency’s performance will also depend on any developments on the trade front, given the yen’s status as a safe-haven that strengthens when global uncertainties are riding high.

As for the antipodeans, both aussie/dollar and kiwi/dollar were marginally lower, perhaps due to the disappointing Chinese Caixin manufacturing PMI overnight.

Day ahead: Trade tensions remain in the spotlight; US ISM Manufacturing index set to lose steam

With Canadian, Australian and most of the European trading centers still being shut for Easter holidays, the focus will turn to the US where Easter Monday is not a public holiday and the economic calendar has some data to deliver today.

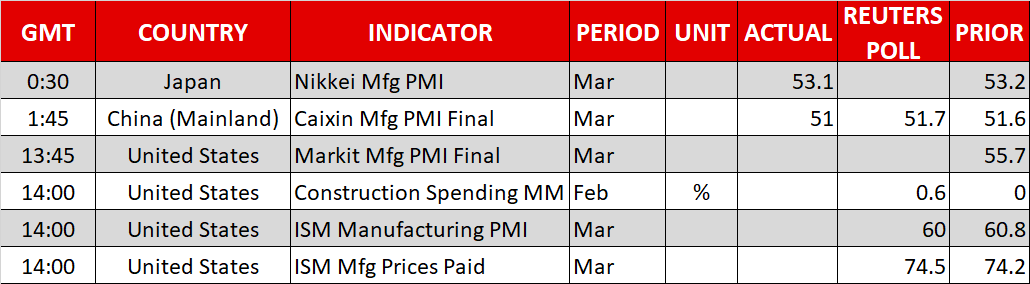

Particularly, at 1400 GMT, the Institute of Supply Management (ISM) will release the US Manufacturing PMI, with the index expected to decline from a 14-year high of 60.8, to 60.0 in March. However, as long as the index remains above 50, the sector is seen as being in expansion. Earlier, at 1345 GMT, the final Markit Manufacturing figure will also attract attention.

Still, the dollar might be more sensitive to any trade headlines that could deteriorate or ease trade tensions between the US and China following China’s decision on Sunday to retaliate to the US import tariffs on steel and aluminum. Investors were somewhat relieved during the previous weeks that things could work out between the countries, after US and Chinese officials showed their willingness to start with negotiations. But yesterday’s news brought new headaches to traders who are now concerned that the sell-off in stock markets might stretch to the second quarter, while safe-haven assets including the yen and gold might experience further demand. Friday’s nonfarm payrolls report could provide support to the dollar if the numbers indicate a tighter labor market, probably showing a fall in the unemployment rate and an acceleration in wage growth. Still, until then, the greenback could remain under pressure if trade tensions intensify in the following days, amid speculation that a global trade war could be around the corner.

Technical analysis – Gold heads up but risks remain on the downside

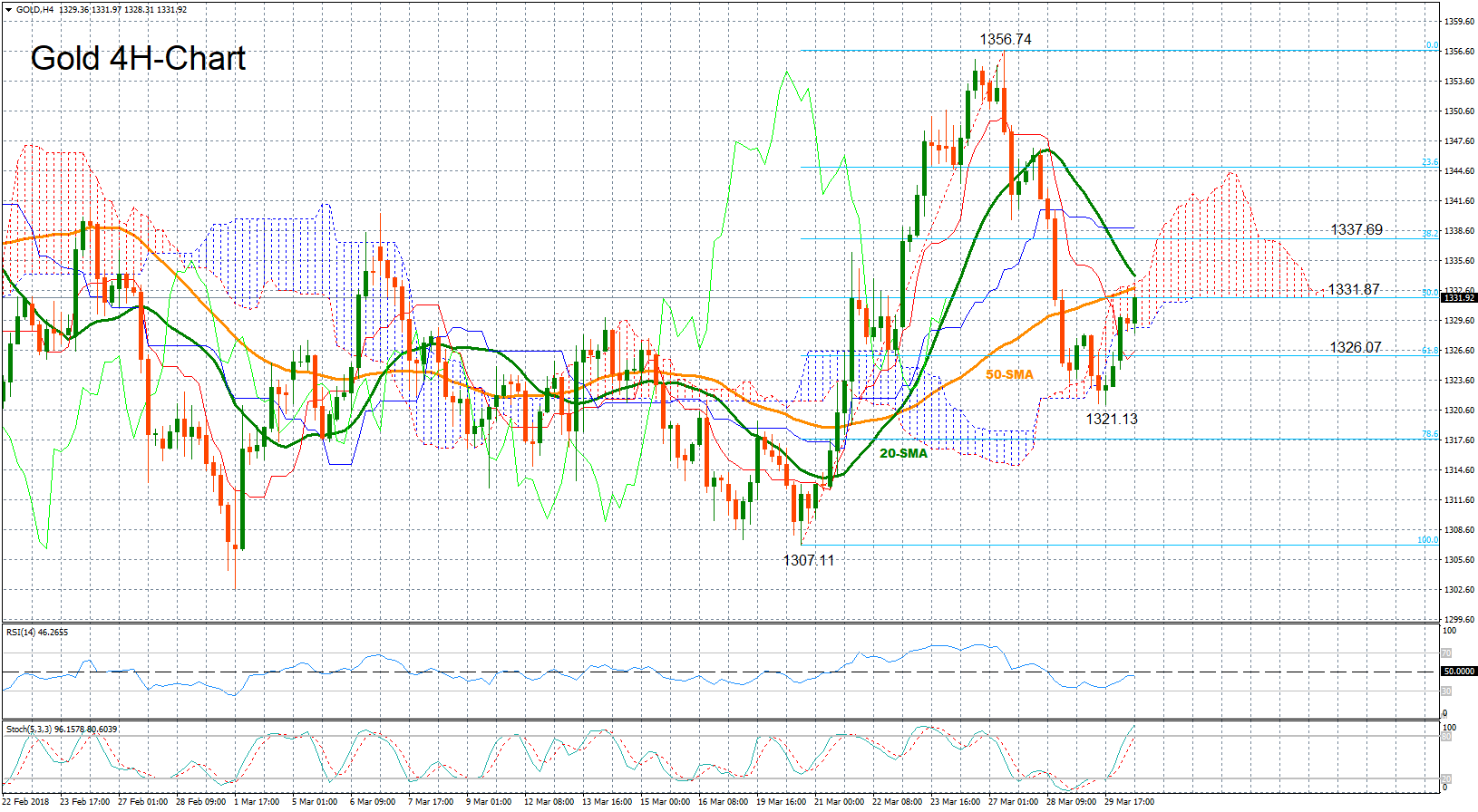

Gold increased its positive momentum on Monday as the dollar was on the back foot, but the sentiment in the market remains bearish in the four-hour chart given that the RSI is still trending below 50, while stochastics are on track to post a bearish cross in overbought territory.

Should risk aversion deepen, the precious metal, which tends to rise when investors are concerned, could crawl up to 1,333 key-level, meeting its 50-period simple moving average before it targets the 20-period SMA at 1,334. Above from there, the next stop could be at 1337.69, which is the 23.6% Fibonacci of the upleg from 1307.11 to 1356.74.

On the downside, any headline that could ease uncertainties around the trade story could push gold down to the 61.8% Fibonacci of 1,326.07, while steeper declines could see a retest of the previous low of 1321.13.

{kind=link}