Here are the latest developments in global markets:

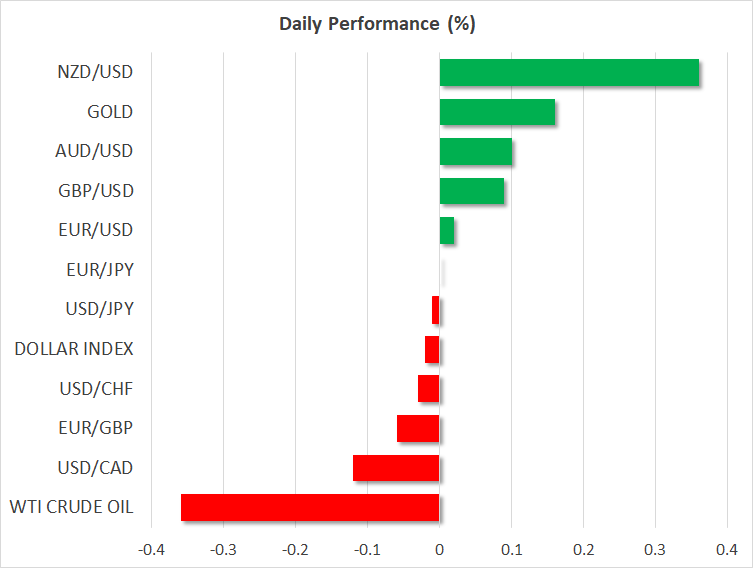

FOREX: The US dollar index was practically unchanged on Wednesday, consolidating after it posted some notable gains yesterday amid a recovery in risk sentiment and a surge in longer-dated US Treasury yields. Kiwi/dollar was among the prime winners today, gaining 0.35%. The loonie surged yesterday as well, on the back of optimism that a NAFTA deal may be reached soon.

STOCKS: US markets recovered sharply, helped by a combination of diminishing risks surrounding Amazon’s outlook and smaller-than-expected US tariffs on Chinese technology exports. The Dow Jones led the rebound, gaining 1.65%, while the S&P 500 and the Nasdaq Composite rose by 1.26% and 1.04% respectively. The S&P 500 managed to climb back above its notorious 200-day moving average. However, the rebound may remain short-lived, as futures tracking the S&P, Dow, and Nasdaq 100 are currently flashing red, pointing to a lower open today. In Asia, Japanese markets followed Wall Street higher but to a much smaller degree, with the Nikkei 225 and the Topix both climbing by roughly 0.1%. In Hong Kong, the Hang Seng was down by 1.1%. As for Europe, futures tracking the major indices are lower, for the most part.

COMMODITIES: In energy markets, oil prices are down today. Both WTI and Brent crude are almost 0.4% lower, unable to draw support from the recovery in equity markets. Oil traders seem to be hesitant to assume new long-positions ahead of today’s weekly EIA crude inventory data, which are projected to show another build in stockpiles, albeit a smaller one than previously. In precious metals, gold is trading 0.15% higher today, recouping some of the losses it posted yesterday in the midst of the risk-on environment.

Major movers: Risk sentiment rebounds despite US tariffs announcement; ball now in China’s court

Risk appetite improved markedly yesterday, evident by the recovery in US stock indices and the losses in safe-haven assets, most notably the yen and gold. The dollar index gained as well, helped by a surge in longer-dated US Treasury yields. The rebound in risk appetite was probably owed to three key factors.

The first was optimism around an imminent NAFTA deal, amid recent reports that the US is pushing for a swift resolution, which helped the loonie regain ground. Secondly, media reports suggested that despite the President’s frequent Twitter outbursts against Amazon, there are no discussions within the White House on how to take action against the company. That pushed Amazon’s stock back into the green (+1.40%), and the rest of the market followed higher. Finally, even though the US announced the details of its technology tariffs against China, the actual size of the tariffs was smaller than previously touted. The US will target Chinese goods worth $50bn, instead of the $60bn that had been rumored, which likely came as a positive surprise and helped ease some concerns that this trade skirmish will escalate much further.

Now, the ball is back in China’s court, and the Asian nation noted it will retaliate with measures of equal intensity and scale. Market chatter suggests China will target US soybean and aircraft exports, bringing into focus companies like plane-maker Boeing. If this is accurate, then another wave of risk-aversion may be in store soon, implying further volatility for equities and safe havens. In the bigger picture though, the overall direction in stock markets could depend on what comes after China retaliates. Will the US announce its own countermeasures and continue playing the tit-for-tat game, or will the two sides sit down at the negotiating table and reach common ground?

In other news, Fed Board Governor Lael Brainard (voter) appeared rather hawkish yesterday, noting that rates will probably rise above the predicted “neutral” level in the coming years due to fiscal stimulus. She is typically on the cautious side of the spectrum, so optimistic comments from her are especially important.

As for the antipodeans, both aussie/dollar and kiwi/dollar are up by 0.1% and 0.35% respectively, boosted by the broader risk-on environment.

Day ahead: Eurozone flash inflation and US ISM non-manufacturing PMI & factory orders on the agenda

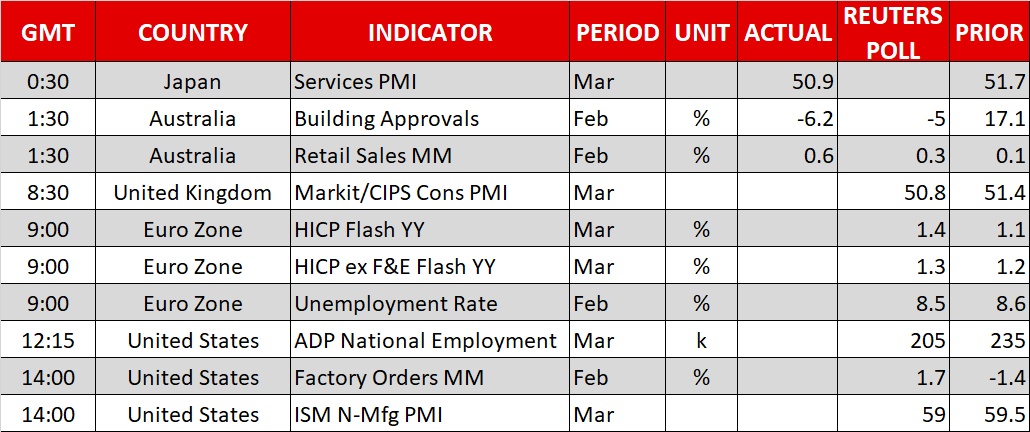

Wednesday’s economic calendar will feature some important releases, including inflation figures out of the eurozone.

At 0830 GMT, the UK’s construction PMI for the month of March will be made public, one day before the corresponding reading for the all-important for the UK economy services sector is released.

The eurozone’s flash inflation figures for the month of March are due at 0900 GMT. The headline Harmonised Index of Consumer Prices (HICP), that uses a common methodology across EU countries, is forecast to rise to 1.4% y/y from February’s 1.1% which constituted the lowest pace of growth for the measure since late 2016. Remarks by ECB policymakers advising against premature tightening – given the inflation rate’s shortfall relative to the Bank’s target of close to but below 2% on a yearly basis – weighed on the common currency recently. A data miss later on the day could further boost such concerns, leading to a weakening euro. The core measures of inflation, that exclude volatile items, will also be watched. February’s unemployment rate out of the eurozone will also be released alongside the numbers for inflation. The rate is projected to decline to 8.5% from the previous 8.6%, hitting its lowest since December 2008.

Releases of importance out of the US include March’s ISM non-manufacturing PMI and February’s factory orders, both scheduled for release at 1400 GMT, while earlier (1215 GMT), the ADP national employment report on the number of positions added to the economy by the private sector during the month of March will also be gathering attention. The latter is viewed by some as a preamble to the non-farm payrolls report (due on Friday) which covers both the public and private sectors.

In energy markets, the weekly EIA crude inventory data at 1430 GMT will be gathering attention, providing fresh indications on the state of US oil production and demand. Crude stockpiles are forecast to have risen by 1.4m barrels in the week ending March 30, less than the 1.6m barrels from the week that preceded.

Any updates on trade have the capacity to drive sentiment in equity markets.

Policymakers making appearances on Wednesday include St. Louis Fed President James Bullard (1345 GMT) and Cleveland Fed President Loretta Mester (1500 GMT). Only the latter is a voting member within the FOMC in 2018.

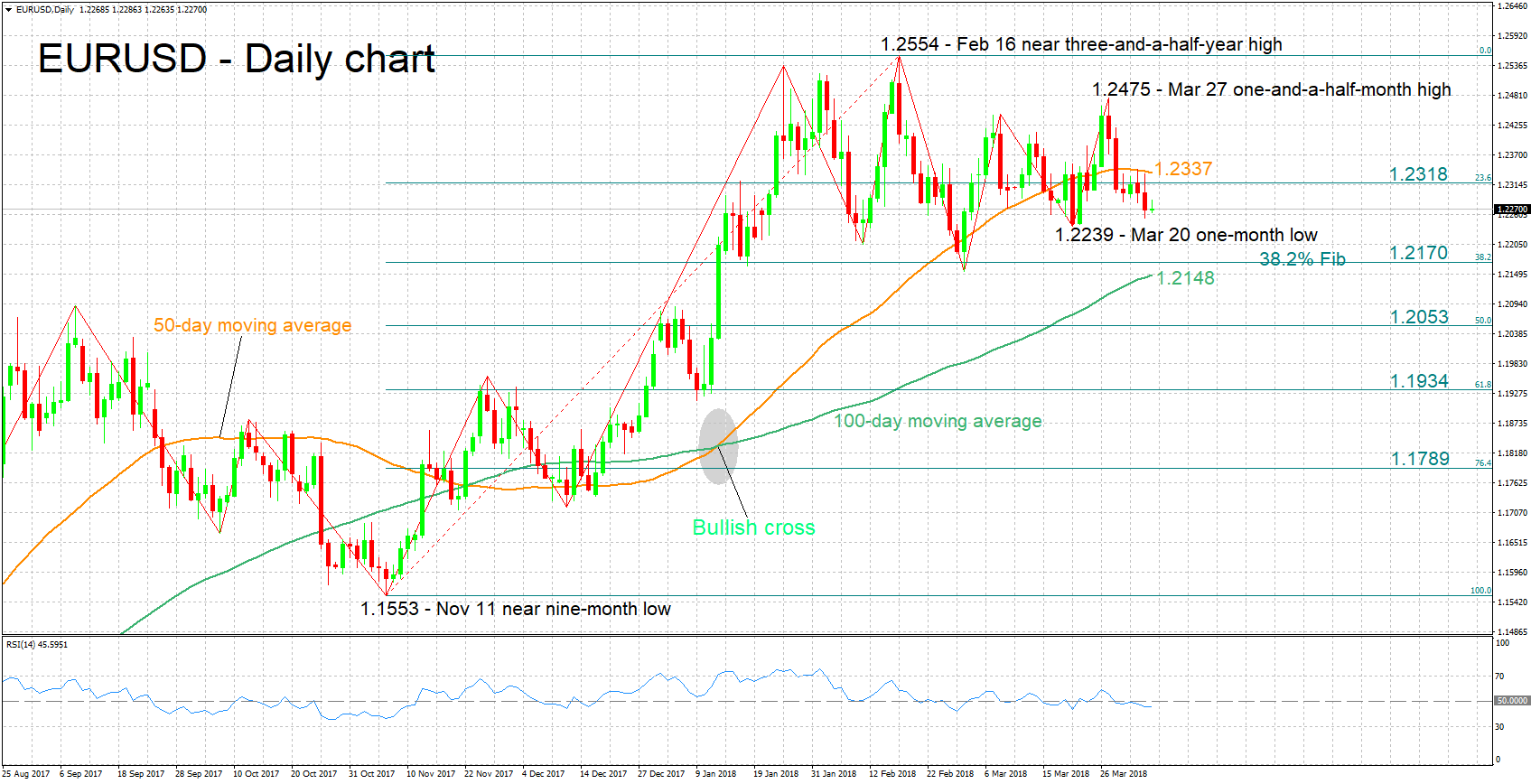

Technical Analysis: EURUSD trades near 2-week low; looking mostly bearish in the short-term

EURUSD has lost significant ground after hitting a one-and-a-half-month high of 1.2475 on March 27, eventually posting a two-week low of 1.2253 during Tuesday’s trading. Price action is currently taking place not far above the aforementioned low. The RSI continues to decline in support of a bearish short-term bias, though it is only moderately negatively sloped at the moment, a sign that negative momentum is not that strong.

Stronger-than-expected inflation figures out of the eurozone later on Wednesday are anticipated to boost the pair, with resistance to advances potentially coming around the 23.6% Fibonacci retracement level of the November 11 to February 16 upleg at 1.2318. The area around this level also includes the 1.23 round figure, as well as the current level of the 50-day moving average at 1.2337.

Conversely, a data miss is likely to be met with selling pressure in EURUSD. Support to declines could initially come around the one-month low of 1.2239 from March 20 – including yesterday’s two-week low of 1.2253 – with steeper falls shifting the focus to the 28.2% Fibonacci mark at 1.2170.