Here are the latest developments in global markets:

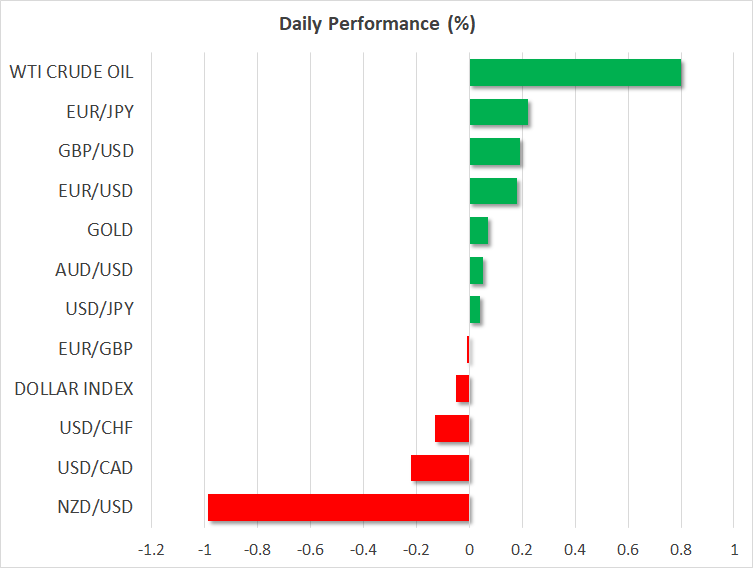

FOREX: The US dollar index was practically flat on Thursday, ahead of the release of the US CPI data for April at 1230 GMT. Kiwi/dollar plunged nearly 1.0% overnight, after the RBNZ kept its policy unchanged but shifted to a more dovish bias, keeping the possibility of a rate cut on the table. Sterling/dollar traded 0.2% higher, as investors awaited the BoE’s rate decision today at 1100 GMT.

STOCKS: Wall Street closed higher yesterday, with energy shares leading the way higher amid a surge in oil prices. The Nasdaq Composite climbed by 1.0%, while the S&P 500 and Dow Jones followed in its tracks, rising by 0.97% and 0.75% respectively. Futures tracking the Dow, S&P, and Nasdaq 100 are also pointing to a higher open today. That said, the performance of these indices today may depend to a large extent on the upcoming US CPI data. Most indices in Asia were in the green as well. Japan’s Nikkei 225 and Topix indices rose by 0.39% and 0.27% correspondingly, while in Hong Kong, the Hang Seng gained 0.96%. In Europe, futures tracking the major benchmarks were also signaling a higher open today, especially for the UK FTSE 100.

COMMODITIES: Oil prices posted another day of spectacular advances on Wednesday, and continued pushing higher today as well, with WTI and Brent crude climbing by 0.8% and 0.7% respectively. Both benchmarks touched fresh multi-year highs. The US decision to leave the Iran nuclear accord, a surprising drawdown in the EIA weekly crude inventories, and reports of armed conflict between Israel and Iran appear to be the main forces behind oil’s latest gains. In precious metals, gold is higher today but by less than 0.1%, recouping some of the losses it posted yesterday. It has been trading in a very narrow range so far this month, between $1,301 and $1,318, largely overlooking reports of rising tensions in the Middle East.

Major movers: Kiwi retreats as RBNZ appears dovish; oil races higher amid geopolitical tensions

Overnight, kiwi/dollar sank nearly 1.0% after the RBNZ kept its policy unchanged but shifted to a more dovish stance, putting the possibility of a rate cut on the table. In the introductory paragraph of the accompanying statement, the new Governor Adrian Orr noted that “the direction of our next move is equally balanced, up or down. Only time and events will tell”. While the prospect of a rate cut appears quite unlikely, this probably signaled the new RBNZ chief will be even more cautious in raising rates than his predecessor, pushing further back rate-hike expectations.

Oil continued racing higher yesterday, as markets digested the US decision to impose new sanctions on Iran and after a surprising drawdown in the weekly EIA inventory data. The surge in crude also boosted the Canadian dollar, which posted a one-week high against its US counterpart.

Turning to geopolitics, safe-haven assets like gold and the yen paid little attention to overnight reports of hostility between Israel and Iran. The Israeli military carried out strikes against Iranian targets in Syria, after Iranian forces launched a rocket attack on Israeli army bases, Israel said. This marks a direct confrontation between the two states, raising the risk of greater escalation just hours after the US withdrew from the Iran deal. While safe havens didn’t react, these reports may have been one of the factors behind oil’s rally. Overall, this story is worth watching closely, as any further tensions could carry wider implications for the region’s stability and consequently, for oil supply moving forward.

Day ahead: BoE decides; US CPI due; geopolitics still a play

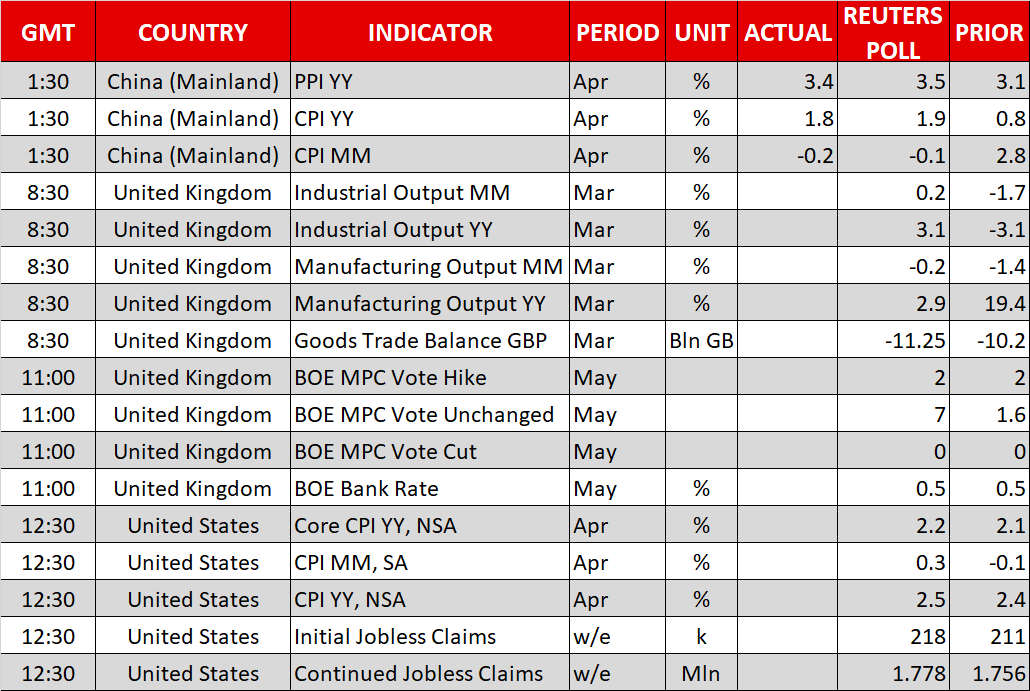

The Bank of England’s decision on interest rates and US inflation figures are expected to be the most market-sensitive events out of Thursday’s calendar, leading to positioning in FX markets.

At 1100 GMT, the Bank of England’s rate decision will be made public, with the meeting minutes and the Bank’s Inflation Report also released at the same time. Markets widely expect the central bank to maintain its base rate unchanged. It’s communication and the number of Monetary Policy Committee (MPC) members voting for a rate hike though, will determine sterling’s movement. Polls suggest a 7-2 vote in favor of rates remaining at current levels. More dissenters (i.e. more MPC members voting for a hike) and signaling of a “hawkish hold” that puts a hike firmly on the table in an upcoming meeting, is anticipated to push sterling higher, and vice versa.

Before the focus turning to the BoE, the UK will be on the receiving end of data on the goods trade balance, industrial output and manufacturing output. All data points are due at 0830 GMT and pertain to the month of March. Manufacturing production is forecast to fall by 0.2% m/m, the same as in February, but grow at a faster pace on an annual basis (2.9% vs 2.5% in February).

Later (1230 GMT), the attention will shift to the US which will see the release of April inflation figures, as gauged by the consumer price index (CPI). Both headline and core CPI – the latter being the measure that excludes volatile food and energy items – are expected to accelerate on a yearly basis, growing at their fastest pace in more than a year. Specifically, they’re projected to expand by 2.5% and 2.2% correspondingly. Monthly headline CPI is also expected to return to positive territory after last month’s contraction, which was attributed to transitory factors.

The inflation numbers do not relate to the Fed’s preferred inflation gauge – that being the core PCE price index – but still can stoke expectations of a steeper interest rate outlook by the US central bank in case of an upside surprise. According to Fed fund futures, markets have fully priced in two additional hikes by the Fed in 2018, while they assign a more than 20% chance for an additional move as well. Meanwhile, weekly data on initial and continued jobless claims out of the US will be made public at the same time as CPI numbers (1230 GMT).

Nvidia is among companies releasing quarterly earnings on Thursday. The chipmaker’s results will be made public after today’s closing bell on Wall Street.

Lastly, geopolitical developments are a factor to be looked at, especially after President Trump’s decision to pull out of the Iran nuclear deal and a possible regional conflict-escalation, as Syria (Iranian forces within the country) and Israel appear to be carrying out attacks against one another.

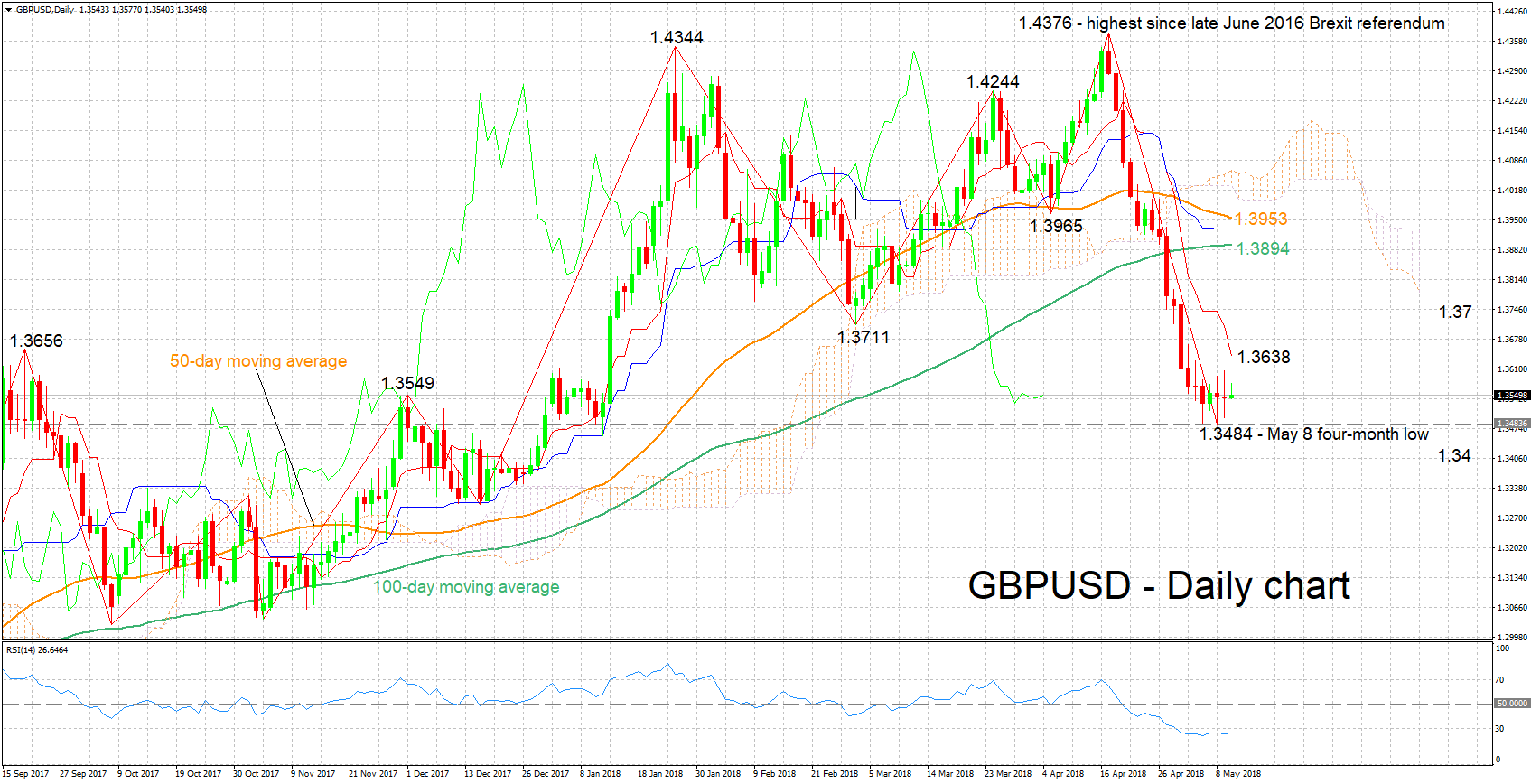

Technical Analysis: GBPUSD short-term bearish; RSI oversold

GBPUSD has contracted considerably after rising to its highest since June 2016 of 1.4376 around mid-April. On Tuesday, it touched a four-month low of 1.3484. The negatively-aligned Tenkan- and Kijun-sen lines are projecting a bearish short-term picture. The Kijun-sen has flatlined though, the implication being that negative momentum is easing. The RSI, which is moving sideways in bearish territory, supports this view as well; notice also that the indicator has entered oversold levels.

A “hawkish hold” by the BoE is anticipated to support the pair, with resistance potentially coming around the current level of the Tenkan-sen at 1.3638 and the 1.37 handle in case of steeper advances.

A dovish tone by the central bank is expected to push GBPUSD lower. Support could emerge around Tuesday’s four-month low of 1.3484 and subsequently the 1.34 handle in the event of sharper losses.

US inflation figures are also likely to spur positioning on the pair.

{kind=link}