Here are the latest developments in global markets:

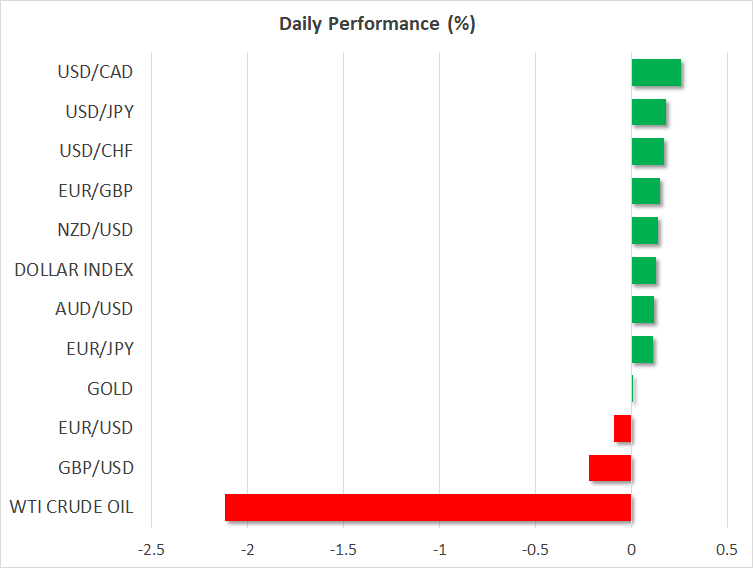

FOREX: The US dollar rose 0.18% versus the yen after three straight days of declines. Meanwhile, the US dollar index jumped by 0.13% to 93.87. Euro/dollar fell by 0.09% and is set to complete the sixth week of declines in a row as concerns over Italy’s debt outlook weighed on sentiment. Pound/dollar moved lower by 0.21% to 1.3347 on Friday as investors eyed UK GDP data for signs of whether the BOE will raise interest rates. The British economy expanded 0.1% q/q in the first three months of 2018 according to updated estimates, in line with the flash estimates and well below the 0.4% in the previous quarter. The antipodean currencies are heading higher with aussie/dollar rising by 0.17% to 0.7587 and kiwi/dollar climbing by 0.17% to 0.6932. Dollar/loonie advanced by 0.24% and is slightly above the 1.2900 handle.

STOCKS: European stocks traded significantly higher during Friday’s session but were on track to finish the week weaker on the back of trade risks and heightened political uncertainty in the Eurozone. The pan-European Stoxx 600 was up 0.37% at 1030 GMT, with almost all sectors in positive territory. The blue-chip Euro STOXX 50 was higher, being up by 0.23% at 1030 GMT. The German DAX 30 surged by 1.00%, while the Italian FTSE MIB 100 declined by 0.28%. The French CAC 40 gained 0.53% and the British FTSE 100 was also in positive territory, jumping by 0.18%. Moreover, the Spanish IBEX 35 moved down by 0.72% as the Spanish Prime Minister could face a no-confidence vote in the coming days (see below). Futures tracking US stock indices were flashing red, pointing to a negative open.

COMMODITIES: Oil prices fell aggressively on Friday as Russia and Saudi Arabia are considering to increase OPEC/non-OPEC supply by 1 million barrels per day on worries the recent rally in oil prices has been overstretched. West Texas Intermediate (WTI) and Brent crude oil plummeted by 1.80% and 1.98%, to $69.44 and $77.25 respectively. Gold struggled below the 200-day simple moving average on Friday after the sharp buying interest yesterday when the US President Donald Trump decided to cancel the meeting with North Korean leader Kim Jong Un. The precious metal moved marginally higher today by 0.08%, at $1,304.90 per ounce.

Day ahead: US durable goods orders pending; eyes on Fed speakers

A few economic releases are scheduled for the remainder of the day, with the spotlight turning to several speeches by a handful of policymakers. Political developments and updates on the trade front are also expected to attract attention in the following days.

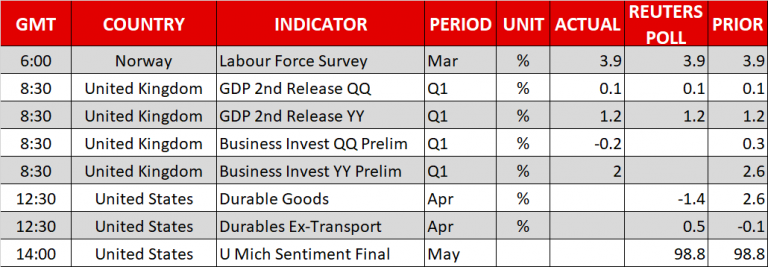

At 1230 GMT, the US will report on new orders for durable goods for the month of April and analysts expect the measure to decline by 1.4% m/m compared to a growth of 2.6% in the previous month. Excluding transportation, though, forecasts are for an expansion of 0.5% m/m compared to a contraction of 0.1% (revised downwards from +0.1%) in March. Later at 1400 GTM, the University of Michigan will publish its final findings on US consumer confidence for May, with the number expected to come at 98.8 as it was initially released.

Besides the data, investors will keep a close eye on any geopolitical headlines. The US President, Donald Trump, decided on Thursday to cancel a planned summit with North Korea’s Kim Jong Un scheduled for June 12, due to North Korea’s recent “tremendous anger and hostility”. North Korea perhaps surprisingly responded with a measured tone, expressing instead its willingness to meet with US officials at any time. This helped turn stock markets back to the upside after a strong sell-off in the wake of the news and tempered demand for safe havens.

Trade developments will be of interest as well since fears over a global trade war have not faded yet. Although the US and China agreed to put trade frictions on hold, Trump expressed his dissatisfaction a few days after, stressing that talks with China need a “different structure”. At the same time, his request to start an investigation into automobiles imports, which would significantly affect EU companies, raised speculation that further tariff threats by the US could come in play.

Meanwhile, uncertainties around Italy’s potential fiscal reforms under the new coalition government could continue to weigh on the euro, while political conditions in Spain are likely to attract attention after sources stated that the Socialists, the biggest opposition party, were planning for a no-confidence vote against the Spanish Prime Minister, Mariano Rajoy. The announcement came after the Spanish Court delivered fines and prison sentences to Rajoy’s conservative party members over illegal practices.

In oil markets, the Baker Hughes report on the number of US oil rigs due out at 1700 GMT has the potential to move oil prices.

As for today’s public appearances, Fed Chair, Jerome Powell, will be participating in the panel discussion on “Financial Stability and Central Bank Transparency” before the Sveriges Riksbank Conference in Sweden at 1320 GMT. Elsewhere, regional Fed presidents, Raphael Bostic, Charles Evans and Robert Kaplan will be making comments before the Federal Reserve Banks of Dallas and Atlanta “Technology-Enabled Disruption: Implications for Business, Labor Markets and Monetary Policy” conference at 1545 GMT. Kaplan will be also giving closing remarks at the conference at 1830 GMT.

On Saturday, the Russian President, Vladimir Putin, will be holding a meeting with the Japanese Prime Minister, Shinzo Abe.