U.S. Highlights

- The first full week of the second quarter was sparse on economic data. The service sector showed signs of modest acceleration, while vehicle sales declined for the second consecutive month in March.

- The Federal Open Market Committee (FOMC) March meeting minutes reiterated members’ unwavering commitment to moving fast to restore price stability.

- The minutes provided a blueprint of the Fed’s balance sheet runoff, which will be more aggressive and ramp up faster than before. At such pace, the runoff should finish by the end of 2024.

Canadian Highlights

- The economic news was non-stop this week, from the Business Outlook Survey, to the Federal Budget, and capping it off with another banner jobs number.

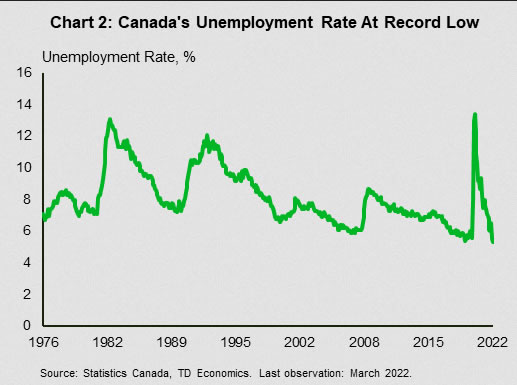

- The job market keeps getting tighter, with the unemployment rate reaching a series low of 5.3%. Wage growth is picking up but remains slightly lower than the latter half of 2019.

- Combined with strong business sentiment, and a steady federal fiscal picture, it is all systems go for a rate hike next week. Given inflation and economic strength, a 50 basis-point move is justified.

U.S. – The Fed’s Most Important Task

The first full week of the second quarter was sparse on economic data. On Tuesday, the Institute for Supply Management released its report on services that provided signs of modest acceleration in economic activity in the sector. Still, the report was full of contrasting elements. On the one hand, demand indicators were higher with business activity, and both new domestic and export orders up on the month. This was likely supported by stronger employment and the recent improvement in delivery times allowing businesses to rebuild depleted inventories.

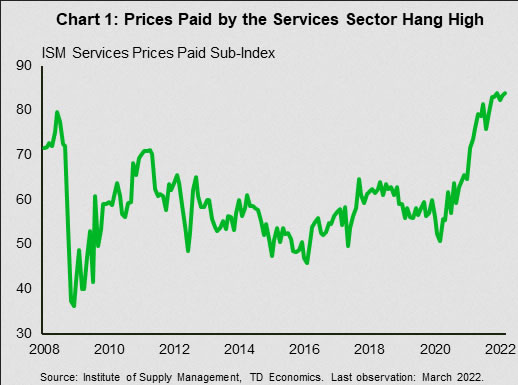

On the other hand, the imports sub-index fell into a contractionary territory while ongoing supply chain issued lowered purchasing managers’ inventory sentiment to an all-time low. The prices paid indicator was unsurprisingly higher given the energy shock dealt by the Russia-Ukraine war with all 18 industries reporting higher prices (Chart 1). In addition, respondents’ comments were quite negative, reflecting the pessimism over increasing cost and ongoing supply chain disruption.

This pessimism was echoed in the vehicle sales release, which showed the second consecutive month of decline in March. While underlying demand remains strong and improving, sales will remain constrained by limited inventory. Furthermore, production may suffer another blow should the war in Ukraine result in semiconductor shortages later in this year. As a result of strong demand and tight supply, the inventory-to-sales ratio – a measure of adequacy of supply relative to current demand – remains historically low. This will continue to put upward pressure on car prices over the near-term.

Fighting persistent price pressures remains the Fed’s most important task. The Federal Open Market Committee (FOMC) March meeting minutes reiterated members’’ unwavering commitment to moving fast to restore price stability and reach a neutral policy stance by year end. Many participants expressed their concerns about inflationary risk and voiced their preference to tighten the policy rate by 50 basis points at the next meeting on May 3rd-4th.

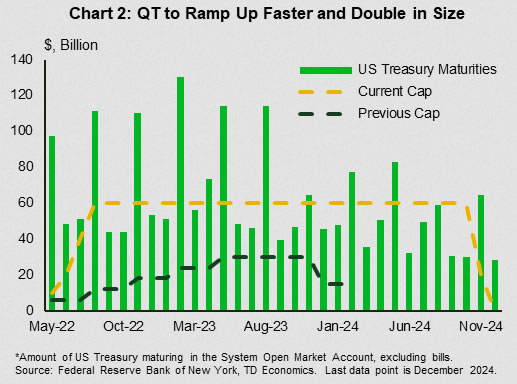

Chart 2 shows the dollar amount of maturing U.S. Treasuries (in billions) in the System Open Market Account (SOMA) from March 2022 to December 2024 alongside the series for monthly cap of the previous runoff cycle of 2017-2019 and the one expected this time. In the previous cycle the Fed limited the caps to $6 billion per month, steadily raising the level to $30 billion over the period of 12 months, and then reducing it to $15 billion in 2019. This time the Fed is expected to phase-in within three months reaching the cap of $60 billion – double the maximum size of the previous runoff cycle.

The minutes also provided a plan for the Fed’s balance sheet runoff (aka Quantitative Tightening or QT). As we wrote in this report, the monthly caps will be larger than in the previous QT cycle, scaled up by the increase in asset holdings (Chart 2). The participants agreed to shed $60 billion Treasury securities and about $35 billion agency MBS monthly, but the phase-in period will be shorter than we expected at just three months. The runoff may start as early as May, which suggests that the balance sheet could shrink by $2.7 trillion by the end of 2024. By this time, we expect that the Fed will reach $1.7 trillion in reserves – the level of reserves “consistent with the Committee’s ample-reserves operating framework”.

Bond markets reacted by selling longer-dated US Treasury securities, which led to yield-curve steepening. At the time of writing, the 10-year Treasury yield was at 2.69% – up 0.3 percentage points relative to where it closed last week.

Canada – Rate Hikes Ahead

The economic news was non-stop this week, from the Business Outlook Survey, to the Federal Budget, and capping it off with another banner jobs number. The overall takeaway is there was nothing in any of it to give the Bank of Canada pause before raising rates by half a point next Wednesday.

The Bank of Canada’s Business Outlook Survey showed that firms remained quite upbeat about the outlook. Investment intentions remained elevated and labour markets remained tight – a pain point for businesses, but a sign of a healthy economy. The survey was largely conducted before Russia invaded Ukraine, though a recent special survey indicated, not surprisingly, that businesses expect the war to add to inflationary pressures through higher input costs. The lower-profile companion survey on consumer expectations echoed the same themes – strong labour markets and inflation worries. However, spending intentions remained strong, and the probability that people would quit their jobs in the next year rose to a series high of 22%.

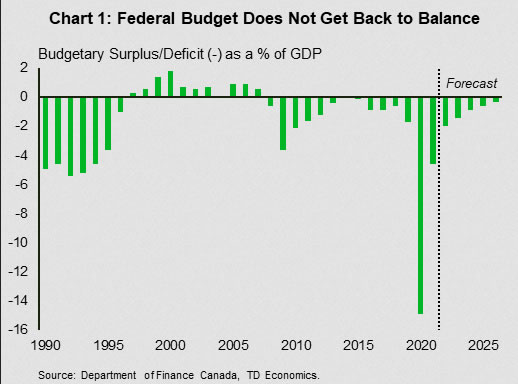

One economic player that inflation is helping is the federal government, where higher inflation has improved the fiscal outlook presented in Budget 2022 relative to what was presented in the Fall Economic Statement (see analysis). However, the budget does not get back to black over the forecast horizon, thanks to close to $60 billion in additional spending (Chart 1). The Federal debt-to-GDP ratio remains on a downward trajectory, however, due to a growing economy.

New spending measures were spread across priorities on housing, climate and environmental action, childcare, defense, dental care, and measures to further reconciliation with Indigenous peoples. Revenue raising measures were targeted: a tax on large financial institutions and increased efforts to close tax loopholes are expected to generate $17 billion over five years.

Topping off the week, March’s employment data revealed that Canada’s job market shows no sign of cooling down, with 73k new jobs created. The unemployment rate fell even lower, to 5.3% – the lowest level since comparable data became available in 1976. Not surprisingly, wage growth has also picked up, with average hourly wage growth up 3.4% versus a year ago. Abstracting from the distortions in wages over the pandemic – as job losses were skewed to lower wage positions, lifting the average – wage growth is still not as strong as it was in late 2019. Wage growth is also not keeping pace with inflation, which was 5.7% year/year in February. But, with the labour market this tight, wage growth is sure to heat up.

The Bank of Canada is widely expected to raise rates 50 basis points next Wednesday. It would be an aggressive move by the Bank, which has only hiked in 25 basis point increments over the past 20 years. Given the hot economy, the move is justified.

{kind=link}