{kind=link}

EUR/GBP is sitting at a key technical and macro junction around 0.86 level as markets head into rate decisions from the ECB and the BoE. While neither meeting is expected to deliver an immediate policy shift, both carry important signals that could shape expectations and positioning in the cross.

Both central banks are widely expected to stand pat. The ECB is set to keep the deposit rate unchanged at 2.00%, while the BoE is expected to leave Bank Rate steady at 3.75%. With these results fully priced in, the focus is firmly on guidance rather than the decisions themselves.

For the ECB, President Christine Lagarde is likely to repeat that policy is in a “good place.” There is little appetite within the Governing Council to debate changes to borrowing costs in the near term, reinforcing expectations of an extended pause.

Near-term inflation has softened, slipping to just 1.7% in January and potentially easing further in coming months. However, that downside surprise has not meaningfully altered the ECB’s broader inflation outlook. One reason is energy. The recent rebound in oil prices, if sustained, would offset much of the disinflationary impact from Euro strength. That reduces any urgency for the ECB to respond to near-term CPI weakness.

Inflation expectations also remain a concern. The ECB’s latest Consumer Expectations Survey showed five-year inflation expectations rising to 2.4% in December, the highest since the survey began. Shorter- and medium-term expectations also edged higher, supporting the ECB’s view that inflation could reaccelerate.

As a result, the ECB appears comfortable with a prolonged pause, with the next move still more likely to be a hike than a cut. One key focus today will be whether Lagarde references recent Dollar weakness and the EUR/USD exchange rate, particularly around the recently tested 1.20 level.

In the UK, the policy picture is more fractured. The BoE’s December rate cut passed by a narrow 5–4 vote, underscoring deep divisions within the Monetary Policy Committee. UK inflation remains elevated, with December’s 3.4% reading the highest among G7 economies. While inflation is expected to move back toward the 2% target, some policymakers remain concerned that underlying pressures are still too strong.

Market pricing reflects that caution. Investors largely expect no move until at least April, and possibly not until July, a much slower pace of easing than seen in 2025. As usual, the MPC vote split will be closely watched for clues on the balance between hawks and doves.

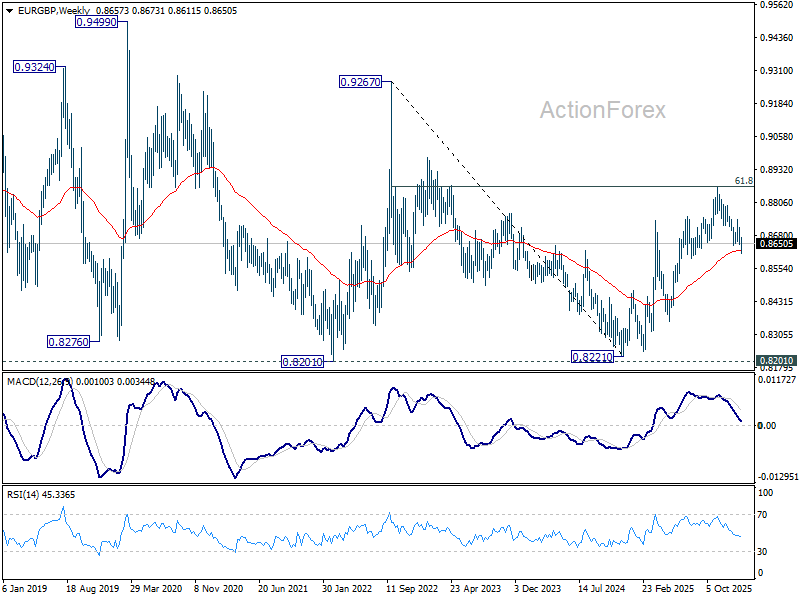

Technically, EUR/GBP is testing a critical support cluster near 0.86. The favored view is that the rebound from the 0.8221 (2024 low was corrective) and may have completed at 0.8863 after failing near 61.8% retracement of 0.9267 (2022 high) to 0.8221 (2024 low) at 0.8867. Decisive break below the 0.8631 support zone (38.2% retracement of 0.8221 to 0.8663 at 0.8618, and 55 W EMA at 0.8625) would confirm bearish reversal.

However, downside confirmation is still lacking. If EUR/GBP finds firm support around current levels and stages a convincing rebound, a break above 0.8744 resistance would suggest that the fall from 0.8863 was merely a corrective pullback. In that scenario, the rise from 0.8221 would likely be resuming, with scope to extend toward through 0.8863 towards 0.9267 in the medium term.