NZD/JPY surged as New Zealand inflation data reinforced expectations for a Reserve Bank of New Zealand rate hike later in the year, with markets responding to persistent price pressures despite soft demand signals. The technical setup suggests NZD/JPY is ready to resume its medium-term uptrend toward 96.50 target.

Q1 CPI came in stronger than expected, holding at 3.1% yoy, keeping inflation above the RBNZ’s target band and supporting the case for further policy tightening. More importantly, the composition matters. While tradable inflation eased slightly, non-tradable inflation held firm at 3.5% yoy, pointing to ongoing domestic price pressures that are harder for policymakers to ignore.

However, at the same time, the NZIER survey paints a more cautious picture on growth. Business confidence deteriorated sharply, and firms reported weak demand conditions, with limited ability to pass on rising costs. This dynamic acts as a natural constraint on inflation, reducing the urgency for immediate policy action.

For the RBNZ, the signal is nuanced. Inflation is firming and supports the case for tightening, but weak demand allows the central bank to move gradually. The base case remains for a hold at the May 27 meeting, with policymakers likely to use a higher OCR track to lay the groundwork for a hike in July or September.

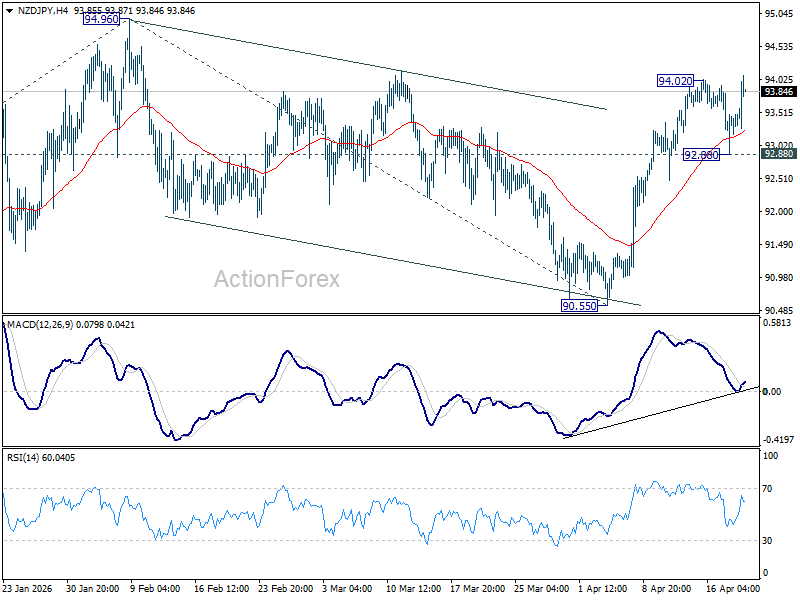

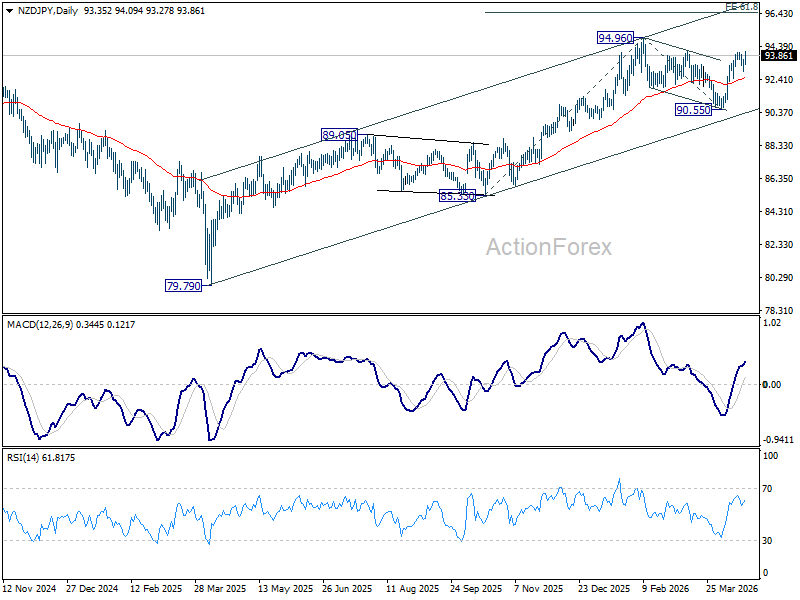

Technically, NZD/JPY’s rise from 90.55 resumed today by breaching 94.02 temporary top. The development reinforces that case that corrective fall from 94.96 has completed with three waves down to 90.55. That is, up trend from 79.79 might be ready to resume. For now, further rise is expected as long as 92.88 support holds. Retest of 94.96 should be seen next. Firm break there will pave the way to 61.8% projection of 85.33 to 94.96 from 90.55 at 96.50.

{kind=link}