Sample Category Title

Canada’s New House Prices Climbed In August

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CAD and closed at 1.2476.

Ibn economic news, Canada's new house price index climbed 0.1% on a monthly basis in August, falling short of market expectations for a rise of 0.2%. In the prior month, the index had risen 0.4%.

On the other hand, the nation's Teranet/National Bank house price index dropped 0.8% on a monthly basis in September. In the previous month, the index had registered a rise of 0.6%.

In the Asian session, at GMT0300, the pair is trading at 1.2469, with the USD trading 0.06% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2438, and a fall through could take it to the next support level of 1.2406. The pair is expected to find its first resistance at 1.2496, and a rise through could take it to the next resistance level of 1.2522.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD failed to continue its bullish momentum yesterday slipped back below 1.1850 and hit 1.1825 earlier today in Asian session. This fact keeps the bearish correction phase remains intact. The bias is bearish in nearest term testing 1.1785. A clear break below that area could trigger further bearish pressure testing 1.1670 level, which from a different technical perspective is the neckline of a potential “head and shoulders” formation as you can see on my daily chart below. On the upside, 1.1900 remains a key resistance which need to be clearly broken to the upside to resume the major bullish trend testing 1.2000 – 1.2090 region.

GBPUSD

The GBPUSD attempted to push lower yesterday slipped below 1.3150 support area but whipsawed to the upside and closed higher at 1.3258, formed a bullish pin bar as you can see on my daily chart below. The bias is bullish in nearest term testing 1.3330 key resistance. A clear break and daily/weekly close above that area would end the bearish correction phase and resume the major bullish trend retesting 1.3615 area next week. Immediate support is seen around 1.3200. A clear break below that area could lead price to neutral zone in nearest term retesting 1.3150 support level. Overall I remain bullish.

USDJPY

The USDJPY had another indecisive movement yesterday. The bias remains neutral in nearest term. The bearish pin bar printed after a false break above 113.20 as you can see on my daily chart below still suggests a potential bearish pressure testing 111.65 region. A clear break below that area would expose 111.00 – 110.65 area. On the upside, a clear break and daily/weekly close above 113.20 would expose 114.50 or higher next week. Overall I remain neutral.

USDCHF

The USDCHF had another insignificant movement yesterday but hit another new weekly low at 0.9711. The bias remains bearish in nearest term testing 0.9700 – 0.9650 region. Immediate resistance remains around 0.9765. A clear break above that area could lead price to neutral zone in nearest term testing 0.9807/36 key resistance area. On the downside, a clear break and daily/weekly close below 0.9650 would expose 0.9590 – 0.9525 region next week. Overall I remain neutral.

Sharp Pound Rebound On 2-Year Brexit Transition Hints, US Inflation Data In Focus

Dollar Treads Water as Investors Await U.S. Inflation Data. The dollar index was steady at 93.083 in early Asian session on Friday, on track for weekly losses as investors awaited U.S. inflation data to gauge the likelihood that the Federal Reserve will stick to its plan to raise interest rates again this year. PPI released on Thursday showed some signs of inflation, at least at the producer level. In the 12 months through September, the PPI jumped 2.6 percent, the biggest gain since February 2012. Traders await CPI readings later in a day that will provide guidance on further path of inflation.

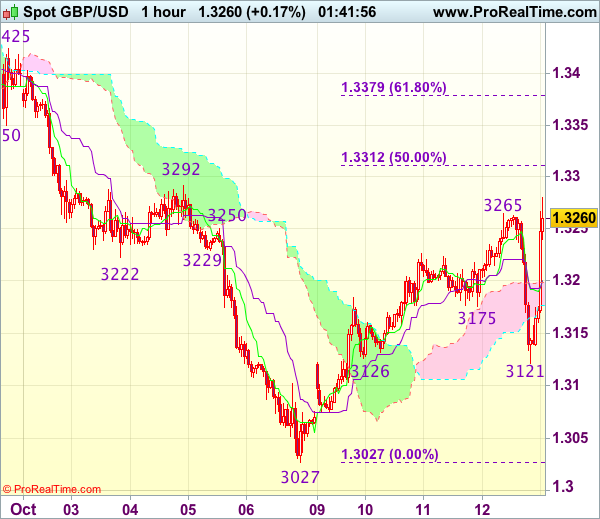

Pound Reverses on Hints of 2-Year Brexit Transition Period. Sterling dipped to as low as 1.3122 on Thursday as markets saw the prospect of no deal being reached after chief Brexit negotiator Michel Barnier said negotiations between the two sides have effectively stalled and “no concessions” will be made. On the same day the pound had a reversal of fortune hitting a high of 1.3289 at the start of the U.S. session on reports the European Union are looking to offer the UK a two-year transition period.

Gold Rally Pauses Ahead of U.S. Inflation Data. Gold prices were little changed amid a steady dollar on Friday, halting a five-day rally as investors wait for key U.S. inflation data for clues on the outlook for potential hikes in U.S. interest rates. Spot gold was nearly unchanged at $1,293.76 an after gaining for five straight sessions. U.S. gold futures for December delivery were flat at $1,296.10 per ounce.

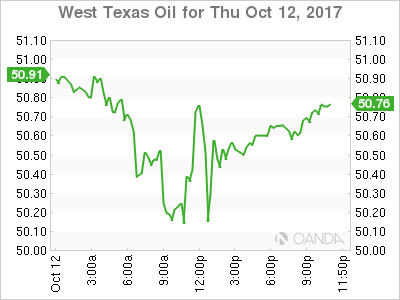

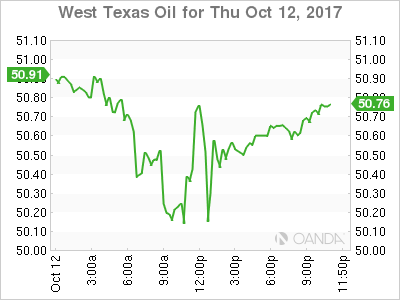

Oil Edges Up as Lower U.S. Production, Inventories Point to Tighter Market. U.S. crude inventories dropped 2.7 million barrels in the week to Oct. 6, to 462.22 million barrels, the EIA said late on Thursday. Crude production slipped 81,000 barrels per day (bpd) to 9.48 million bpd, its first fall since the week to Sept. 1. With the OPEC leading a production cut, analysts said that global oil markets were on a path to rebalancing after years of oversupply. U.S. WTI crude futures CLc1 were trading at $50.72 per barrel, up 0.1 percent from their last settlement, Brent crude futures LCOc1 were at $56.35, up 0.2 percent from the previous close.

Watch Out Today for:

12:30 pm GMT: USD Consumer Price Index

12:30 pm GMT: USD Retail Sales

Market Morning Briefing: Strong Rise In The Pound

STOCKS

Dow (22841.01, -0.14%) may have some chances of testing 23000-23250 levels in the near term while Dax (12982.89, +0.09%) may continue to trade sideways and spend some more sessions without any actual movement.

Nikkei (21003.50, +0.23%) has made a multi-year high after breaking above crucial resistance near 21000. While the upside momentum continues, we could see a test of 22000 soon. However, we resume the exhaustion point for Nikkei on the upside is nearing and we could soon see a reversal of trend for the longer term.

Shanghai (3388.76, +0.08%) would gradually rise towards 3400-3420 in the near term. There could be some sideways consolidation within 3400-3360 levels before the price rises towards 3400 or above.

Nifty (10096.40, +1.12%) recovered sharply yesterday keeping the upside momentum intact. 9950-9980 seems to be an immediate support region and while that holds, a test of 10200 looks possible.

COMMODITIES

Gold (1295.94) may test initial resistance near 1300 which if holds could bring back the prices towards 1280; else a rise towards 1310 is possible in the near term while Silver (17.26) could be headed towards 17.50 soon.

Brent (56.49) and WTI (50.89) are trading slightly lower today. But there could be some scope of testing 57.45 in Brent and 51.50-52.00 in WTI in the near to medium term.

Copper (3.1150) is moving up as expected and could re-test levels near 3.15-3.18 in the next few sessions. Thereafter the price could pause for some time before again deciding on further movement.

FOREX

Bit of profit-taking/ consolidation in the Euro (1.1850) seen yesterday, down from 1.1878 to 1.1825, within overall uptrend targeting 1.1950+. Intra-day Support at 1.1825 and at 1.1800. Longs still preferred.

We had set a target of 92.50 on Dollar Index (92.96) yesterday, but that is possible only on break below immediate Support near the current level, which might not break easily.

Dollar-Yen (112.08) has drifted lower, trying to break below 112.00. Can see 111.80 and then 111.50, if successful. Appears ranged between 111.50-113.00 in the medium term.

Good Support near 132.50 on Euro-Yen (132.85), which can push the Cross up towards 134+, perhaps limiting the downside in Dollar-Yen to 111.80 in the near term. Let us see this.

Strong rise in the Pound (1.3275) over the last few days, coming close to our target of 1.33. Might drift into directionless sideways range in the near term now. Long-term Resistance seen in the 1.34-45 region.

Dollar-Yuan (6.5805) could come down a bit more towards 6.55 over the next few days, which might be decent levels to bounce from. Need to see if Dollar-Rupee (65.05/10) will find Support at 65.00 today or not.

INTEREST RATES

As mentioned yesterday, the German-US-10Yr Spread (-1.88%), has Support at -1.93%. Dips likely to be bought for eventual rise towards -1.85%.

Continued strong correlation between the UK-US 10 Yr Spread (-0.94%), which may have a small Resistance near the current level. Need to see how this behaves today.

The dip in Dollar-Yen (112.08) is being accompanied by a small dip in the US-Japan 10Yr Spread (2.26%), which has Support coming up near 2.22%. This could limit the downside in Dollar-Yen to 111.80-50. Suggests that the Euro-Yen could be a good Long.

A Trendless 24 hours

A Trendless 24 hours

For the most part, its been another trendless 24 hours in forex land as the markets appeared content to bang around in current ranges ahead of CPI. While tax reform has again stumbled out of the gate, the dollar has recovered some semblance of composure after PPI has surprised to the upside, boosting expectations for tonight's pivotal inflation print ( CPI).However, it's apparent that until more details are reaped from both the Fed and Tax reform, the market will play home on the range second guessing positioning and doing an about-face on headline risk

In a headline giddy Thursday, there appeared to be a significant compromise brewing amongst Republicans but given the bloated nature of the current Tax code for every compromise tabled there seems to be another band-aid fixed elsewhere. Understanding and patience will be the name of the game for this to pass but it would not surprise me if we found ourselves back dead in the water next week.

The pound was the most prominent headline chaser falling to 1.3120 on an ambiguous headline ” BARNIER SAYS BREXIT TALKS HAVE REACHED DEADLOCK”. IN fact, this comment was completely misread as he was simply referring to the ” divorce bill”.Then GBP rocketed to just shy of the 1.3300 level when German newspaper Handelsblatt says Barnier may offer the UK a 2y transition stay in the EU market if the UK agreed to settle its financial obligations with the EU and sign a divorce agreement.The proposed extension sits well with the markest and reduces the likelihood of a “Cliff Edge” scenario, but this is not a new negotiating ploy so chasing top side sterling risk is definitely at one's peril.

On the Fed Chair front, its expected this critical decision will be not arriving until November with the latest market straw polls indicating 50 % of participants view Jerome Powell as the incumbent. This view has also weighed on dollar sentiment this week given his more centrist -doveish lean than the markets early front-runner Kevin Warsh.

What have we gleaned from this week?

1) The FOMC minutes confirmed that the Fed is erring on data dependency. Not surprisingly when they are now faced with both a possible interest rate hike and the daunting task of balance sheet reduction

2) Tax Reform, for the most part, remains stuck in the muck despite some concessions.

3) EU political concerns are fading.

The sum of these parts suggests buoyant risk appetite a less attractive US dollar with higher Beta currencies like the Aud and Kiwi the near-term shooting stars. But let's see what surprises CPI may have in store.

USD/CAD Canadian Dollar Lower After Oil Falters

The Canadian dollar depreciated on Thursday due to a report by the International Energy Agency that dampened the energy market’s optimism on demand growth. The IEA numbers put demand for Organization of the Petroleum Exporting Countries (OPEC) crude would be at around 32.5 million barrels which is 150,000 barrels below current production levels. The OPEC and other major producers agreed to cut output and it seems that even after that supply is still higher than demand.

Canadian home resale prices dropped to a seven year low, while new home prices remained flat. The major catalyst of the Canadian real estate cool down was the Bank of Canada (BoC) two rate hikes so far in 2017. The central bank remains cautious about what even higher rates could do to households that are carrying record levels of debt, particularly in mortgages.

The US dollar traded higher versus the loonie after US data posted strong gains. US producer prices rose by the most in six months. The PPI was up 0.40 percent in September and comes at a time when the market is giving more weight to inflation data. The data is particularly strong considering the weather played a huge factor during that period.

The fourth round of NAFTA negotiations will kick off in Virginia this week. The Trump administration has played hardball ahead and during the negotiations with even the US Chamber of Commerce saying that rules of origin demands could torpedo the talks.

The USD/CAD is trading at 1.24780 at the end of the North American session. Inflation data in the US is expected to continue to boost the USD after a strong PPI. The Fed minutes released yesterday were full of concerns from FOMC members about persistent low inflation. Canadian data will be absent on Friday as there are no major releases schedules with all eyes on US retail sales and consumer price index.

The US Bureau of Labor Statistics will release the consumer price index (CPI) on Friday, October 13 at 8:30 am EDT. Core CPI is expected to have gained 0.2 percent, the same as last month for the change in inflation excluding food and energy. The more volatile CPI reading is forecasted at 0.6 percent. US retail sales data will also be released at the same time with core sales anticipated to have gained 0.9 percent. The headline figure adding back auto is expected to have jumped 1.7 percent. The rebound in both is expected to be directly linked to the negative impact hurricanes Harvey and Irma had on purchasing decisions.

The rise of US producer prices (PPI) on Thursday by 0.4 percent doubled the forecast and another inflationary data gain on Friday could put the FOMC minutes in a new light. If inflation is indeed rising faster than expected it could move the emphasis on the doves and put the hawks back in the drivers seat ahead of the December Fed meeting.

The release of the consumer price index on Friday will be a decisive indicator to close out the week of the US dollar. The minutes from the September Federal Open Market Committee (FOMC) meeting showed a growing concern that the factors keeping inflation low could be more longer term than originally thought. Many FOMC members still see another rate hike as appropriate despite those concerns leaving the decision on the table for December but the outlook for 2018 is for less tightening actions from the U.S. Federal Reserve.

Oil gave back some of the gains of the week despite optimism from producers about higher energy demand forecasts and the release of the US weekly crude inventories showing a 2.7 million barrel drawdown on Thursday. The main factor for the decline in prices was a report by the International Energy Agency that forecasted lower demand for Organization of the Petroleum Exporting Countries (OPEC) crude. Current production is more that the appetite which means that oil prices can only recover if OPEC and other major producers not only extend the duration of the cut agreement, but limit their production even further.

US supply is not bound by this agreement and continues to ramp up higher making the OPEC cuts less effective. The US has turned from a net importer of oil to an exporter and with global demand for energy products stable the downward pressure on prices will continue until something changes.

Market events to watch this week:

Friday, October 13

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Dollar Mixed Ahead Of US Inflation Indicator

Retail sales and inflation to make or break USD

The US dollar is higher against the NZD, AUD, GBP and JPY but finds itself lower against the CAD, EUR and CHF. The currency did not build a lot of momentum after the release of the Federal Open Market Committee (FOMC) minutes released Wednesday. The US central bank remains committed to higher rates, but there is a growing concern about consistent low inflation.

The US Bureau of Labor Statistics will release the consumer price index (CPI) on Friday, October 13 at 8:30 am EDT. Core CPI is expected to have gained 0.2 percent, the same as last month for the change in inflation excluding food and energy. The more volatile CPI reading is forecasted at 0.6 percent. US retail sales data will also be released at the same time with core sales anticipated to have gained 0.9 percent. The headline figure adding back auto is expected to have jumped 1.7 percent. The rebound in both is expected to be directly linked to the negative impact hurricanes Harvey and Irma had on purchasing decisions.

The rise of US producer prices (PPI) on Thursday by 0.4 percent doubled the forecast and another inflationary data gain on Friday could put the FOMC minutes in a new light. If inflation is indeed rising faster than expected it could move the emphasis on the doves and put the hawks back in the drivers seat ahead of the December Fed meeting.

The EUR/USD gained 0.20 percent since the Asian open on Thursday. The single currency is trading at 1.18364 on the back of strong eurozone data. Industrial production was 3.8 percent in August and beat expectations of a 2.6 percent rise. The improvement of economic indicators has been steady and could provide further evidence of recovery ahead of the European Central Bank (ECB) meeting. The central bank is anticipated to start tapering its QE program this year, which is boosting the EUR.

While the Fed tried to communicate to the market that tapering did not mean tightening it seems ECB President Mario Draghi wants to be more clear on the subject by saying earlier today that current rates will remain well past the end of the bond buying program. The market is not buying it, as it happened with the Fed and the EUR is rising. German policy makers will not be happy with those words as they have pushed for and end to all stimulus

US data also posted strong gains. US producer prices rose by the most in six months. The PPI was up 0.40 percent in September and comes at a time when the market is giving more weight to inflation data. The data is particularly strong considering the weather played a huge factor during that period.

The release of the consumer price index on Friday will be a decisive indicator to close out the week of the US dollar. The minutes from the September Federal Open Market Committee (FOMC) meeting showed a growing concern that the factors keeping inflation low could be more longer term than originally thought. Many FOMC members still see another rate hike as appropriate despite those concerns leaving the decision on the table for December but the outlook for 2018 is for less tightening actions from the U.S. Federal Reserve.

Oil gave back some of the gains of the week despite optimism from producers about higher energy demand forecasts and the release of the US weekly crude inventories showing a 2.7 million barrel drawdown on Thursday. The main factor for the decline in prices was a report by the International Energy Agency that forecasted lower demand for Organization of the Petroleum Exporting Countries (OPEC) crude. Current production is more that the appetite which means that oil prices can only recover if OPEC and other major producers not only extend the duration of the cut agreement, but limit their production even further.

US supply is not bound by this agreement and continues to ramp up higher making the OPEC cuts less effective. The US has turned from a net importer of oil to an exporter and with global demand for energy products stable the downward pressure on prices will continue until something changes.

Market events to watch this week:

Friday, October 13

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Pound Gets A Glimmer Of Hope

The Bank of England meeting draws ever-closer but Thursday's big rebound in the pound shows it's still all about politics and Brexit. The New Zealand dollar was the top performer while the euro lagged. Chinese trade balance isn't on most economic calendars but it might be released early. A new GBP trade was issued to Premium members today, 6 days after the last GBP trade was closed at a profit.

A report in the German press said that the EU's Barnier wants to offer Theresa May a two year transition period before the full Brexit. Cable had been slumping on the day but immediately shot to 1.3250 from 1.3175 and continued another 40 pips higher from there before running into resistance at 1.3300.

In a sense, the headline shouldn't come as a surprise. The term 'transition period' is a misnomer. The EU will basically offer the UK another two years in the EU, under all the same EU terms. There is no transitioning, it's the same old deal.

At the same time, it's the first actual attempt at negotiating from the EU. Up to this point, all the signals suggested they were intent on punishing the UK so as to dissuade anyone else from exiting. Still, this may prove to hardly be an effort to negotiate. What we did learn for sure is that any negotiation-positive headlines provide longer lasting pound gains than any hawkish BoE chatter. It will be interesting to compare that to BOE headlines in the weeks ahead as we sort out whether May or Carney is the hand guiding GBP. But before November's BoE decision/inflation report, stay tuned for the next week's crucial UK-EU talks.

In US news, PPI numbers were released Thursday and core measures were a touch on the high side. Normally, that wouldn't be notable but it sparked a 20-pip rally in the US dollar. It was later erased but the initial reaction underscores how sensitive the market will be to Friday's CPI report.

Another report that could move markets (and the Aussie) is the September China trade balance report at 0200 GMT. The balance is less-important than imports and exports, where are expected up 16.5% and 10.9%, respectively.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3275

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.3206

Kijun-Sen level : 1.3206

Ichimoku cloud top : 1.3199

Ichimoku cloud bottom : 1.3176

Original strategy :

Sold at 1.3200, stopped at 1.3235

Position : - Short at 1.3200

Target : -

Stop : - 1.3235

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day initial fall to 1.3121, the subsequent rally dampened our bearishness and suggesting near term upside risk remains for the rise from 1.3027 to bring a stronger retracement of recent decline towards 1.3310-15 (50% Fibonacci retracement of 1.3596-1.3027), however, near term overbought condition should limit upside to 1.3345-50 and price should falter below 1.3375-80 (61.8% Fibonacci retracement) and bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.3240 would bring test of the Kijun-Sen (now at 1.3206) but only break there would suggest top is possibly formed, bring weakness to the lower Kumo (now at 1.3176) and then 1.3150.

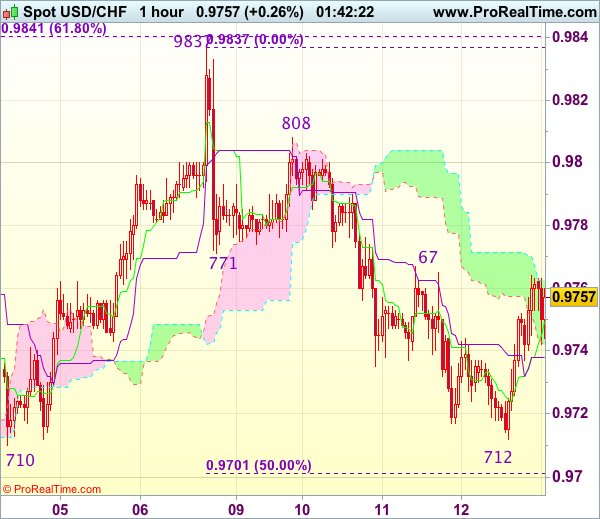

Trade Idea Wrap-up: USD/CHF – Hold short entered at 0.9755

USD/CHF - 0.9749

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9750

Kijun-Sen level : 0.9739

Ichimoku cloud top : 0.9763

Ichimoku cloud bottom : 0.9742

Original strategy :

Sold at 0.9755, Target: 0.9655, Stop: 0.9790

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9790

New strategy :

Hold short entered at 0.9755, Target: 0.9655, Stop: 0.9790

Position : - Short at 0.9755

Target : - 0.9655

Stop : - 0.9790

Although the greenback has rebounded after holding above previous support at 0.9710 and consolidation with initial upside bias is seen, reckon resistance at 0.9767-71 would limit upside and bearishness remains for the decline from 0.9837 top to resume after consolidation, below said support at 0.9710-12 would confirm and extend weakness to 0.9669-70 (61.8% Fibonacci retracement of 0.9565-0.9837 and previous support) but previous support at 0.9642 should remain intact due to oversold condition.

In view of this, we are holding on to our short position entered at 0.9755. Only break of resistance at 0.9808 would signal an intra-day low is formed and indicate the pullback from 0.9837 has ended, bring retest of this level later.