Sample Category Title

EUR/USD Trend Lines in Confluence with POC Zone

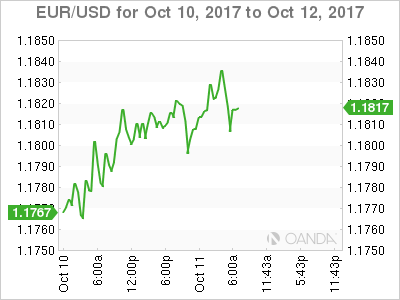

The EUR/USD is in a strong bullish trend and as we can see on the chart the price has pierced through 1.1800 driven by risk sentiment and the Spain situation. Today FOMC meeting minutes are the most important event so we might see two-way price action. At this point the price is still going up straight from the trend line and 23.6 fib. Continuation above 1.1855 aims for 1.1880 and 1.1895. However, if the price gets in a retracement phase watch for 1.1760-75 zone (D L4, EMA89, trend line, ATR low, W H3). Targets remain the same if the pair breaks 1.1810 on the bounce up. Only a move below 1.1750 might make a bearish breakout towards 1.1720 and 1.1695.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 – Daily Camarilla Pivot (Daily Support)

- D L4 – Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Focus on FOMC Minutes for Rate Guidance

Overnight

Asia:

- Japan Aug Core Machine Orders M/M: 3.4% v 1.0%e; Y/Y: 4.4% v 0.7%e

- Japan govt raises assessment of machine orders, orders showing signs of pick up (**Note: prior view was that orders were in a lull)

Europe:

- Catalan President Puigdemont: asks for mandate to declare Catalonia an independent state; proposed to suspend referendum results for several weeks in order to hold talks

- Spain Deputy PM Saenz: Catalan President has put Catalonia into uncertain situation; Any dialogue must be within the law. PM Rajoy to consider next steps at cabinet meeting on Wed, Oct 11th

- PM May: getting close to agreement regarding EU citizens rights; reiterates UK will not be throwing EU citizens out of the country

- ECB General Council said to have an agreement not to raise rates until well past the end of bond buying

- Ireland Fin Min Donohoe: no additional plans for bad bank NAMA after its mandated conclusion

Americas:

- Fed's Kaplan (moderate, voter): will be assessing the progress of the US economy toward full employment and looking for more signs of upward inflation as while weighing potential interest-rate hikes

- President Trump: doesn't believe argument with Sen Corker (R-TN) will hurt tax reform. Intends to adjust tax reform plan to make it stronger

- White House: No adjustments to make to tax framework at this time; President reached decision on an overall Iran strategy; willing to work with Corker on taxes; will make announcement on Iran deal by Friday

- Bank of Canada (BOC) Wilkins: Canada household sector is vulnerable to a negative shock due to indebtedness levels

- Mexico Foreign Min Videgaray: we'll only move forward with NAFTA if it's good for Mexico. Reiterated Mexico would not pay for or participate in any physical barrier between the US and Mexico

Energy:

- 58.5% (1.02M bpd) of current Gulf of Mexico oil production still shut in due to Hurricane Nate effects (vs 85% yesterday) - govt agency BSEE

Economic data

- (JP) Japan Sept Preliminary Machine Tool Orders: 45.3% v 36.2% prior

- (TR) Turkey Aug Current Account Balance: -$1.2B v -$1.4Be

- (ES) Spain Sept Final CPI M/M: 0.2% v 0.2%e; Y/Y: 1.8% v 1.8%e

- (ES) Spain Sept Final CPI EU Harmonized M/M: 0.6% v 0.6%e; Y/Y: 1.8% v 1.9%e

- (ES) Spain Sept CPI Core M/M: 0.0% v 0.2% prior; Y/Y: 1.2% v 1.2%e

- (TW) Taiwan Sept Trade Balance: $6.7B v $5.9Be; Exports Y/Y: 28.1% v 13.6%e; Imports Y/Y: 22.2% v 9.8%e

Fixed Income Issuance:

- (IN) India sold total INR110B vs. INR110B indicated in 3-month, 6-month and 12-month bills

- (DK) Denmark sold total DKK4.98B in 3-month and 6-month bills

- (SE) Sweden sold SEK10B vs. SEK10B indicated in 3-month Bills; Avg Yield: -0.6964% v -0.7542% prior; Bid-to-cover: 2.47x v 2.51x prior

- (IT) Italy Debt Agency (Tesoro) sold €6.0B vs. €6.0B indicated in 12-month Bills; Avg yield: -0.344% v -0.326% prior; Bid-to-cover: 1.96x v 1.86x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 390.0, FTSE flat at 7535, DAX 0.1% at 12956, CAC-40 -0.2% at 5354, IBEX-35 +1.3% at 10272, FTSE MIB 0.1% at 22349, SMI +0.1% at 9276, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade little change across the board with the exception of the Spanish Ibex which trades sharply higher after the Catalonia president suspended results of the independence referendum for several weeks.

In corporate news Gerresheimer and Cropenergies trade higher after results, while Dunelm trades sharply higher after strong Q1 results and LFL sales. Merlin Entertainment trades lower after reportedly refuting claims its in talks with SeaWorld, whilst Spanish Banks rebound in Spain helping the Ibex outperform.

Looking ahead to the US morning, as we enter into Earnings season, notable earners include Delta Airlines and Blackrock and Fastenal.

Equities

- Consumer Discretionary: Dunelm [DNLM.UK] +5.0% (Q1 update)

- Industrials: Gerresheimer [GXI.DE] +1.0% (Earnings), Mondi [MNDI.UK] -6.2% (Profit warning), GEA Group [G1A.DE] +6.4% (Elliott's Paul Singer announces 3.01% stake)

- Material: CropEnergies [CE2.DE] +1.2% (Earnings, lifts outlook)

- Healthcare: Smith and Nephew [SN.UK] +4.0% (Elliot Management (Singer) has reportedly built a stake)

- Technology: Agfa Gevaert [AGFB.BE] +3.3% (To separate the HealthCare IT activities into a stand-alone legal entity structure and organization)

Speakers

- ECB's Smets (Belgium): Favors extended QE taper and believed that a certain extension maters for QE exits. Re-calibration to be gradual and cautious

- Chancellor of Exchequer Hammond (Fin Min): Domestic economy was being affected by uncertainty. Prepared to spend if no-agreement in Brexit negotiations when necessary; needed to determine what is a realistic worst case scenario that we can plan for

- Catalonia govt spokesperson Turull: Central govt application of article 155 would mean that its refuse dialogue

- Poland Central Bank's Zyzynski reiterated view that difficult to talk about interest rate increases; inflation was not that high

- Sweden Central Bank (Riksbank) Dep Gov Jochnick: Reiterates wage inflation remained subdued. Believed that labor market tightness will support wages down the road

- S&P analyst: Return of growth in South Africa could stabilize the sovereign rating

- China Foreign Ministry reiterated its view that all sides should exercise restraint over North Korea situation. US warship entered its waters; such action harms sovereignty

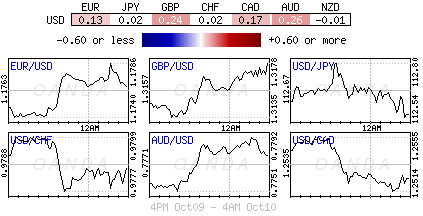

Currencies

- USD was slightly lowers as markets awaited the FOMC minutes to be released later today. Dealers noted that currencies of current-account deficit countries were the exciting assets to play for a sustained reaction to today's release of the FOMC minutes

- Numerous dealers and analysts noted that the Euro currency was poised to move higher. Catalan's President Puigdemont backing away from breaking the link to Madrid should normalize Spanish markets, allowing sovereign spreads to come in and the IBEX to rally. ECB taper talks was also another factor. EUR/USD at 2-week highs above 1.1840 just ahead of the NY morning.

Fixed Income

- Bund futures trade at 161.30 little change as Spanish political tensions ease. Continued downside targets 161.03 while upside resistance stands initially at 162.07, followed by 163.27.

- Gilt futures trade at 123.80 down 11 ticks with no major UK releases due for today. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

- Wednesday's liquidity report showed Tuesday's excess liquidity fell to €1.790T from €1.791T and use of the marginal lending facility rose to €221M from €185M.

- Corporate issuance saw $13.4B come to market via 4 Issuance was headlined by Broadcom Corp $4B issuance and Northrop Grumman $8.25B 5 part offering.

Looking Ahead

- (IT) Italy to hold confidence vote on electoral laws

- (US) President Trump meets Canada PM Trudeau in White House (NAFTA discussions)

- 05:30 (DE) Germany to sell €3.0B 2022 BOBL

- 05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.25B in 2022 and 2027 OT bonds

- 06:00 (RU) Russia announces weekly OFZ bond auction; to sell combined RUB30B in 2024 and 2027 OFZ bonds

- 06:30 (DE) German Gov updates Fall economic forecasts

- 07:00 (US) MBA Mortgage Applications w/e Oct 6th: No est v -0.4% prior

- 07:00 (BR) Brazil Oct IGP-M Inflation (1st Preview): 0.4%e v 0.3% prior

- 07:00 OPEC Monthly Report

- 07:15 (US) Fed's Evans (dove, voter) on economy and monetary policy

- 07:30 (CL) Chile Central Bank Traders Survey

- 07:30 (CL) Chile Central Bank Economist Survey

- 08:00 (BR) Brazil Aug Retail Sales M/M: 0.1%e v 0.0% prior;' Y/Y: 4.4%e v 3.1% prior

- 08:00 (BR) Brazil Aug Broad Retail Sales M/M: 0.6%e v 0.2% prior; Y/Y: 8.5%e v 5.7% prior

- 08:00 (UK) Baltic Dry Bulk Index

- 08:00 (NO) Norway Central Bank (Norges) Dep Gov Nicolaisen

- 10:00 (US) Aug JOLTS Job Openings: 6.135Me v 6.170M prior

- 11:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

- 11:00 (BR) Brazil to sell 2018, 2019 and 201 LTN Bills

- 11:30 (BR) Brazil weekly Currency Flows Weekly

- 12:00 (US) DOE Short-Term Crude Outlook

- 13:00 (US) Treasury to sell 3-Year Notes

- 13:00 (US) Treasury to sell 10-Year Notes Reopening

- 14:00 (US) FOMC Sept Meeting Minutes

- 14:40 (US) Fed's Williams (moderate, non-voter)

- 14:50 (BE) ECB's Praet (Belgium) speaks in New York

- 16:30 (US) Weekly API Oil Inventories

Catalonia & Corker

Separatist leaders in Catalonia did not declare independence on Tuesday. Instead, they called for dialogue. The euro pushed across the board before stabilizing in Wednesday trading ahead of the FOMC minutes. The post-Puigdemont euro moves helped the Premium EURUSD trade into a 100-pip gain. The trade remains open.

The coalition of separatist parties in Catalan parliament is struggling to find a way forward amidst threats from Madrid. Leader Puigdemont attempted inching closer towards independence without a formal declaration on Tuesday. Instead, asserted his mandate to declare independence, but asked for weeks of dialogue and hinted at international mediation. The hardcore ranks of separatists called it a betrayal while the government hinted he could be prosecuted for declaring independence anyway.

The euro climbed about 15 pips after failure to declare independence. For the past few weeks, the currency has shown diminishing sensitivity to the Catalonya story; in part because Catalonia will continue to use the euro. The downsides at the moment relate to Spanish growth and that's a small part of eurozone GDP. Nor is it likely to derail ECB plans to taper. EUR/USD rose above 1.1800 on the day, a 70 pip rise.

USD softness is re-emerging due to two main reasons: Renewed uncertainty about taxes after Trump picked a fight with high-ranking Republican Senator Bob Corker. Trump can only afford to lose two votes in the Senate and his spat with Corker has taken a personal tone.

The other reason is China, which seems to be undertaking a concerted effort to boost the yuan ahead of the party congress and Trump's visit in a month. USD/JPY has fallen 1.3% in two days this week.

Yen Ticks Higher on Strong Japanese Manufacturing Report

USD/JPY has posted small losses in the Wednesday session. In North American trade, the pair is trading at 112.31, down 0.12% on the day. On the release front, Japanese Preliminary Tool Orders impressed with a reading of 45.3% in September, up from 36.3% a month earlier. Later in the day, Japan releases the Producers Price Index, which is expected to edge up to 3.0%. In the US, JOLTS Job Openings is expected to ease slightly to 6.13 million. Today's highlight is the Federal Reserve minutes from the September policy meeting.

Japan's current account surplus climbed to JPY 2.27 trillion in August, marking the highest monthly surplus since 2007. The strong reading points to an increase in exports, thanks the weak Japanese currency and strong global demand for Japanese products. Still, chronically weak inflation remains a sore point, and the Bank of Japan has acknowledged that it does not expect its inflation target of just below 2.0% percent to be reached before 2020. On Tuesday, a BoJ report gave a thumbs-up to the economy, noted that exports were strong and consumer spending and construction had strengthened. Despite improving economic conditions, BOJ Governor Haruhiko Kuroda reiterated a familiar message on Tuesday, saying that the bank will continue its ultra-loose stimulus program until inflation moves above its target of 2 percent.

The Federal Reserve will release its minutes from the September meeting. At the September meeting, the Fed did not raise interest rates but did announce it would begin trimming its $4.2 billion balance sheet in October. This is seen as a vote of confidence in the US economy, which continues to show strong growth. At time of the September meeting, the odds of December rate hike were pegged around 50 percent. However, the odds have now surged to 91 percent. The primary reason for the huge shift in market sentiment can be attributed to Fed policymakers coming out in support of a rate hike, notably Fed Chair Janet Yellen. The lack of inflation remains the most significant impediment to raising rates, but Yellen and other FOMC members have insisted that strong economic conditions will lead to higher inflation levels. Even if inflation does not move higher before 2018, the Fed now appears ready to raise rates for a third and final time this year.

Technical Outlook: USDCAD – Falling Daily Cloud, Higher Oil Prices Continue To Cap Recovery

The pair is holding in tight range on Wednesday, with near-term risk turning lower as CAD got boosted by higher oil prices.

The USDCAD pair's price is in descending mode from 06 Oct high at 1.2597, after the base of descending daily cloud capped recovery. The price remained capped by falling cloud in past few sessions and probes below initial support at 1.2507 (daily Tenkan-sen), firm break of which would generate another negative signal for extension of pullback from 1.2597.

However, corrective action could be shallow if Fed minutes today come in hawkish tone that would boost the greenback. US inflation data on Friday are also in near-term focus.

Bullish scenario requires firm penetration into daily cloud to signal further upside.

Lift above 1.2597 peak would expose 26 Aug top at 1.2662 and cloud top at 1.2697, in extension.

Res: 1.2527, 1.2558, 1.2597, 1.2662

Sup: 1.2507, 1.2484, 1.2448, 1.2416

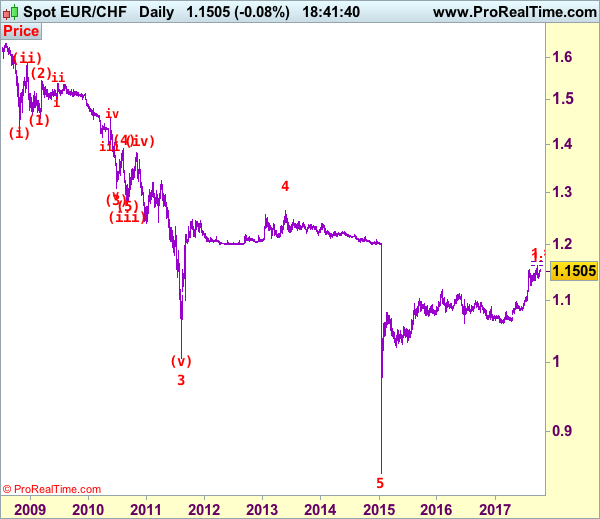

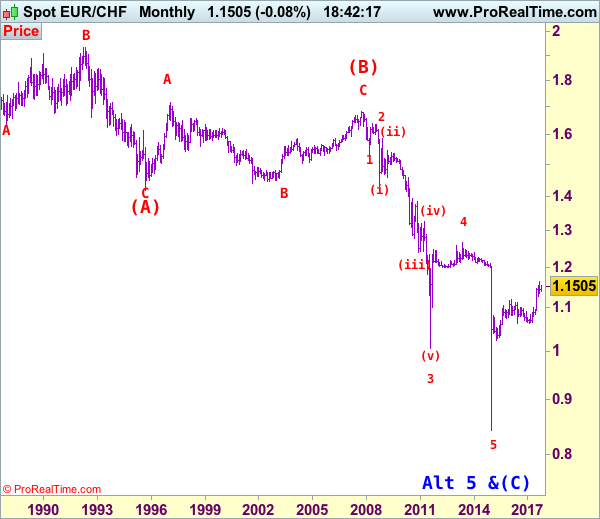

EUR/CHF Elliott Wave Analysis

EUR/CHF : 1.1509

Despite falling to 1.1388, the single currency found renewed buying interest at 1.1388 and has rebounded (we recommended to buy at 1.1455 and a long position was entered), our indicated upside target at 1.1655 was met (with 200 points profit) and consolidation with mild upside bias remains for gain to 1.1550 and then 1.1600 but only break of resistance at 1.1624 would signal recent upmove has resumed and extend gain to 1.1695-00 (61.8% projection of 1.0833-1.1538 measuring from 1.1259), however, this wave v is likely to be limited to1.1800 and price should falter well below 1.2000, bring correction later.

To recap our preferred count, the decline from 1.6828 (end wave (B)) is labeled as the beginning of wave (C) which should unfold as an impulsive move with 1: 1.5326, 2: 1.6377 and wave 3 is sub-divided into (i): 1.4300, (ii): 1.5880 and wave (iii) is still unfolding with (1): 1.4577, (2): 1.5448 and wave (3) is an extended 3rd with i: 1.5006, ii: 1.5383, wave iii: 1.3073, then wave iv ended at 1.3925 and wave v at 1.3073, wave (4) ended at 1.3925 and wave (5) has ended at 1.2765 which also marked the low of wave (iii) and wave (iv) has ended at 1.3835 and wave (v) as well as larger degree wave 3 has ended at 1.0075. The selloff from 1.2650 signals wave 4 has ended there and we are taking a view that the wave 5 could also have ended 0.8426, hence consolidation is seen with mild upside bias for rebound to 1.1400 (already met), then towards 1.1600.

On the downside, whilst initial pullback to 1.1455-60 cannot be ruled out, reckon 1.1400 would limit downside and bring another rise later. Only a drop below said support at 1.1388 would signal a temporary top has been formed at 1.1624 (wave v top) and bring retracement of recent rise to 1.1345, break there would add credence to this view, then weakness to another previous support at 1.1259 which is likely to hold from here.

Recommendation: Long entered at 1.1455 met target at 1.1655 with 200 points profit.

The long-term downtrend started from 1.9626 (Apr 1985) to 1.4166 (Sep 1995) is treated as wave (A) with A:1.6285 (Dec 1987), B: 1.9342 (May 1992) and C: 1.4166, then wave (B) ended at 1.6828 with A: 1.7147 (Feb 1997), B: 1.4398 (Sep 2001), C: 1.6828 (Nov 2007), therefore, wave (C) is now in progress with the breakdown indicated as above. This wave (C) already met indicated downside target at 1.1455/60 and 1.1300, it could have ended at 0.8426, consolidation with mild upside bias is seen for gain to 1.1000 and later towards 1.2000.

CAC Ticks Lower, Catalonia Suspends Declaration Of Independence

The CAC index has inched lower in the Wednesday session. Currently, the CAC is trading at 5,357.80, down 0.07% on the day. On the release front, there are no French or eurozone events on the schedule.

France's public sector workers held a nationwide strike on Tuesday, in protest of the government's plans to dismiss 120,000 public sector workers and reduce sick leave benefits. The government has promised to continue negotiations with unions, and this has led to split among unions over how to respond to Macron's reforms. Although this strike was endorsed by all 9 of France's public service unions, the government said that only 14 percent of state public workers went on strike. French President Emmanuel Macron's appears determined to reform the economy and trim the public sector, arguing that deep reforms are needed in order to make the French economy more competitive.

All eyes remain on Spain, after Catalan President Carles Puigdemont declared independence, but quickly qualified the move by suspending any formal secession moves. Puigdemont announced that he is open to dialogue with the Spanish government, but Madrid continues to take a hard line against the Catalan leader. The Spanish government is holding an emergency meeting to determine its response, and is reportedly considering imposing Article 155 of Spain's constitution, which would allow the government to suspend the Catalan government and hold new elections. This “nuclear option” could mark a steep escalation in the constitutional crisis. Although Catalan leaders say they have a mandate for independence based on the referendum (in which 90% voted for independence), Catalans are deeply divided over the issue. Several banks and major companies have announced they will move their legal headquarters from Barcelona to Madrid, and the constitutional crisis could take a toll on the Spanish economy if the stalemate continues. However, the crisis is not expected to affect the eurozone, and French stock markets have remained steady this week.

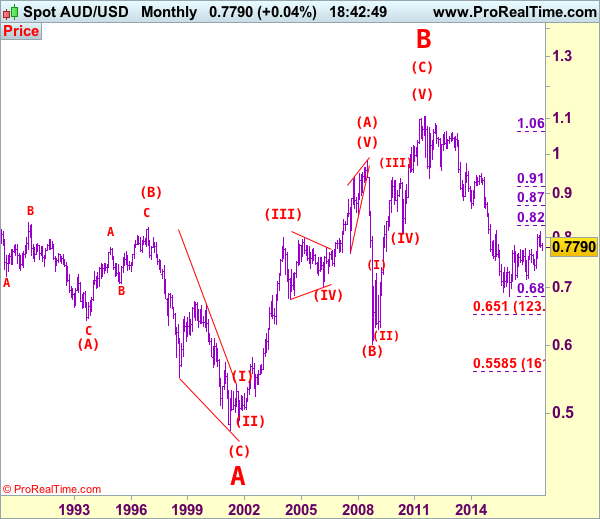

AUD/USD Elliott Wave Analysis

AUD/USD – 0.7790

Aussie has dropped again after brief recovery to 0.7875 last week, adding credence to our view that top has been formed at 0.8125 earlier and our bearishness remains for this fall from there to bring retracement of recent rise, below support at 0.7733 would extend weakness to previous resistance at 0.7712, break there would bring further fall towards 0.7640-50 but oversold condition should limit downside and reckon support at 0.7570 would hold from here, bring rebound later.

We are keeping our count that top has been formed at 1.1081 (wave 5 of V) and major correction (A-B-C-X-A-B-C) has commenced, indicated downside targets at 0.7945 (61.8% Fibonacci retracement of entire rise from 0.6007-1.1081) and 0.7750 had been met and downside bias is seen for further weakness to 0.6800, then 0.6700 but reckon 0.6500 would hold from here.

Our preferred count is that the rally from 0.6007 to 0.7270 (7 Jan 2009) is marked as wave A, the retreat to 0.6248 (2 Feb 2009) is wave B and the subsequent upmove is labeled as wave C with wave (iii) and wave (iv) ended at 0.8265 and 0.7700 respectively and wave (v) as well as 3 ended at 0.9407, then wave 4 ended at 0.8066 (instead of 0.8578). The wave 5 has met our indicated projection target of 1.1060 and could ended at 1.1081, this level is now treated as the peak of wave (C) as well as larger degree wave B, hence major fall in wave C has commenced, our initial downside target at psychological support at 0.7000 has just been met and further weakness to 0.6500 would be seen later.

On the upside, whilst initial recovery to 0.7830-35 cannot be ruled out, reckon upside would be limited to said resistance at 0.7875 and bring another decline later to aforesaid downside targets. Above previous support at 0.7908 would suggest first leg of decline from 0.8125 has ended instead, bring a stronger rebound to 0.7940-50 but upside should be limited to 0.8020 and bring another decline later. A daily close above 0.8020 would risk test of 0.8080 but only break of resistance at 0.8103 would signal correction from 0.8125 has ended, bring retest of this level first.

Recommendation: Sell again at 0.7870 for 0.7670 with stop above 0.7970.

Our alternate count on the daily chart treated the top formed in 2008 at 0.9851 could be a larger degree wave I and was followed by a deep and sharp correction in wave II to 0.6007 and wave III is unfolding from there.

The long-term uptrend started from 0.4775 (2 Apr 2001) with an impulsive structure. Wave I is labeled as 0.4775 to 0.9851 (15 Jul 2008), wave II has ended at 0.6007 (Oct 2008) and wave III is still in progress which may extend further gain to 1.1265.

Catalonia Relief Supports Equities And EUR

Spanish capital markets are breathing a sigh of relief; while the EUR (€1.1842) trades within striking distance of its two-week high this morning as European markets took relief from Catalonia stopping short of declaring immediate independence from Madrid yesterday.

Catalonia's leader Carles Puigdemont resisted a formal declaration of independence Tuesday, instead indicated that the want away region sought to hold official talks with the Spanish government over their future.

Spanish PM Rajoy will convene an extraordinary meeting of his cabinet in Madrid today to discuss his next move.

Stateside, investors will parse today's FOMC minutes (02:00 pm EDT) for further confirmation that a December rate increase is on track. U.S ten-year Treasury yields are trading a tad lower after President Trump indicated yesterday that he plans to make changes to his tax plan within the next few weeks.

The market is also concerned that the President's ongoing public spat with Senator Corker could stymie a potential tax overhaul.

1. Global stocks in the black

Japan's Nikkei share index closed at its highest in 21-years overnight, with gains mainly led by defensive shares, though exporters benefitted from solid global growth. The Nikkei rose +0.3%, while the broader Topix rallied +0.1%, its highest finish in a decade.

Note: Kobe Steel (Japans second biggest steel maker) tumbled for a second day, shedding -36% of its value in just two days following its data fabrication scandal.

Down-under, Aussie stocks rallied further after a Tuesday pause ended a solid two-day rebound, with the S&P/ASX 200 up +0.6%. Tech's also continued to boost South Korea's stock market, with the Kospi up +0.7% to near its record, set in July.

In Hong Kong, stocks fell, pressured by a sharp reversal in property shares after the city's chief executive Carrie Lam unveiled a mix of housing and tax relief policies that disappointed the market. The Hang Seng index fell -0.4%, while the China Enterprises Index lost -0.1%.

In China, stocks firmed overnight, supported by a jump in defensive consumer staples, while resources shares curbed gains. The blue-chip CSI300 index rose +0.3%, while the Shanghai Composite Index added +0.2%.

In Europe, regional indices trade little changed across the board with the exception of the Spanish Ibex, which trades sharply higher after the Catalonia president suspended results of the independence referendum for several weeks.

U.S stocks are set to open in the 'red' (-0.1%).

Indices: Stoxx600 flat at 390.0, FTSE flat at 7535, DAX 0.1% at 12956, CAC-40 -0.2% at 5354, IBEX-35 +1.3% at 10272, FTSE MIB 0.1% at 22349, SMI +0.1% at 9276, S&P 500 Futures -0.1%

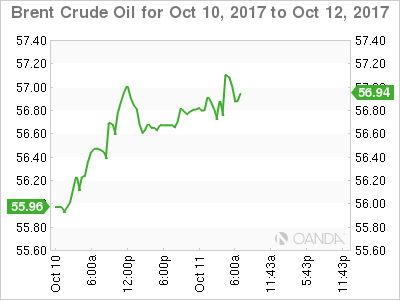

2. Oil rises on signs of a tighter market, gold unchanged

Ahead of the U.S open, oil prices are a tad better bid, rising for a third consecutive day on signs that markets are gradually tightening after years of oversupply, although the outlook for 2018 remained less certain.

Brent crude futures are trading at +$56.75 per barrel, up +14c, or +0.25% from yesterday's close. U.S West Texas Intermediate (WTI) crude futures are at +$51.09 a barrel, up +17c, or +0.33%, from Tuesday's settlement price.

Expect investors to look to the U.S's fuel inventory data today and tomorrow for indicators on price direction.

Note: Both reports are delayed a day due to Monday's U.S federal holiday.

The OPEC-led production cuts started in January and are set to expire at the end of March 2018. Prices are supported as OPEC said oil markets were “rebalancing fast” after years of oversupply.

Note: Discussions to extend the pact are taking place, but production elsewhere is rising.

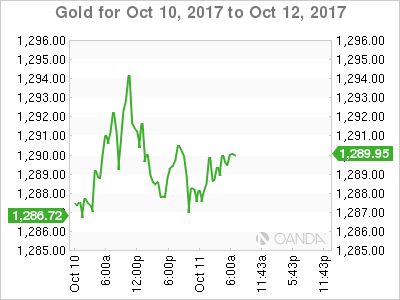

Gold prices trade relatively stable ahead of the U.S open as the 'big' dollar held steady, with investors waiting for Fed minutes for clues on the outlook for potential rate rises. Spot gold is unchanged at +$1,287.36 an ounce.

3. Sovereign yields mixed results

The remainder of this week is expected to be rather eventful for fixed income traders.

Today stateside, the auctions of three-year and 10-year Treasury notes are both scheduled, while a sale of 30-year Treasury bonds is slated for tomorrow. Dealers will want to make room for product and are expected to cheapen up the curve to take down product.

This afternoon, the Fed will release minutes from its September meeting. The market will scour the report for potential clues on future interest rates – currently, fed fund futures are pricing in a +90% odds for a December rate hike.

On Friday there is U.S retail sales and inflation data, the consumer-price index, to keep fixed income traders busy mapping the future of U.S yields.

The yield on U.S 10-year Treasuries declined -1 bps to +2.35%, while Germany's 10-year Bund yield gained +1 bps to +0.46%. In the U.K, the 10-year Gilt yield gained +1 bps to +1.363%, while Spain's 10-year yield dropped -3 bps to +1.66%.

4. Euro waits for a catalyst

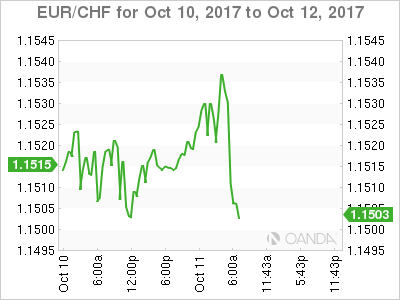

The EUR's (€1.1810) gains are limited, even as it rises to two-week highs outright (€1.1845) and against the CHF (€1.1531) after Catalan President Puigdemont suspended a declaration of independence yesterday afternoon. The market is waiting for Spanish Prime Minister Rajoy's response to the crisis (a press conference is timed for 06:00 am EDT) and is key for providing direction for 'single' unit.

The 'mighty' USD is also under pressure amid ongoing uncertainty over who will be the next Fed chair. Fed Governor Jerome Powell is now in the running and is regarded as more 'hawkish' than incumbent Janet Yellen, whose term expires in February. If anointed, many believe that he probably would not look to unwind stimulus as aggressively as some of the other candidates on the short list.

5. Hong Kong's GDP pointed toward high end

Hong Kong's new Chief Executive Carrie Lam gave an upbeat view on the city's economy during her inaugural policy speech last night, by stating that 2017 GDP is likely to grow faster than the +3.5%, the midpoint of the government's raised August forecast and above the +2.9% annual average of the past decade.

Note: H1's growth was +4% amid a tight labor market.

Technical Outlook: Turkish Lira Boosted By Better Than Expected C/A Numbers

Turkish lira strengthens against dollar on Wednesday, boosted by better than expected Turkish current account numbers. Trade gap narrowed in August to $1.23 billion, beating forecast for $1.4 billion and previous month's gap of $5.12 billion. Lira's fresh rally probes again below strong support at 3.6696, provided by daily Tenkan-sen, which was cracked on Tuesday's spike to 3.6618. Yesterday's spike lower was short-lived but the greenback is coming under renewed pressure on signs of Trump's tax plan stall and fresh strength of Turkish lira on solid data. Close below Tenkan-sen will be seen as bearish signal which would trigger further weakness and result in filling Monday's gap. Key events which would also strongly influence the performance of USDTRY pair are FOMC minutes today and US CPI data, due on Friday.

Res: 3.7078, 3.7301, 3.7853, 3.8109

Sup: 3.6512, 3.6370, 3.6094, 3.5938