Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

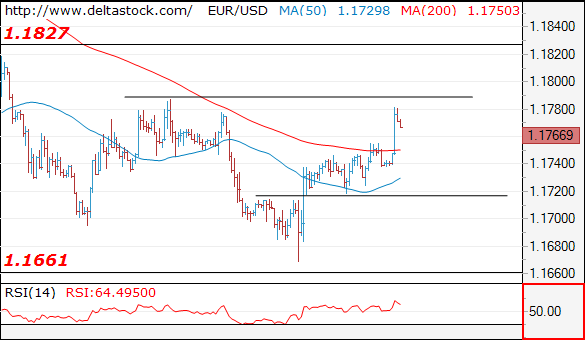

EUR/USD

Current level - 1.1766

The intraday bias here is positive, for a break through 1.1785 hurdle, for a tight test of 1.1830 major resistance. Crucial on the downside is 1.1720.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1785 | 1.1830 | 1.1720 | 1.1660 |

| 1.1830 | 1.2070 | 1.1660 | 1.1480 |

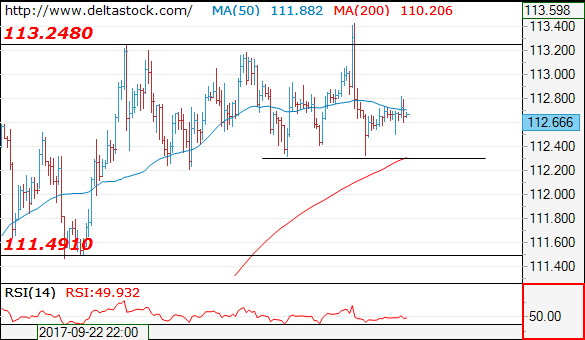

USD/JPY

Current level - 112.66

The bias remains bearish below 112.90, for a violation of 112.30, towards 111.50 major support.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.90 | 113.80 | 112.30 | 111.50 |

| 113.80 | 114.50 | 111.50 | 107.30 |

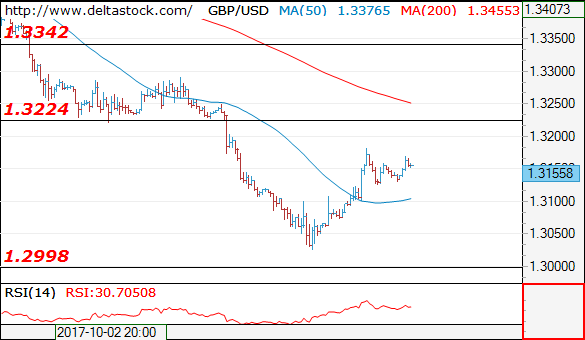

GBP/USD

Current level - 1.3155

My outlook remains positive above 1.3100 area, for a rise towards 1.3220 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3150 | 1.3340 | 1.3000 | 1.2910 |

| 1.3220 | 1.3650 | 1.2910 | 1.2760 |

Market Morning Briefing: Aussie Could Test 0.7700

STOCKS

Dow (22761.07, -0.06%) could trade below immediate resistance near 22800-22850 region and may have been exhausted after the recent rally in the last few weeks. A pause could be expected now where the index may trade sideways in the 22500-22800 region. A test of 22500 is on the cards for the coming sessions. Only on a sustained break above 22850, we may look at higher levels of 23000.

Dax (12976.40, +0.16%) made a fresh high of 12996 reaching almost our initial target of 13000. We will have to see if the index pauses here or heads higher to break above 13000. Some sessions of sideways consolidation would be preferred just now before an attempt to move further up. Note important resistance zone of 13000-13050.

Nikkei (20770.99, +0.39%) has broken above medium term resistance at 20750 and while the index trades above this level, there could be chances of testing crucial resistance near 20900-21000 levels on the upside in the near to medium term. Near term looks bullish contrary to our expectation of a pause below 20750.

Shanghai (3359.87, -0.43%) fell sharply in the last 2-sessions from 3410. The current fall may extend towards 3330-3325 before again bouncing back towards 3375 and higher.

Nifty (9988.75, +0.09%) was almost stable yesterday. A sustained rise above 10000 is necessary to take the index towards 10050-10100 in the next few sessions; else the index could continue to trade in the 10000-9900 region this week.

COMMODITIES

Gold (1286.62) has bounced well from 1260 levels last week and while that holds, we could see a rise towards 1293-1295 levels over today and tomorrow. Near term looks bullish.

Silver (17.028) has also broken above 16.75 and if the price manages to remain above 17 just now, we could see an extension of the current up move towards 17.50 where the price could take a pause or trade sideways for some time.

Brent (55.83) tested 55 on the downside yesterday and has bounced back from there. While above 55, a rise to 56.30-56.50 is possible. Trade within 56.65-55.00 could be expected in the coming sessions.

WTI (49.65) has interim support at 49 and while that holds, the price could move up towards 50.00-50.50 in the 2-sessions.

Copper (3.0435) has been coming off from 3.05, in line with our expectation but may bounce back from 3.00 to move up to 3.10 in the near term. The corrective dip is short lived and we could soon see a bounce by the end of the week.

FOREX

Dollar Index (93.548) has faced decent rejection from 94 and while that holds, the index could come off towards 93.26-93.00 levels in the near term. Euro (1.1771) on the other hand has moved above 1.1750. the low of 1.1668 tested on Friday could possibly be the near term low for the coming sessions and if prices remain above 1.1700, the Euro could head higher towards 1.1850 given that the resistance at 94 holds on the Dollar Index.

Dollar Yen (112.677) has been trading in the 113.30-112.30 region for the last 8-9 sessions unable to decide which direction to take. The currency pair is likely to continue to trade within the mentioned region for a few more session trying to move up towards 113.00 or higher. A break on either side is needed to get some clarity on further movement. Looking at Nikkei, it could be headed towards crucial resistance and the upside could be limited for the near term.

Pound (1.3158) has bounced from 1.30 and while that holds, a rise to 1.3275 is a possibility. Near term looks bullish.

Aussie (0.7786) could test 0.7700 on the downside before starting to move up again. Trade within 0.78-0.77 looks likely in the near term.

Dollar Rupee could spend some time in the 65.20-65.50 region before trying to move down to 65.00. Some time and price correction is preferred now especially after the sharp rally in the last 2-3 weeks from levels near 64.00 to almost levels near 65.80.

INTEREST RATES

The US yields have paused and could come down a bit before resuming a rise again by next week. A slight dip could be expected in the coming sessions. Note important resistances on the 30YR (2.91%) and 10Yr (2.36%) near 3.00% and 2.50% respectively.

The German-US 2YR (-2.21%) and the German-US 10YR (-1.91%) are trading just above medium term support levels and if that holds the yield spreads could bounce back sharply indicating a rise in Euro for the coming sessions.

Composition Of Market Risks Remains Unchanged

Composition of market risks remains unchanged

With US market on holiday, price action went as expected.But the one exception is TRY which continues to labour on the escalation of tension between US and Turkey and has precipitated a sell-off across most EM carry trade.Speculators are in no mood for unpleasant news more so with the Catalonian consternations heading for more moments of middlement.

Outside of the Turkey tantrum, the composition of forex market risks remains unchanged as the dollar, for the most part, anchors at current levels.

Trader's remain on geopolitical watch as North Korea celebrates the founding of the North Korean communist party on today.

Australian Dollar

With holidays in Japan and the US, it's been a slow start to the week for the Australian dollar which remains mired in tight ranges. However, dealers continue to view the weak domestic retail sales as a huge negative. Given the record debt levels, how much more spending power can the average consumer add to the economy?. And with the markets still likely underpriced the inflationary fall out from US tax reform, the Aussie will likely remain a go-to short over the near term.

Factor in the slide and Iron ore prices as China state mandates reducing steel production; iron ore demand could contiue to wilt.

The Australian economy looks little more than an asset bubble sitting on top of an iron ore mine. Both of which are the critical negatives in this weak Aussie dollar view.

Chinese Yuan

China returned from the Golden week with a bang as mainland equities soared to multi-year highs driven by last week RRR cuts. ON the FX market there was an aggressive culling of long USD. The liquidation appears guided to provide currency stability heading into the NPC on October 19.

Japanese Yen

Dollar-yen lacks in any momentum wedged between tracking US fixed income and a possible geopolitical flare up. However, the USDJPY continues to exhibit a higher acuteness to softening US rates so top side momentum should cap at 113.20 until this week's critical US CPI reading.

The Euro

Despite the heightened political risk, robust EU economic data continues to attract EURUSD buyers ahead of the critical 1.1700.

ECB's Sabine Lautenschlaeger was on the wires overnight; her hawkish comments also appear supportive for the EUR But with the Euro unchanged this week, the political overhang has taken the air out of the EUR ballon, and this ongoing political uncertainty will most certainly cap any near-term rallies.

The British Pound

The pound was undoubtedly the most energetic performer overnight After an error on Friday, the Office of National Statistics has confirmed that the UK unit labour costs have been revised up from 1.6% to 2.4% YoY. Predictably the inflation revision led to further pricing-in of a November BoE rate hike. But the sterling trade remains fraught with chaos with lots of head scratching on both the political and monetary policy fronts

New Zealand Dollar

NZ$ stays on the back foot after the weekend shift in election results. But the markets continue to bid on dip mode expecting the election tumult and the broader uncertainties to dissipate which could provide a lift to the Kiwi near-term expectations

Asia EMfx

The volatility in both US rates and commodities has muddied the landscape as the market continues to drift in no man's land. Geopolitical risks remain elevated which is not helping matters, but selective opportunities should stay in fashion. While the exclusive carry trades remains a tough grind the economic fundamentals continue to look favourable on the THB, MYR despite the overnight purge in EM positions overnight

Positioning on the MYR remains very light and on the first sign from the sell-off in global fixed income abates ,I expect regional inflows to pick up again.

Turkish Lira

Where do we go from here.? The Carry trade should remain alive and well however over the near term there will likely remain a lack of confidence in the TRY institutional markets after fairweather liquidity providers baulked at providing streamable quotes and the one or two that did support electronic venues felt 2-4 % spread was appropriate for market conditions. If there's any doubt what adds more unwarranted fuel to market unwinds, look no further than the risk-averse mindset that dominates today's Top Tier bank trading rooms. what investor appreciates his stop-loss triggered on a disproportionately wide 4% spread

Gold Rally Continues On Holiday Monday

After an uneventful week, gold has started the week with gains. In Monday’s North American trade, the spot price for an ounce of gold is $1280.61, up 0.37% on the day. There are no US releases today, and banks are closed for Columbus Day.

Gold prices moved higher on Friday, as Nonfarm Employment Change shocked the markets by wiping out 33 thousand jobs in September, much weaker than the estimate of a gain of 85 thousand. The dismal release was a result of the severe impact of hurricanes Harvey and Irma, which hit the US in late August and early September. The two storms caused $150-200 billion in damage and also took a toll on the employment market, although the labor market is expected to rebound as the recovery effort intensifies. There was better news from wage growth, which accelerated to 0.5%, above the estimate of 0.3%. This reading is pointing to stronger inflationary pressure, although we’ll have to wait for additional inflation indicators, such as CPI, to gauge inflation is moving higher. As well, the unemployment rate fell from to 4.2% in September, down from 4.4% a month earlier.

Early in the year, the Federal Reserve broadly hinted that it would raise rates three or four times in 2017, and a third hike in December now appears very likely. Fed futures are currently priced in at 91%, which is remarkable, considering that only a month ago, the odds of a December increase were just 31 percent. A strong US economy has helped raise the odds, but the primary reason for the huge shift in market sentiment can be attributed to the Fed policymakers that have come out in support of a rate hike, notably Fed Chair Janet Yellen. The lack of inflation remains the most significant impediment to raising rates, but Yellen and other FOMC members have insisted that strong economic conditions will lead to higher inflation levels.

Elliott Wave Trade Ideas Performance Update

3 positions were entered last week with total profit of 365 points and the positions are listed below.

22 Sep : USD/CAD - Long at 1.2285, exited at 1.2450 (+ 165 points)

9 Oct : GBP/JPY - Short at 151.00, exited at 149.00 (+ 200 points)

9 Oct : EUR/GBP - Short at 0.8930,

| AUD EUR/JPY EUR/GBP CAD GBP GBPJPY

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar - 20 +115 +132 - 19

Apr + 30 - 40 +120 + 45

May - 55 +100 - 6 -65 -60

Jun + 81 +150 - 10 +185 -120 +205

Jul - 40 - 60

Aug +155 +200 + 100 + 195 -45 - 50

Sep -50 + 165 + 5

Oct +200

Nov

Dec

Y-T-D + 371 + 68 +167 +823 -230 +285

Pound Starts Week Higher, UK Manufacturing Production Next

The British pound has posted gains in the Monday session. In North American trade, GBP/USD is trading at 1.3134, up 0.46% on the day. In the US, banks are closed for Columbus Day and there are no US events on the schedule. Later in the day, the UK releases the sole event of the day, BRC Retail Sales Monitor. On Tuesday, the UK will publish Manufacturing Production, which is expected to slow to 0.3%.

The pound suffered its worst weekly decline of 2017, as GBP/USD slumped 2.4% last week. On Friday, the pound dropped to 1.3027, its lowest level since September 7. Investors remain worried about the political longevity of Prime Minister Theresa May. There were no broadsides fired at May at the Conservative party convention last week, but she still remains vulnerable to being ousted. Meanwhile, it's back to Brexit this week, as British and European negotiators meet in Brussels. The sides are scheduled to discuss Britain's financial settlement, one of the key sticking points between the parties. Britain is keen to discuss trade talks, but the Europeans have insisted that progress first be made on a number of issues, such as the size of Britain's bill for leaving the European Union.

Non Farm Employment Change wiped out 33 thousand jobs in September, much weaker than the estimate of a gain of 85 thousand. However, the weak reading didn't cause any alarm in the markets, but rather underscored the severe impact of Hurricanes Harvey and Irma, which hit the US in late August and early September. The two storms caused $150-200 billion in damage and also took a toll on the employment market, although the labor market is expected to rebound as the recovery effort intensifies. On a brighter note, wage growth accelerated to 0.5%, above the estimate of 0.3%. This reading is pointing to stronger inflationary pressure, although we'll have to wait for additional inflation indicators, such as CPI, to gauge inflation is moving higher. There was more good news from September job data, as the unemployment rate fell from to 4.2% in September, down from 4.4% a month earlier.

Dollar Steady as North Korean Tensions Weigh; Pound Gains Ground Ahead of May’s Speech

Investors maintained their risk-averse stance during the European trading hours amid fears that North Korea is planning another missile test in the near term, restricting the dollar from recovering. On the other hand, the pound was the best performer ahead of May's speech later today and as Brexit negotiations were entering their fifth round.

Although optimism on the US economy remained high among investors following Friday's upbeat readings on wage growth and unemployment rate indicated in the employment report, the dollar edged lower to a four-day low of 93.44 during the session before it edged up to 93.55 afterwards. Against the yen, the greenback remained flat around 112.69, while safe-haven gold was up 0.41% at $1,280.40 per ounce.

In other news, the Turkish foreign ministry called the US on Monday to remove its suspension on visa services arguing that it causes "unnecessary tensions", while the Ministry of Justice said that "trying a Turkish citizen for a crime committed in Turkey is our right". This comes after a Turkish employee working at the US Consulate in Turkey was arrested and accused of holding links with the Fethullah Gulen who was blamed for the unsuccessful military coup in July 2016. The greenback gained 2.74% against the Turkish lira, climbing to 3.7159.

The pound surged by 0.64% to $1.3146 as investors were upbeat on May's speech at the British Parliament later today. May is expected to highlight the UK government's willingness to achieve a special partnership with the EU after Brexit and say that the ball is now in the EU court according to an extract released by her office. In response, an EU spokesman argued on Monday that "the ball is entirely in the UK court".

The euro was moving sideways around $1.1731 despite the Catalan foreign affairs chief, Raul Romeva, calling for dialogue with Spain on Monday. However, the Spanish Deputy Prime Minister, Soraya Saenz de Santamaria, argued once again that the Spanish government "will take all necessary measures if Puigdemont declares unilateral independence".

Meanwhile, in Germany, political uncertainty eased after the German Chancellor Angela Merkel said to start separate coalition talks next week with the Greens and the Free Democrats.

In terms of data out of the Eurozone, the Sentix Investor Confidence Index indicated that investors' economic outlook for the next six months improved unexpectedly in October. The index rose by 1.5 points to a 10-year high of 29.7, exceeding the forecast of 28.5.

In other currencies, the aussie and the kiwi continued weakening, with the aussie being 0.23% down on the day at $0.7751 and the kiwi falling by 0.41% to $0.7063.

In the Gulf of Mexico, oil refineries were restarting their operations after Hurricane Nate forced oil producers to shut their pipelines on Friday, driving oil prices near to one-month low levels. However, comments by the OPEC Secretary general Mohammad Barkido on Monday pushed oil prices higher. Particularly, Barkido argued that "there is a clear evidence that the market is rebalancing", while he also added that growth in US oil output has slowed down compared to the first half of 2017.

WTI crude was up 0.32% on the day at $49.45 per barrel and Brent was 0.13% up at $55.69.

Candlesticks and Ichimoku Trade Ideas Performance Update

5 positions were entered among all 4 currency pairs with total loss of 25 points and the positions are listed below:

22 Sep : USD/JPY - Long at 111.70, exited at 111.90 (+ 20 points)

27 Sep : USD/CHF - Long at 0.9685, exited at 0.9710 (+ 25 points)

27 Sep : USD/JPY - Long at 112.65, exited at 112.65 ( 0 point)

29 Sep : GBP/USD - Long at 1.3375, exited at 1.3340 (- 35 points)

9 Oct : USD/CHF - Short at 0.9705, exited at 0.9740 (- 35 points)

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr + 65 + 93 + 50 - 40

May - 65 - 35 + 100 -175

Jun -100 -10 - 10 +175

Jul + 85 - 35 - 8

Aug + 35 +210 + 35 +65

Sep +129 +210 +200 - 70

Oct - 35

Nov

Dec

Y-T-D + 492 +423 +392 - 79

Brent Oil Upside Completed

The Brent Oil dropped today and reached new lows, but failed to stay near 55.29 low and now has squeezed a little. Price plunged on Friday and confirmed that we may have a larger drop in the upcoming weeks. Technically, it should drop much deeper after a false breakout, but it could increase a little again to retest another resistance before will really drop.

The rate is trading above the $55.50 per ounce, could increase a little if the USD/CAD will drop towards the 1.2460 static support in the upcoming days.

Brent is into a correction phase right now, remains to see how long this will be because stands above crucial support levels. Personally, I believe that only the fundamental factors could keep it higher because technically has failed to stay in the green territory.

Price dropped and resumed the bearish movement, but it could come back to retest the 250% Fibonacci line (descending dotted line) before will drop towards the downside line of the minor ascending channel. Technically, is expected to drop after the false breakout above the median line (ML) of the blue ascending pitchfork, it should be attracted by the 50% Fibonacci line (ascending dotted line), but is premature to talk about a larger drop because anything could happen.

AUD/USD Facing Tough Support

Price is trading in the red on the Daily chart, but shows some exhaustion signs after the failure to approach and reach the 0.7732 Friday's low. Price is pressuring the 0.7755 horizontal support, another false breakout will announce a minor increase towards the median line (ml) of the descending pitchfork. The next major downside target will be at the first warning line (WL1) of the ascending pitchfork, will reach it only if the USDX will climb again above the 93.81 static resistance.