Sample Category Title

EUR/USD Analysis: Plunges Amid FOMC Statement

A decision of the Fed to start reducing the size of its $4.5 trillion asset portfolio caused a very high volatility in the markets, which resulted in 123 points appreciation of the Dollar against the Euro just in one hour. From technical perspective, this event signified a breakout of the pair from a rising wedge. Although the fall was sharp, it was stopped by a combined support formed by the monthly PP at 1.1881 together with the bottom trend-line of a dominant ascending channel. On the one hand, today the buck might make another attempt to break to the bottom, using the downside momentum from the yesterday’s event. On the other hand, on a daily chart it looks like the rate formed a third reaction low yesterday and, for this reason, has to make a fully-fledged rebound.

EUR/USD: Fed Interest Rate Decision

The Euro fell sharply against its American counterpart, following the Fed’s announcement of its interest rate decision on Wednesday. The Euro dropped against the US Dollar by 0.91% or 109 base points to the 1.1903 mark, entering the area close the weekly low.

The two-day meeting of the Fed resulted in an overall agreement to keep interest rates unchanged at 1.25%, as widely anticipated. Despite lowered inflation forecasts, the FOMC still forecasted one more rate increase by the end of 2017 to sustain the US economic growth. The Central Bank also noted that it will start unwinding its balance sheet in October, while the market wanted it to wait and see how September’s hurricanes affected the economy.

GBP/USD: UK Retail Sales

The Sterling strengthened significantly against the US Dollar, as all the main components of the UK retail sales report showed better-than-expected figures for August. After the release, the GBP/USD jumped by 0.67% or 91 base point to touch the daily high of 1.3606 However, by the next couple of hours the pair resumed trading in a weaker area between the 1.3525 and 1.3560 marks.

The Office for National Statistics reported that both Britain’s retail sales and core retail sales rose 1.0% in August, beating expectations for a 0.2% rise and ignoring rising prices brought by post-referendum weakness of the Sterling. Therefore, strong figures are likely to boost expectations for the Bank of England’s rate hike announcement in November.

Dollar Bulls Awaken As Yellen Announces Twin Tightening

The struggling greenback has finally found a lifeline after the Federal Reserve maintained its intention to raise interest rates in 2017 and begin the process of trimming the balance sheet.

Before the Fed announced its decision, there were high expectations that monetary policymakers would drag interest rate expectations lower for 2017. This sentiment was due to persistently low inflation and the negative impact of Hurricanes Harvey and Irma on economic growth. Instead, the U.S. central bank decided to look past low inflation and said the harm of the Hurricanes would have no lasting economic impact.

The relatively hawkish statement and unchanged interest rates projections for 2017 and 2018, have forced market participants to adjust their expectations for an interest rate hike in December 2017, from a chance of 50% to above 70%. The repricing has boosted U.S. 2-year treasury bills by 5 basis points or 3.5%, to trade at the highest levels since Nov 2008, while the longer-dated 10-year bond yields hovered near a one-month high.

The primary beneficiary of the higher bond yields was the U.S. dollar, which rose to a two-month high against the Yen and sent the Euro below $1.19. For a couple of years, economists have been predicting the end of the three decades bull bond market, but this has never occurred due to investors pessimistic long-term inflation outlook. It is yet to be seen whether the reversal in yields will resume towards the end of the year.

The Consumer Price Index (CPI) and Personal Consumption Expenditure (PCE) for the next two to three months, are likely to be primary drivers of the U.S. dollar until the year-end. Janet Yellen herself does not know whether the slowdown in inflation is transitory or persistent, she simply described the slowdown as a "mystery" and said if the fed view changes on inflation, it would require an alteration in monetary policy.

Surprisingly, U.S. stock indices did not fall on a hawkish Fed. I believe lowering the estimated long-term neutral interest rates from 3% to 2.8%, prevented stocks from falling as overstretched valuations will continue to look acceptable, every time long-term interest rates are dragged lower. Back in 2012 longer run interest rates were seen around 4.25% and if they remained close to this level, it would have been tough to justify a PE ratio of 24 on S&P 500. However, it does make sense now.

Currency traders should continue to focus on interest rate differentials, as it will remain the primary driver of FX markets. Safe havens will also come under further pressure if U.S. yields manage to recover further and given no geopolitical surprises. If gold ended Friday below $1,295, this would attract sellers with the potential of testing the 50% retracement from $1,204 to $1,357 around $1,280.

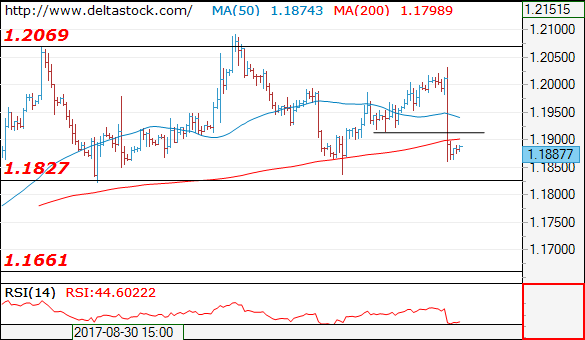

EURO Testing Monthly Pivot

The EURUSD pair has come under heavy selling pressure, as the U.S dollar index surged higher, following yesterday FOMC meeting. Following the monetary policy statement release, the 1-hour price-candle immediately spiked to 1.2031, then fell to 1.1861.

Price-action has subsequently recovered above the pairs 50-month moving average, at 1.1870, and is now probing the EURUSD monthly pivot point, at 1.1884.

Today's daily price close will be critical, as yesterday we saw the euro move price above the former weekly price high. Today the EURUSD must hold price above the former weekly price low, at 1.1838, to keep medium-term bullish trading sentiment intact.

Key intraday technical support is found at the 1.1870 level, and the pairs 50-day moving average, at 1.1851.

Below 1.1851, the former weekly low is found at 1.1838, with further support at 1.1815.

Resistance above the 1.1884 level is found at the Monday price low, at 1.1915, and the pairs weekly pivot point, at 1.1938.

Today's EURUSD daily calculated pivot point is found at the 1.1929 level

.

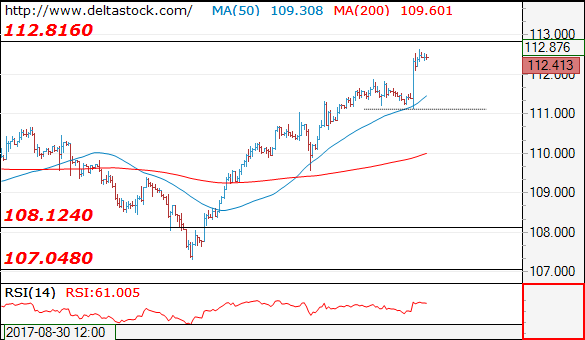

USDYEN Bullish After Fed And BoJ

The USDJPY pair has moved to its highest trading level since July 17th, hitting 112.64, after the Federal Reserve announced that they will start to taper their balance sheet in October and look to raise U.S interest rates one more time in 2017.

The Bank of Japan interest rate decision and press conference has largely been a non-event for foreign exchange markets, as the BOJ choose to keep monetary unchanged. The USDJPY pair trades close to its 8-week high, with price-action currently around the 112.40 region.

The USDJPY pair now trades above its monthly pivot point and 200-week moving average, indicating that the pair is now bullish in the medium and long-term while trading above these important technical levels.

Key intraday technical USDJPY resistance above the current daily price high is found at the 112.86, 113.20 and 113.89 levels.

Key intraday USDJPY support is found at the July 26th price high, at 112.19, and the pairs daily pivot point, at 111.98.

Below the 111.98 level, further intraday support is found at 111.87, and the USDJPY monthly pivot point, at 111.65.

.

Markets React To Fed, BoJ Continues Thursday

It has been a highly active week in the financial markets, with investors tracking a deluge of economic data and monetary policy developments. On Thursday, market participants will continue to dissect a pair of central bank meetings that shed important insights about the future.

The US Federal Reserve voted to keep interest rates on hold Wednesday and said it would begin to unwind its portfolio of bonds next month. Beginning in October, the Fed will reduce its portfolio holdings by $10 billion per month. At this pace, it'll be a few years before the central bank goes through half of its $4.5 trillion balance sheet.

Officials also voted to keep the federal funds rate on hold at 1.25%, and signaled that December was still primed for a rate adjustment.

The Bank of Japan (BOJ) also kept monetary policy on hold Thursday amid unexpected dissent. One member of the policy committee, Goushi Kataoka, voted against the decision to leave the target interest rates and asset purchase program unchanged.

The Japanese yen wasn't impacted by the decision, with the USD/JPY trading slightly higher during Asian trade.

Monetary policy will continue to drive the markets later in the day, with key speeches from European Central Bank (ECB) President Mario Draghi and Peter Praet, a member of the ECB's Executive Board. The ECB will also release its Economic Bulletin at 08:00 GMT. The publication takes a deep dive into the performance of the euro area economy.

Shifting gears to economic data, investors can expect a steady stream of reports over the next few hours. UK National Statistics will report on public sector net borrowing at 08:30 GMT. At the same time, the British Bankers' Association will release mortgage approvals for the month of August.

North American releases include US weekly jobless claims, the Philadelphia Fed's Manufacturing Survey and the Housing Price Index courtesy of the Federal Housing Finance Agency (FHWA). These reports will be released between 12:30 and 13:00 GMT.

USD/JPY

The USD/JPY is trading at two-month highs after risk appetite burned a hole through the yen. The pair was last up 0.1% at 112.46 after breaking sharply higher on Wednesday. The next psychological test comes just ahead of 113.00. On the downside, Tuesday's high at 111.87 provides a solid support zone.

GBP/USD

Cable held within a narrow range on Thursday after losing 100 pips during the previous session. It's still too early to conclude that the dollar bulls have regained control of the market. As such, the pair remains strongly supported at 1.3440.

EUR/USD

Like the pound before it, the euro dropped more than 100 pips after the FOMC meeting. The EUR/USD has fallen below the 1.19 handle. The September low of around 1.1835 offers good short-term support, but a break below that level would damage the euro's bullish outlook

Dollar Shines As Fed Meets Expectations, Yen Fails To Find Support On BOJ Decision

The dollar advanced against a basket of major currencies on late Wednesday, rising to a one-week high after the Fed's rate-setting committee decided to set October as the starting date of unwinding their overloaded balance sheet, while they also agreed to keep interest rates unchanged as markets had projected. Likewise, the BOJ's monetary decision early on Thursday matched expectations, with the central bank maintaining its monetary strategy steady. However, the BOJ's monetary outcome had little impact on market actions.

In a widely expected move, the Fed policymakers agreed unanimously on late Wednesday to keep interest rates steady in a range of 1-1.25%, while the FOMC statement signaled another rate hike of 0.25 percentage points probably in December. Besides that, the Fed reiterated in its statement that the rates will likely rise in a gradual path with the so-called dot plot of interest-rate forecasts showing three-quarter rate hikes in 2018, as was also signaled in June's meeting.

Regarding the withdrawal of quantitative easing, Fed officials voted unanimously to reduce the size of the $4.5 billion balance sheet next month, saying that $6 billion in Treasuries and $4 billion in mortgage-backed securities will be cut every month. The reductions in the holdings of the bonds are expected to rise every three months until they reach the amount of $30 billion and $20 billion respectively (for Treasuries and MBS).

Despite the financial damage from the recent powerful hurricanes, the Fed policymakers claimed that the negative impact from those storms will affect the country's economic performance only in the short term. In the medium term though, they anticipate the economy to continue strengthening, with improvements in the labor market driving inflation towards the Fed's 2% goal. Fed Chair Janet Yellen, commenting on inflation in her press conference after the two-day monetary meeting concluded said that the recent price slowdown was “mysterious”, while she added that if factors contributing to this slowdown are proven persistent, then the central bank will have to change its monetary strategy.

Following the FOMC statement, the dollar index surged by almost 1.20% to a one-week high of 92.46 before it slipped to 92.30 during the Asian session.

Dollar/yen hit a two-month high at 112.61, with markets showing a muted reaction to the BOJ's monetary decision early on Thursday. The Japanese central bank kept its charge on excess reserves from other financial institutions at -0.1%, while it also maintained its yield target for 10-year government bonds at 0% with an eight to one vote. In addition, the BOJ expressed its optimism on economic performance in its monetary statement, suggesting that there was no need for additional stimulus as economic activities are expected to recover gradually and push inflation towards the central bank's 2% target. However, the new member, Goushi Kataoka, seemed more dovish, arguing that the current policy was not sufficient to lift prices up to the target during 2019. In contrast, the BOJ's Governor, Haruhiko Kuroda, said in his press conference after the release of the monetary statement that current monetary strategy is supporting inflation but adjustments to this are not excluded if they are needed to maintain price momentum.

In other currencies, the aussie sank by 1% to $0.7956, in the wake of the Fed decision as well as due to comments made by RBA Governor Philip Lowe. Lowe stated at a business event in Perth that inflation is unlikely to rise to 2.5% anytime soon, with interest rates remaining at low levels for some time. Moreover, commenting on the direction of interest rates, he said that rates “are more likely to go up than down”.

The kiwi dropped by 0.60% to $0.7309 ahead of the national elections on September 23 although GDP figures for the second quarter published early today came in as expected. Specifically, New Zealand's output expanded by 0.8% q/q and by 2.5% y/y.

Regarding oil prices, WTI crude dropped by 0.24% on the day to $50.57 per barrel and Brent declined by 0.18% to $56.19 after the EIA weekly report indicated that US crude inventories during the past week rose more than expected.

Gold was down by 0.53% at $1,294.30 per ounce.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1887

Yesterday's reversal at 1.2035 has been confirmed with the break through 1.1915 and the bias is negative, for a tight test of 1.1830 major support. The latter is the last hurdle before 1.1660 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1915 | 1.2160 | 1.1830 | 1.1830 |

| 1.2035 | 1.2500 | 1.1830 | 1.1660 |

USD/JPY

Current level - 112.43

The recent consolidation built a base at 111.10 and the uptrend is intact, heading for a tight test of 112.80 resistance area. Initial intraday support lies at 111.90 and crucial on the downside is 111.10.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.80 | 112.80 | 111.90 | 108.12 |

| 112.80 | 114.50 | 111.10 | 107.30 |

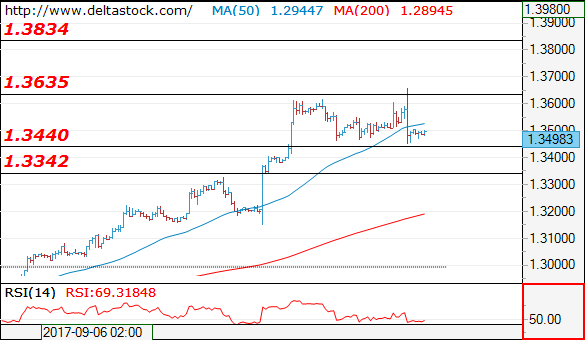

GBP/USD

Current level - 1.3498

The sharp reversal at 1.3655 signals a negative bias, for a test of 1.3440 support and a break through that area will challenge 1.3340 zone. Initial intraday resistance lies at 1.3530.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3530 | 1.3650 | 1.3440 | 1.3340 |

| 1.3650 | 1.3830 | 1.3340 | 1.3150 |

USDJPY Retains Medium-Term Neutral Outlook, Short-Term Bullish Phase Intact

USDJPY remains neutral in the medium term and has been trading in a broad range between 108 and 114 over the past 6 months. The near-term bullish phase that started last week from near solid support in the 108-area is still in place.

Momentum indicators are providing bullish signals, as the RSI has crossed above 50 and the MACD above zero. Ichimoku cloud analysis shows the market has risen above the cloud, while the Tenkan-sen line has crossed above the Kijun-sen line, giving a bullish signal.

The bounce off the September 8 low of 107.31 is still in progress. The short-term bias is strongly bullish after USDJPY rose above the 200-day MA to hit a high of 112.64 so far. There is scope for another push higher towards the top of the range at 114. Breaking above the July 11 high of 114.49 would allow the uptrend to extend further to target the next major peak at 115.50. From here the market would shift its neutral medium-term bias to a bullish one.

Failure to rise above resistance at 114 could see USDJPY reverse back down towards the lower end of the range. Immediate support is at the top of the cloud at 111.60. A drop into the cloud would change the short-term bullish technical tone and focus would turn to the 108-support area. Should this solid support level be broken, USDJPY would move out of the 6-month range and the medium-term picture would turn from neutral to bearish.

In the short term, there is limited risk to the downside but the medium-term outlook remains neutral within the established 6-month range between 108 and 114.