Sample Category Title

Trade Idea: EUR/JPY – Buy at 132.40

EUR/JPY - 133.82

Original strategy:

Buy at 132.40, Target: 134.40, Stop: 131.80

Position: -

Target: -

Stop: -

New strategy :

Buy at 132.40, Target: 134.40, Stop: 131.80

Position: -

Target: -

Stop:-

As the single currency has continued trading with a firm bias after recent rally, adding credence to our view that recent upmove is still in progress and bullishness remains for further gain to 134.50-60, then towards 135.00-10, however, near term overbought condition should limit upside and reckon 135.55-60 would hold from here, risk from there is seen for a retreat to take place later.

In view of this, we are looking to reinstate long on pullback as 132.30-40 should limit downside and bring another rise. Below support at 132.27 would defer and risk test of previous resistance at 132.01 (should turn into support) but only break there would signal a temporary top is formed, bring correction to 131.40-50 first.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

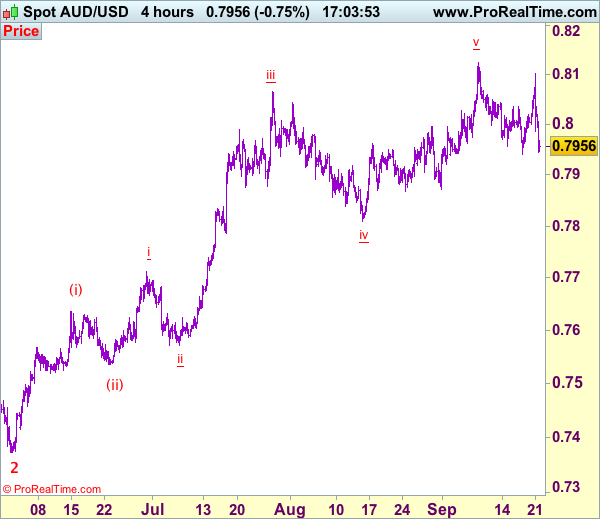

Trade Idea: AUD/USD – Sell at 0.8040

AUD/USD – 0.7957

New strategy :

Sell at 0.8040, Target: 0.7840, Stop: 0.8100

Position: -

Target: -

Stop:-

Although aussie rose briefly to 0.8103, the pair met renewed selling interest there and has dropped sharply (our original strategy to sell at 0.8080 turned out to be accurate and timely), retaining our view that further consolidation below recent high at 0.8125 (this month’s high) would take place and mild downside bias remains for weakness to 0.7900, however, break of support at 0.8967-71 is needed to confirm temporary top has been formed there, bring retracement of recent rise to 0.7800 first.

In view of this, we are looking to sell aussie again on recovery as 0.8040-50 should limit upside. Above said resistance at 0.8103 would abort and risk retest of 0.8125 but break of latter level is needed to confirm upmove has resumed and extend gain to 0.8150-60, then towards 0.8200 later.

On the 4-hour chart, recent upmove from 0.7329 is unfolding as an impulsive rise with wave 3 as well as smaller degree wave (iii) extending, only minor wave v of (iii) has ended at 0.8125, hence bullishness remains for this move to extend headway to 0.8200, then towards 0.8300, however, reckon upside would be limited to 0.8400 and the final wave 5 should falter below 0.8500, bring correction probably next week.

USD Gains As FOMC Keeps Its Rate Path Unchanged

The Fed kept interest rates unchanged yesterday, and announced it will begin to reduce the size of its enormous balance sheet in October, as was widely anticipated. In line with our view, policymakers kept the “dot plot” broadly unchanged as well to signal one more rate hike this year and another three in 2018.

This may have surprised investors looking for a downward revision in the rate path due to the recent soft patch in inflation. As a result, the probability for another rate hike by December jumped to 70%, and the market bought dollars aggressively.

What we also found interesting was Chair Yellen's comment during the press conference that the shortfall in inflation this year is largely a mystery, and that idiosyncratic factors don't fully explain the recent softness. In any case, the Fed chief made it clear that the Committee still expects inflation to rise in the future, mostly as a result of a very tight labor market that should, over time, push wages higher. This is in line with our view that the Fed could raise rates once again this year despite below-target inflation, like it did in June.

As for the dollar, we believe that it may remain under buying interest this week, as markets digest the “hawkish” Fed. As for the coming months, however, we believe that the USD's performance may depend primarily on its counterparts. For example, it could continue to gain against the weaker yen, but underperform against the almighty euro.

Gold fell yesterday as the Fed kept the door open for another hike this year. The slide came after the metal tested as a resistance the crossroads of the 1315 (R1) level and the prior uptrend line drawn from the low of the 10th of July. Subsequently, the bears managed to overcome the key support (now turned into resistance) obstacle of 1300 (R1). In our view, if the day closes below that hurdle, sellers may remain in the driver's seat and perhaps push the price below 1292 (S1). Such a dip may pave the way for our next support territory of 1280 (S2).

BoJ: The song remains the same

Overnight, the BoJ kept its policy unchanged as well, providing absolutely no hints that it is considering to alter its ultra-loose framework anytime soon. We share that view, given that even though inflation has risen a bit in recent months, it still remains very far away from the Bank's 2% target. If seen in isolation, the fact that the BoJ remains committed to ultra-expansionary policy should work against JPY over time, in an environment where other major central banks are either raising rates or showing signs they could do so soon. As such, we expect the yen to remain on the back foot in coming weeks, especially amid a risk-on market environment.

USD/JPY surged yesterday following the Fed decision. The pair rebounded from near the key support territory of 111.00 (S3), and rallied to emerge above two resistance barriers in a row. At the time of writing, the rate is trading above the 112.20 (S1) level and we expect it to challenge the 112.90 (R1) resistance soon. Given that the rate continues to trade above 111.00 (S3), and that yesterday's rally confirmed a forthcoming higher high on the 4-hour chart, we maintain the view that the near-term outlook is positive. A break above 112.90 (R1) may carry more bullish extensions and perhaps open the way for our next resistance of 113.60 (R2).

Today's highlights:

The Norges Bank will announce its own rate decision today, and the forecast is for the Bank to stand pat. When it last met, the NB removed its easing bias, while it revised slightly higher its expected rate path for 2017 and 2018. Since then, economic data have been mixed. The nation's GDP accelerated notably in Q2, which is in line with the Bank's forecast, while the unemployment rate slid further in August. On the other hand, inflation slowed in August, confounding expectations of accelerating. Given this slowdown in inflation, we think officials could push further back the timing of when they expect to start raising interest rates, something that could weigh on the NOK.

As for the economic indicators, in the US, the Philly Fed business activity index for September and initial jobless claims for the week ended September 15th are due out.

We have two ECB speakers on the agenda: President Mario Draghi and Executive Board member Peter Praet. Following the latest media reports suggesting there is division within the ECB regarding its QE exit, any further hints that the Bank may be headed for a “dovish tapering” could work against EUR.

XAU/USD

Support: 1292 (S1), 1280 (S2), 1265 (S3)

Resistance: 1300 (R1), 1315 (R2), 1333 (R3)

USD/JPY

Support: 112.20 (S1), 111.80 (S2), 111.00 (S3)

Resistance: 112.90 (R1), 113.60 (R2), 114.30 (R3)

(BOJ) Statement on Monetary Policy – September 21, 2017

1. At the Monetary Policy Meeting held today, the Policy Board of the Bank of Japan decided upon the following.

(1) Yield curve control

The Bank decided, by an 8-1 majority vote, to set the following guideline for market operations for the intermeeting period. [Note 1]

The short-term policy interest rate:

The Bank will apply a negative interest rate of minus 0.1 percent to the Policy-Rate Balances in current accounts held by financial institutions at the Bank.

The long-term interest rate:

The Bank will purchase Japanese government bonds (JGBs) so that 10-year JGB yields will remain at around zero percent. With regard to the amount of JGBs to be purchased, the Bank will conduct purchases at more or less the current pace -- an annual pace of increase in the amount outstanding of its JGB holdings of about 80 trillion yen -- aiming to achieve the target level of the long-term interest rate specified by the guideline.

(2) Guidelines for asset purchases

With regard to asset purchases other than JGB purchases, the Bank decided, by a unanimous vote, to set the following guidelines.

a) The Bank will purchase exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs) so that their amounts outstanding will increase at annual paces of about 6 trillion yen and about 90 billion yen, respectively.

b) As for CP and corporate bonds, the Bank will maintain their amounts outstanding at about 2.2 trillion yen and about 3.2 trillion yen, respectively.

2. Japan's economy is expanding moderately, with a virtuous cycle from income to spending operating. Overseas economies have continued to grow at a moderate pace on the whole. In this situation, exports have been on an increasing trend. On the domestic demand side, business fixed investment has been on a moderate increasing trend with corporate profits improving. Private consumption has increased its resilience against the background of steady improvement in the employment and income situation. Meanwhile, public investment has been increasing and housing investment has been more or less flat. Reflecting these increases in demand both at home and abroad, industrial production has been on an increasing trend, and labor market conditions have continued to tighten steadily. Financial conditions are highly accommodative. On the price front, the year-on-year rate of change in the consumer price index (CPI, all items less fresh food) is around 0.5 percent. Inflation expectations have remained in a weakening phase.

3. With regard to the outlook, Japan's economy is likely to continue its moderate expansion. Domestic demand is likely to follow an uptrend, with a virtuous cycle from income to spending being maintained in both the corporate and household sectors, on the back of highly accommodative financial conditions and fiscal spending through the government's large-scale stimulus measures. Exports are expected to continue their moderate increasing trend on the back of the improvement in overseas economies. The year-on-year rate of change in the CPI is likely to continue on an uptrend and increase toward 2 percent, mainly on the back of an improvement in the output gap and a rise in medium- to long-term inflation expectations. [Note 2]

4. Risks to the outlook include the following: the U.S. economic policies and their impact on global financial markets; developments in emerging and commodity-exporting economies; negotiations on the United Kingdom's exit from the European Union (EU) and their effects; prospects regarding the European debt problem, including the financial sector; and geopolitical risks.

5. The Bank will continue with "Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control," aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner. It will continue expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds 2 percent and stays above the target in a stable manner. The Bank will make policy adjustments as appropriate, taking account of developments in economic activity and prices as well as financial conditions, with a view to maintaining the momentum toward achieving the price stability target.

[Note 1] Voting for the action: Mr. H. Kuroda, Mr. K. Iwata, Mr. H. Nakaso, Mr. Y. Harada, Mr. Y. Funo, Mr. M. Sakurai, Ms. T. Masai, and Mr. H. Suzuki. Voting against the action: Mr. G. Kataoka. Mr. G. Kataoka dissented, considering that, since there remained an excess supply capacity in capital stock and the labor market, monetary easing effects gained from the current yield curve were not enough for 2 percent inflation to be achieved around fiscal 2019.

[Note 2] Mr. G. Kataoka opposed the description on the outlook for the CPI, considering that, although the year-on-year rate of change in the CPI was likely to increase for the time being reflecting developments in crude oil prices and foreign exchange rates, the possibility of the rate of change increasing toward 2 percent from 2018 onward was low at this point.

Technical Outlook: USDJPY – Extended Post-Fed Bullish Acceleration Approaches Targets At 112.80/113.00

The pair continues to trend higher after hawkish Fed boosted dollar on Wednesday and Bank of Japan, as expected, kept policy steady at the end of two-day meeting, keeping the overall bullish trajectory in play. Fresh extension approaches next targets at 112.80 (Fibo 76.4% of 114.49/107.31 descend) and psychological 113.00 barrier (also Fibo 50% of larger 118.66/107.31 descend). Bulls may take a breather at these points as strongly overbought slow stochastic on daily chart warns of pullback. Broken 200SMA (112.18) should ideally contain dips and guard daily cloud top (111.61) violation of which would sideline bulls and signal deeper correction.

Res: 112.80, 113.00, 113.57, 113.96

Sup: 112.35, 112.18, 111.75, 111.61

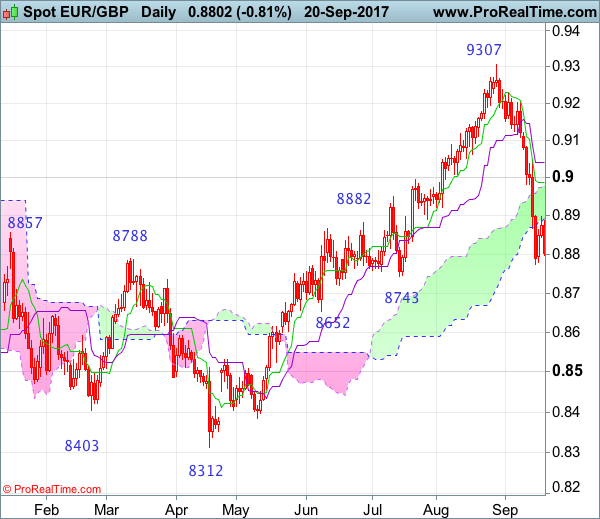

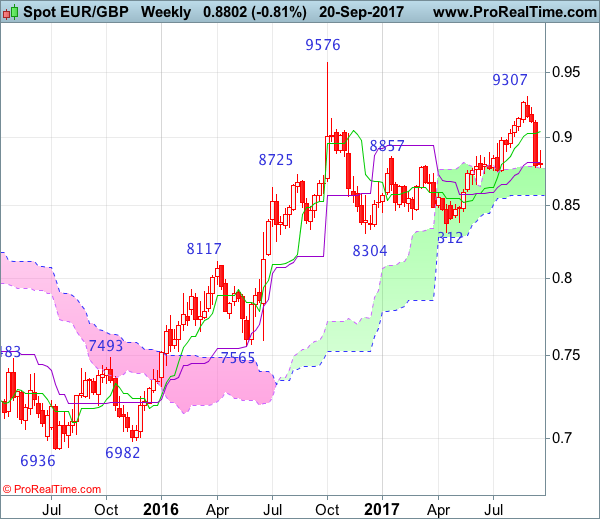

EUR/GBP Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: N/A

• ime of formation: N/A

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 29 Aug 2017

• Trend bias: Down

EURGBP – 0.8826

The single currency has dropped again since late last week, suggesting recent reversal from 0.9307 top is still in progress and may extend weakness to 0.8770, below there would bring further decline to 0.8740-43, then towards 0.8700, however, near term oversold condition should limit downside and as the aforesaid selloff is a bit over-extended, reckon previous support at 0.8652 would hold from here, risk from there remains for a much-needed corrective rebound to take place later.

On the upside, whilst initial recovery to 0.8870-75, then 0.8900 cannot be ruled out, reckon the Tenkan-Sen (now at 0.8948) would limit upside and bring another decline later. Above the upper Kumo (now at 0.9006) would defer and suggest a temporary low is formed instead, risk test of the Kijun-Sen (now at 0.9041) and then towards 0.9060-65, having said that, as top has been formed at 0.9307, reckon upside would be limited to 0.9100-10 and the pair shall head south again from there later.

Recommendation: Stand aside for this week.

On the weekly chart, last week’s selloff formed long black candlestick, dampening our bullishness and signaling recent upmove has indeed ended at 0.9307 earlier, hence consolidation would take place below said resistance for the rest of 2017 and downside bias is seen for at least a retracement of recent upmove to 0.8740-45, then 0.8700, however, as broad outlook remains consolidative (gyration within 0.8304-0.9576 range should take place), downside should be limited to previous support at 0.8652 and price should stay above 0.8590-00, bring rebound later.

On the upside, expect recovery to be limited to 0.8900-10 and 0.8950-60 should hold, bring another decline. Above the Tenkan-Sen (now at 0.9041) would defer and risk a stronger rebound to 0.9040-50, however, upside should be limited to 0.9120-25 and price should falter below 0.9190-00, bring another decline later. Above 0.9225-30 would abort and suggest the retreat from 0.9307 has ended instead, bring retest of this level later.

Technical Outlook: GBPUSD Is Consolidating Post-Fed Fall, Further Easing Seen On Sustained Break Of Key 1.3461/51 Supports

Cable is holding within narrow consolidation in early Thursday's trading, following 200 pips- wide range on Wednesday, when the pair was boosted by better than expected UK retail sales data and then hit strongly on hawkish tone from Fed.

The pair spiked to 1.3655 (the highest since June 2016) just before Fed and fell sharply to day's low at 1.3452 after hawkish Fed boosted the greenback.

Despite hitting fresh low at 1.3452, cable is still holding above lows of past three day's congestion and pivotal support at 1.3461 (Fibo 61.8% of 1.3148/1.3655 upleg).

Long upper wicks of Wed/Tue daily candles weigh on near term action, along with daily RSI which is reversing from overbought territory.

Sustained break below 1.3461/52 would trigger fresh bearish acceleration towards 1.3400 (rising daily Tenkan-sen and spark further downside on break here.

The pair may stay in prolonged consolidation while 1.3452 support holds.

Res: 1.3513, 1.3551, 1.3618, 1.3655

Sup: 1.3461, 1.3452, 1.3400, 1.3348

Technical Outlook: EURUSD – Techs Suggest Further Weakness After Consolidation

The Euro is consolidating above fresh post-Fed lows at 1.1865 zone in early Thursday, with scope seen for further downside.

The single currency was sharply lower on hawkish tone after FOMC September’s meeting. Fed signaled one more rate hike this year and plans three hikes in 2018, as well as start of reducing its portfolio in October.

Wednesday’s bearish acceleration was contained by daily Kijun-sen (1.1877) which was dented but without close below, leaving space for consolidation before bears resume.

Bearish Engulfing on Wednesday as well as formation of H&S pattern on daily chart is strong bearish signal which requires break below Kijun-sen as initial support and the H&S pattern’s neckline at 1.1842 for confirmation.

Fresh bears may travel towards 1.1720 (daily cloud top / Fibo 38.2% of 1.1118/1.2092 upleg) and 1.1662 (17 Aug trough) in extension.

Corrective upticks are seen as selling opportunities and should be capped by hourly cloud (spanned between 1.1967 and 1.1994).

Conversely, return above 1.2000 will be bullish signal.

Res: 1.1900, 1.1926, 1.1967, 1.1994

Sup: 1.1877, 1.1861, 1.1842, 1.1826

XAU/USD Analysis: Bypasses Psychological Level At 1,300.00

As it was expected, most of the previous trading day the pair spent in a surge, trying to reach and break through a barrier set by the 100-hour SMA and the upper edge of a descending channel. A decision made by the Fed to leave the interest rate unchanged an impulse strong enough to push the rate through a significant support, which was located near the 1,300.00 mark. From a general perspective, further movement of the pair is expected to continue to be guided by bears. As regards the current situation, after crossing the above psychological level the rate has not significant obstacles on its way up until the weekly S3 at 1,286.17, which is located at the intersection with the bottom boundary of the active formation. Hence, the gold is likely to lose some more value against the buck today.

USD/JPY Analysis: Tests Upper Boundary Of Long-Term Pattern

As with other major currencies, the Fed's decision to reduce the bonds it owns and keep the interest rate unchanged led to sharp appreciation of the Greenback against the Yen.

This surge forced the pair to test a combined resistance level formed by the monthly R2 at 112.54 in conjunction with the upper boundary of a long-term falling wedge. From this perspective, the exchange rate is likely to make a rebound and spend the upcoming month moving in the southern direction.

On the other hand, the pair continues to fluctuate in a junior ascending channel whose relevance is supported by the soaring 55-, 100- and 200-hour SMAs.