Sample Category Title

The Fed Draws A Clearer Picture Of Rate Hike By The End Of The Year

Dollar Rebounds After Fed Statement. As anticipated, the Fed announced it would begin from next month to reduce its approximately $4.2 trillion in holdings of U.S. Treasury bonds and mortgage-backed securities acquired in the years after the 2008 financial crisis. The dollar index was up 0.1 percent at 92.623 and near a two-week high of 92.697 set overnight, when it added 0.8 percent.

Dollar Extended Its Gains Against Euro. The euro is recovering from the losses suffered on Wednesday, when the common currency’s slide against the dollar nudged it away from a 21-month high of 134.160 set on Tuesday.

Kiwi Bounces as US Gains. The New Zealand dollar was down 0.3 percent at $0.7334, its rally the previous day petering out against a broadly stronger dollar. The kiwi soared to a 1-1/2-month high of $0.7435 on Wednesday after a poll showed New Zealand’s ruling National Party pulled ahead of the rival Labor Party ahead of a general election this weekend.

Dollar Hits 2-Month High Vs Yen On Heightened Fed Hike Expectations. The dollar rose to a two-month high against the yen on Thursday after a hawkish-sounding Federal Reserve heightened expectations for an interest rate hike in December.

Gold hits 3-week low. Gold dropped to its lowest level in over three weeks at $1295.65 on Thursday as a stronger US dollar and the increasing likelihood of another Federal Reserve interest rate hike this year curbed demand.

Oil Prices Dip Due to Hike in US Crude Production. Oil prices dipped during Thursday’s trade due to hike in US crude inventories and production as well as stronger dollar. US oil production has largely recovered from the shutdowns following Hurricane Harvey, currently standing at 9.51 million barrels per day (bpd), up from 8.78 million bpd directly after the storm hit the US Gulf Coast.

Watch Out Today for:

03:00 am GMT: JPY BoJ Interest Rate Decision

06:10 am GMT: AUD RBA’s Governor Philip Lowe Speech

07:30 am GMT: JPY Bank of Japan Governor Kuroda Speech

14:30 pm GMT: EUR ECB President Draghi’s Speech

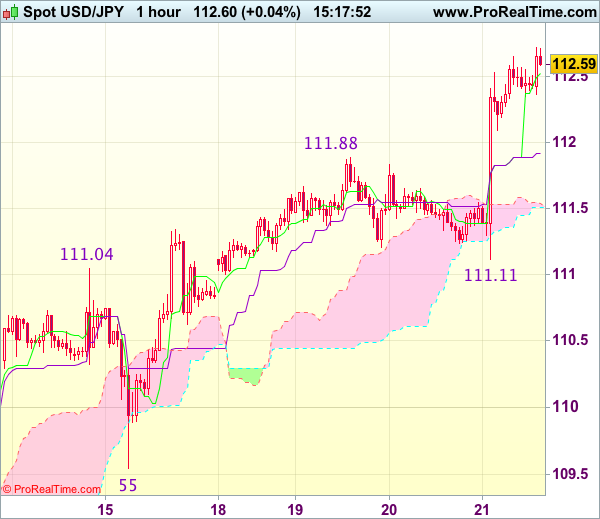

Trade Idea : USD/JPY – Buy at 111.90

USD/JPY - 112.60

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 111.53

Kijun-Sen level : 111.92

Ichimoku cloud top : 111.54

Ichimoku cloud bottom : 111.51

Original strategy :

Buy at 110.70, Target: 111.70, Stop: 110.35

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.90, Target: 112.90, Stop: 111.55

Position : -

Target : -

Stop : -

The greenback has rallied after finding renewed buying interest at 111.11 yesterday (after Fed), adding credence to our bullish view that recent upmove is still in progress and may extend further gain to 112.90-00, however, loss of near term upward momentum should prevent sharp move beyond 113.25-30 (1.236 times projection of 107.32-111.04 measuring from 109.55) and previous chart resistance at 113.58 would hold from here, bring retreat later.

In view of this, would not chase this move here and would be prudent to buy dollar on subsequent pullback as previous resistance at 111.88 should turn into support and contain downside, bring another upmove. Below the Ichimoku cloud (now at 111.51-54) would defer and suggest a temporary top is possibly formed, risk weakness towards support at 111.11.

XAUUSD Intraday Analysis

XAUUSD (1299.75): Gold prices extended the declines following a slight bounce. Failure to retest the resistance level at 1324 - 1320 saw gold prices posting sharp declines to slide to 1300 support level. This potentially marks the downside target in gold. There is scope for prices to now post a reversal off this support which could see a retest back to the initial resistance level followed by further gains on an upside breakout. To the downside, below 1300, gold prices could be seen testing the 1290 handle where the next support comes in.

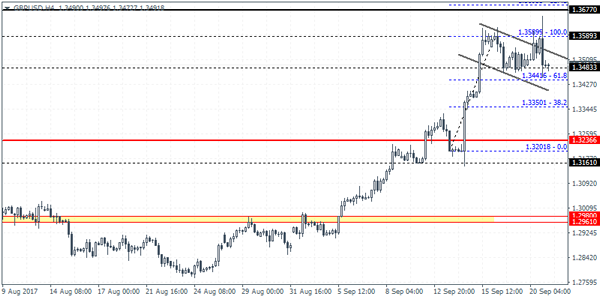

GBPUSD Intraday Analysis

GBPUSD (1.3491):The British pound closed with a doji yesterday as price continued to consolidate above the 1.3500 handle. The bullish flag pattern remains in play as GBPUSD is seen currently testing the support level at 1.3483. As long as this support holds, the bias is to the upside although resistance at 1.3590 will need to be breachedin order to set the stage for further gains. In the near term, GBPUSD could be seen consolidating within the resistance and support levels. A breakout from could either validate or invalidate the bullish flag pattern.

EURUSD Intraday Analysis

EURUSD (1.1885): The EURUSD fell sharply yesterday to close at a 4-day low. Price action is expected to continue the momentum, but the declines could be stalled near 1.1820. On the 4-hour chart, the head and shoulders pattern failed with price reversing strongly. EURUSD is seen currently supported at 1.1882 along with the rising trend line. This could offer some near-term support, but unless the bullish momentum sends the common currency to post fresh highs, we can expect this sideways pattern to continue.

US Dollar Jumps At Fed Signals One More Rate Hike This Year

The Fed's meeting yesterday was in line with expectations as the central bank announced its balance sheet normalization which starts in October. The Fed will be unwinding $10 billion per month in a mix of both Treasuries and MBS's. The central bank also signaled that there could be one more rate hike by the end of this year.

Inflation expectations were cut back from policy makers for 2017 and 2018, and there was one less rate hike projected for next year. The Fed's meeting saw the US dollar postingstrong gains with the markets now re-pricing the possibility of another rate hike this year.

Later in the evening, New Zealand's quarterly GDP data showed that the economy expanded at a pace of 0.8% as expected. Q1 GDP data was also revised higher to show a 0.6% increase.

Looking ahead, the BoJ's monetary policy and press conference are coming up today. The central bank is expected to keep policy unchanged at today's meeting. The ECB President, Mario Draghi will be speaking later in the afternoon which could pose some risks for the euro currency.

Currencies: Will Fed’s ‘Normalization Commitment’ Finally Support The Dollar?

Sunrise Market Commentary

- Rates: Flattening US yield curve after Fed verdict

US Treasuries lost ground yesterday after the FOMC decision, flattening the yield curve. We conclude that US Treasuries reentered a sell-on-upticks phase after the Fed confirmed his view on 2017/2018 interest rate policy. A December rate hike isn't fully discounted yet. Short term though, we could get some correction higher after a nine straight days decline. - Currencies: Will Fed's 'normalization commitment' finally support the dollar?

The dollar jumped higher across the board yesterday as the Fed indicated that it wants to continue a gradual rate hike cycle. Of late markets hardly believed the Fed's intentions. Will this time be different? A break below the EUR/USD 1.1823 correction is needed soon in order to create a more constructive sentiment on the US currency

The Sunrise Headlines

- US equities dropped on the FOMC decision, but it was a knee-jerk reaction and main indices closed narrowly mixed. A similar picture in Asia overnight, as markets have difficulties to find a firm direction (firmer dollar).

- The Fed indicated it remained on track to raise short-term rates later this year and said it would begin shrinking its portfolio of bonds next month, starting to close the books on an unprecedented and controversial policy experiment.

- The Bank of Japan kept monetary stimulus unchanged, but a dovish new board member opposed the decision in his first meeting, an unexpected dissension on a board chosen entirely by Prime Minister Shinzo Abe.

- Spain's government is willing to discuss giving Catalonia more money and greater financial autonomy if the region backs down from its demands for independence, one of Madrid's senior ministers has told the Financial Times.

- Greece is considering swapping 20 small bond issues for a few new ones, as it prepares to exit its bailout. It would consolidate the secondary market into a few liquid benchmark issues.

- Shares in Australian gold miners were down as the price of the precious metal neared a one-month low after the US central bank said it would start to reverse its crisis-era stimulus programme from next month.

- Today's calendar contains the Philly Fed business survey and EMU consumer confidence. ECB Praet and Smets speak. France, Spain and the US tap the bond markets. The Norges Banks meets and the Riksbank publishes Minutes.

Currencies: Will Fed's 'Normalization Commitment' Finally Support The Dollar?

Dollar jumps as Fed maintains course

Yesterday, the Fed, as expected, announced the start of the run-off of its balance sheet, while the policy rate was left unchanged. The Fed kept its rate path (median dots) of one more 25 bps rate increase this year and three next year. The process of gradual policy normalisation will continue even as several uncertainties remain. US yields rose modestly and the curve flattened. The dollar reacted accordingly. EUR/USD tumbled from about 1.20 to the 1.1862 area and closed the session at 1.1892. USD/JPY jumped to the mid 112 area and finished at 112.22.

Overnight, Asian equities are trading mixed. A stronger dollar and higher US yields are a mixed factor for Asian/EM markets. The BOJ, as expected, left its policy (target rates and asset purchases) unchanged. A new member, Kataoka, dissented as he saw little chance of the BOJ reaching its target in 2019. So, there was a soft note in the policy decision. Even so, USD/JPY makes only modest additional gains after yesterday's post-Fed rally. USD/JPY trades at 112.43. EUR/USD stabilizes around 1.1885.

Today, the calendar contains EMU consumer confidence and speeches of ECB Praet and Smets. Consumer confidence is expected stable, just below its cyclical highs. The debate on the ECB's APP programme is in full swing. Smets and Praet are close to Mario Draghi and key players inside the ECB. So, any comments from them on the fate of APP won't go unnoticed. In the US, initial claims are expected to rise as a result of the tropical storms. Markets will ignore the increase as noise. The Philly Fed business survey is expected to show a stable, but strong headline figure (17.1). The headline index was volatile since the start of the year, but on the positive side. A good report might be slightly USD supportive.

Investors will take a second look at yesterday's Fed policy decision. The dollar made a nice rebound, but EUR/USD still didn't break any technically important level. The Fed assessment basically remains unchanged. Question is whether markets will gradually give more credence to the Fed rate path than they did until now. We see a chance for a modest dollar comeback as yesterday's Fed 'guidance' suggest that there is little reason for US yields to decline again from current levels unless there comes high profile negative news. A fast break below EUR/USD the 1.1823 ST range bottom would be an indication that the USD rebound has somewhat further to go. Otherwise, doubts will soon return

From a technical point of view EUR/USD hovers in a consolidation pattern between 1.1823 and 1.2070. It was disappointing for EUR/USD bears that last week's correction didn't reach the range bottom. More confirmation is needed that the bottoming out process in US yields and in the dollar might be the start of more sustained USD gains (against the euro). In case of a break, next support in EUR/USD comes in at 1.1774 and 1.1662

The day-to-day momentum in USD/JPY remains more constructive. The yen trades weak across the board and the dollar might be in better shape post-Fed. USD/JPY regained the 110.67/95 previous resistance. This a short-term positive. The yen might stay under pressure at least until the next event risk pops up. The 114. 49 correction top is the next important reference.

EUR/USD: will the dollar be able to capitalize on Fed normalization call?

EUR/GBP

EUR/GBP nears again the correction low

Yesterday , UK August retail sales were reported strong, supporting the recent BoE call for a rate rise in the coming months. A first sterling rebound after the report was short-lived and EUR/GBP returned to the 0.8880 area. This suggested that the GBP rally was losing momentum. However, EUR/GBP gradually declined again later on during the US session. The decline of EUR/GBP accelerated in line EUR/USD after the Fed policy decision. The pair closed the session at 0.8813. Cable finished the session little changed at 1.3495, a good sterling performance.

Today, the UK public finance data will be published, but they are at best only of intraday significance. Markets will look forward to the speech of UK MP on Brexit tomorrow in Italy. Earlier this week, it looked the speech could give the Brexit process a new positive dynamic, but recent comments sounded again sceptical. In this context, is there room for further GBP gains? Will EUR/GBP feel some pressure from a further decline in EUR/USD? Last week's correction low at 0.878 is a first key support.

EUR/GBP made an impressive uptrend since April and set a MT top at 0.9307 late August. The euro was strong and UK price data were soft enough to keep the BoE side-lined. Recent UK price data amended this story and the ST-trend reversal of sterling was reinforced by hawkish BoE comments. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of relative euro strength and sterling softness to persist. However, the prospect of (limited) withdrawal of BOE stimulus put a solid floor for sterling ST term. We look out how far the current correction has to go. EUR/GBP is nearing support at 0.8743 and 0.8652, which we consider difficult to break. We start looking to buy EUR/GBP on dips.

EUR/GBP: GBP-rebound rebound slows

Elliott Wave View: DXY Double Correction

DXY Short Term Elliott Wave view suggests that the decline to 91.01 ended Primary wave ((3)). Primary wave ((4)) bounce remains in progress as a double three Elliott Wave structure. Up from 91.01, Intermediate wave (W) ended at 92.66 and Intermediate wave (X) ended at 91.591. Near term, while pullbacks stay above 91.591, expect Index to extend higher towards 93.227 – 93.618 area to complete Primary wave ((4)). Afterwards, Index should resume the decline lower or at least pullback in 3 waves. We don't like buying the proposed bounce.

DXY 1 Hour Elliott Wave Chart

Double three ( 7 swings) is the most important pattern in Elliott wave's new theory. It is also probably the most common pattern in the market these days. Double three is also known as a 7-swing structure. It is a very reliable pattern that gives traders a good opportunity to trade with a well-defined level of risk and target areas. The image below shows what Elliott Wave Double Three looks like. It has labels (W), (X), (Y) and an internal structure of 3-3-3. This means that all 3 legs has corrective sequences. Each (W) and (Y) is formed by 3 wave oscillations and has a structure of A, B, C or W, X, Y of smaller degrees.

Focus May Now Turn To The ECB

Market movers today

Markets will continue to digest the FOMC meeting yesterday,

In the Scandi markets, today's key event is the Norges Bank meeting, where we share the consensus view that Norges Bank will not touch interest rates. The minutes from the Riksbank's September meeting are also due out (see page 2).

In the euro area, consumer confidence data for September is due out . Wage growth has started to pick up in Q2, but as inflation has also increased since 2016, real wage growth remains low and could act as a drag on consumer confidence. We expect a small decrease in confidence to -1.6 in September.

In the US, the Fed Philly index for September is due to be released, which we expect to fall somewhat given the extremely large gap between ISM manufacturing and Markit PMI manufacturing. The numbers may be somewhat affected by the recent hurricanes although it remains our base case that any impact should be short -lived.

ECB president Mario Draghi is also due to speak in Frankfurt this afternoon.

Selected market news

The FOMC statement yesterday came out on the hawkish side compared to market pricing with the Fed still projecting another hike this year and three more hikes next year. It compared with a market that was pricing in less than two hikes by the end of 2018 ahead of the meeting. The message from the Fed pushed bond yields up and sent EUR/USD below 1.19. Equity markets initially sold off but recouped the losses and finished broadly flat . Asian markets are mostly higher but the S&P future is treading water in overnight trading. The Fed's projection is broadly in line with our own expectations as we see a continually tightening labour market as keeping the Fed on the path of very gradual rate hikes.

Focus may now turn to the ECB with a long list of speeches in coming days from ECB members, see Bloomberg. The markets will be looking for clues on what to expect at the important 26 October meeting, when the ECB has stated it will give more clear signals on its exit strategy.

Otherwise, the next thing up is the German election on Sunday, although German Chancellor Angela Merkel is widely expected to win. While she has lost some ground recently, the polls still point very much to another term for her.

The Bank of Japan kept monetary policy unchanged this morning but a dovish new member dissented the decision. However, this was widely expected. The JPY did not move on the announcement.

Market Update – Asian Session: Markets Little Changed As BOJ And Fed Decisions Come In As Expected

Asia Summary

Asian equity markets opened mixed, Google and HTC confirmed a cooperation agreement with the transfer of some employee assets to Google. Nikkei opening the strongest ahead of BOJ. Broad dollar strength the theme in the currencies, after the Fed statement was widely in line with expectations. Bank of Japan (BOJ) also left policy unchanged, as expected. Little movement in USD/JPY as a result, holding around 112.40. Dissenter Kataoka said yield curve control is not enough to meet inflation target ~FY19 and sees low chance of CPI increasing from 2018 on.

China PBOC sets yuan reference rate-0.3% at 6.5867, the weakest level since Sept 1st. Onshore yuan fell 0.4% to 6.601 per dollar, in line for weakest closing level since Aug. 28 . Offshore yuan declines 0.2% to 6.5984. The HKMA was un-usually chatty about the HK$, saying they believe the USD/HKD to eventually weaken to 7.85 (currently 7.8013) v trading band 7.75-7.85; Will not roll out measures to support HK$ rate.

Key economic data

(JP) BANK OF JAPAN (BOJ) LEAVES INTEREST RATE ON EXCESS RESERVES (IOER) UNCHANGED AT -0.10%; AS EXPECTED

(NZ) NEW ZEALAND Q2 GDP Q/Q: 0.8% V 0.8%E; Y/Y: 2.5% V 2.5%E

(KR) South Korea Sept Exports 20-days Y/Y: +31.1% v 11.6% prior; Imports Y/Y: 23.9% v 11.2% prior (corrected by South Korea Customs Agency)

(AU) Australia Aug RBA Govt FX Transactions (A$): -0.6B v -1.03B prior

(NZ) NEW ZEALAND AUG CREDIT CARD SPENDING M/M: -0.7% V 0.8% PRIOR; Y/Y: 6.4% V 7.1% PRIOR

Speakers and Press

China/Hong Kong

(CN) PBoC Guangzhou Branch bans long-term consumer loans - Chinese Press

USD/HKD (HK) HKMA's Yue: Believes USD/HKD to eventually weaken to 7.85 (currently 7.8013) v trading band 7.75-7.85

(CN) China National Development and Reform Commission (NDRC) releases guidelines related to minimum and maximum coal inventories: Coal producing regions must guarantee supply

(CN) China Commerce Ministry (MOFCOM): Hopes can work together with EU and oppose global trade protectionism; willing to quicken China/EU investment talks and expand bilateral investment

Korea

(KR) South Korea Vice Fin Min: Impact of FOMC on domestic markets won’t be ‘big’

(KR) Korea Institute for International Economic Policy (think tank) says China's actions related to Thaad missile defense system hurt the Chinese

(KR) Bank of Korea (BOK) quarterly statement on financial stability: household debt growth is expected to stabilize on property measures released Aug. 2 and additional steps to be released soon on household debt

Japan

(JP) Columbia University professor Takatoshi Ito (candidate to be next BOJ Gov): If the BOJ reaches its 2% inflation target in two years, it will take another five years to wind down

New Zealand

(NZ) RBNZ comments on approach for bank disclosure: Key bank metrics to be disclosed quarterly

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.4%, Hang Seng +0.0%; Shanghai Composite +0.2%, ASX200 -1.0%, Kospi +0.0%

Equity Futures: S&P500 -0.0%; Nasdaq100 -0.1%, Dax +0.0%, FTSE100 -0.3%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1895-1.1865; JPY 112.64-112.27; AUD 0.8034-0.7993;NZD 0.7364-0.7326

Dec Gold -0.2% at $1,303/oz; Nov Crude Oil +0.0% at $50.70/brl; Dec Copper -0.6% at $2.94/lb

(CN) PBoC OMO: injects CNY60B in 7 and 28-day reverse repos v injected combined CNY30B in 7 and 28 day reverse repos prior

USD/CNY (CN) China PBOC sets yuan reference rate at 6.5867 v 6.5670 prior (weakest level since Sept 1st)

(NZ) New Zealand sells NZ$200M in 2.75% 2025 bonds; avg yield 2.9072%; bid-to-cover 3.91x

(TH) Thailand Central Bank sells THB45B in 3-yr central bank bond; avg yield 1.5024%; bid-to-cover 2.50x

Equities notable movers

Australia/New Zealand

CBA.AU Confirms AIA to acquire Life Insurance unit for A$3.8B, enters 20-yr partnership with AIA; Undertaking a strategic review of its global asset management business; will consider a range of options, including an IPO; -0.1%

MGC.AU Mongolia Yili Industry Group, a privately-owned Chinese dairy company, made a higher than expected bid with speculation that the bid may be as high as A$1.20/shr - Aussie press; +9.5%

Japan

3064.JP Weakness attributed to report of Amazon starting B2B business in Japan; -5.5%

Taiwan

2498.TW Confirms $1.1B cooperation agreement with Google, where Google will acquire part of HTC engineering team related to Pixel phone

Hong Kong/China

3908.HK Tencent to acquire 4.95% stake; +11.6%

439.HK Subsidiary signs strategic partnership with Xiong'an new area; +9%