Sample Category Title

Fed Announces Tapering But No Rate Hike; Unchanged Dots Seen as Hawkish

Highlights:

- The target range for the fed funds rate was left unchanged at 1.00-1.25% as expected.

- The Fed announced they will implement a previously-outlined plan to begin shrinking their balance sheet by tapering reinvestment next month. The fed funds rate remains the committee's main policy tool and the Fed does not expect to make changes to the balance sheet normalization program outlined in June.

- An otherwise little-changed policy statement indicated the Fed will be looking through the transitory effect of recent severe weather on economic activity and inflation.

- Economic projections only saw minor tweaks. Current-year GDP growth was revised higher but core PCE inflation is expected to be slightly lower.

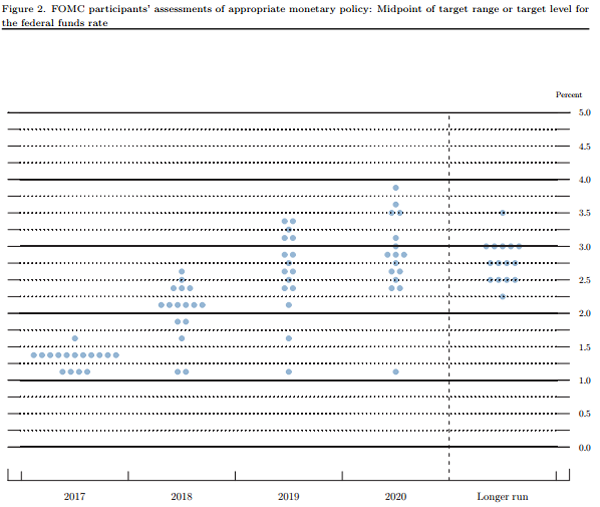

- The 'dot plot' continues to show a majority of committee members expect one more rate hike this year, while a median of three hikes are still seen as appropriate next year.

Our Take:

There was little doubt about the outcome of today's meeting—a change in reinvestment policy and pause in rate hikes had been well-signaled by policymakers. So instead the focus was on the Fed's thoughts on inflation and any implications for the pace of tightening outlined in the 'dot plot'. In the event, Chair Yellen's comments largely stuck to the script: inflation has been held down by some transitory factors and should return to the Fed's 2% objective as those factors dissipate and tighter economic and labour market conditions put upward pressure on prices. That view was backed up by a little-changed set of 'dot plot' projections showing another rate hike is likely by the end of this year with three more rate hikes seen next year. Confirmation that gradual tightening is likely to continue despite slowing spot inflation prompted a modest USD rally and slight selloff in Treasuries.

Upcoming economic reports are likely to be impacted by severe weather—there was already evidence of that in the latest data for August. While those effects should prove transitory, they will make it a bit trickier to get a read on the economy's underlying growth trend. The Fed is well aware of this, so we don't see a couple of disappointing reports knocking them off their plan to continue on a path of gradual rate hikes. That path remains data dependent, however, and further downside surprises on inflation in particular might lead to a more cautious removal of accommodation. In that sense it was encouraging to see some signs of stabilization in recent CPI data. We continue to expect one more rate hike in December and further moves next year.

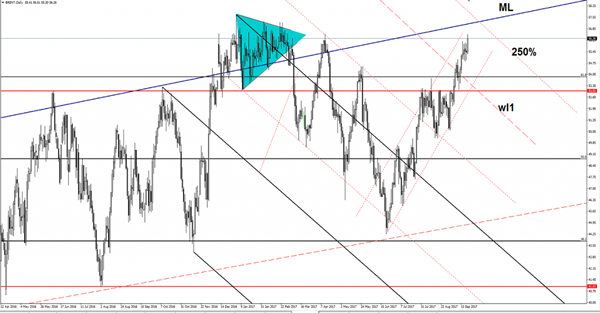

Brent Oil Ignores The Crude Levels

The Brent rallies and seems determined to reach the $57 per barrel in the upcoming days. Is strongly bullish on the short term and resumes the upside movement as predicted. Price increased even if the United States Crude Oil Inventories were reported at 4.6M in the previous week, much higher versus the 2.8M estimate. The next target will be at the median line (ML) of the major ascending pitchfork, it could be attracted by the confluence area formed between the ML with the 250% Fibonacci line.

Gold Further Decrease Confirmed

The yellow metal is trading in the red and will hit fresh new lows if the USDX will jump much higher. Gold edged lower and invalidated the breakout above the WL1 (descending dotted line) and above the uptrend line. Price reached the 23.6% retracement level, where has found temporary support, a valid breakdown below this obstacle will confirm a further drop towards the 38.2% retracement level.

USD/JPY BOJ Eyed

The currency pair rallied in the last hours and reached some important resistance levels. Is trading in the green even if the Federal Reserve has decided to keep the Federal Funds Rate steady at 1.25%. The greenback rallied versus all its rivals after the FOMC, the USDX jumped aggressively and now is pressuring the 92.49 static resistance again.

I've said in the previous weeks that only an accumulation will signal another broader rebound. The index is still trapped below some important resistance levels. Technically, the index is still expected to turn to the upside and to recover after the immense drop.

The Japanese Yen drops further as the Nikkei extends the current rally. JP225 increased as much as 20413 level and seems motivated to reach new peaks in the upcoming hours.

Price edged higher and erased the morning losses as the USD bulls have stepped in again and have taken the lead. USD/JPY has jumped much above the 38.2% retracement level and have reached the first warning line (wl1) of the ascending pitchfork and the median line (ml) of the minor blue ascending pitchfork.

A breakout through the confluence area formed between the mentioned levels will accelerate the upside momentum, only a rejection will send the rate down again.

Feds Hawkish Dots Surprise

Feds Hawkish Dots Surprise

The Fed(dots) surprised on the hawkish side, paving the road for a broad USD rally as the FX markets activity roared back to life with volumes surging. US 10y yields rose 6bps towards 2.29%, while equities and gold all took a dip lower.

The markets jumped to attention when twelve Fed officials (up from eight in June) still want to hike at least once more in 2017. This overwhelming sign of confidence in the US economy caught traders by surprise and has transiently quashed the market view to sell dollar on rallies. While the Feds hawkish shift does not guarantee a December hike, it will take an unlikely string of tepid economic data to turn the Feds current suasion, but this unexpected policy lean should change investors view of the greenback from a red light zone to an amber scenario.

This change in sentiment is visible on the-the CME FedWatch Tool where the December rate hike probabilities are no longer profoundly underpriced. And with the markets underestimating on only about one-and-a-half hikes through the end of 2018, far below the Fed’s June middlemost view of four, a string of positive US economic numbers or even a glint of wage inflation could light a fire under the dollar bulls, and the USD could make an unlikely revival

If the markets were looking for a new US dollar narrative, today’s hawkish fed resolve is providing that fodder.

The markets were focusing on the Fed inflation view, and Chair Yellen did not disappoint the dollar bulls stating that inflation undershoots are “transitory…more broadly based” and are likely to “fade away.” While doubling down, stressed the Feds view that monetary policy also repeats with a lag…that’s also a risk that we want to be careful not to allow the economy to overheat.”

Well, folks, it doesn’t get any more brazenly hawkish from Dr Yellen who along with the majority of her colleagues are clearly in the December rate hike camp and the markets are reacting to this news.

The Euro

EURUSD caved from the 1.2000 area towards 1.1860 and them found a happy place near 1.1900.The EURO is holding the critical support zone as pre FOMC comments from another ECB hawk, Netherland’s Knot, stating that the ECB does need a recalibration of policy continues to resonate.

While today’s hawkish Fed resolve is a win for the greenback, the Euro bulls will likely to fade the EURUSD weakness as they continue to view the EURO as cheap in the face of the ECB policy convergence

Japanese Yen

USDJPY cruised for pre-FOMC 111.10 levels to 112.20 before Yellen took to her post FOMC presser when then a high of 112.60 was printed. We’ve come off the highs in early APAC trade as the Asia traders continue to digest the overnight events.

Australian Dollar

The Aussie broke the .8100 level on the FOMC spike and got pummeled lower to the .7990 before finding some legs to march back above.8025 in early Asia trade. Regional currency sentiment, especially in Asia EMFX, remains stout on ebbing capital outflows and I think this is also boosting the Aussie sentiment which is used as a liquid G-10 proxy for APAC. Also, the Commodity Bloc is getting a boost from WTI prices which climbed above $51.07 into the Fix. Prices retreated after the FOMC meeting but just mildly as market sentiment remains buoyed by the Iraq oil minister’s comments that Opec was considering additional production cuts.

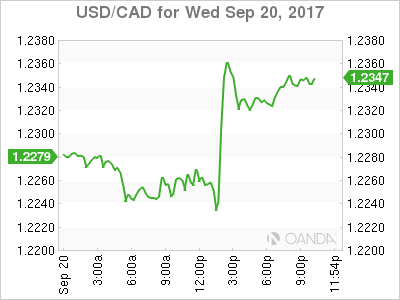

USD/CAD Canadian Dollar Lower After Fed Statement

Fed members forecast one more US rate hike

The Canadian dollar is lower against its US counterpart on Wednesday. The U.S. Federal Reserve published its updated economic projections and as expected kept the interest rate unchanged at 100-125 basis points. Also keeping with market forecasts the US central bank announced it will start the reduction of its balance sheet in October. The start date was the only piece missing as the Fed has already outlined the process it would follow.

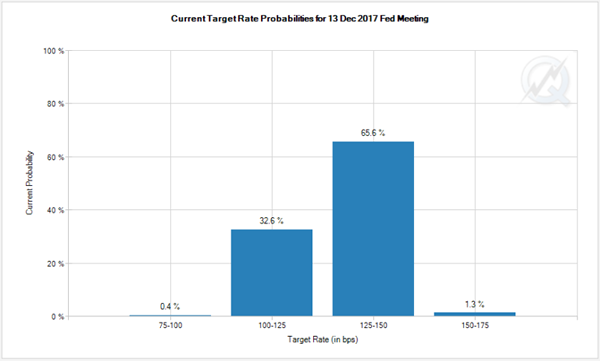

The loonie had been trading higher against the USD ahead of the Federal Open Market Committee (FOMC) statement but retreated once the economic projections were published. The main takeaway was the number of members that still see a rate hike in 2017. 11 out of 16 officials still see the appropriate level for this year at 125 to 150 basis points. Fed Chair Janet Yellen press conference did not add a lot of additional details but went through the statement and faced questions from the financial press. The Fed is facing a balancing act of strong growth and solid employment but on the other hand declining inflation.

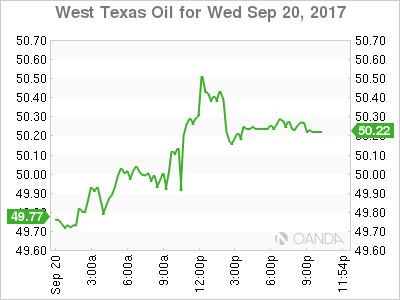

Oil rose during the day, despite the larger than anticipated weekly US crude inventories reported this morning. The higher than expected number was taken as a positive given the disruption caused by Hurricane Harvey and Irma in oil refineries and platforms.

Canadian inflation and retail sales data due on Friday will close the week for CAD traders. The currency pair will now trade guided on other economic indicators, geopolitical events and the statement of the Bank of Japan (BOJ).

The USD/CAD rose 0.612 percent on Tuesday. The currency pair is trading at 1.2347 after the U.S. Federal Reserve announced the beginning of its balance sheet reduction plans. The pair is near daily highs as the dollar rally stalled once Fed Chair Janet Yellen press conference started. The US central bank updated its economic projections and while inflation remains muted there are still 11 members who are forecasting another price hike before the end of the year.

The Fed has raised rates at the December Federal Open Market Committee (FOMC) meeting in the past two years and could do so at the final meeting of the year. The central bank has supported the dollar with 2 rate hikes in 2017 so far, and is now shedding its massive balance sheet. The portfolio of bonds that were accumulated as part of the stimulus program will shrink by $10 billion each month.

US energy prices rose 1.433 percent in the last 24 hours. The price of West Texas Intermediate is trading at $50.18 near a four month high. Sparks between the United States and Iran and signals from Organization of the Petroleum Exporting Countries (OPEC) and nom-members about extending the production cut agreement supported higher energy prices. A meeting is scheduled for this Friday with could come with confirmation of an extension beyond March 2018.

The Energy Information Administration (EIA) report of weekly US crude inventories showed a higher than expected rise at 4.6 million barrels. The glut is seen as a positive given the disruptions in American production and proof of the flexibility and speed of shale output.

Market events to watch this week:

Wednesday, September 20

6:45pm NZD GDP q/q

11:50pm JPY Monetary Policy Statement

Thursday, September 21

Tentative JPY BOJ Policy Rate

2:30am JPY BOJ Press Conference

8:30am USD Unemployment Claims

Friday, September 22

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

8:30am All Day NZD Parliamentary Elections

USD Rallies As Fed Holds Firm On Rate Hikes

The US dollar made a comeback on Wednesday after the Fed stood by its previous belief that interest rates will rise once more this year.

Markets have been increasingly pricing this out in recent months with inflation data, Fed commentary and the recent economic impact of hurricanes among the reasons for this. The Fed though remains undeterred and only marginally revised lower projected Fed funds rate for 2019.

The dollar – which for a while has looked extremely stretched having fallen more than 10% from its peak at the start of the year – rallied quite aggressively after the release of statement and projections and has stabilised near its highs throughout Chair Janet Yellen’s press conference.

Whether these moves will be maintained we’ll see over the next few days but with a number of dollar pairs having already stumbled, there is potential for an arguably long overdue dollar correction to take place. The ECB will probably be more relieved than anyone, with suspicious “sources” releasing statements every time the EURUSD pair reached 1.20, clearly a sign that the central bank does not like this level. With it back below 1.19, at least for now, the ECB will likely be much more content.

The hawkish Fed position weighed on Gold which fell back below $1,300 for the first time since August. With geopolitical risk subsiding, at least for now, and the Fed maintaining its view on interest rates, Gold below $1,300 may become the norm once again.

US Treasuries also jumped to their highest since early August as the probability of a rate hike jumped to around 67%.

Fed Keeps Rate Unchanged Announces Balance Sheet Reduction

The U.S. Federal Reserve kept the benchmark US interest rate unchanged at 100-125 basis points as expected and also anticipated was the announcement that the central bank’s balance sheet will start its reduction in October.

The US dollar has advanced across the board as the economic projections from Fed members are mixed, but there are still some members forecasting a rate hike later in the year.

December Dots Drive Dollar

The FOMC delivered a hawkish forecast on Wednesday and a fresh message of cautious optimism despite a hurricane-driven setback. The US dollar jumped across the board on the headlines while the euro was the laggard on the day. The Bank of Japan is next. A new JPY trade has been issued ahead of the Fed.

We warned about a hawkish surprise ahead of the Fed and the implausibility that the dots would be significantly downgraded. They weren't. 12 of the 16 FOMC attendees expect the Fed to hike again this year, that's the same as in June.

That's a strong message that despite worries about inflation, the Fed remains optimistic about the economy. That was partly reflected in the statement, where they touted a pickup in business investment. The formal forecasts on GDP, jobs and PCE inflation were tweaked but not enough to overshadow the dots.

It is a similar story for 2018, where the Fed median continues to show three hikes in addition to one before year end. The market doesn't believe in such an aggressive path and the Fed has frequently overstated the path but even two hikes in the next 15 months may be sufficient for a sustained USD bid.

As expected, the balance sheet reduction will also get underway in October but we will have to wait a few weeks before we get more details.

We won't have to wait long, however, for more central bank news. The BOJ decision is due around 0300 GMT plus-or-minus 30 minutes. There are no expectations for any kind of change in policy. Kuroda is happy to watch as other central banks tighten policy and depress the yen. He won't want to give any kind of indication that Japan is prepared to join in the global tightening.

The yen stance is reflected in things like AUD/JPY. On Wednesday, the pair broke above the July high to the best levels since December 2015 in what could be a significant break.

FOMC Leaves Rates Unchanged and Sticks to its Plans to Gradually Unwind Balance Sheet

As widely expected, the Federal Open Market Committee (FOMC) left the target range for the federal funds rate unchanged between 1 and 1-1/4 percent.

The Committee announced its plan to gradually reduce its balance sheet by tapering reinvestments in its Treasury and MBS portfolio. As previously telegraphed in its addendum to the June statement, the Fed will runoff at $10 billion per month initially ($6bn for UST/$4bn for MBS), raising it gradually to $50bn per month by October 2018, with the same 60/40 split between UST and MBS.

The statement made few changes to its assessment of the economy, noting the continued strength in job growth, and pick up in investment activity. The Committee recognized the negative impact of recent hurricanes on near-term economic activity with a boost expected thereafter as rebuilding begins. Moreover, it indicated that it anticipates a temporary effect on inflation as gasoline and other items rise in price due to shortages – particularly due to refinery outages in southeast Texas.

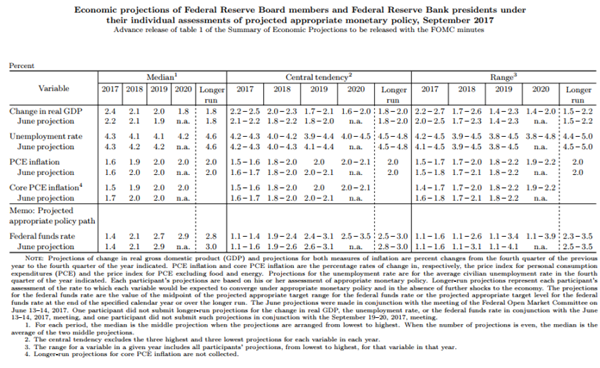

The Summary of Economic Projections (SEP) showed a slightly lower median unemployment rate in 2018 through 2019, with the rate hitting an expected trough of 4.1% (from 4.2% previously), before rising to 4.2% in 2020. The expected rate over the longer-term remained unchanged at 4.6%. The SEP also brought down the median estimate for core PCE inflation to 1.5% (from 1.7%) by the end of 2017 and to 1.9% (from 2.0%) by the end of 2018. Long-term rates were unchanged.

Importantly, the SEP interest rate projections for the near-term were largely unchanged, even as longer-term expectations edged lower. The median dot still suggests one more hike later this year and three additional hikes in 2018. However, the median estimate fell to 2.7% (from 2.9%) in 2019, and the longer-term median interest rate projection edged down a similar amount to 2.8% (from 3.0%) with the central tendency falling to 2.5% to 3.0% (from 2.8% to 3.0% previously).

Key Implications

As was widely expected, the Fed has finally embarked on a course of balance sheet normalization beginning next month. The balance sheet runoff will be very gradual, and markets have so far taken the reversal of the printing presses in stride. However, given the complicated nature of the financial linkages across the monetary system, we believe there is still some scope for increased volatility as global financial markets begin to feel the turning QE tide of the world's largest central bank.

With the details on balance sheet normalization sticking to the script laid out in June, we were focused on changes to participants projections. But, here too there was little to get excited about. Participants marked to market their expectations for inflation, but balanced this with a slightly lower unemployment rate through the next two years. That said, the movement down in long-term expectations for the federal funds rate appears fairly broad-based, with five dots at 2.5% or less (from just one at 2.5% in June), vindicating the recent financial market moves in longer-term yields.

The Committee indicated that while recent hurricanes are likely to impact inflation and economic activity in the near term, disrupting it first and then boosting it thereafter as rebuilding begins, the storms are "unlikely to materially alter the course of the national economy over the medium term." As such, we expect the Fed to see through any of the volatility in the data over the coming months in so far as it pertains to their outlook for the national economy, with the storms unlikely to prevent the Fed from potentially raising rates at their December meeting – particularly should inflation data firm by then as we expect.