Sample Category Title

Dollar Stays Weak on Prospect of Dovish Fed Later

The US dollar remained weak ahead of the Federal Reserve's announcement and the Fed Chair's press conference later in the session. Traders seemed to be bracing for an on balance dovish message from the Fed, even though the market still expected a rate hike at the end of the year to be more likely than not.

There was virtual unanimity that the Fed would not increase rates today but rather only announce the starting date for the gradual reduction of its huge 4.47 trillion dollar balance sheet. The Fed would probably start reducing its balance sheet by 10 billion dollars a month starting from October and very slowly increase the speed of the reduction next year. The big question that forex market participants will be waiting to be answered is with respect to the Fed board's forecasts for future rate increases (the "dot plot") and the assessment of economic conditions – together with fresh forecasts about growth, inflation and unemployment. There was a chance that the Fed would appear more dovish with respect to the prospects for tightening in 2018 and 2019 but would likely stay the course for a December hike. Such Fed meetings – complete with new economic forecasts and a press conference by the Fed Chair, take place only once a quarter – hence the market's heightened anticipation.

The dollar was struggling to hold on to its ground as euro/dollar kept making forays above 1.20 but was not able to secure a foothold above the psychologically important level. Euro/dollar was at 1.1992 at the time of writing. Dollar/yen was also around 50 pips away from the day's highs, trading at 111.39 while the pound was also strong at 1.3557 after briefly spiking above the 1.36 following positive economic news out of the UK.

British retail sales for August surprised the market by coming in much stronger than expected, while the previous month's figures were also revised higher. This contradicted evidence that wage growth was not keeping with inflation and creating problems for consumers, which raises some interesting questions as to what is really happening in the UK economy right now. Month-on-month the growth rate was 1% compared to expectations of 0.2% growth, while year-on-year the increase was at 2.4%. The latest data increased the odds that the Bank of England was going to hike interest rates at its next meeting on November 2. Euro/pound was pushed lower by the numbers to 0.8845 after spiking down to 0.8825 immediately after the release of the figures.

In the United States, the last economic data point before the Fed decision was existing home sales for August. They dropped 1.7% month-on-month compared to expectations of a small 0.3% increase. The annualized number of sales was 5.35 million units compared to 5.44 million the previous month. It was possible that the figures were distorted by Hurricane Harvey that hit Texas during August.

Finally in commodities, gold was holding above the $1310 an ounce level. The front-month US oil futures contract was holding onto $50 a barrel at 50.40 as higher than expected crude oil stocks were counterbalanced by a substantial draw in distillate stocks (-5.6 million barrels).

Fed Into Focus

Choppy USD trade ensues ahead of today's highly anticipated Fed announcement, Yellen conference and dot plot forecats. The antipodean currencies dominate trading, led by a soaring kiwi as NZ's ruling National party pushes wirg a 9-pt lead ahead of Saturday's elections. UK retail sales beat expectations and US existing home sales fell by more than expected. New trade actions and videos will be posted this afternoon ahead of the Fed's announcement.

Trump was at the UN and ramped up rhetoric against North Korea and Iran but there is little international consensus in favour of near-term action, especially on Iran where France immediately said it was against abandoning the nuclear deal. At the moment, the dollar is less-sensitive to geopolitical headlines than it was a month ago. That's in part due to higher liquidity but there is also a newfound sense that a rash move is unlikely.

Balance Sheet to Overshadow Dots

Expect the focus to center on the balance sheet reduction program, which is anticipated to begin next month. What will be the planned reduction amount in 2017? $30 bn, $40bn or more? And how would the amount be distributed in 2018 and thereafter? Ashraf tells me to get ready for a potentially "faster & earlier than expected" balance sheet reduction schedule, which could prop USD higher.

The FOMC decision may prove to be more hawkish than many believe. The dot plot will be downgraded to some degree but 12 of the 16 dots in June pointed to more hikes this year and it would be a tremendous shift to eliminate that.

Yellen will also want to keep her options open, especially if Republicans can find a way to deliver a tax cut. The market overall is net short the US dollar but Yellen and the Fed are optimistic about the economy. All it would take to restart the US dollar rally is a fresh hint at a December hike and a reiteration that policymakers are confident inflation will return to 2% in 2018.

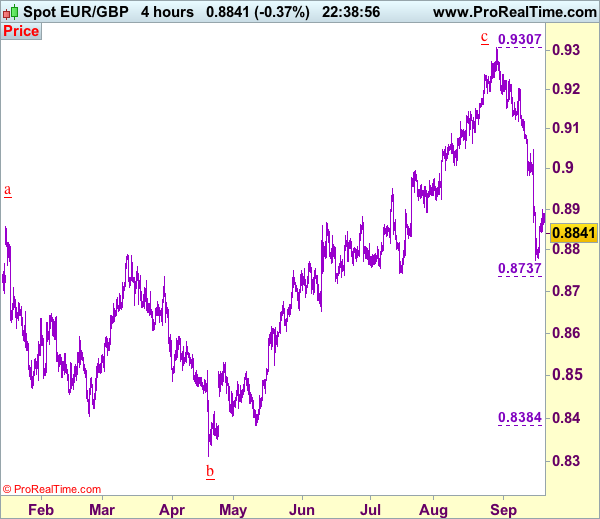

Trade Idea: EUR/GBP – Sell at 0.8975

EUR/GBP - 0.8835

Original strategy :

Sell at 0.8955, Target: 0.8800, Stop: 0.8995

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8975, Target: 0.8800, Stop: 0.9015

Position : -

Target : -

Stop : -

Euro’s rebound after last week’s selloff to 0.8774 has retained our view that further consolidation above this level would be seen and corrective bounce to 0.8907-10 is likely, however, reckon upside would be limited to 0.8950-55 and 0.8970-75 should hold, bring another decline later, below 0.8805-10 would bring retest of said support at 0.8774, break there would signal the reversal from 0.9307 top is still in progress and bearishness remains for this fall to extend weakness towards 0.8737-43 (61.8% Fibonacci retracement of 0.8384-0.9307 and previous support) but near term oversold condition should limit downside to 0.8719 support and reckon another previous chart support at 0.8652 would hold.

In view of this, would not chase this fall here and we are looking to sell euro on further recovery as 0.8970-75 should limit upside and bring another decline later. Above previous support at 0.8982 would abort and signal a temporary low has been formed, bring retracement of recent decline to 0.9000 but price should falter below resistance at 0.9048 and bring another selloff next week.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

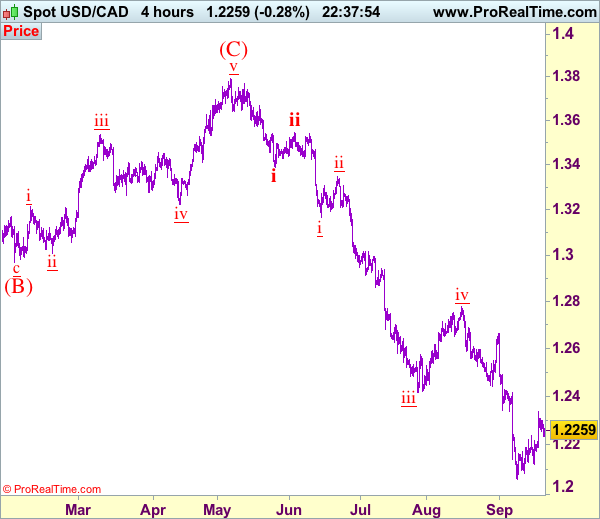

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.2259

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the greenback has retreated after rising to 1.2338 and consolidation below this level would be seen, reckon downside would be limited to 1.2200 and 1.2170-75 should hold, bring another rebound later, above 1.2300 would bring test of said resistance at 1.2338, break there would signal a temporary low has been formed at 1.2061 earlier, bring retracement of recent decline to 1.2390-00 but reckon resistance at 1.2425-30 would hold from here, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below 1.2200 would bring weakness to 1.2170-75 but break there is needed to suggest the rebound from 1.2061 low has ended, bring further all towards support at 1.2121, break there would confirm and bring retest of 1.2061 later, break there would signal recent decline has resumed and extend weakness towards psychological support at 1.2000. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Yellen to Help the Dollar?

- European equity indices lose some ground with Spain (-1%) a notable underperformer on increased tensions in Catalunya (see below). US stock markets open nearly unchanged with investors waiting for the outcome of tonight's FOMC meeting.

- UK retail sales rose in August at their fastest pace in four months (1% M/M), providing further evidence of a tentative pickup in consumer spending. The July figure was upwardly revised from 0.5% M/M to 0.7%M/M. EUR/GBP temporary dropped from 0.888 to 0.883, but sterling couldn't hold on to gains.

- Spain's paramilitary national police have raided the headquarters of the Catalan government in Barcelona in the latest offensive against the proposed referendum on independence, set to be held in less than two weeks' time. They arrested 13 people for their alleged involvement in planning the secession vote.

- NZD/USD jumped towards 0.74 following the release of a new poll showing the governing National Party could rule alone after the country's general election on September 23.

- Greek banks are set to float revised plans to reduce their non-performing loans to their boards early next month, bank sources said, in news that drove down shares in the country's lenders.

Rates

Core bonds modestly higher ahead of FOMC decision

Core bonds fared reasonably well today amid low volumes though as the hyped FOMC meeting is drawing to an end (decision at 20:00 CET). The gains remained modest though (see lower) and were technically irrelevant. ECB Knot, a hawk, said that a recalibration of the policy was overdue as the main rational for ECB asset purchases has vanished. He is confident inflation will return to target. However, his comments had no traction in the bond market, as the Bund safeguarded its morning gains. We didn't see a strong trigger for the Bund morning gains. UK retail sales were much stronger than expected, but Gilts only made a knee jerk reaction. The modest gains might have been technically inspired, coming after last week's sharp declines. Some traders are looking for a technical bottom formation.

The German Finanzagentur launched a new 30-yr Bund (€2B 1.25% Aug2048). Total bids amounted to €2.93B, remarkably stronger than the €1.5B average at the previous 4 long term Bund auctions, and resulting in an official bid cover of 1.8. The auction tailed 1 cent and the Bundesbank set aside €0.37B for secondary market operations (real bid cover 1.5).

At the time of writing, US yields declined by 1.1 bp (2-yr) to 1.3 bps (5-yr). German yields dropped more, notably between 0.3 bps (2-yr) and 2.8 bps (30-yr).

On intra-EMU bond markets, 10-yr yield spread changes versus Germany widened modestly. Spain and Italy underperformed with 10-yr yield spreads up 3 bps. In the case of Spain that's a surprisingly good performance as nervousness on the Catalan referendum increases. The National police raided the headquarters of the Catalan government and detained senior Catalan officials. Ballot boxes were seized too in an attempt to prevent the referendum from taking place. Spanish bond holders were not overly concerned.

Currencies

Yellen to help the dollar?

USD investors basically stayed side-lined today, awaiting the Fed's policy assessment. Trading in EUR/USD and USD/JPY was confined to tight ranges. If anything, the dollar traded with a cautious bias.

Overnight, Asian equities were narrowly mixed even as WS closed again at record levels. Japan August trade data were strong, but don't change to broader picture for the BOJ's policy. The BOJ is largely expected to keep course tomorrow, lagging the normalisation in other major economies. The yen continued to trade weak. The overall picture for the dollar was unchanged. USD/JPY holds in the mid 111 area, within reach of the ST correction top. At the same time, the dollar struggled against the euro. EUR/USD tried to regain the 1.20 barrier.

There were only second tier eco data in Europe. Equities showed no clear trend. Core bonds traded with a mild positive bias as traders counted down to tonight's Fed decision. The slight decline in core German & US yields was more negative for the dollar than for the euro, but the moves were very limited. USD/JPY drifted back lower in the 111 big figure. EUR/USD mostly traded just north of 1.20.

More wait-and-see action during the US session. Dollar sentiment was slightly more constructive as core yields reversed this mornings' modest setback. EUR/USD trades at around 1.20. USD/JPY is changing hands in the 111.40 area. Negative headlines on Catalonia until now hardly impact the euro.

The FOMC will most likely leave its policy rate unchanged, but announce the start of a gradual unwinding of its balance sheet. Markets will keep a close eye at the 'dots' indicating the rate hike expectations of the individual Fed members. We expect the median dots for 2017 and 2018 to remain unchanged suggesting respectively one additional rate hike for 2017 and 3 hikes in 2018. This scenario shouldn't be too bad for the dollar, if markets give some more credence to the Fed compared to what they did of late…

Sterling hardly profits from strong retail sales

UK August retail sales were stronger than expected at 1.0% M/M and 2.4% Y/Y. The July figure was also upward revised. The BoE recently indicated that it could raise rates over the coming months if the economy continues to perform as expected. Today's retail sales evidently leave this option perfectly open. EUR/GBP declined about half a big figure upon the publication of the report. Even so, the gain was modest and evaporated quite soon. Overall euro strength maybe played a minor role. However, the price move might be another indication that the easiest part of the GBP comeback might be behind us. The headlines from EU policy makers on Brexit were less constructive, too. EUR/GBP trades currently around 0.8860. Cable also couldn't maintain the intraday gains and trades in the 1.3540 area.

Gold Steady Ahead of FOMC Rate Statement

Gold has ticked upwards in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1311.87, up 0.14%. In economic news, the US releases Existing Home Sales, which is expected to improve to 5.46 million. All eyes are on the Federal Reserve, which will release a rate statement at the conclusion of its policy meeting.

What can we expect from Janet Yellen on Wednesday? The FOMC is expected to hold the benchmark rate at 1.25%, so analysts will be looking for details about the the Fed balance sheet and a possible rate hike in December. Earlier in the year, the Fed outlined plans to begin reducing its bloated balance sheet of $4.2 trillion, and the markets are expecting more details, such as a start date for the tapering. The Fed is expected to reduce the balance sheet by not replacing some maturing bonds, starting at $10 billion/month, and gradually moving higher. This move can be viewed as a mini-rate hike, and could provide a boost for the US dollar against major rivals. However, if the Fed does not address its balance sheet, the markets could get nervous and the US dollar could lose ground. As for inflation, persistently low levels remains well below the Fed target of 2% and this has hampered plans for a third rate hike in 2017. Janet Yellen has not discussed a December move, but in recent weeks, some FOMC members have come out against another rate hike before inflation moves higher, even if this means waiting until 2018. If the rate statement addresses the timing of another rate hike, we could see substantial movement from the US dollar.

Gold prices are linked to interest rate moves, as the metal tends to move lower when interest rates increase. Keeping this rule of thumb in mind, traders should keep an eye on recent developments at the Bank of England. The pound jumped 3.0% last week, after the minutes of the BoE's policy meeting strongly hinted at a rate hike before the end of the year. BoE Governor Mark Carney reiterated this stance at a speech to the International Monetary Fund on Monday, saying that monetary policy "would have to move". The BoE will hold its next policy meeting on November 2, and further hints about a rate hike over the next few weeks could weigh on gold prices.

Spot Gold Extended Recovery Rally

Spot Gold extended recovery rally from temporary footstep at $1304 for the second day, but gains were limited at $1316 and so far unable to sustain probe above initial barrier at $1312 (daily Kijun-sen).

Pivotal barrier at $1320 (broken bull-trendline / 20SMA) stay intact for now and keep near-term risk shifted lower. Gold is eyeing the outcome of FOMC policy meeting as the yellow metal, sensitive on US interest rate changes, would react on both scenarios.

Hawkish Fed is expected to send gold price lower, as break below next target at $1299 (Fibo 38.2% of $1204/$1357 rally) could extend towards $1280 (rising 55SMA).

If US policymakers fail to deliver firmer signals of possible rate cut by the end of the year and provide more details on timing of the beginning of reduction of massive portfolio, gold would rally.

Break above $1320 would expose next pivots at $1331 (daily Tenkan-sen) and $1334 (last week's tops which formed a lower platform).

Res: 1312; 1320; 1325; 1331

Sup: 1309; 1304; 1299; 1292

Dollar Depressed ahead of FOMC Decision

The Dollar has drifted lower against a basket of major currencies, ahead of the Federal Reserve decision later today, which is largely expected to conclude with an unchanged monetary policy.

With it being considered a previous conclusion that US interest rates will be left unchanged in September, much attention will likely be directed towards the Fed's forward guidance, for clues on future monetary policy. While the central bank is also expected to announce the unwinding of its mammoth balance sheet today, the real action will be in the Fed's economic projections and Yellen's Press Conference. With concerns over low inflation in the U.S raising questions over when the next rate hike will come, it will be interesting to hear Yellen's thoughts on this topic. This could be a very lively session for the Dollar, especially when considering how the FOMC will be updating its economic projections and providing its forecast for growth, inflation and interest rates.

Dollar bulls could be offered a rare opportunity to bounce back, if Yellen adopts a hawkish tone during her press conference. A situation where the Fed is cautious and expresses concern over low inflation, is likely to weigh on rate hike expectations, consequently punishing the Dollar.

The Dollar Index remains bearish on the daily charts, with sustained weakness below 91.50, encouraging a further decline towards 91.00.

Commodity spotlight – WTI

WTI Crude found comfort above $50 on Wednesday, after Iraq's Oil Minister said OPEC and other oil producers were considering extending or even deepening supply cuts, to rebalance the markets.

As the OPEC meeting looms, an extension of the current production deal beyond March is a possibility, especially when considering how OPEC's crude oil production fell last month, for the first time since April. With oil prices steadily appreciating, as investors become increasingly optimistic over OPEC's effort to stabilize the saturated markets, the cartel should be encouraged to extend the current deal, which may fuel the upside.

Nigeria and Libya are likely to be in the spotlight during Friday's OPEC meeting, with discussions centered on the progress of their deal to limit output. With both countries currently exempt from the OPEC led deal to cut production, it will be interesting to see if the two nations agree to limit their output and how this will impact oil prices.

Technical traders will continue to observe how WTI Crude behaves above $50. A solid daily close above this level should encourage a further appreciation towards $51.50.

EUR/USD Stays Higher

The currency pair has resumed the minor rebound and has touched a near-term dynamic resistance. Technically is expected to drop on the short term, but unfortunately, the fundamental factors will take the lead later. Price has changed little till now, but a high volatility is expected during the FOMC, you should stay away from trading tonight because you can ruin your account.

EUR/USD is trading right below a long-term major resistance level (1.2041), has made two false breakouts above this major obstacle, but a disappointment tonight will help the buyers to lead the rate much above it.

The European currency has received support from the German PPI, which has increased by 0.2% in August, beating the 0.1% estimate. The US is to release the Existing Home Sales later, the indicator is expected to increase from 5.44M to 5.46M in the previous month.

The Federal Reserve is expected to maintain the Federal Funds Rate unchanged at 1.25%, but the FOMC could shake the markets with its announcements regarding the monetary policy.

Price finally retested the upper median line (uml) of the minor descending pitchfork, the rebound was expected after failure to retest the median line (ml). It was almost to retest the upper median line (UML) of the ascending pitchfork, could still reach this line in the upcoming hours. Technically is expected to drop after the retest of the mentioned levels, but the fundamental factors could drive it towards new peaks.

EUR/CHF Another Leg Lower?

EUR/CHF dropped today and failed to reach the next major upside target from the fifth warning line (WL5). Now is pressuring the broken warning line (wl1) of the minor ascending pitchfork, a failure to stay above this line and above the 1.1536 level will send the rate towards the upper median line (uml) again.