Sample Category Title

Australia’s Home Loan Approvals Advanced Above Expectations In July

For the 24 hours to 23:00 GMT, the AUD rose 0.5% against the USD and closed at 0.8047.

LME Copper prices declined 0.3% or $21.5/MT to $6842.5/MT. Aluminium prices rose 0.3% or $5.5/MT to $2075.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.8095, with the AUD trading 0.6% higher against the USD from yesterday's close.

Early morning data showed that Australia's seasonally adjusted home loan approvals climbed 2.9% on a monthly basis in July, more than market expectations for a rise of 1.0%. In the previous month, home loan approvals had recorded a revised gain of 1.2%.

Elsewhere in China, Australia's largest trading partner, trade balance surprisingly narrowed to CNY286.5 billion in August, compared to market consensus for the nation's trade surplus to widen to CNY335.7 billion. In the previous month, the nation had recorded a trade surplus of CNY321.2 billion. Meanwhile, the nation's exports rose less-than-expected by 6.9% YoY in August, after recording a rise of 11.2% in the prior month. Meanwhile, the nation's imports grew more-than-anticipated by 14.4% in August, compared to an advance of 14.7% in the preceding month.

The pair is expected to find support at 0.8014, and a fall through could take it to the next support level of 0.7932. The pair is expected to find its first resistance at 0.8138, and a rise through could take it to the next resistance level of 0.8180.

Going forward, all eyes will be on a speech by the Reserve Bank of Australia's (RBA) Governor, Philip Lowe, scheduled in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

ECB Retained Its Benchmark Interest Rate At Record Low

For the 24 hours to 23:00 GMT, the EUR rose 0.81% against the USD and closed at 1.2022, after the European Central Bank (ECB) President, Mario Draghi, hinted that the long-awaited decision about scaling back the ECB’s quantitative easing programme would likely come in next month.

The ECB, at its latest monetary policy meeting, opted to leave the key interest rate unchanged at a record low level of 0.00% and pledged to continue its bond-buying programme through December 2017 and possibly beyond if needed. In a post-meeting statement, the ECB President stated that the governing council had held early talks on how long to maintain its extraordinary stimulus efforts and added that the central bank will make the “bulk” of its decisions in October.

Gains in the Euro were boosted further, after the ECB upgraded the Euro-bloc’s growth outlook, now expecting the common currency region to grow 2.2% in 2017, up from a previous forecast of 1.9%, given the region’s improving fundamentals. However, the central bank lowered its forecasts for inflation to 1.2% next year from 1.3% previously and to 1.5% in 2019 from 1.6%.

On the macro front, the Euro-zone’s seasonally adjusted final gross domestic product (GDP) rose 0.6% on a quarterly basis in the second quarter of 2017, in line with the preliminary figures. In the previous quarter, GDP had advanced by a revised 0.5%.

Separately, Germany’s seasonally adjusted industrial production surprisingly remained flat on a monthly basis in July, compared to market consensus for a rise of 0.5%. In the previous month, industrial production had dropped 1.1%.

The greenback lost ground against its major counterparts, after data indicated that the number of Americans filing for fresh jobless claims jumped to a level of 298.0K in the week ended 02 September, hitting its highest level in more than two years. Meanwhile, market participants had expected initial jobless claims to advance to a level of 245.0K, after recording a level of 236.0K in the prior week. On the other hand, the nation’s IBD/TIPP economic optimism index advanced more-than-anticipated to a level of 53.4 in September, compared to a reading of 52.2 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.2075, with the EUR trading 0.44% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1963, and a fall through could take it to the next support level of 1.1851. The pair is expected to find its first resistance at 1.2138, and a rise through could take it to the next resistance level of 1.2201.

Moving ahead, investors will focus on Germany’s trade balance figures for July, slated to release in a few hours. Moreover, the US final wholesale inventories and consumer credit change, both for July, will be on investors’ radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK’s Halifax House Prices Grew At Its Quickest Pace This Year In August

For the 24 hours to 23:00 GMT, the GBP rose 0.37% against the USD and closed at 1.3096, after UK's Halifax house price index climbed more-than-expected by 1.1% on a monthly basis in August, surging at its fastest pace in eight months, suggesting that upswing in the nation's property market may be on the horizon. In the previous month, the index had advanced by a revised 0.7%, while markets were anticipating for a gain of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.3128, with the GBP trading 0.24% higher against the USD from yesterday's close.

The pair is expected to find support at 1.3061, and a fall through could take it to the next support level of 1.2994. The pair is expected to find its first resistance at 1.3167, and a rise through could take it to the next resistance level of 1.3206.

Trading trends in the Pound is expected to be determined by the release of Britain's industrial as well as manufacturing production data along with total trade balance figures, all for July, slated to release in a few hours. Also, later in the day, traders would eye the NIESR GDP estimate numbers for the three months ended August.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Economic Growth Sharply Revised Lower In 2Q 2017

For the 24 hours to 23:00 GMT, the USD declined 0.76% against the JPY and closed at 108.37.

In the Asian session, at GMT0300, the pair is trading at 108.17, with the USD trading 0.18% lower against the JPY from yesterday's close.

Overnight data indicated that Japan's final gross domestic product (GDP) grew less than initially estimated by 0.6% on a quarterly basis in the second quarter of 2017, while the preliminary print had indicated an advance of 1.0%. The nation's GDP had risen by a revised 0.4% in the previous quarter.

Meanwhile, the nation's (BOP basis) trade surplus unexpectedly widened to ¥566.6 billion in July, up from a surplus of ¥518.5 billion in the previous month, while investors had envisaged the nation to register a surplus of ¥518.0 billion.

The pair is expected to find support at 107.77, and a fall through could take it to the next support level of 107.37. The pair is expected to find its first resistance at 108.85, and a rise through could take it to the next resistance level of 109.53.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Higher, Ahead Of Swiss Unemployment Rate Data

For the 24 hours to 23:00 GMT, the USD declined 0.61% against the CHF and closed at 0.9502.

In the Asian session, at GMT0300, the pair is trading at 0.9450, with the USD trading 0.55% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9403, and a fall through could take it to the next support level of 0.9355. The pair is expected to find its first resistance at 0.9534, and a rise through could take it to the next resistance level of 0.9617.

Going ahead, investors will look forward to Switzerland’s unemployment rate data for August, slated to release in a while.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canadian Building Permits Declined For The First Since March 2017 In July

For the 24 hours to 23:00 GMT, the USD declined 1.00% against the CAD and closed at 1.2114.

In economic news, Canada’s building permits registered a drop of 3.5% on a monthly basis in July, more than market expectations for a fall of 1.5% and dipping for the first time in four months. Building permits had recorded a revised rise of 4.4% in the previous month. Moreover, the nation’s seasonally adjusted Ivey PMI eased to a level of 56.3 in August, compared to a level of 60.0 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2071, with the USD trading 0.35% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2012, and a fall through could take it to the next support level of 1.1953. The pair is expected to find its first resistance at 1.2183, and a rise through could take it to the next resistance level of 1.2295.

Ahead in the day, traders would draw their attention to Canada’s unemployment rate for August.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

ECB Review: Warming Up To QE Extension In October

Key points

- Draghi confirmed the bulk of QE decisions is likely in October – the 33% limits will not be lifted, hence capital key deviations continue

- The inflation outlook was revised lower reflecting the stronger euro – a substantial degree of monetary accommodation is still needed

- The underlying euro momentum remains strong and any dips in EUR/USD should be shallow and short-lived

- Focus on the euro and the smaller concern about an abrupt end to QE resulted in a strong performance for the periphery bond markets

The ECB left its policy measures unchanged and President Mario Draghi confirmed that the bulk of decisions regarding the QE purchases beyond 2017 will most likely be taken in October. There was a lot of focus on the exchange rate development and during the introductory statement Draghi mentioned the euro appreciation three times, saying that ‘the recent volatility in the exchange rate represents a source of uncertainty that requires monitoring'. Notably, the FX market did not perceive Draghi as dovish enough to counteract the strong underlying momentum and EUR/USD ended higher. In fixed income markets, the periphery was the big winner, reflecting it is now deemed more likely that the QE programme will continue in 2018.

The discussion about how to continue the QE programme beyond 2017 has started and Draghi gave some insights. First of all, the sequencing in the exit strategy was not discussed, hence it was confirmed that policy rates will remain at their present levels after the QE programme has ended. Secondly, the ECB did not consider lifting the 33% issue/issuer limits. Related to this, the ECB did not discuss scarcity issues but Draghi argued that the ECB has repeatedly shown its ability to deal with this. Instead, focus was on the length and size of the programme including pros and cons of different scenarios for the future purchases. In addition, Draghi opened up for higher purchases in France, Italy and Spain and lower ones in Germany and the Netherlands where the holdings are approaching the 33% limit, as he said there has always been and will always be deviation from the capital key distribution.

We still believe the ECB will announce a reduction in its QE purchases to EUR40bn per month in H1 18 at the next meeting in October. The programme should be continued without lifting the 33% limits, but instead be based on continued capital key deviations. We also consider it likely that the ECB will buy a higher share of corporate bonds. These purchases will have a more direct economic impact and the ECB's holdings are not close to the 70% ISIN limit.

Downward revision to the inflation forecast due to stronger euro

The Governing Council discussed three topics at today's meeting and Draghi's conclusion was the following.

1. The strong growth momentum boosts confidence that inflation will pick up eventually. Related to this, the ECB lifted its GDP growth forecast for 2017 to 2.2% from 1.9% reflecting the recent strong data. The projections for 2018 and 2019 were kept unchanged at 1.8% and 1.7%, respectively. The ECB added that there are downside risks to the growth outlook related to developments in foreign exchange markets.

2. The inflation outlook was revised down a bit, mainly reflecting the euro appreciation. It was still judged that a substantial degree of monetary accommodation was needed for underlying prices to pick up. The ECB kept its 2017 inflation forecast unchanged at 1.5% but lowered the 2018 and 2019 forecast by 0.1pp to 1.2% and 1.5%, respectively. Interestingly, the ECB lowered its core inflation forecast for 2019 by 0.2pp to 1.5%.

3. The exchange rate was once again described as not being a policy target, but Draghi said it is very important for growth and inflation and to such an extent that the medium-term outlook for inflation was revised down. Due to this and according to Draghi, the ECB must take exchange rate developments into account in its decisions as also reflected in the comment in the introductory statement about the exchange rate's possible implications for the medium-term outlook for price stability.

FX: underlying EUR momentum remains strong

The FX market bought the pair on ECB's more positive assessment of economic growth this year and the signals that an announcement on monetary policy awaits in October. However, at the press conference Draghi made an effort to cap a further rise in EUR/USD by stressing the negative impact on the medium-term outlook for inflation from the stronger euro. Hence, while the price action today underscores our view that underlying euro momentum remains strong, the market will keep in mind that the ECB is unlikely to tolerate a further strong euro appreciation in the short term, which should put a soft cap on the pair ahead of the October meeting. We maintain our view that any dip should be shallow and short-lived.

Fixed income: support to the carry-friendly environment

The fixed income market and particularly the periphery reacted positively to the message from Draghi that a decision will be taken at the October meeting and not least that the euro is being monitored closely. The more the euro appreciates the more likely it becomes that the ECB will extend its QE programme and postpone rate hikes. Hence, the key variable for the fixed income market at the moment is the euro. We have seen 10Y German yields a few basis points lower and the curve steepened slightly as 2Y bond yields fell a bit less after the press briefing. The focus on the euro and the smaller concern about an abrupt end to QE pushed investors towards periphery bond markets that performed strongly after the press briefing. 10Y Spanish and Italian yields outperformed Germany by some 4bp this afternoon. We agree with the positive reaction in periphery and core FI markets. In our view Draghi today supported the carry-friendly environment we have seen over the summer. We are long 5Y Spain and 5Y Italy versus swaps in our Government Bond Weekly trading portfolio and we are very comfortable with these trades in light of the message from Draghi today

Market Morning Briefing: ECB Kept Rates Unchanged Yesterday

STOCKS

Dow (21784.78, -0.10%) closed just above support levels on the 3-day candle chart. A rise from here is necessary to keep the immediate uptrend intact; else a fall towards 21600 or lower is possible in the next couple of weeks.

Dax (12296.63, +0.67%) has moved up sharply to close at higher levels after the ECB meeting yesterday. A rise in the coming sessions is possible towards 12400-12500.

Nikkei (19337.04, -0.31%) looks weak. While the Dollar Yen is headed to lower levels, Nikkei could remain weak too and target levels near 19200-19200 in the near term.

Shanghai (3368.90, +0.10%) looks bullish while above 3350. It could possibly consolidate sideways for some more sessions before resuming the uptrend.

Nifty (9929.90, +0.14%) is expected to remain bullish while above 9750 as we have been mentioning for quite some time now. The index could possibly spend some time within 9750-10000 levels before deciding on further direction. The index is likely to remain stable today.

COMMODITIES

Gold (1356) moved higher and met our target of 1350 as Dollar index in trading below 91.50 levels. Immediate trading range for Gold is now 1335-1371 with an interim support at 1345. Gold is highly overbought thus we might see weekend profit booking at current levels . Similarly Silver (18.23) has also moved higher but still within the range of 16.90-18.25. Please maintain caution at higher levels due to overbought nature. In the medium term,both Gold and Silver are out of their short term bearish channel but the supports of 1288 and 16.80-90 should hold to keep the bullish momentum intact.

Copper (3.15) is trading within the narrow range of 3.12-3.17. Only above 3.17 , higher levels of 3.26 can come into consideration. The only concern in the short term overbought condition which might cause short term profit booking at current levels.

Brent (54.60) is trading within the bullish channel of 50-55.60 since June 17 and we will remain bullish while it is trading above 50 regions on a weekly closing basis. WTI (49.22) has also moved higher but still within the bearish channel of 45-50 since march 17. Technically there are no sign of weakness so for but we need to be little cautious as a price correction for a 4.6MB surplus in U.S. weekly crude inventory is overdue.

FOREX

ECB kept rates unchanged yesterday. The next meeting in October would be important as it is now a 'confirmed date' when the ECB will seriously debate when to start its 'taper' from. Euro (1.2055) shot up to 1.20 soon after the ECB yesterday and is trading above 1.20. While the longer term target of 1.2150-1.2250 remains on the cards for the medium term, we could expect Euro to end the week on a stronger note. The ECB has raised its GDP growth forecasts but slightly powered its inflation forecast.

Dollar Index (91.347) has come down below our initial target of 92. Important support is visible near 90.70-91.00 region and while that holds a bounce back towards 92-93 is possible in the next couple of weeks. For now a test of 90.70 is possible on the downside.

Dollar-Yen (108.125) is trading near crucial support zone of 108.00-108.13, responding to the Euro strength and while that holds, we could see a bounce back from current levels (last seen in April). In case we see a weekly close at levels below 108, the direction could tilt on the downside for the near term.

Euro-Yen (130.53) is holding above immediate support levels just above 129 and seems to be potentially bullish for the coming sessions. There is a fair scope of a rise towards 131-132 in the near term.

The Pound (1.3128) has been rising strongly since the last 2-weeks and could target 1.3270, the high seen on 3rd August’17. Near term looks bullish.

Sharp rise in Aussie (0.8098) is seen this week. A rise towards 0.82 is possible while support at 0.7950 holds.

Dollar-Rupee (64.04) is expected to trade within 64.15-63.95 today. The strength in Euro may lead to some Rupee strength today.

INTEREST RATES

The benchmark US 10Yr yield (2.04%) has dipped again. It could possibly touch 1.97 regions but that will be a highly oversold territory , thus we are not expecting further downside beyond 1.97 regions.

EUR/USD moved higher as the The German-US 2 Yr Spread (-2.05%) and the German-US 10Yr Spread (1.76%) has been rebound. Otherwise there were no such stimulus for Eur in the yesterday's ECB meet.

Japan 10Yr yield (0.02%) moved higher while the 30Yr (0.82%) and the 5Yr (-0.14%) are almost stable at the time of this writing. No directional clarity so far but definitively yields are consolidating at these levels.

The UK 5Yr and 30Yr Gilt Yields (5Yr 0.43% and 20Yr 1.57%) had moved lower towards their respective supports. The UK 10Yr (1.03%) looks stable, might retest its immediate resistance of 1.07-08% region.

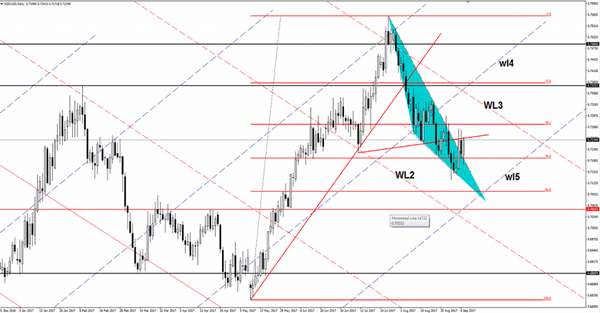

NZD/USD Falling Wedge Validated

NZD/USD rallied after the retest of the upside line of the Falling Wedge pattern and now reached the up sloping red line. Has dropped below the 50% retracement level, but the sellers weren't able to keep it there.

I've said in the previous reports that a minor consolidation here will send it towards the third warning line (WL3).

USD/JPY Edging Lower

USD/JPY moves in range on the Daily chart, but a breakdown seems imminent. Price is trading in the red and dropped below the 108.12 major static support, a valid breakdown is somehow expected. Technically, it could drop further after the retest of the warning line (wl1), but until the rate closes below the 108.12 level, nothing is certain.