Sample Category Title

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 7 September 2017

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases. Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the current monthly pace of €60 billion, are intended to run until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The net purchases are made alongside reinvestments of the principal payments from maturing securities purchased under the asset purchase programme.

The incoming information, including our new staff projections, confirms a broadly unchanged medium-term outlook for euro area economic growth and inflation. The economic expansion, which accelerated more than expected in the first half of 2017, continues to be solid and broad-based across countries and sectors. At the same time, the recent volatility in the exchange rate represents a source of uncertainty which requires monitoring with regard to its possible implications for the medium-term outlook for price stability.

While the ongoing economic expansion provides confidence that inflation will gradually head to levels in line with our inflation aim, it has yet to translate sufficiently into stronger inflation dynamics. Measures of underlying inflation have ticked up slightly in recent months but, overall, remain at subdued levels. Therefore, a very substantial degree of monetary accommodation is still needed for underlying inflation pressures to gradually build up and support headline inflation developments in the medium term. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase our asset purchase programme in terms of size and/or duration. This autumn we will decide on the calibration of our policy instruments beyond the end of the year, taking into account the expected path of inflation and the financial conditions needed for a sustained return of inflation rates towards levels that are below, but close to, 2%.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.6%, quarter on quarter, in the second quarter of 2017, after 0.5% in the first quarter. Survey data point to continued broad-based growth in the period ahead. Our monetary policy measures are supporting domestic demand and have facilitated the deleveraging process. Private consumption is underpinned by employment gains, which are also benefiting from past labour market reforms, and by increasing household wealth. The recovery in investment continues to benefit from very favourable financing conditions and improvements in corporate profitability. Moreover, the broad-based global recovery will support euro area exports.

This assessment is broadly reflected in the September 2017 ECB staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.2% in 2017, by 1.8% in 2018 and by 1.7% in 2019. Compared with the June 2017 Eurosystem staff macroeconomic projections, the outlook for real GDP growth has been revised up for 2017, reflecting the recent stronger growth momentum, and is broadly unchanged thereafter.

Risks surrounding the euro area growth outlook remain broadly balanced. On the one hand, the current positive cyclical momentum increases the chances of a stronger than expected economic upswing. On the other hand, downside risks continue to exist, primarily relating to global factors and developments in foreign exchange markets.

Euro area annual HICP inflation was 1.5% in August. Looking ahead, on the basis of current futures prices for oil, annual rates of headline inflation are likely to temporarily decline towards the turn of the year, mainly reflecting base effects in energy prices. At the same time, measures of underlying inflation have ticked up moderately in recent months, but have yet to show convincing signs of a sustained upward trend. Domestic cost pressures, notably from labour markets, are still subdued. Underlying inflation in the euro area is expected to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding gradual absorption of economic slack and rising wages.

This assessment is also broadly reflected in the September 2017 ECB staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.5% in 2017, 1.2% in 2018 and 1.5% in 2019. Compared with the June 2017 Eurosystem staff macroeconomic projections, the outlook for headline HICP inflation has been revised down slightly, mainly reflecting the recent appreciation of the euro exchange rate.

Turning to the monetary analysis, broad money (M3), despite some monthly volatility, continues to expand at a robust pace, with an annual rate of growth of 4.5% in July 2017, after 5.0% in June. As in previous months, annual growth in M3 was mainly supported by its most liquid components, with the narrow monetary aggregate M1 expanding at an annual rate of 9.1% in July 2017, down from 9.7% in June.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations increased to 2.4% in July 2017, up from 2.0% in June, while the annual growth rate of loans to households remained stable at 2.6%. The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for a continued very substantial degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2%.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to strengthening the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area growth potential and productivity. Regarding fiscal policies, all countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalances procedure over time and across countries remains essential to bolster the resilience of the euro area economy. Strengthening Economic and Monetary Union remains a priority. The Governing Council welcomes the ongoing discussions on further enhancing the institutional architecture of our Economic and Monetary Union.

We are now at your disposal for questions.

>

(ECB) Monetary Policy Decisions

At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the net asset purchases, at the current monthly pace of €60 billion, are intended to run until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The net purchases are made alongside reinvestments of the principal payments from maturing securities purchased under the asset purchase programme. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the programme in terms of size and/or duration.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

CAC Gains Ground Despite Dovish ECB Statement

The CAC index has posted considerable gains in the Thursday session, continuing the upward movement which we saw on Wednesday. Currently, the index is at 5,136.50, up 0.69% on the day. On the release front, France's trade deficit widened to EUR 6.0 billion, much higher than the estimate of EUR 4.5 billion. Eurozone Revised GDP rose 0.6% in the second quarter, matching the estimate. The ECB held interest rates at 0.00%, and the rate statement indicated that the ECB would maintain its asset purchases program. On Friday, France releases the Government Budget Balance and Industrial Production.

The ECB rate statement was more dovish than expected, surprising many analysts. The ECB said that it was maintaining its quantitative easing program to December, adding that it could increase purchases if necessary. The statement said that if the economic outlook became "less favourable", the bank was prepared to increase QE in terms of size or duration. Given that the eurozone economy has rebounded in 2017, there were expectations that the ECB would take a more hawkish stance, and hint at a tapering of QE in early 2018. The ECB has yet to decide what to do next, and analysts do not expect the details of the new program to be announced until October or possibly December. ECB policymakers must weigh competing interests – Germany would like nothing more than the ECB to simply exit the program, which was brought in as an emergency measure to begin with. However, France and other eurozone members, which are not enjoying German-style growth, favor a gradual tapering of the program, perhaps lowering monthly asset purchases from EUR 60 billion to EUR 45 billion. The markets will be monitoring ECB President Mario Draghi's follow-up press conference, looking for some details about its plans for the QE program.

Britain's departure from the European Union promises to have a significant impact on the Eurozone financial sector, and stock markets will also be affected. One issue under discussion relates to clearing houses based in Britain, specifically over euro-denominated trades. The European Commission is working on a draft law that would see joint supervision between the EU and Britain over such transactions, but France wants the European Securities and Markets Authority (ESMA) to have greater authority, such as a veto, over these transactions. This is one more example of the immense difficulty in untangling the British financial sector from the continent, and there will likely be intense wrangling between the two sides at the Brexit negotiations, as Britain tries to minimize the damage to London, which is set to lose its status as the premier financial hub in Europe.

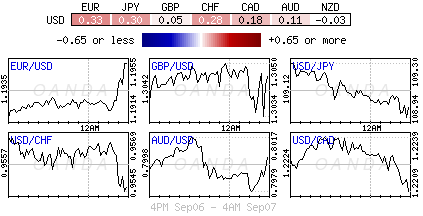

GBP/USD Strongly Bullish

GBP/USD edges higher on the Daily chart and is expected to reach new upside targets very soon. Price increases as the USDX drop aggressively again and approach the 91.64 previous low. The index will drop towards fresh new lows if will close below the mentioned static support.

USDX is trading in the red ahead of the ECB and ahead of the high impact US data. The greenback needs a strong support from the United States economy to be able to climb higher and to recover after the immense drop.

The ECB Press Conference will have an impact on the USD as well, a dovish speech will boost the USD and will punish the Euro. We'll have to be patient to see what impact will have the US figures, the Unemployment Claims could increase from 236K to 245K in the previous week, the Revised Nonfarm Productivity may increase by 1.3% in the second quarter, beating the 0.9% estimate, while the Revised unit Labor Costs indicator is expected to increase by 0.3%.

Price goes higher as expected, the perspective is bullish and should hit new highs in the upcoming days. The next upside target will be at the first warning line (wl1) of the minor ascending pitchfork, where he may find temporary resistance again. We have a breakout underway, has managed to pass beyond the 1.3046 level, signaling that the buyers are very strong.

USD/CHF On A Declining Path

USD/CHF extends the bearish movement as the dollar index drops further. Price is going down after the retest of the warning line (up sloping red line) and the 0.9634 level. Now is approaching the 0.9498 static support, a valid breakdown will confirm a drop towards the lower median line (lml) of the descending pitchfork and towards the 0.9440 horizontal downside obstacle. Only a rebound will send it towards the median line (ml) again.

EUR/CHF Another Breakout Attempt

EUR/CHF resumed the yesterday's bullish candle and climbed above the WL2 and the WL4, but failed to stay there. Price had lost altitude in the last hours, so a false breakout will signal an overbought and a potential drop at least till will reach the upper median line (uml).

I've said in another article that the rate could resume the upside movement if will jump and will stabilize above the 1.1415 level.

US: Debt Limit Fight Postponed amid Increased Fed Uncertainty

- Yesterday was a very eventful day, as Donald Trump struck a deal with the Democrats on Harvey aid, government funding until December and a suspension of the debt limit until mid-December.

- In our view, this is just kicking the can down the road, as we now risk a government shutdown in December and/or a government default at some pint early next year.

- Yesterday, the Fed's Vice Chair Stanley Fischer announced that he will step down on or around 13 October, leaving four empty seats in the Board of Governors.

- The Wall Street Journal reports that President Trump is unlikely to nominate Gary Cohn as the next Fed Chair. This has increased the probability of the reappointment of Janet Yellen but Trump is known for wanting his own people in key positions.

- The many empty seats mean that it is difficult to say what direction the Fed will take next year. The Republicans may use the opportunity to shift the Fed in a more hawkish and rule-based direction.

Debt limit suspended until mid-December

Despite Republican House Speaker Paul Ryan saying that the Democratic proposal to suspend the debt limit for months was 'ridiculous and disgraceful', President Trump sided with the Democrats. This means that we now have a bipartisan deal on Harvey aid, funding for the government for three months and a suspension of the debt limit until mid-December. The deal came earlier than we had expected, as we thought (in line with Republican members of Congress) the Trump administration would be willing to fight harder for a longer lasting solution to the debt limit. Basically, the deal means the risk of a government shutdown has only been postponed from the end of this month to December. Republicans still need a budget for the fiscal year 2018 (lasting from 1 October 2017 to 30 September 2018), eventually allowing them to avoid filibusters in the Senate through budget reconciliation. However, the main problem for the Republicans remains the internal disagreement between the fiscal hawks and the more moderate Republicans. The former, unlike the latter, wants to make major cuts in fiscal spending.

While the suspension of the debt limit expires in mid-December, the stricter deadline is likely some months afterwards, as the Treasury can now 'refill' some of the extraordinary measures it has exhausted in recent months. This means there is still a risk of a government default at some point in 2018. It is not an option only to increase the Treasury's cash buffer at the Federal Reserve, as it needs to be back at the current level when the suspension of the debt limit expires in mid-December.

The suspension of the debt limit also means that the US Treasury can increase its debt issuance again.

Vice Chair Fischer steps down, four out of seven seats are now vacant

In addition, Fed Vice Chair Stanley Fischer has written a resignation letter to President Trump due to personal circumstances. Fischer will step down on or around 13 October, leaving four vacant seats at the Fed. While this move caught everyone by surprise, most believed Trump would not reappoint Fischer anyway when his term expired in June next year, so markets barely moved on the announcement.

With four out of seven seats at the Fed Board of Governors currently vacant - and possibly soon five, as it is not our base case that Trump will reappoint Janet Yellen as Fed Chair (see more below) - Trump has the power to shape the Federal Reserve in the way he wants (although the Senate has to approve his nominations). This makes it more difficult to say what the Fed will do next year, as it is difficult to say in which direction the Fed will go. Trump has not said much about monetary policy but he has said a few mutually contradicting things: (1) he says he wants higher rates but is a 'low interest rate guy' and (2) he says a strong USD is a sign of strength but that a weak USD is good for US exports. In other words, it is difficult to say whether the Fed will turn more hawkish or more dovish, as Trump does not really seem interested in monetary policy, as he thinks of economic policy in terms of trade policy and tax reform/deregulation/infrastructure investments. While President Trump does not seem very interested in monetary policy and the Fed, the Republican Party certainly is, as many Republicans are dissatisfied with the Fed's low-rate policy. Many Republicans want a more rule-based Fed, which bases its monetary policy decisions on a policy rule. Based on a simple Taylor rule, which links the Fed funds rate to inflation and unemployment, the Fed funds rate should be around 3% now. In other words, we might see a more hawkish and rule-based Fed next year but the uncertainty is high. For more, see what we wrote back in February: Research US: Trump to nominate three Fed governors - Tarullo resigns, 13 February. Overall, it seems fair to say, the Fed's independence may come under greater pressure.

Trump has already nominated Randal K. Quarles, as former Treasury Department official, to serve as Fed Vice Chair for Supervision (see NY Times). Quarles is considered more dovish on financial regulation than Daniel Tarullo, who was previously in charge of supervision (at least in practice).

Trump's economic adviser Gary Cohn was favourite to succeed Yellen as Fed Chair but The Wall Street Journal reports that Trump is unlikely to nominate him due to Cohn's criticism after Charlottesville. According to PredictIt, the most likely scenario is now that Yellen will be reappointed but this is not our base case.

GBPUSD Pushed Towards 1.3100

Sterling continues to move higher during the European trading session, as the U.S dollar index comes under selling pressure, ahead of the European Central Bank's policy decision in Frankfurt, later today.

Currently, price-action is testing resistance towards the current the 1.3100 region, which the pair now trading above the 1.3082 level, which represents the former monthly pivot point for the GBPUSD pair.

This afternoons price moves in the GBPUSD pair, may be strongly correlated to the direction the EURUSD pair takes, during and after ECB President Mario Draghi's press conference.

Key technical resistance above the 1.3100 level is located at 1.3125,1.3190 and 1.3220.

To the downside, intraday GBPUSD support is found at 1.3045, 1.3019, and the daily pivot point, at 1.2998. Below the 1.2998 level, the 50-day moving average becomes key support, at 1.2984.

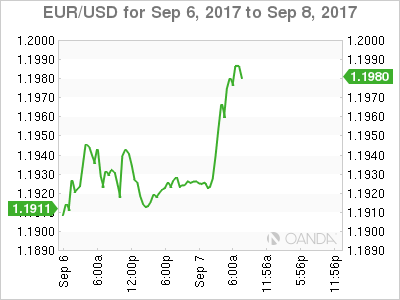

EURUSD Tests 1.20 ahead of ECB Meeting

The EURUSD continues to advance higher during the European trading session, with the pair falling just short of 1.2000, hitting 1.1995, ahead of today's European Central Bank interest rate decision and press conference.

Euro buyers look ready to continue the strong uptrend seen over the summer months, with technical traders ready to test towards the historical 1.2139 Fibonacci resistance level.

The EURUSD remains strongly bullish against the U.S dollar on all-time frames, although fundamental developments from today's ECB press conference will dictate the pairs intraday directional bias.

Key technical resistance is located at 1.2030, the yearly price high at 1.2070, and the 1.2100 level. Above the 1.2100 level, traders should look to strong weekly resistance from 1.2139, 1.2160 and the December 2014 price high, at 1.2220.

To the downside, look for key intraday support at 1.1945, 1.1918 and 1.1884.

Below 1.1884, look for strong EURUSD weekly support at the 1.1744 and 1.1664 levels.

Markets Seek Clarity From Draghi

Thursday September 7: Five things the markets are talking about

The best-laid plans sometimes fail to materialize. For instance, if the ECB had been hoping to exit QE undercover of the Fed's observance to a predictable path of 'normalisation' has very much been complicated by stubbornly low U.S inflation and U.S political uncertainty.

The EUR has appreciated close to +14% since the start of this year outright, causing a few sleepless nights at the ECB because it has been pushing inflation lower, the opposite to what the Euro policy makers require.

What to expect from the ECB?

Consensus expect the ECB to delay announcing plans to reduce monetary stimulus or QE until October, following the 'single' unit's recent rise above the psychological €1.20 handle – the banks pain threshold level. The ECB will have to revise inflation projections down, blaming the strong EUR, and to acknowledge further downside risks – which should cap the EUR for the short-term.

Note: Saying nothing would constitute an invitation to drive the EUR higher, which no doubt is not in the interest of the ECB.

The 'smart' money will be 'short' EUR's or small core 'long' the single unit heading into this morning's ECB press conference (08:30 am EDT) in particular, with many expecting Draghi to address the pace of EUR appreciation.

The markets objective will be to buy dips, which should be short lived as any decline will be used to position for a further move up in EUR/USD on a 6-12 month horizon (€1.25-27).

Elsewhere, the U.S dollar continues to struggle against its G-10 peers as tensions over North Korea outweigh positive sentiment arising from yesterday's extension of the U.S debt limit. The market is also keeping an eye on Hurricane Ira (and crude prices), which is currently barrelling towards Florida.

1. Stocks get the green light

In Japan, the Nikkei share average rallied overnight, pulling away from its four-month intraday low after news of an agreement to raise the U.S debt limit yesterday helped restore investors' risk appetites. The Nikkei ended +0.2% higher, while the broader Topix rallied +0.4%.

Down-under, Australia's S&P/ASX 200 Index was little changed after Aussie retail sales data struggled last month (+0.0% vs. +0.2%e). In South Korea, the Kospi rallied +1.1%.

In Hong Kong, stocks reversed earlier gains to end lower overnight, pressured by losses in the mainland share market. The Hang Seng index fell -0.3%, while the China Enterprises Index lost -0.2%.

In China, equities fell, as profit taking in resource shares following their recent rally and weakness in the banking sector offset strong gains in real estate companies. The blue-chip CSI300 index fell -0.5%, while the Shanghai Composite Index lost -0.6%.

In Europe, regional bourses trade mixed with outperformance in the DAX, whilst weakness is observed on the FTSE 100 and the Swiss SMI. Markets are trading in a holding pattern ahead of this morning's ECB rate decision and press conference.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx600 flat at 373.8, FTSE flat at 7357, DAX +0.6% at 12283, CAC-40 +0.3% at 5115, IBEX-35 +0.1% at 10140, FTSE MIB -0.4% at 21739, SMI -0.2% at 8839, S&P 500 Futures -0.2%

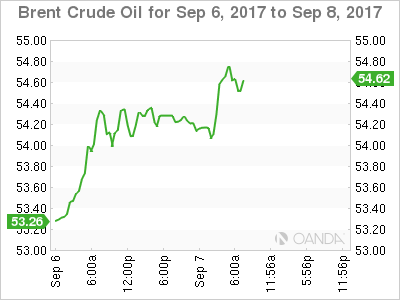

2. Oil dips on fears 'Irma' could hit crude shipments, gold steady

Oil prices have dipped a tad overnight over fears that Hurricane Irma could interrupt crude shipments in and out of the U.S, and as Libyan output begins to recover from disruptions.

Note: However, prices are receiving some support from rising demand in the U.S, where Gulf Coast refineries are restarting in the wake of Hurricane Harvey.

Brent crude futures have dipped -21c, or -0.4% to +$53.99 a barrel, while U.S West Texas Intermediate (WTI) crude futures are down -18c, or -0.4% at +$48.98 a barrel.

Also putting pressure on crude prices is oil output at Libya's Sharara field, the country's largest, resumed yesterday, which had been shut down for more than two-weeks.

Investors will take direction from todays EIA inventory report (11:00 am EDT).

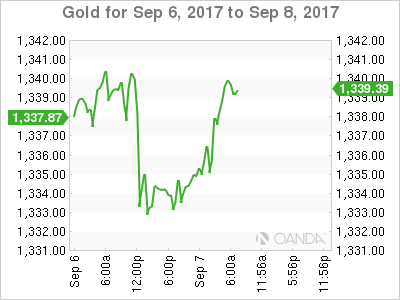

Expectations that the Fed will raise rates gradually have been a boon for gold. Ongoing rising tensions between the U.S and North Korea have also boosted demand for the 'yellow' metal, contributing to a +15% gain this year.

Overnight, gold prices held steady, supported by a weaker dollar, as markets await the outcome of today's ECB policy meet – spot gold is unchanged at +$1,333.90 per ounce, after easing -0.3% in yesterday's session.

3. Unexpectedly 'hawkish' Draghi could trigger Bund sell-off

With the ECB expected to do whatever it takes to keep short end rates anchored has fixed income dealers believing that the eurozone bond yield cure will steepen even further. Current Eonia forwards imply no rate rises by the ECB until spring 2019.

Therefore, any 'hawkish' talk should push longer yields higher. If Draghi sounds more hawkish than expected, this would trigger a sell-off in German bunds, with 10-year yields rising back to the +0.40-0.45% area. 10-year Bund yields currently trade at +0.36%.

Elsewhere, U.S 10-year Treasuries declined -1 bps to +2.09%, while U.K Gilt yields back up +2 bps to +1.026%.

In Sweden, the Riksbank is sticking to its established policy script – this morning policy makers kept both policy and rate path unchanged. The statement reiterated that first rate hike will not be seen until mid-2018, but was prepared for more easing if necessary. Governor Ingves noted that the “domestic economy was developing better than expected, but its too early to make policy less expansionary.” The SEK ($7.9688) currency has strengthened faster than its July forecast.

4. Dollar under pressure vs. G10

The EUR/USD (€1.1980) is trading at session highs ahead of the ECB rate decision. The ECB is expected to keep policy steady with particular focus on whether euro policy makers would provide any guidelines on its looming QE taper. No final decision on the next steps is expected until next month's meeting.

Overall, the FX market is relatively quiet, but the USD remains on soft footing vs. its G10 counterparts. USD/JPY (¥108.88) is a tad lower as the Korea peninsula concerns remain on the front burner with another N. Korean missile launch possible ahead of Sept. 9.

GBP (£1.3071) has rallied to a four-week high ahead of the U.S open. Down-under overnight, the AUD (A$0.8015) briefly held some strength for most of the session before falling back after a tepid Aussie retail sales report last month.

5. Eurozone economy stronger than estimated

Data this morning showed that the eurozone economy grew more quickly over the 12 months through June than previously estimated. Eurostat left its estimate of quarter-to-quarter growth for the three months to June unchanged at +0.6%. But, raised its estimate of growth in Q3, 2016 to +0.5% from +0.4%.

As a result, it now estimates that the economy was +2.3% larger in the three months to June than it was in the same period last year – the fastest rate of growth recorded in six-years.

Note: The Eurozone has outpaced the U.S in Q1 and accelerated further in the three months to June.

But data released by the European Union's statistics agency showed the pickup began earlier than previously thought. it raised its estimate of growth in the third quarter of last year to 0.5% from 0.4%.

Note: The ECB is expected to raise their growth forecasts for this year and next later this morning.