Sample Category Title

USDJPY Showing Neutral Picture In Short And Medium Term, Risk Is To The Downside

USDJPY is showing a neutral picture in the medium term, trading within a broad range between 108.00 and 114.50 since March. The near-term bias is also neutral as the pair has been in a consolidation phase since mid-August and is pivoting around the key 110.00 level. This level is also the 50% Fibonacci retracement of the uptrend from 101.18 to 118.66 (November to December 2016 rally).

Momentum oscillators are moving sideways and highlighting the lack of direction in the market. RSI and MACD are also in bearish territory which suggest the immediate bias is tilted to the downside. The July 18 bearish crossover of the 50-day and 200-day moving averages also point to bearishness in the market.

The first support comes in the zone between 107.96 (61.8% Fibonacci) and the key 108.00 level. This is the lower end of the March-September range and a break to the downside would change the overall bias to bearish from neutral with scope to target 105.50.

USDJPY would need to clear 110.00 and break above the top of the recent range at 110.90 to weaken downside pressure. Breaking above the March-September top of the range at 114.49 could see another leg higher for a re-test of the December high at 118.66. From here, there would be increased odds for a resumption of the longer-term uptrend from November 2016.

For now, there is little momentum in the market and the neutral bias is expected to stay in place.

NZDUSD In Clear Downtrend, Ichimoku Cloud Reaffirms Bearish Picture

NZDUSD maintains a weak technical undertone and has been in a clear downtrend since retreating from the July 27 top of 0.7557. The market has been making lower highs and lower lows and is currently trading below the key 0.7200 level.

On the 4-hour chart, the immediate risk is to the downside as prices have fallen below the 20- and 50-period moving averages. The bearish view was strengthened after the crossover of the shorter-term SMA below the 50 SMA on August 23. Downside momentum is gaining traction since the RSI has broken below 50 and is entering bearish territory.

The immediate target to the downside is the August 31 low at 0.7131. From here, the focus would turn to another key area at 0.7057 which acted as support as well as resistance in the recent past (between March to June). The key psychological 0.7000 level is another support which, if broken, would target the multi-month low at 0.6817 (touched on May 11).

The bearish bias remains favorable unless there is a move above support-turned resistance at 0.7200 that would decrease downside pressure. A rise above the September 5 high of 0.7262 and cloud top would open the way to key resistances level at 0.7300 and 0.7340. A continued push higher would see a shift in the current bearish trend.

For now, there are no signals for a change in the downtrend. Ichimoku cloud chart analysis reaffirms the bearish picture as NZDUSD is below the cloud.

Dollar Fails To Rise On Higher US Debt Ceiling, Focus On ECB

After a surprise rate hike from the Bank of Canada, US Congressional leaders and the president decided unexpectedly on late Wednesday to raise the government’s debt limit. However, the dollar failed to strengthen, as geopolitical risks continued to weigh on the markets, while the Fed’s Vice Chairman surprised markets by submitting his resignation. The euro was also in focus, as investors are widely expecting the European Central Bank to kick off its policy meeting later today.

On Wednesday, the US president, Donald Trump agreed with congressional leaders to lift the maximum amount the government can borrow and extend funding until December 15. However, this was a surprise as Trump’s fellow Republicans were hoping for a longer-term debt limit extension rather than a shorter-term deal, which was mainly supported by Democrats whose proposal was finally accepted by Trump. The US Treasury Secretary, Steven Mnuchin, said to reporters after the decision that the president chose to keep the period short as he considers raising military funding this year given the heightened risks from North Korea.

In the same day, Trump said that a military response against to North Korean threats was “certainly not his first option”, while he favored stricter sanctions that will likely limit North Korea’s spending on nuclear programs. Meanwhile, in South Korea, the public protested the deployment of the country’s defense system which took place early today in order to strengthen country’s military power to refute North Korean potential attacks. This comes after the South Korean Business Daily reported that North Korea is planning to fire an intercontinental ballistic missile probably this Saturday when the regime will celebrate the founding day.

In other news out of the US, the Fed Vice Chairman, Stanley Fischer, unexpectedly submitted his resignation on Wednesday eight months before his term ends, saying that he would leave his position in mid-October.

The dollar index could not gain on the debt ceiling decision, retreating by 0.11% to 92.11 during Asian trading.

Dollar/yen declined by 0.13% to 109.09 while dollar/swissie was mainly flat around 0.9562.

Euro/dollar edged up by 0.08% to 1.1925 ahead of the ECB policy meeting later today when the markets will focus on ECB Chief Maio Draghi’s new hints on the strategy the central bank will follow to taper its asset holdings.

The loonie eased against its US counterpart but maintained most of the gains it attracted yesterday, which drove the currency to a more than two-year high after the BOC decided to hike rates to 1% on Wednesday. Dollar/loonie was slightly down by 0.01% at 1.2217.

The aussie followed a downtrend early in the session as data out of the country showed that retail sales and trade balance fell short of expectations in July. Household spending posted zero growth m/m, missing the forecast of a rise of 0.3%. The figure fell below the previous mark of 0.2% which was downwardly revised from 0.3%. Regarding the trade balance, the surplus narrowed from A$0.888bn to A$0.460bn, while analysts expected a surplus of A$0.875bn.

Following the data, the aussie retreated by 0.16% to $0.7986.

Looking at commodities, oil prices declined from yesterday’s highs as the weekly report from the American Petroleum Institute showed that oil inventories rose by 2.791mn barrels last week while expectations were for the figure to increase by 4.000mn barrels. The change in inventories was at negative 5.780mn barrels in the week ending August 31. However, experts believe that future reports will give a clearer picture on the negative impact of the disastrous tropical storm Harvey caused to the US oil industry, while the EIA statement is also expected to provide evidence on US oil inventories later today. In the meantime, energy producers are also worried about Hurricane Irma which has battered the Carribean yesterday and is currently heading towards Florida.

WTI crude dropped by 0.24% to $49.04 per barrel while Brent declined by 0.35% to $54.01.

Gold was up by 0.26% to 1337.40 an ounce as geopolitical uncertainties linger in the background.

ECB Seen Holding Off On Taper Talk

It's been a steady, albeit unremarkable, start to trading on Thursday, with risk appetite gradually improving ahead of today's ECB decision.

The euro has been well bid this morning ahead of the ECBs interest rate decision and Mario Draghi's press conference, with traders either anticipating taper talk or testing the central banks resolve as it prepares to further wind down its quantitative easing program. The current program expires at the end of the year and there is a clear desire to reduce it to zero and normalize monetary policy, but with this comes many obstacles, most notably the goal of 2% inflation.

Not only is the ECB far from achieving this target but this year's appreciation of the euro has made the job of do so all the more difficult. The euro is up more than 13% against the dollar this year and more than 7% against the pound which will continue to weigh on inflation going forward. The issue for the ECB is that by announcing a reduction in stimulus, it risks exacerbating the problem by driving the euro higher again, assuming of course that this isn't already priced in.

The ECB is clearly already uncomfortable with the gains that the currency has made – as seen by repeated mentions of it and coincidentally timed “ECB source” leaks referencing QE – to the point that it is now expected to hold off on announcing an extension to the program until later in the year. The likelihood remains that another reduction will be announced now either in October or December with the goal or ending the program at the end of next year but policy makers are clearly being very careful about how and when they announce it so as to avoid any unwanted euro appreciation.

I therefore expect ECB President Mario Draghi to be very dovish today and possibly even leave the door ajar to no tapering to take place when the extension is announced, even if that is extremely unlikely to happen. The goal of this will be simply to take the pressure off the currency ahead of the announcement later in the year and manage its ascent. Whether traders buy it or not is another question and we're already seeing some appetite this morning to test the 1.20 level that has so far held strong.

With risk appetite gradually improving and geopolitics becoming less of a drag on markets, for now, focus is switching back to fundamentals and today's US data will give us some insight into just that. Weekly jobless claims, non-farm productivity and unit labor costs data will all be released ahead of the open on Wall Street today and we'll also get crude inventory numbers from EIA. A build of a little over 4 million barrels is expected this week with the effects of Hurricane Harvey driving much of the gains.

Technical Outlook: WTI Oil May Come Under Pressure On Fears Of Hurricane Irma Impact, Rising Oil Inventories

WTI oil price is consolidating in early Thursday’s trading after strong bullish acceleration in past two days peaked at $49.40.

Strong recovery rally from $45.57 low retraced 76.4% of $50.41/$45.57 pullback, as oil price received strong boost on increased demand after Texas refineries were restarted.

Technical studies on daily chart are in strong bullish setup but overbought slow stochastic suggests oil price may show hesitation ahead of key barriers at $49.65 (200SMA) and psychological $50.00 barrier.

Oil is awaiting release of EIA crude stocks data today (release was delayed for one day due to US Labor Day holiday on Monday) which may pressure the oil price as forecast for today shows a build of oil inventories by 4 million barrels after series of strong draws in previous few weeks.

On the other side, release of API crude stocks data on Tuesday showed build of 2.8 million barrels last week, compared to forecasted build of 4.0 million barrels.

Rising oil inventories signal lower price and the oil price may come under increased pressure on rising fears on impact from Hurricane Irma which is approaching the US coast and may interrupt oil shipments in and out the US.

Session low at $48.93 marks initial support followed by former highs at $48.72 and broken Fibo 61.8% barrier at $48.56.

Res: 49.40, 49.65, 50.00, 50.20

Sup: 48.93, 48.72, 48.56, 47.89

Technical Outlook: AUDUSD – Extended Hesitation At 0.8000 But Bulls Remain Intact

The Aussie dollar remains bid but show strong hesitation at 0.8000 resistance which was dented on Tue/Wed's spikes to 0.8028/20 but so far without close above. In addition, long-legged Doji that was left on Wednesday supports the notion. The pair came under pressure overnight after Australian Retail Sales miss (0.0% in July vs 0.3% forecast) but dips were limited so far at 0.7974, keeping intact rising 10SMA (currently at 0.7960) which marks initial support. Daily techs are in full bullish setup and supportive for further advance, but close above 0.8000 is required to generate bullish signal for extension towards key barrier at 0.8065 (23 July new 26-month high) and extension of broader uptrend on break. On the other side, repeated failure at 0.8000 would risk extended consolidation which needs to hold above 0.7960/50 supports (10SMA/daily Tenkan-sen) and keep immediate bulls intact. Otherwise, break lower would signal recovery stall and stronger pullback which would expose daily Kijun-sen (0.7918) and daily cloud top (0.7894)

Res: 0.8028, 0.8042, 0.8065, 0.8100

Sup: 0.7974, 0.7960, 0.7950, 0.7918

Daily Technical Analysis: USDCAD Down After An Unexpected Rate Hike

As we have seen tightening in the US by the Fed over the past year, there usually is a correlation with other Western economies following the US lead in returning Monetary Policy to historical levels. In this case, the BoC had increased their rate for the second time in recent months largely following an improvement in GDP Growth, along with price stability in their major export Oil and Gas. Needless to say, BoC is somewhat hamstrung with its ability to continue hiking due to its high household debt levels along with real estate prices in Toronto having dropped 20% since April 2017.

At this point the USD/CAD is trapped below the POC zone 1.2308-1.2336 (order block, trend line, D H3, W L3, 61.8, EMA89) and we could see another rejection if the price retraces to the zone. The MACD is way below the 0 line, while histograms are up so we might see a retracement. However 4h or strong 1h candle close below 1.2148 should target 1.2070 that is a both a weekly and daily support.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

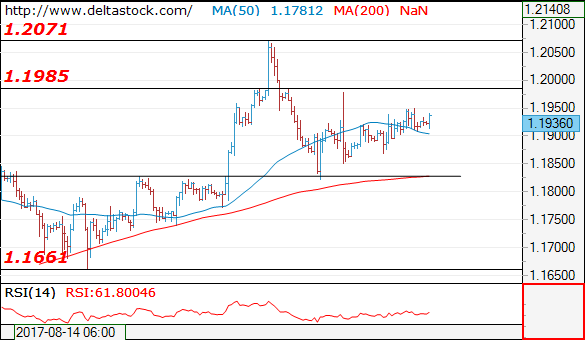

EUR/USD

Current level - 1.1936

The intraday bias is slightly positive, for a test of 1.1985 resistance area and the latter is expected to cap the upside, for another leg downwards, to 1.1830. A violation of the latter will challenge 1.1660.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1980 | 1.2070 | 1.1830 | 1.1830 |

| 1.2070 | 1.2160 | 1.1740 | 1.1660 |

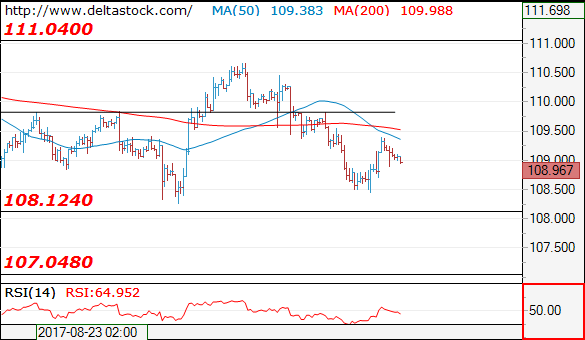

USD/JPY

Current level - 108.96

Current rebound should be considered corrective, preceding a break through 108.10, towards 107.00 area. Initial intraday resistance lies at 109.80.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.80 | 111.00 | 108.10 | 108.10 |

| 110.60 | 112.20 | 108.10 | 107.00 |

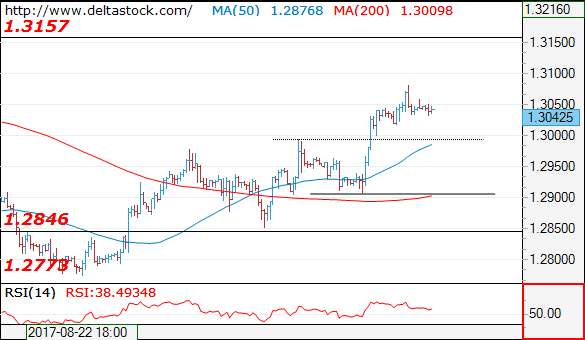

GBP/USD

Current level - 1.3042

The bias is still positive above 1.2990, for a possible test of 1.3150 area. Crucial on the downside is 1.2910 is a violation of that area will challenge 1.2770 low again.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3080 | 1.3157 | 1.2990 | 1.2773 |

| 1.3157 | 1.3260 | 1.2907 | 1.2606 |

EUR Strengthens Ahead Of ECB Meeting

Euro traps Draghi

Investors are bracing for an event heavy day. The highlight will clearly be the European central banks. However, the substantives information on monetary policy strategy path from this meeting is unlikely. We had originally penciled in a comments outlining the path towards normalization. The recent strength in Euro will keep the ECB focused on exchange rates and likely water down any discussion on extension of the Asset Purchase Program. While economic data has improved significantly in the EU, a slight delay to measure the market’s reaction to any Fed actions won’t meaningfully risk a surge in inflation outlook.

Yet, titillating the markets with hints of cutting QE purchases (even buffered with minimal extension) could send EURUSD back above 1.20. We don’t think Draghi will take the risk. There is a case that Draghi is only delaying the inevitable and should start announce an QE extension today to prepare the market for eventual trimming of size. Markets will likely dissect every sentence causing EUR vol to increase, but the longer-term outlook indicates that the ECB need to start tighten policy. The Euro has become less sensitive to short-end yield movements; beneficial yields spread will send EURUSD higher. Europe has enjoyed the benefits of a weaker Euro, judging from the improvement in German industrial production (4.0% from 2.7% y/y) exports will need to adjust to a strong Euro moving forward.

Long SEK Riksbank delay

Elsewhere the Riksbank will keep to the sidelines in their rate decision today. Sweden central banks is likely to prefer to let the ECB to move first on normalization. The Riksbank today will likely copy Draghi trick of balancing acknowledging stronger economic growth without shifting policy strategy. However, as with Euro traders the market sis not fooled by the delay. Sweden’s above trend in growth and inflations indicates that policy needs to tighten. In addition, as with the ECB asset purchase program technicalities could be actually preventing the Riksbank from purchasing more assets. Any suggestion that market liquidity could handle further intervention would be a marginally dovish outcome and negative SEK. However, most logical path for the Riksback are slow and steady removal of emergence measures and strong SEK.

Donald and Democrats deal

Finally, Wall Street is celebrating the removal of the immediate threat of the debt ceiling. However, the real news was Trump working with Democrats with a clear success. In rare bipartisan deal Trump, republicans with democrats extended the U.S. debt limit and provide government funding until Dec. 15th. Should the Republican-led Congress pass the bill, the 3-month deal would prevent an extraordinary default on U.S. government debt, preserve the government funded for the fiscal year starting Oct. 1. This was a massive first step. True it was clipped to a money for victims of Hurricane Harvey but still. The path towards meaningful tax reform just got a little less steep (an potentially other stimulus). As a desk we were early to write off the Trump pro-growth, reflation story, however a shift to the center, highlighted by this 3-month extension, could the start of something real. A unified US government could have profound effects on our market outlook.

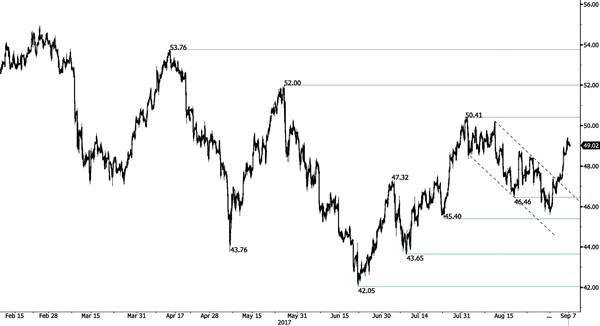

CRUDE OIL Drifting Higher

Crude oil is showing further buying interest since bouncing off key support at 45.40. Strong resistance can be found at 50.41 (31/07/2017). Hourly support is given at 45.40 (17/08/2017 high). Expected to show continued short-term bearish move.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).