Sample Category Title

Technical Outlook: AUDUSD Holding Within Triangle Ahead Of JH Speeches

Repeated strong rejection at 0.7867 (Fibo 61.8% of 0.7807/0.7962 upleg) on Friday and subsequent quick bounce suggests very strong support. In addition, two attempts below daily Tenkan-sen (0.7885) failed to close below, signaling that near-term pullback from 0.7962 (17 Aug high) might be running out of steam.

Near-term action is holding in triangular pattern (upper boundary at 0.7933, reinforced by daily Kijun-sen and lower at 0.7867) with break of either side needed to generate firmer direction signal.

Top at 0.7962 marks next pivotal barrier, violation of which would open way for fresh attempts through 0.8000. On the downside, loss of strong 0.7867 support would risk retest of key n/t support at 0.7807 (15 Aug correction low), reinforced by the top of rising daily cloud.

Res: 0.7920, 0.7933, 0.7950, 0.7962

Sup: 0.7885, 0.7867, 0.7832, 0.7807

All Eyes On Jackson Hole

US futures are flat ahead of the open on Friday, in keeping with moves seen elsewhere in the markets as we await comments from two of the world’s most influential central bankers later on in the session.

The Jackson Hole Symposium is widely regarded as one of the most notable annual events, not only because of the speakers it attracts but also because it has been used as a platform to warn of upcoming policy announcements. In the past it has been Janet Yellen’s predecessors – Alan Greenspan and Ben Bernanke - that have delivered such warnings, the question today is whether she will do the same.

The final months of the year are going to be very interesting as far as the Fed and the ECB are concerned which makes today’s appearances from Fed Chair Yellen and ECB President Mario Draghi all the more interesting. Both central banks have started the process of tightening monetary policy, although the ECB would probably claim it’s more a case of removing accommodation. Either way, with the process underway, investors are keen to know what they plan next.

The Fed is already well underway with its rate hikes, having started almost two years ago and having raised three more times since (so four in total). With inflation still lagging well below target though, there is growing unease within the central bank about whether the current pace is appropriate. Investors have long been unsure that there’ll be another rate hike this year and the message seems to finally be filtering through to the Fed. It will be interesting to see whether Yellen will address this today or instead focus on balance sheet reduction, which is expected to be announced in September and doesn’t interest investors in the same way.

The ECB is taking a far more cautious approach having dealt with a far more severe crisis for the last decade, one that the region is only just starting to truly recover from. The central bank announced one reduction on asset purchases last December and it’s expected to announce another in the coming months. While investors are desperate to get more information on this, I think it’s highly unlikely given the ECBs unease at past market reactions. I think the central bank will prefer to address this after the meeting next month on home turf and won’t want to risk further tightening of financial conditions in the meantime, with the euro having already sharply appreciated this year.

Yen Inches Down As Inflation Pressure Remains Weak In Japan

According to the Ministry of International Affairs and Communications, Japanese core inflation continued rising steadily for the seventh consecutive month in July. However, the measure remained weak, as anticipated, far away from the Bank of Japan’s (BOJ) 2% target, reducing chances for a rate hike anytime soon. Consequently, the yen retreated slightly against its US counterpart during the Asian trading hours.

As analysts projected, for the month of July, headline consumer prices in Japan picked up by 0.4% y/y for the fourth consecutive month.

Excluding fresh food items, the core CPI index improved in line with forecasts by 0.1 percentage points to 0.5% y/y, recording the highest growth since April 2015 and gaining for the seventh straight month. Though it remained below 2015 levels when the index was above the 2% target before the massive earthquake of a magnitude of 8.5 (Richter scale) hits the country. Barring energy products as well, the index posted its first growth in five months, increasing by 0.1% y/y.

Food prices were up by 0.6% y/y (-0.3% m/m, seasonally adjusted), while fuel, light and water charges increased the most, jumping by 4.3% y/y (0% m/m, seasonally adjusted).

In Tokyo, the flash CPI index for the month of August, experienced the highest increase since 2016, hinting that nationwide inflation to be released next month might elevate. The index rose surprisingly by 0.4 percentage points to 0.5% y/y, exceeding the forecast of 0.3%. Core CPI came in better than expected as well at 0.4% y/y. This was above the forecast of 0.3% and July’s mark of 0.2%.

While the Japanese economy picked up speed in the second quarter, with GDP growing substantially from 0.4% to 1.0% and household and business spending showing signs of improvement, companies still felt hesitant to raise prices. They were also reluctant to increase wages as they believe that the recent economic pickup might be temporary. Hence, taking all this into account, the decision of the BOJ in July to downgrade its inflation forecasts for the next two years is justified together with the projections that the BOJ will likely stick to its current ultra-easy policy during its next meeting on September 20. Note that the BOJ expects inflation to touch its 2% target in the fiscal year to March 2020 as it anticipates that gradual developments in the labor market will boost prices.

Looking at the reaction in the forex markets, the yen fell immediately by 0.20% relative to the dollar, with dollar/yen climbing from 109.51 prior the data release to a session high of 109.71. However, the pair edged down afterwards, last trading at 109.64.

Markets Turn To Yellen And Draghi For Guidance

Today, all eyes will be on two highly-anticipated speeches by Fed Chair Janet Yellen and ECB President Mario Draghi at Jackson Hole. Kicking off with Yellen, her speech will center on financial stability. Even though the subject suggests she may refrain from commenting on interest rates, she could always make a reference to the outlook of the US economy that indirectly conveys her policy view. Should she echo recent comments from Fed’s Dudley, who still favors another rate hike this year, markets could reprice the probability for such action, which now rests at only 39% according to the Fed funds futures. This could help the dollar recover some of its latest losses.

USD/JPY edged north after it found support once again near the 108.70 (S1) obstacle. Nevertheless, the rate found again resistance at 109.75 (R1) and retreated somewhat. The pair has been oscillating between 108.70 (S1) and 111.00 (R3) since the 28th of July and therefore, the short-term path remains sideways. Having said that, given that the latest recovery started from near the lower bound of the range, we see the case for the pair to continue trading higher. Yellen’s speech today could be the catalyst for further advances. A break above 109.75 (R1) could set the stage for more bullish extensions, perhaps towards our next resistance level of 110.35 (R2).

As for the bigger picture, the pair continues to trade within the broader range between 108.70 (S1) and 114.40. This keeps the medium-term outlook flat as well, and enhances the case for further recovery within the range. Nevertheless, we will keep an eye on a potential US government shutdown, increased speculation around which could bring the pair under renewed selling interest in coming weeks. In our view, a clear close below the key support zone of 108.70 (S1) is needed to turn the medium-term picture back negative.

Turning to Draghi, even though media reports familiar with 'ECB sources' suggest he is unlikely to deliver a new policy message, we believe investors will still be hanging on his lips for any hints on policy and/or the euro. That said, we think that any such remarks are unlikely to deviate from the communication at the latest ECB press conference. Back then, Draghi was explicit in stating that the conversation regarding changes to QE will take place in the 'autumn', suggesting he is highly unlikely to preannounce anything at a non-monetary policy meeting, especially if he doesn’t have the blessings of the Governing Council.

As such, we view the risks surrounding the euro today as being tilted to the downside. Investors looking for a preemptive QE-tapering announcement could be left disappointed, and Draghi could even mention the risk of future exchange rate appreciation as we saw in the latest ECB minutes, both of which could weigh on the currency.

On the other hand, if he doesn’t talk about the euro at all, this may signal that the Bank is not so worried about the currency. In this case, we could even see a relief rally, as traders get the 'green light' to renter long-EUR positions. On balance though, we think this is a lower-probability outcome than the above.

EUR/USD traded in a consolidative manner yesterday, staying slightly below the key resistance of 1.1830 (R1), which appears to be the upper bound of the sideways range the pair is trading within since the 4th of August, the lower bound of which is at 1.1660 (S2). Bearing in mind that the pair is still within this range, we consider the near-term outlook to be flat for now. Having said that though, we see the likelihood for a slide within the range, especially if Draghi appears concerned about the prospect of future euro appreciation. We expect such a slide to challenge the 1.1730 (S1) support, and if the bears are strong enough to overcome it, we believe that there is the prospect for extensions towards the 1.1660 (S2) barrier.

Switching to the daily chart, we still see a longer-term uptrend. The price structure remains higher peaks and higher troughs above the uptrend line taken from the low of the 17th April. As such, we would treat any possible slide on Draghi’s remarks today as a corrective move of that longer-term upside path. We believe that we are likely to see the resumption of the existing trend in coming weeks, given that the ECB remains set to announce QE changes soon. Although fresh data could be a game-changer, we think that a realistic scenario is one where the Bank removes it QE bias in September, thereby paving the way for an announcement in October that the pace of asset purchases may be reduced by the turn of the year.

As for today’s economic data:

We get Germany’s Ifo survey for August and US durable goods orders for July. However, there releases are very likely to be overshadowed by the aforementioned Jackson Hole speeches

EUR/USD

Support: 1.1730 (S1), 1.1660 (S2), 1,1590 (S3)

Resistance: 1.1830 (R1), 1.1900 (R2), 1.1980 (R3)

USD/JPY

Support: 108.70 (S1), 108.00 (S2), 107.40 (S3)

Resistance: 109.75 (R1), 110.35 (R2), 111.00 (R3)

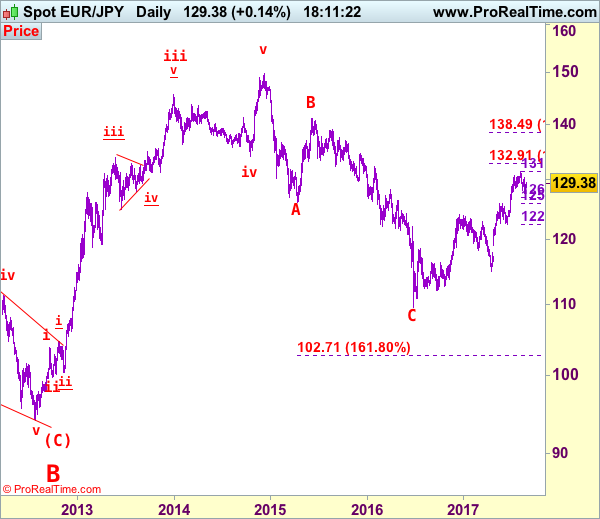

EUR/JPY Elliott Wave Analysis

EUR/JPY - 129.38

Despite falling to 127.56 late last week, as the greenback found good support there and has rebounded throughout this week, suggesting consolidation above this level would be seen and gain to 129.50-60 and possibly 130.00 cannot be ruled out, however, only a daily close above resistance at 130.40 would signal the retreat from 131.40 has ended instead, risk a stronger rebound to 130.80-85 but price should falter below 131.40, bring another leg of corrective decline later this month. Only above said resistance at 131.40 would extend medium term upmove from 109.49 low (2016 low) to extend further gain to 132.00-10, however, overbought condition should prevent sharp move beyond 132.90-00 (1.236 times projection of 109.49-124.10 measuring from 114.85) and price should falter well below previous chart resistance at 134.59.

The daily chart is labeled as attached, early selloff from 169.97 (July 2008) to 112.08 is wave (A) of B instead of end of entire wave B and then the rebound from there to 139.26 is wave (B), hence, wave (C) has possibly ended at 94.12 with a diagonal triangle as labeled in the daily chart, hence upside bias is seen for further gain. Recent rally above indicated retracement level at 116.69 (50% Fibonacci retracement of the intermediate fall from 139.26-94.12) adds credence to this view and signal major reversal has commenced but first leg of this wave C has possibly ended at 149.79, hence wave 2 has commenced with wave A ended at 126.09, followed by wave B at 141.06, wave C commenced and could have ended at 109.49, above 126.00 would add credence to this view, then headway to 130.00 would follow.

On the downside, expect pullback to be limited to 128.45-50 and bring another rebound. Below 128.30-35 would risk test of 127.80-85 but break there is needed to signal the rebound from 127.56 has ended instead, bring another test of this level. Once this support is penetrated, this would revive our near term bearishness for the corrective fall from 131.40 top to bring retracement of recent upmove to 127.44 support, then 126.85-90 (50% Fibonacci retracement of 122.38-131.40), however, only a break of latter level would provide confirmation that temporary top has been formed at 131.40, bring further fall to 126.45-50. Having said that, price should stay above previous resistance at 125.82 (now support) and euro may head north again from there. \

Recommendation: Stand aside for this week.

To re-cap the corrective upmove from the record low of 88.93 (18 Oct 2000), the wave A from there is subdivided as: 1:88.93-113.72, 2:99.88 (1 Jun 2001), 3:140.91 (30 May 2003), 4:124.17 (10 Nov 2003) and 5 ended at record high of 169.97 (21 Jul 2008). The brief but sharp selloff to 112.08 is viewed as a-b-c x a-b-c wave (A) of B. The subsequent rebound to 139.26 is (B) of B and (C) of (B) has possibly ended at 94.12 and in any case price should stay well above previous chart support at 88.93, bring rally in larger degree wave C towards 150.00.

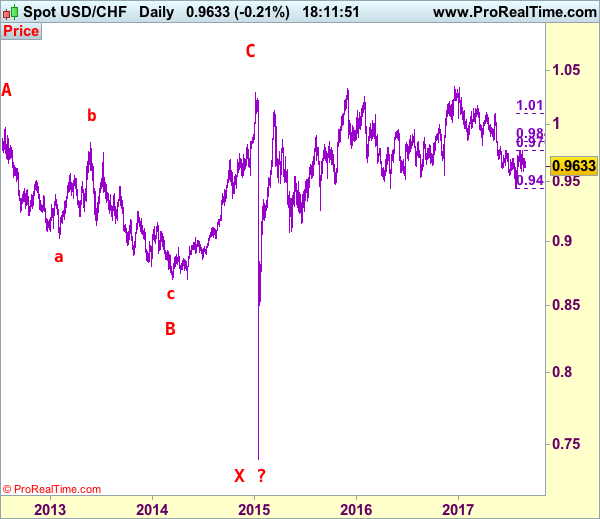

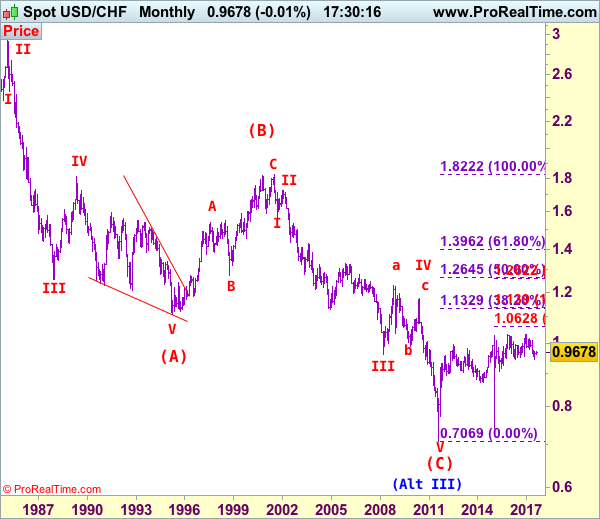

USD/CHF Elliott Wave Analysis

USD/CHF – 0.9635

As the greenback retreated again after faltering below indicated resistance at 0.9773, retaining our view that further consolidation would be seen and although initial downside risk is for weakness to 0.9583 support, as early strong rebound from 0.9438 to 0.9773 signals a temporary low has possibly been formed at 0.9438, reckon downside would be limited to 0.9540-50 and bring another rebound later. Above 0.9700 would bring another bounce to 0.9773 resistance but break there is needed to add credence to this view and extend the rebound from 0.9438 low for further gain to 0.9845-50 (61.8% Fibonacci retracement of 1.0100-0.9438) but reckon upside would be limited to 0.9890-00 and price should falter well below psychological resistance at 1.0000.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the downside, whilst initial pullback to 0.9580-85 cannot be ruled out, reckon 0.9550-55 would limit downside and bring another rebound to aforesaid upside targets. Only a drop below said recent low at 0.9438 would revive bearishness and signal the erratic decline from 1.0344 top (formed back in late 2016) is still in progress and downside bias remains for this move to extend weakness to 0.9390-00, however, loss of downward momentum should prevent sharp fall below 0.9300-10, risk from there has increased for a rebound to take place probably later.

Recommendation: Buy at 0.9555 for 0.9755 with stop below 0.9455

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.

Market Update – European Session: Focus On Jackson Hole Central Bank Speak For Policy Guidance

Notes/Observations

Jackson Hole surprises not expected but markets still await policy statements from Yellen, Draghi

German Ifo business falls less than expected in August

Overnight

Asia:

Japan July National CPI saw the core rate register its 7th straight positive reading and its largest rise since Mar 2015. ( CPI Y/Y: 0.4% v 0.4%e; CPI Ex Fresh Food (core) Y/Y: 0.5% v 0.5%e; CPI Ex Fresh Food/Energy (core-core) Y/Y: 0.1% v 0.1%)

Europe:

France July Net Change in Jobseekers: +34.9K v -17.5Ke

Germany Fin Min Schaeuble reiterated view that believes that ECB did not overstep its mandate but also reiterated stance that ECB should tighten policy sooner rather than later

Americas:

White House spokesperson: President Trump relationship with Republican congressional leaders is fine; there are policy differences but shared goals

Fed's Kaplan (moderate, voter): Has not lost faith inflation will get back to 2%; Does not favor raising 2% inflation target

Economic data

(DE) Germany Q2 Final GDP Q/Q: 0.6% v 0.6%e; Y/Y: 2.1% v 2.1%e; GDP NSA Y/Y: 0.8% v 0.8%e

(DE) Germany Q2 Private Consumption Q/Q: 0.8% v 0.7%e, Government Spending Q/Q: 0.6% v 0.6%e, Capital Investment Q/Q: 1.0% v 1.1%e, Construction Investment Q/Q: 0.9% v 1.6%e, Domestic Demand Q/Q: 1.0% v 1.0%e, Exports Q/Q: 0.7% v 1.2%e, Imports Q/Q: 1.7% v 2.0%e

(DE) Germany July Import Price Index M/M: -0.4% v 0.0%e, Y/Y: 1.9% v 2.3%e

(FR) France Aug Consumer Confidence: 103 v 103e

(DE) Germany Aug IFO Business Climate: 115.9 v 115.5e; Current Assessment: 124.6 v 125.0e, Expectation Survey: 107.9 v 106.8e

Fixed Income Issuance:

(ZA) South Africa sold total ZAR650M vs. ZAR650M indicated in I/L 2025, 2029 and 2046 bond

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 375.1, FTSE +0.2% at 7425, DAX +0.2% at 12201, CAC-40 flat at 5114, IBEX-35 +0.1% at 10368, FTSE MIB flat at 21730, SMI -0.2% at 8925, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trade higher in narrow trade with the markets awaiting policy statements from Yellen and Draghi. Supermarket stocks are under pressure on the back of reports that Amazon are looking to lower prices at Wholefoods to gain market share. Ahold Delhaize trades lower by over 4% with Carrefour down over 2% as the sector weighs. Else where Computacenter rises sharply after raising forecasts once again, and Provident Financial trades over 20% higher after providing an update on its consumer credit division.

Equities

Consumer discretionary [ Ahold Delhaize [AD.NL] -4.0%, Tesco [TSCO.UK] -1.8%, Sainsbury's [SBRY.UK] -1.1%, Carrefour [CA.FR] -2.3%, Casino [CO.FR] -1.5% (Amazon to lower prices at Whole foods to gain market share)]

Industrials: [WYG [WYG.UK] -40% (Trading update)]

Financials: [Provident Financial [PFG.UK] +22% (Consumer credit division update), Augean [AUG.UK] -50% (Notice of Assessment for Landfill Tax from Her Majesty's Revenue and Customs)]

Technology: [Computacenter [CCC.UK] +15% (Earnings)]

Speakers

UK Foreign Sec Johnson stated that would meet obligations on Brexit bil; to pay not a penny more or less than legally obligated

France Fin Min le Maire: Domestic economy remains too fragile; latest jobless data shows that more work needs to be down

German IFO Economists noted that there was no overheating of domestic economy; German businesses were getting used to Trump politics. Business climate index remained at a very high level. It added that auto industry, antitrust allegation, and the diesel affair had, no noticeable effects in the survey

US National Economic Council Dir Cohn: Trump to push for tax reform passage by end 2017; President to launch major push next week with speech in Missouri

NATO Sec Gen Stoltenberg: Urges Russia to be transparent in its exercises and abide by international agreements

S&P Affirms Hong Kong Sovereign rating at AAA; Outlook remains negative

Currencies

FX markets quiet ahead of the key speeches at Jackson Hole later today. Analysts are not expecting any surprises by either Fed’s Yellen or ECB’s Draghi. Dealers noted that Draghi was more likely to say something about Europe's single currency than the ECB's €60B/month bond purchase program

The recent uptick in US bond yields were supporting the greenback. EUR/USD just under the 1.18 level, GBP/USD at 1.2810 and USD/JPY at 109.65

Fixed Income

Bund futures trades at 164.44 down 24 ticks as euro zone fixed income markets remain in narrow ranges ahead of Jackson Hole Meeting. Downside targets 163.50 followed by 162.56. To the upside the 164.50 to 165.20 remains key resistance.

Gilt futures trades at 127.85 down 27 ticks after easing off the 128.14 high from Thursday. A resumption to the upside could eye 128.25 then 128.75. A move back below 126.51 targets 125.97

Friday’s liquidity report showed Thursday’s excess liquidity fell to €1.703T from €1.721T and use of the marginal lending facility fell to €131M from €1.085B prior.

Corporate issuance no deals price in high grade primary. For the week ending August 23rd IG Funds reported inflows of $3.3B, while High Yields funds reported inflows of $1.01B

Looking Ahead

(BR) Brazil Aug CNI Consumer Confidence: No est v 99.5 prior

06:00 (UK) DMO to sell combined £5.5B in 1-month, 3-month and 6-month bills

06:45 (US) Daily Libor Fixing

07:00 (BR) Brazil Aug FGV Consumer Confidence: No est v 82 prior

07:30 (TR) Turkey Aug Capacity Utilization: 78.7%e v 78.7% prior

07:30 (TR) Turkey Aug Real Sector Confidence (Seasonally Adj): No est v 107.7 prior; Real Sector Confidence (unadj): No est v 109.5 prior

07:30 (IN) India Weekly Forex Reserves

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) July Preliminary Durable Goods Orders: -6.0%e v +6.4% prior; Durables Ex Transportation: 0.4%e v 0.1% prior, Capital Goods Orders (Non-defense/ex-aircraft): 0.4%e v 0.0% prior, Capital Goods Shipment (Non-defense/ex-aircraft): 0.2%e v 0.1% prior; Durables Ex-Defense: No est v 5.6% prior

08:30 (SE) Sweden PM Lofven with Finland PM Siplia

09:00 (MX) Mexico July Unemployment Rate (Seasonally Adj): 3.3%e v 3.3% prior; Unemployment Rate (Unadj): 3.5%e v 3.3% prior

10:00 (MX) Mexico Q2 Current Account: -$4.5Be v -$6.9B prior

10:00 (US) Fed Chair Yellen speaks at Jackson Hole on financial stability

11:00 (EU) Potential sovereign ratings after European close(Finland Sovereign Debt to be rated by Canadian rating agency DBRS; Hungary Sovereign Debt to be rated by S&P ; Lituania and Slovenia by Fitch

11:30 (SE) Sweden PM Lofven and Finland PM Siplia post meeting press conference

13:00 (US) Weekly Baker Hughes Rig Count data

14:30 (BR) Brazil July Tax Collections (BRL): 110.0Be v 104.1B prior

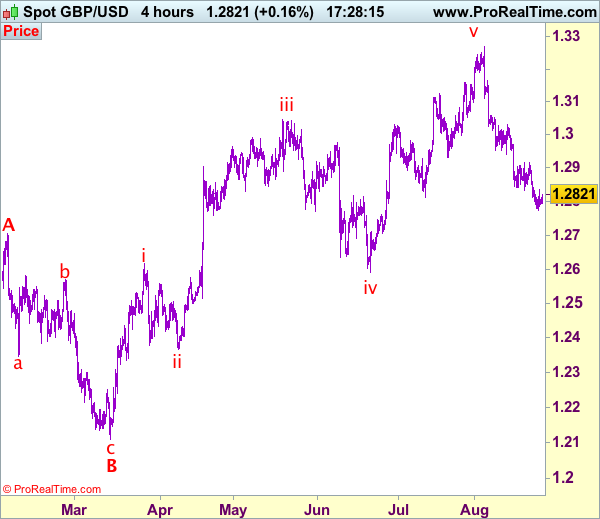

Trade Idea: GBP/USD – Sell at 1.2910

GBP/USD – 1.2823

Original strategy :

Sell at 1.2910, Target: 1.2710, Stop: 1.2970

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2910, Target: 1.2710, Stop: 1.2970

Position: -

Target: -

Stop:-

As cable has recovered after falling to 1.2774 yesterday, suggesting minor consolidation above this level would be seen and another corrective bounce to 1.2860-70 cannot be ruled out, however, reckon resistance at 1.2917-18 would limit upside and bring another decline later, below said support at 1.2774 would extend recent selloff from 1.3269 top to 1.2750 but loss of downward momentum should prevent sharp fall below 1.2730-35 and previous support at 1.2706 should remain intact, bring rebound later,

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as said resistance at 1.2917-18 should limit upside, bring another decline. Above 1.2970-80 would defer and risk a stronger rebound to 1.3000 and possibly test of resistance at 1.3032, however, only break of latter level would abort and signal the fall from 1.3269 has ended instead, bring a stronger rebound to 1.3059 and possibly towards 1.3100 but previous support at 1.3112 (now resistance) should remain intact.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

Technical Outlook: USDJPY Attempts Above N/T Congestion Tops Ahead Of Yellen

The pair edged higher in Asian trading on Friday, in extension of previous day's rally and probing the upper boundary of three-day congestion at 109.80, reinforced by sideways-moving daily Tenkan-sen and falling 20SMA.

Daily technicals in firm bearish mode do not see stronger prospect for more significant recovery on firm break above 110.00 for now, but formation of reversal pattern on weekly chart, following repeated downside rejections at weekly cloud base (108.80), could be seen as initial bullish signal.

However, near-term direction would be likely defined by the tone of Yellen / Draghi's speeches at Jackson Hole later today.

Firmer bullish signal could be expected on sustained lift above 110.00 barrier which would expose next breakpoints at 111.00 zone, while increased risk of continuation of larger downtrend from 114.49 (11 July peak) could be expected on firm break below weekly cloud base.

Res: 109.77, 110.00, 110.40, 111.00

Sup: 109.49, 109.15, 108.84, 108.60

Trade Idea: GBP/JPY – Sell at 141.40

GBP/JPY - 140.57

Original strategy:

Sell at 141.40, Target: 139.40, Stop: 142.00

Position: -

Target: -

Stop: -

New strategy :

Sell at 141.40, Target: 139.40, Stop: 142.00

Position: -

Target: -

Stop:-

As the British pound has rebounded after falling to 139. 35 yesterday, hence consolidation above this level would be seen and another corrective bounce to 141.00-05 cannot be ruled out, however, reckon upside would be limited to 141.40-50 and bring another decline later, below 139.80-85 would signal the rebound from 139.35 has ended, bring retest of this level, break there would extend recent decline to 138.70 (previous support) but loss of downward momentum should prevent sharp fall below 138.30 and 138.00 should hold, risk from there has increased for another corrective rebound.

In view of this, would not chase this fall here and we are looking to sell sterling on subsequent recovery as 141.40-50 should limit upside and bring such a decline. Only a break of resistance at 142.05 would suggest low is possibly formed instead, bring a stronger rebound to 142.50-60 but resistance at 143.20 should remain intact and bring another decline later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.