Sample Category Title

Dollar Direction Depends On ECB Rhetoric

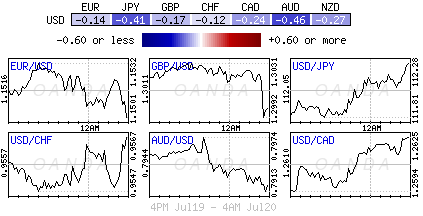

Thursday July 20: Five things the markets are talking about

Investors are trying to calculate whether company earnings will be strong enough to warrant such lofty equity prices, and if their own domestic economies can handle higher interest rates.

Overnight, the Bank of Japan (BoJ) pushed back its forecast for reaching +2% inflation while keeping its policy settings on hold (see below), further highlighting Japan's struggle to achieve stable price growth. The next clues come from the ECB's policy rate announcement this morning (07:45 am EST).

The market is not expecting any changes from the ECB interest rate policy, but is looking for any signs of the outlook for the bank's quantitative easing (QE).

Its +€60B a month asset program expires at the end of the year and everyone wants to know what comes next. An announcement regarding the next steps is more likely in September when Euro policy makers will also release their new macro-economic projections, however, ECB's Draghi may provide further insight at today's press conference (08:30 am EST).

The not so 'mighty' dollar continues to trade atop of its 10-month low as the U.S health-care reform bill crashed this week, casting further doubt on President Trump's policy agenda.

The pound is under pressure following this week's demise on yesterday's disappointing U.K inflation print, while the Aussie dollar strengthens on the go-to 'carry' trade and overnight job numbers (+14K). Global bond prices have weakened, while gold and oil trade lower.

1. Stocks get the green light

Stateside yesterday, stocks continued their rally; bypassing the markets concerns on timely implementation of U.S economic reform policies. The Nasdaq and S&P hit new all-time highs. This momentum was carried through to Asia and Europe.

Note: investor volume is lagging again for the NYSE, -17% below its three-month average, while the Nasdaq volumes remain in line. The VIX index continues to fall, dropping -2%, to 9.70 Wednesday.

In Japan, the Nikkei ended +0.6% higher, while the broader Topix rose +0.7%, its highest closing level since August 2015.

In Hong Kong, stocks finished higher for a ninth straight session, its longest winning streak since April 2015, as technology stocks powered through. The benchmark Hang Seng index ended up +0.3%, its highest level since June 2015. The Hang Seng China Enterprises Index was -0.1% lower.

In China, their major stock indexes rose for a third consecutive day, led by the blue-chip CSI300 index reaching a fresh 18-month high (+0.5%), with sentiment lifted by expectations of robust first-half corporate earnings. The Shanghai Composite Index added +0.4%.

In Europe, most indices trade modestly higher, led by the DAX. Corporate earnings and the ECB are expected to set the tone for their afternoon session.

U.S stocks are set to open little changed.

Indices: Stoxx600 +0.2% at 368, FTSE +0.4% at 7457, DAX +0.4% at 12506, CAC-40 +0.3% at 5233, IBEX-35 flat at 10590, FTSE MIB flat at 21481, SMI -0.1% at 9018, S&P 500 Futures flat

2. Oil steady after big drop in U.S. fuel stocks, gold lower

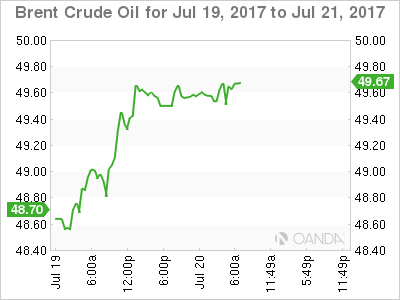

Oil prices are holding steady ahead of the U.S open, hanging on to yesterday's gains when falling U.S crude inventories supported the market.

Note: Crude oil prices are still capped below the psychological $50-per-barrel mark on concerns about high production from the OPEC despite its pledge to cut output along with some other producers.

Brent crude futures is at +$49.68 per barrel, just -2c down from yesterday's close, while U.S West Texas Intermediate (WTI) crude futures are at +$47.09 per barrel, -3c below their last nights close.

Prices for both crudes jumped more than +1.5% in yesterday's session after the EIA's report showed U.S crude and fuel stocks fell last week.

Note: U.S crude inventories dropped by -4.7m barrels in the week to July 14, against the markets expectations for a decrease of -3.2m barrels. Inventories still remain near the upper half of the average for this time of the year.

Crude 'bears' believe that climbing U.S output and high inventories, as well as the increased production from some OPEC members, will prevent prices from rising much further.

Gold prices are a tad lower ahead of the ECB meeting; a stronger USD is weighing on the precious metal. Spot gold has fallen -0.2% to +$1,237.86 per ounce.

3. Yields back up to flatten some Central Bank Curves

The Bank of Japan (BoJ) left its policy steady (as expected). The Interest Rate on Excess Reserves (IOER) was unchanged at -0.10%. Governor Kuroda and fellow policy makers maintained their policy framework of 'QQE with Yield Control (YCC) ' with 10-year JGB's yield around +0% and annual pace of QE at ¥80T.

The vote again was 7-2 and their outlook had the BoJ again delaying reaching their desired +2% inflation target by another year, pushing it out to 2019 from 2018 – its now the sixth such delay in achieving the target.

Elsewhere, U.S Treasuries have lost some ground given the markets interest in equities. Yields have firmed across the U.S curve, which continues to flatten. The benchmark 10's has backed up +1bps to +2.27%, with 30-year yield unchanged and the 10/30s spread flattening by -1bp to +58.

New supply is also providing some pressure this week – new government bond sales in Germany and the U.K, along with U.S corporate debt issuance have also put some selling pressure on Treasuries. Germany's 10-year yield has rallied +1 bps to +0.55%, the first advance in a week, while U.K 10-year Gilt yield has backed up +2 bps to +1.212%.

4. Dollar direction depends on ECB rhetoric

EUR/USD (€1.1502) continues to hover near its recent high this week on hopes of an ECB tapering hint this morning, which could lay the groundwork for an autumn policy shift. The recent run-up in investors 'long' EUR currency positions will be scaled back aggressively if ECB's Draghi is less hawkish than expected. First round of support appears at €1.1475 and then €1.1440.

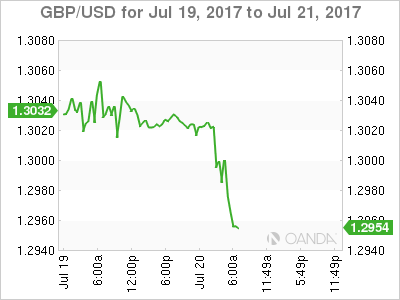

GBP/USD (£1.2960) was soft ahead of U.K retail sales numbers this morning (see below) after yesterday's lower than expected U.K inflation print. Despite sales rebounding in Q2, the pound has been unable to gain any traction. Sterling remains weak due to Brexit uncertainty.

Note: U.K data has been very volatile recently with +1-2% monthly rises and falls have become the new norm, making it difficult to determine an underlying trend.

USD/JPY (¥112.35) is fractionally higher following the BoJ's post-rate decision press conference as Governor Kuroda again reiterated his pledged do more 'easing' if necessary.

5. U.K Retail Sales Rebounded in Q2

U.K retail sales rebounded in Q2, growing +1.5%, a gain that is expected to contribute an approximate +0.09% to Q2 GDP growth.

Note: Retail sales were a drag on growth in Q1, shrinking -1.4%.

Digging deeper, sales were driven by spending in drug stores and on computers, sporting equipment and furnishings; food stores saw sales volumes increase only modestly amid rising prices.

The market is expecting a stronger contribution to growth from business investment and exports as the U.K consumer struggles with higher inflation and inadequate wage growth.

DAX Gains Ground Ahead Of ECB Decision

The DAX index has posted gains in the Thursday session. Currently, the DAX is trading at 12,497.00, up 45% on the day. Currently, the index is trading at 5187.80, up 0.29% on the day. In economic news, today's highlight is the monthly ECB policy meeting. There was positive news from German and eurozone indicators. German PPI improved to 0.0%, above the estimate of -0.1%. The eurozone current surplus jumped to EUR 30.1 billion, well above the estimate of EUR 23.3 billion.

The ECB is on center stage on Thursday, as ECB members meet for the monthly policy meeting. The bank is expected to hold rates at 0.00%, where it has pegged since March 2016. Analysts will be keeping a close eye on the rate statement, as well as Mario Draghi's press conference, which has been known to shake up the markets. With the eurozone economy showing improvement in 2017, there is some pressure on policymakers to tighten monetary policy. In December 2016, the bank tapered QE while extending the scheme until December, and this type of scenario could be adopted once again. Will the bank make a similar move at this meeting? As OANDA Senior Currency Analyst Craig Erlam explains, we're unlikely to see any moves today, but the markets are casting a glance ahead to the September meeting:

While we're not expecting any changes from the ECB today, it's €60 billion a month asset program expires at the end of the year and traders are looking for clues regarding what comes next. An announcement on this is unlikely until September when it releases its new macro-economic projections but Mario Draghi may offer some insight into what we can expect during the press conference.

The most likely decision, despite the central bank still falling well short of its inflation target, will be to cut its purchases by another €20 billion as it did in April and extend by another six months. There has been a lot of speculation about a more explicit phasing out but I think the ECB want to be more careful given the fragile nature of the recovery. The result will likely be the same though with the central bank ending its quantitative easing program either at the end of 2018 or early 2019.

It's been another brutal week for the Trump administration, which is sorely in need of a legislative victory in Capitol Hill. One of Trump's flagship projects has been replacing Obamacare, but that goal may have been dashed this week. Trump's health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility and popularity will take another hit if he's unable to produce. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

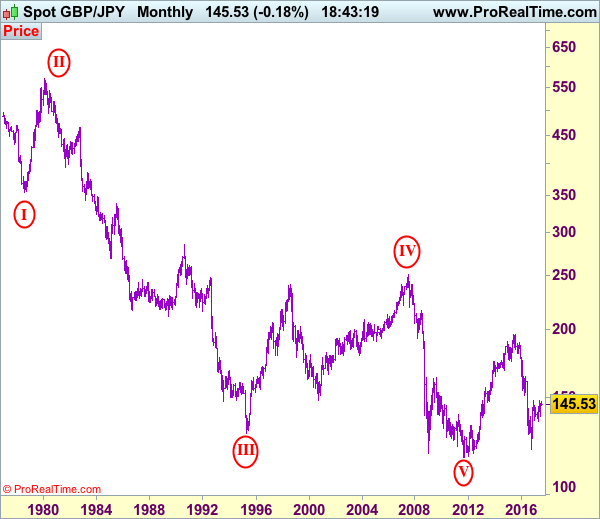

GBP/JPY Elliott Wave Analysis

GBP/JPY – 145.55

GBP/JPY – Wave 5 as well as wave (III) has possibly ended at 116.85

As stealing has retreated after faltering below last week’s high at 147.75, suggesting 1-2 weeks of consolidation below this level would be seen and mild downside bias is for weakness to 144.50, then 144.00, however, break of 143.25-30 is needed two signal the rebound from 138.70 has ended at 147.75 and bring at least a retracement of this rise to 142.50 (previous resistance), then 142.00 but price should stay well above 140.00, bring rebound later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

On the upside, whilst recovery to 146.00 and then 146.50 cannot be ruled out, reckon 147.00 would cap upside and bring another retreat. Only break of said resistance at 147.765 would revive bullishness and bring test of previous chart resistance at 148.10, break there would signal early rise from 135.60 (this year’s low) has resumed for gain to 148.45 (another previous resistance) and later 149.00-10 but price should falter below psychological level at 150.00, bring retreat late.

Recommendation: Sell at 146.50 for 144.50 with stop above 147.50.

The long-term downtrend from 570.99 (29 Feb 1980) is labeled as an impulsive wave with III with circle ended at 129.77 (20 Apr 1995) and the corrective rebound to 251.12 (20 Jul 2007) is treated as wave IV with circle and the wave V with circle selloff from 251.12 has possibly ended at 116.80 (almost reached our indicated target at 116.00) and major correction has commenced from there and indicated upside target at 183.90-00 (50% Fibonacci retracement of 251.10-116.85) had been met, reckon upside would be limited to 199.80-90 (61.8% Fibonacci retracement) and bring wave (V) decline in later part of 2017.

Euro Jumpy Ahead Of ECB Meeting

The euro has posted small losses in the Thursday session. Currently, EUR/USD is trading at the 1.15 line. On the release front, German PPI improved to 0.0%, above the estimate of -0.1%. The eurozone current surplus jumped to EUR 30.1 billion, well above the estimate of EUR 23.3 billion. Later in the day, the ECB meets for a policy meeting. In the US, there are two key events. Unemployment claims is expected to edge lower to 245 thousand, and Philly Fed Manufacturing Index is forecast to slip to 23.4 points.

All eyes are on the ECB, which will release a rate statement, followed by a press conference with Mario Draghi. In December 2016, the bank tapered QE while extending the scheme until December, and this type of scenario could be adopted once again. Will the bank make a similar move at this meeting? OANDA Senior Currency Analyst Craig Erlam explains that we're unlikely to see any moves today, but the markets are casting a glance ahead to the September meeting:

While we're not expecting any changes from the ECB today, it's €60 billion a month asset program expires at the end of the year and traders are looking for clues regarding what comes next. An announcement on this is unlikely until September when it releases its new macro-economic projections but Mario Draghi may offer some insight into what we can expect during the press conference.

The most likely decision, despite the central bank still falling well short of its inflation target, will be to cut its purchases by another €20 billion as it did in April and extend by another six months. There has been a lot of speculation about a more explicit phasing out but I think the ECB want to be more careful given the fragile nature of the recovery. The result will likely be the same though with the central bank ending its quantitative easing program either at the end of 2018 or early 2019.

President Trump hasn't done very well at learning how to tango with Congress, and this week's debacle on Capitol Hill could make the gap between Trump and Republican lawmakers even harder to bridge. Trump had vowed to replace Obamacare, but his health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

Market Update – European Session: ECB Seen Keeping Policy Steady But Could Lay Out The Groundwork For An Autumn...

Notes/Observations

ECB is the main event of the day but not expected to provide concrete steps in the direction of a monetary policy; could lay the groundwork for an autumn policy shift

BoJ kept its policy steady (as expected) but again pushed back the timing for reaching its 2% inflation target to FY2019 (**Note: 6th such delay in achieving the CPI target)

UK Jun Retail sales data beats expectations aided by warm weather

Overnight

Asia:

Bank of Japan (BOJ) left its policy steady (as expected). Interest Rate on Excess Reserves (IOER) unchanged at -0.10%; maintained its policy framework of "QQE with Yield Control (YCC) " with 10-year JGB yield around 0% and annual pace of QE at 80T. Vote again 7-2. Outlook had BOJ again delayed reaching 2% inflation target to ~FY19 from ~FY18 (6th such delay in achieving the target)

Australia Jun Employment saw its 4th consecutive increase (+14.0K v +15.0Ke); Unemployment Rate in-line at 5.6%

China FX Regulator SAFE: Fund flows situation stabilized and improved in H1. Impact of US hike on Chinese cross border capital flows has diminished; forex supply and demand basically balanced since Feb. H1 forex sale ratio declined 'significantly'. H1 capital flows were the most balanced in 3 years

Chinese Embassy in Washington: US/China acknowledged significant progress on 100 day action plan for trade; discussed 1 year action plan on economic cooperation

US Treasury: China acknowledged shared objectives of reducing our US trade deficit

Europe:

Germany Finance Ministry Monthly Report noted that indicators suggested 'lively' economic upswing in Q2 with quarterly GDP seen around 0.6%

PM May: Brexit negotiating position is as good as it was pre-election. No such thing as an un-sackable minister, but the team is together at the moment

Americas:

US Trade Rep: first round of NAFTA talks to take place in Washington DC between Aug 16-20th (**Note: Said to be planning for seven rounds of NAFTA talks, taking place at three-week intervals)

Brazil govt reportedly mulling higher gasoline taxes to help reach budget target. Could hike federal VAT on gasoline

Energy:

Iraq Oil Min: reiterates Iraq plans to raise oil output to 5M bpd by end of year

Economic Data

(NL) Netherlands Jun Unemployment Rate: 4.9% v 5.1% prior

(NL) Netherlands July Consumer Confidence: 25 v 23 prior

(DE) Germany Jun PPI M/M: 0.0% v -0.1%e; Y/Y: 2.4% v 2.3%e

(CH) Swiss Jun Trade Balance (CHF): 2.8B v 3.4B prior; Real Exports M/M: -1.9% v +3.7 prior; Real Imports M/M: -0.5% v +1.4% prior

(TW) Taiwan Jun Export Orders Y/Y: 13.0% v 7.0%

(UK) Jun Retail Sales (Ex Auto Fuel) M/M: 0.9% v +0.5%e; Y/Y:3.0% v 2.5%e

(UK) Jun Retail Sales (including Auto Fuel) M/M: 0.6% v +0.4%e; Y/Y: 2.9% v 2.5%e

(HK) Hong Kong Jun CPI Composite Y/Y: 1.9% v 2.1%e

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.58B vs. €4.0-5.0B indicated range in 2021, 2022 and 2027 SPGB bonds

Sold €0.7B in 0.05% 2021 bonds; Avg yield: 0.026% v +0.021% prior, Bid-to-cover: 3.68x v 1.96x prior

Sold €1.29B in 0.40% 2022 bonds; Avg yield: 0.314% v 0.337% prior; Bid-to-cover: 3.42x v 2.26x prior

Sold €2.59B in 1.45% 2027 bonds; Avg yield: 1.649% v 1.395% prior; Bid-to-cover: 1.23x v 1.78x prior

(FR) France Debt Agency (AFT) sold total € vs. €6.5-7.5B indicated range in 2020 and 2022 Oats (3 tranches)

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.2% at 368, FTSE +0.4% at 7457, DAX +0.4% at 12506, CAC-40 +0.3% at 5233, IBEX-35 flat at 10590, FTSE MIB flat at 21481, SMI -0.1% at 9018, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trade modestly higher across the board led by the Dax, following another record high close in US Indices overnight.

Corporate earnings continued with notable earnings from SAP, ABB and Publicis this morning. Easyjet trades lower after announcing relatively strong results but ticket price pressures in H2 weigh on the stock, whilst the overall airline sector trades lower led by Lufthansa. Elsewhere Unilever reported a boost in profits helped by cutting costs faster then expected.

Looking ahead to the US morning notable earner include Danaher, Abbot Labs and BB&T.

Equities

Consumer discretionary [Givaudan [GIVN.CH] -1.7% (Earnings), Easyjet [EZJ.UK] -5.5% (Earnings), Sports Direct +6.8% (Earnings), Zooplus [ZO1.DE] -10% (Earnings), Publicis [PUB.FR] 2.5% (Earnings), Remy Cointreau [REMY.FR] -2.0% (Earnings), - Luftanhsa [LHA.DE] -6.5%, Int Con Airlines [IAG.UK] -2.9% , Air France [AF.FR] -4.5% (Sector move), Unilver [UNA.NL] +0.6% (Earnings)]

Industrials: [ABB [ABBN.CH] -3.3% (Earnings), Saab [SAABB.SE] -4% (Earnings)]

Technology: [Moneysupermarket [MONY.UK] -7% (Earnings), Ingenico +8% (Earnings, Acquistion)]

Speakers

Germany Chemical Industry Group (VCI) raised 2017 production and revenue forecasts; expects positive business to continue in H2

Turkey Presidential advisor Ertem reiterated govt view that high interest rates in country were unsustainable

BOJ Gov Kuroda post rate decision press conference reiterated that virtuous economic cycle was working; risks to prices and economy were tilted to the downside. To continue with powerful easing. Japan was no longer in a state of falling prices but have yet to achieve the 2% target. FY19/20 GDP growth to slow slightly due to Capex and schedule 2nd phase of planned sales tax hike. Had implemented the necessary policies to achieve the 2% inflation target but reiterated view to adjust monetary policy as needed to maintain momentum towards price target. Yield control was a sustainable policy framework that allowed the central bank to flexibly respond to economy and prices

Australia PM Turnball said to warn borrowers about potential rate rise as RBA sending a signal which is probably prudent

Thailand Central Bank Gov Veerathai: Strong THB currency (Baht) due to concerns over US economic and political situation

Currencies

ECB decision and press conference seen as the main event of the day. The General Council was not expected to provide concrete steps in the direction of a monetary policy turnaround. EUR/USD hovered near recent high on hopes of an ECB tapering hint which could lay the groundwork for an autumn policy shift. The recent run-up in the EUR currency positions could be scaled back if markets think the ECB was less hawkish than expected. EUR/USD holding above 1.15 level.

GBP/USD was softer heading into the session over concerns about the pending retail sales data. GBP/USD dipped below the 1.30 handle. In recent months higher inflation coupled with weaker nominal earnings suggested a squeeze on real income, which in turn may weigh on consumption. Today.s data was an upside surprise and helped the GBP/USD regain a foothold above the 1.30 area.

USD/JPY was fractionally higher following the BOJ post-rate decision press conference as Kuroda reiterated his pledged it would do more easing if necessary. The perpetual BOJ dissenters (Kiuchi and Sato) participated in their last meeting and to be replaced by likely-pro-Kuroda cheerleaders.

Fixed Income

Bund futures trade at 161.72 down 9 ticks as riskier assets rally from the European open. Resistance lies near the 162.10 level followed by 162.75. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 126.22 lower by 16 ticks following the better than expected UK retail sales. Price finds key support at the 125.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.72 region, followed by 127.50.

Thursday’s liquidity report showed Wednesday’s excess liquidity fell sharply to €1.647T a drop of €9B from €1.656T. Use of the marginal lending facility rose to €208M from €111M prior.

Corporate issuance saw $13.3B come to market via 4 issuers headlined by Goldman Sachs $3.5B 3-part senior note self-led offering and Morgan Stanley $7B senior unsecured benchmark notes

Looking Ahead

(ID) Indonesia Central Bank (BI) Interest Rate Decision: Expected to leave Reverse Repo Rate unchanged at 4.75%

(PT) Portugal May Current Account: No est v €0.2B prior

05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds (3 tranches)

05:50 France Debt Agency (AFT) to sell €1.25-1.75B in 2027, 2028 and 2047 I/L Oats (Oatei)

06:00 (IL) Israel May Manufacturing Production M/M: No est v 1.9% prior

06:00 (RO) Romania to sell 6-month Bills

07:45 (EU) ECB Interest Rate Decision: Expected to keep all Key Rates unchanged

08:00 (BR) Brazil July IBGE Inflation IPCA-15 M/M: -0.1%e v +0.2% prior; Y/Y: 2.9%e v 3.5% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 245Ke v 247K prior; Continuing Claims: 1.95Me v 1.945M prior

08:30 (US) July Philadelphia Fed Business Outlook: 23.7e v 27.6 prior

08:30 (EU) ECB chief Draghi post rate decision press conference

09:00 (RU) Russia Gold and Forex Reserve w/e July 14th: No est v $410.9B prior

09:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to leave Interest Rtes unchanged at 7.00%

10:00 (US) Jun Leading Index: 0.4%e v 0.3% prior

10:00 (EU) Euro Zone July Advance Consumer Confidence: -1.2e v -1.3 prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (BR) Brazil to sell Fixed Rate 2027 Bonds

11:00 (BR) Brazil to sell 2018, 2019 and 2020 LTN Bills

13:00 (US) Treasury to sell 10-Year TIPS

15:00 (MX) Mexico Citibanamex Survey of Economist

EUR/USD Analysis: Retreats As Expected

The common European currency has consolidated its gains against the US Dollar, as the currency exchange rate had retreated down to the 1.1510 mark on Thursday morning. During the decline the pair had begun to trade in limbo around the weekly R1, which is located at the 1.1516 level. The pair was not continuing the retreat due to the fact that additional support was approaching. The 100-hour SMA was located at the 1.1499 level, and it was approaching the pair from the downside. There are two possible outcomes to the situation. However, one of them is more likely. As the pair has bounced off the resistance of a massive scale pattern, it is likely going to decline. In addition to that, below the 100-hour SMA there is an almost 50 base points large range free from any type of notable support levels.

GBP/USD Analysis: Fluctuates Around Weekly PP

Thursday's trading session the currency pair started in a sluggish horizontal movement, being squeezed between the 55- and 100-hour SMAs from the top and the weekly PP at 1.3008 from the bottom. In anticipation of a release of the UK Retail Sales at 8:30 GMT the Pound fell below the above support level towards the 200-hour SMA. But since the data appeared to be better than analysts expected, the pair made a u-turn and started a steady recovery. Accordingly, the second half of the day the rate is expected to spend in attempts to break through the above resistance level, which will be supplemented also by the 20-hour SMA. This scenario is supported by a number of technical indicators, which point out that the pair is oversold.

USD/JPY Analysis: Breaks From Falling Wedge

In line with expectations, the currency pair bounced off from a lower support line near the 111.596 mark and left a falling wedge in an upward direction, bypassing on the way the 20-, 55- and 100-hour SMAs. Such outcome should establish a new uptrend, which will guide movement of the pair at least in next two days. However, for this theory to be true, the currency exchange rate has to bypass two combined resistance levels. The first is formed by the 200-hour SMA and the weekly PP at 113.098, while the second is set up by the weekly and monthly R1 at 113.940. Most probably, one of them will manage to turn around the currency rate, provided that this will not happen even earlier.

XAU/USD Analysis: Moves In Accordance With Pattern

The bullion's price continues to move in accordance with the discovered patterns. On Thursday morning the commodity price decline to trade below the resistance of the 55-hour SMA, which was located at the 1,240 mark. The metal was making attempts to regain lost ground during the morning hours of the session. However, in accordance with the ascending channel pattern, in which the metal trades, the bullion is set to decline down to the support line of the mentioned pattern. Before that occurs the commodity price might face the support of the 100-hour SMA, which on Thursday was located near the 1,235 mark. Meanwhile, down to the just mentioned simple moving average there are no other support levels, which creates a free range of almost 500 base points.

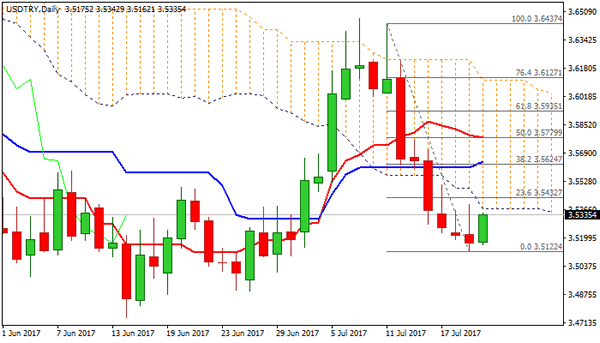

Technical Outlook: USDTRY – Limited Correction Seen Ahead Of Fresh Downside

The pair bounces on Thursday after bear-leg from 3.6437 (07 July high) hit fresh three-week low at 3.5122 on Wednesday, failing so far to clearly penetrate weekly cloud (cloud top lies at 3.5340).

Falling thick daily cloud continues to weigh (cloud base lies at 3.5371), seeing risk of limited recovery before broader bears resume.

However, strong bullish signal is developing on reversal of deeply oversold slow stochastic on daily chart, which may trigger stronger correction. Penetration into daily cloud would open next 3.5472 (converged 20/55SMA in attempt to form bear-cross) and expose 3.5624 (Fibo 38.2% of 3.6437/3.5122 / daily Kijun-sen).

Sustained break here is needed to sideline bears and signal stronger correction.

Otherwise, early recovery rejection (ideally under daily cloud) would keep immediate risk at the downside.

Firm break through weekly cloud top would open 3.4837 (200SMA) and risk bearish extension towards weekly cloud base at 3.3633, as continuation of broader bear-phase from record high at 3.9414 (11 Jan high).

Res: 3.5371, 3.5472, 3.5624, 3.5780

Sup: 3.5255, 3.5122, 3.5000, 3.4837