Sample Category Title

Draghi sends USD higher in face of soft US data | DXY, USDJPY

Despite weak data from thr US, it was dovish comments from Draghi and hawkish comments from the Fed which helped lift the Dollar.

Speaking to students in Lisbon, Draghi once again lowered expectations of ECB tightening to send the Euro lower and support the Greenback. This helped to erase losses seen from weak durable goods and manufacturing data, which was extended further once Fed members continued their hawkish commentary.

Durable goods and manufacturing sentiment added to the long list of weak data from the US, to weight on the Greenback despite further hawkish comments from Fed members. Durable goods declined -1.1% compared with -0.8% prior and -0.6% expected. This makes it the 2nd month of contraction which has helped drag the YoY rate to just 2.7%. Excluding transportation durable goods managed to squeeze a 0.1% expansion in June, yet does not quite claw back the -0.5% contraction in May. The YoY% rate however is at a slightly heathier level of 5.5% and the underlying index is just below 3 year highs.

GDP data for Q1 will be revised this week, although the real concern going forward is that data so far for Q3 is also below par and leading sentiment indicators aren't reviving hopes of a rebound. If we continue to see PMI surveys soften and hard data such as durable goods, inflation or growth struggle to rebound then it essentially kills off any need for the Fed to raise. Markit PMI data also disappointed on Friday and these reads can lead the rise of fall of GDP by 6-12 months on average.

For the foreseeable future, we doubt the US Dollar Index will be able to break out of the 96.50 - 97.88 range. Whilst the Fed continue with their hawkish narrative to help support the Dollar, the data which is presented prevents it from breaking higher. This also means we doubt we'll see significant trends develop unless we see either of these opposing forces switch to the other's side (dovish fed with weak data, or hawkish fed with strong data).

D1 closed with a bullish piercing pattern to warn of near-term strength, although at current levels the rewards to risk ratio may be undesirable to trade D1 as we are too close to the monthly pivot (black line). Moreover, the rally from the bullish pinback may be part of a correction higher which also limits the potential upside form here. So, we may want to monitor for signs of weakness below 97.881 to aid timing a long position on EURUSD. An alternative scenario (and least favoured under the current climate) I for an inverted head and shoulders pattern to materialise. We would need to see a form close above 97.88 (neckline) and if successful it projects an approximate target around 99.50.

A more bullish scenario appears to be forming with USDJPY. We highlighted the minor pullback above 11080 last week and we have now seen a bullish follow-through. If we can clear the 112.10 resistance level then we find ourselves in an area which has relatively little in the way of resistance towards the 114.38 target. If we are to see a decent close above 112.10 then the odds of a direct rally towards target is increased. Yet if we are to falter around current levels and return to 110.80, then we must consider a deeper pullback and frustratingly slower journey towards the eventual target.

CRUDE OIL – Builds Up On Bull Recovery

CRUDE OIL - The commodity continues to retain its upside pressure on correction. On the downside, support resides at the 43.00 level where a break will expose the 42.50 level. A cut through here will set the stage for a run at the 42.00 level. Further down, support resides at the 41.50 level. Its daily RSI is bullish and pointing higher suggesting further strength. On the upside, resistance resides at the 44.00 level. Further out, resistance comes in at the 44.50 level. A break above here will aim at the 45.00 level and then the 45.50 level followed by the 46.00 level. All in all, CRUDE OIL remains biased to the upside on further strength.

A Slow Burn

A Slow Burn

Slow start to the week for markets with so many countries out on holiday (on account of Eid or local holidays), As well, investors remain extremely tentative ahead of this week’s star-studded cast of central bankers hitting the airwaves. In addition to the ECB Forum (the equivalent to Jackson-Hole schmooze fest ) being held in Sintra, Portugal this week., Dr Yellen makes an appearance in London later today. But despite the plethora of central bankers on tap, it’s unlikely there will be any revelations on monetary policy forthcoming.And given the proximity to the recent FOMC, there will certainly be no backpedalling from Dr Yellen. However, the week could turn interesting, yet highly inconclusive, as currency markets get knocked to and fro driven by month/quarter/half year end flows this week, so best not to bring out the summer desk pillow just yet.

While it’s difficult to put much trust in current price action ( using overnight Gold price as an example) risk sentiment seems improved. And with few negatives hitting the airwaves, dealers were left to assume the age-old adage of no news is good news. Equities are trading in the green ever so slightly, oil prices are moving higher, and FX has followed correspondingly

Japanese Yen

The beneficiary of the positive shift in risk sentiment is the USDJPY which has been trading in sympathy with Oil and equities. With the price of oil back from the dead, it provided the overnight fillip for the dollar-yen bulls. After a slow burn higher throughout the NY morning, an afternoon NY gap took out the 110.80 level (100 days moving average), and the markets are now within striking distance of the psychological 112.00 level. With the JPY crosses trading well, a push higher looks in the cards.

British Pound

The pound appears to have returned to its post-election happy valley between 1.2700-1.2750 although the markets have quite been quiet with volumes well below average. Even a new deal with Northern Ireland’s DUP party failed to animate. It seems that any optimism remains short lived these days, after all, that’s to rejoice about the possibility of another election and ongoing Brexit uncertainty. Not to mention rising inflation, weak wage growth and a negative shift in recent economic data is hardly a confidence builder for the Pound

Australian Dollar

The Australian dollar is firmer on the back of higher Iron ore and oil prices. The uptick in oil prices has buoyed risk sentiment, and global investors are expressing some pockets, small mind you, of interest in both commodity based and higher yielding currencies overnight. Despite the positive risk vibe, there will likely be some hesitation to breach the .7600 level with Dr Yellen on tap as there’s little chance of policy back peddling and if anything she may reaffirm her for FOMC hawkish view.

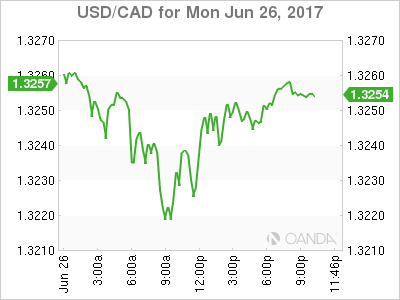

USD/CAD Canadian Dollar Higher After US Durable Goods Disappoint

The Canadian dollar started the week gaining versus the US dollar. The comments from Bank of Canada (BoC) policy makers on June 11 had pushed the loonie higher against the greenback, but the Fed turned up the rhetoric last week to even things out. Fed members were mixed in their endorsement/criticism of the aggressive rate hike path, but most were in agreement that the central bank needs to start shrinking its massive balance sheet. The trillions of dollars which were accumulated as part of the Fed's quantitive easing program and are still in the books of the CB need to be sold in a gradual manner for true normalization to be achieved.

The week started with few economic indicators to guide the market. New orders for US durable goods in May fell by 1.1 percent month to month, removing transportation items also disappointed with a 0.1 percent gain when 0.4 percent was expected. Second quarter growth has proven sluggish and the durable goods data hit the USD to the downside. The main champion for the dollar has been the Fed and this week there will be plenty of fedspeak to digest with three Federal Open Market Committee (FOMC) members due to speak on Tuesday.

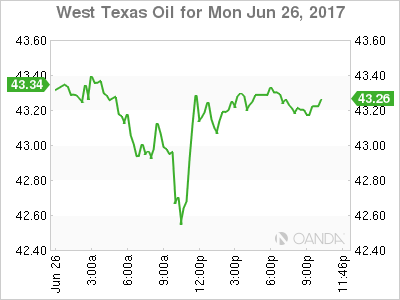

Oil prices are higher on the North American session than last week. This all could change with the release of the US crude inventories on Wednesday at 10:30 am EDT. The OPEC oil production cut agreement has failed to spark a rally in energy prices when US and other non-agreement producers are ramping up their supply keeping the crude glut in place.

The USD/CAD lost 0.253 percent in the last 24 hours. The currency pair is trading at 1.3237 after a disappointing US durable goods number early on Monday. The final reading of the US second quarter GDP will be released on Thursday, June 28 at 8:30 am EDT with growth now expected to be lower than the 1.2 percent gain reported last month.

Bank of Canada (BoC) Governor Stephen Poloz will be in Europe this week to attend the European Central Bank (ECB) Forum in Portugal. He will be joined in a panel by the heads of the Bank of England (BoE), Bank of Japan (BOJ) and the host. At this stage the BOJ stands apart as the other have made hawkish statements about their respective economies being on the mend with rate hikes and end of QE programs to start this year. In Canada the comments from Deputy Governor Carolyn Wilkins in Winnipeg put a rate hike firmly on the table for this year. The weak inflation data on Friday is not expected to derail an upcoming hike, but it could have pushed it further back towards the fourth quarter or later.

Crude gained 0.799 percent in the last 24 hours. West Texas Intermediate is trading at $43.27 near daily highs after a slow start to the week. Energy prices managed to trade above the $43 price line awaiting the weekly inventory data that tells the score between the Organization of the Petroleum Exporting Countries (OPEC) production cuts and the US ramp up of supply.

Energy prices touched 7 month lows last week and market sentiment is expecting another drop, specially if inventories of crude or gasoline in the US show another large buildup. US production has grown by about 10 percent with Brazil and Canada also increasing output, while the OPEC is now considering further cuts to keep prices from falling further.

Market events to watch this week:

Tuesday, June 27

10:00 am USD CB Consumer Confidence

Wednesday, June 28

10:30 am USD Crude Oil Inventories

Thursday, June 29

8:30 am USD Final GDP q/q

8:30 am USD Unemployment Claims

Friday, June 30

4:30 am GBP Current Account

8:30 am CAD GDP m/m

Pound Inches Upwards, PM May Secures DUP Support

The British pound has started the trading week quietly. In North American trade, GBP/USD has ticked higher and is trading at 1.2730. On the release front, British BBA Mortgage Approvals dipped to 40.3 thousand, matching the forecast. In the US, durable goods orders missed expectations, disappointing the markets. Core Durable Goods came in at 0.1%, missing the forecast of 0.4%. Durable Goods Orders declined 1.1%, short of the forecast of -0.5%. On Tuesday, we’ll get a look at CB Consumer Confidence and Fed Chair Janet Yellen will speak at an event in London.

It’s been a rough few weeks for British Prime Minister Theresa May, who suffered a major setback in the recent election, as she lost her majority in parliament. May has had to deal with domestic critics, some who have been blistering in their attacks on her poor performance in the election. With the Brexit talks finally underway, May has to deal with European leaders who are unhappy with Britain ditching their club. There was finally some good news on Monday for the embattled May, who reached an agreement with the DUP, a small Irish party. The DUP will not formally enter the government, but has committed to support the government on its legislative agenda, Brexit and the budget. In return, May will provide Northern Ireland with an additional one billion pounds over the next two years. The deal should provide May with some breathing room in parliament, allowing her to shift gears from damage control and focus on the economy and the Brexit negotiations.

There was positive news last week from the US construction industry. On Friday, New Home Sales jumped to 610 thousand, above the forecast of 599 thousand. Earlier in the week, Existing Home Sales improved to 5.62 million, beating the estimate of 5.54 million. There had been concerns about construction numbers, as Building Permits and Housing Starts both missed expectations in the May releases. Later in the week, the economy receives a report card, with the release of Final GDP for the first quarter. Preliminary GDP, which was released in May, came in at 1.2%, and this is the forecast for Final GDP. Will weak inflation and consumer spending result in a weaker than expected GDP report? If so, the US dollar could be a casualty and lose ground against its rivals.

Bearish Trend In Oil

Due to the jack of all trades nature of my role, I didn't manage to get my forex daily market update blog published yesterday. As a result, here it is today!

If you haven't noticed when you've gone to fill up your car at the local petrol station, petrol is cheap! Since we featured the following daily resistance zone, a lot has changed.

So let's take another look at oil:

Oil Daily:

As I'm sure you're aware, each market essentially has its own different personality when it comes to the way that price moves between support and resistance levels. When commodities markets like oil trend, they tend to REALLY trend. Just take a look at that last little down leg (I say little in the context of the daily chart, but there's 2 months worth of candles in there) and you can see what I mean.

I've then zoomed into an intraday chart, which is in this case an hourly, to highlight the trending nature of the market. The chart looks a bit boring zoomed out as far as I have, but I needed to do this so I could show the entire move down from where price last rejected down out of the higher time frame resistance zone.

Oil Hourly:

If you're a forex trading textbook manufacturer, you're free to use this chart to highlight how price moves between levels in a perfect down trend. Here you can clearly see how short term support forms, short term support breaks and short term support is finally retested as resistance. Rinse then repeat as many times as necessary.

Yen Ticks Lower, US Durables Disappoint

USD/JPY is showing limited movement at the start of the week. The pair has posted small losses on Monday and is trading at 111.50 in North American trade. In Japan, the BoJ released its Summary of Opinions for the June policy meeting, and SPPI was unchanged at 0.7%, matching the forecast. In the US, durable goods orders were soft – Core Durable Goods came in at 0.1%, missing the forecast of 0.4%. Durable Goods Orders declined 1.1%, short of the forecast of -0.5%. On Tuesday, we'll get a look at CB Consumer Confidence and Fed Chair Janet Yellen will speak at an event in London.

The BoJ Summary of Opinions didn't contain any nuggets with regard to monetary policy, as policymakers said that inflation would likely remain at low levels for an extensive period, which meant that the bank's ultra-loose accommodative policy would stay in place until a stronger economy pushed up prices. At the same time, the board members acknowledged that it was important for the BoJ to clearly communicate its plans to the markets. In the immediate present, that meant that the markets should be discouraged from speculating that the bank would withdraw monetary stimulus anytime soon. Japan's economy has shown improvement, leading to speculation on the part of the markets that the BoJ might taper its policy, but the BoJ has reiterated that this is a non-starter before inflation moves closer to the bank's target of 2.0%.

US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Later in the week, the economy receives a report card, with the release of Final GDP for the first quarter. Preliminary GDP, which was released in May, came in at 1.2%, and this is the forecast for the upcoming GDP report. Consumer spending has also been softer than expected, and this means that Final GDP could miss expectations. If the economy falls short of this modest estimate, the dollar could respond with losses.

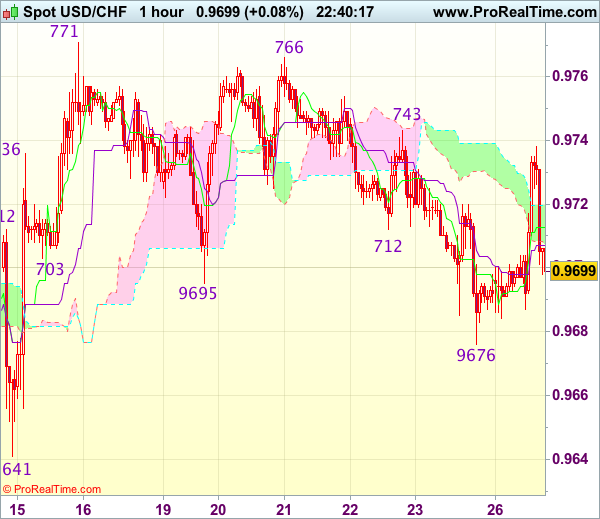

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9706

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9713

Kijun-Sen level : 0.9711

Ichimoku cloud top : 0.9715

Ichimoku cloud bottom : 0.9702

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite intra-day brief rise to 0.9738, lack of follow through buying and current retreat suggest downside risk remains and test of support at 0.9676 (Friday’s low) cannot be ruled out, break there would signal the erratic fall from 0.9771 top is still in progress for retracement of recent rise, hence further weakness to 0.9660 would be seen, however, as broad outlook remains consolidative, still reckon downside would be limited to 0.9641 support, risk from there is seen for another rise to take place later.

On the upside, expect recovery to be limited to resistance at 0.9720 and price should falter below resistance at 0.9743, bring another decline later. Only a firm break above resistance at 0.9743 would revive bullishness and signal low is formed, bring test of 0.9766-71 resistance first. Once this resistance is penetrated, this would confirm recent rise from 0.9613 low has resumed for test of resistance at 0.9808, then towards another previous resistance at 0.9825.

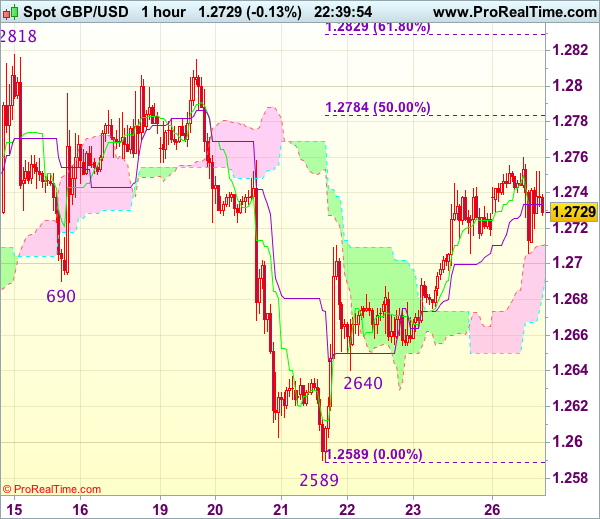

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2736

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2750

Kijun-Sen level : 1.2733

Ichimoku cloud top : 1.2699

Ichimoku cloud bottom : 1.2661

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has continued moving higher after last week’s strong rebound from 1.2589, suggesting near term upside risk remains for this move to bring retracement of recent decline to 1.2780-85 (50% Fibonacci retracement of 1.2978-1.2589), however, reckon upside would be limited to 1.2800 and price should falter below resistance at 1.2818, bring another selloff later.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below 1.2705-10 would suggest an intra-day top is formed, bring weakness towards 1.2675-80 but break of latter level is needed to signal the rebound from 1.2589 has ended, bring retest of this level later.

Dollar Falls on Durable Goods Miss; Sterling Boosted on DUP Deal; Gold Declines

The main economic releases during today's European session pertained to durable goods orders out of the US and the Ifo business sentiment survey out of Germany. Beyond these, gold experienced a considerable decline and sterling received a boost after UK Prime Minister struck a deal with Northern Ireland's Democratic Unionist Party which would support her minority government.

In US economic releases, durable goods orders fell by 1.1% in May. This negatively compares to the 0.6% drop expected and exceeds April's decline by 0.9%. The data point to a loss in momentum in the manufacturing sector during the middle of the second quarter of the year.

In terms of reaction in the forex markets to the durable goods numbers, the dollar experienced sizable losses relative to majors including the yen and the euro as the data hit the markets. Dollar/yen fell to as low as 111.35. The pair traded at 111.66 previously. Euro/dollar rose to its highest on the day, at 1.1219, shortly after the figures were released. This also marks an eleven-day high for the pair which traded at 1.1188 before the data became public.

The dollar index, a broader gauge of the US currency's strength, was down one-tenth of a percent in afternoon European trading hours. Earlier in the day, San Francisco Fed President (a non-voting FOMC member), John Williams delivered a hawkish speech during which he said "If we delay (hiking) too long, the economy will eventually overheat, causing inflation or some other problem." His talk failed to significantly lift the greenback as investors remain sceptical. The CME Group's 30-day Fed Fund futures prices are currently placing the odds of another rate hike at less than 50% during the Fed's December meeting. Dollar/yen was last up on the day, trading at 111.42. In the meantime, euro/dollar was up, above the 1.12 handle. Federal Reserve Chair Janet Yellen will be speaking tomorrow in London.

During morning European trading hours, the Ifo institute's survey gauging business sentiment in Germany, Europe's largest economy, was released. The institute's business climate index for the month of June beat expectations, rising to the all-time high of 115.1 from May's 114.6. Forecasts were for a reading of 114.5. The sub-indices measuring current business conditions and expectations for the future were also released above projections and their respective figures from the previous month. The German economy seems to be maintaining positive momentum, being helped by private consumption and dodging potential threats to growth for the time being such as Brexit developments and upcoming federal elections in September. The Ifo institute chief Clemens Fuest stated that "Sentiment among German businesses is jubilant". Despite the upbeat figures, euro/dollar edged lower, though not by much, upon immediate release of the data.

Sterling firmed up, hitting a one-week high of $1.2759 in early European session, amid the news that Theresa May was about to seal a deal with the Democratic Unionist Party, which would give her a better grip of the government. Such a deal materialized a couple of hours later. Pound/dollar eased later in the day but was last still marginally up on the day, trading at 1.2741. Relative to the euro, sterling was slightly lower in afternoon European trading, with euro/pound eyeing the 0.88 handle.

Taking a look at gold, the precious metal steeply declined as a result of a large sell order hitting the markets today. In particular, the commodity fell to the more than one-month low of $1235.84 an ounce. Reports made reference to an accidental sale with the seller trying to quickly make up for the mistake by placing long positions immediately after. The precious metal made up for a significant part of the loss but was still last trading more than 1.0% down on the day, at $1244.25 an ounce.

Looking ahead, European Central Bank President Mario Draghi is scheduled to give a speech at 17:30 GMT.