Sample Category Title

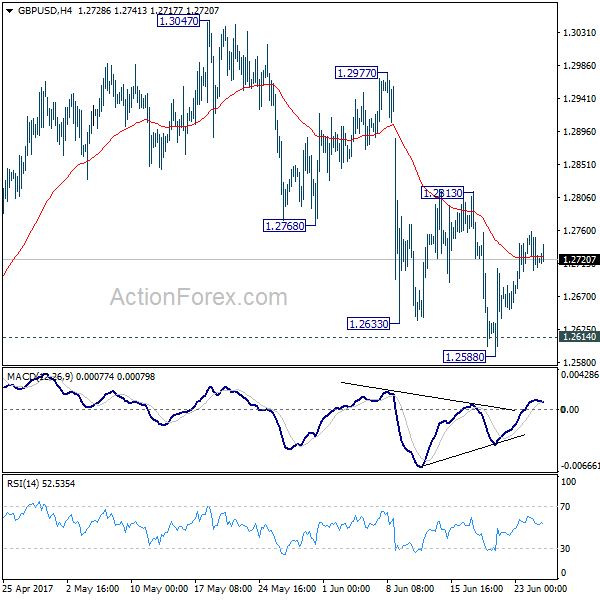

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2698; (P) 1.2728; (R1) 1.2752; More...

No change in GBP/USD's outlook as it's bounded in range of 1.2588/2813. Intraday bias stays neutral for the moment. With 1.2813 resistance intact, deeper decline is expected. Sustained break of 1.2614 resistance turned support will confirm our bearish view that consolidation pattern from 1.1946 has completed. In that case, deeper fall should be seen back to retest 1.1946 low. However, break of 1.2813 resistance will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed at 1.3047 after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

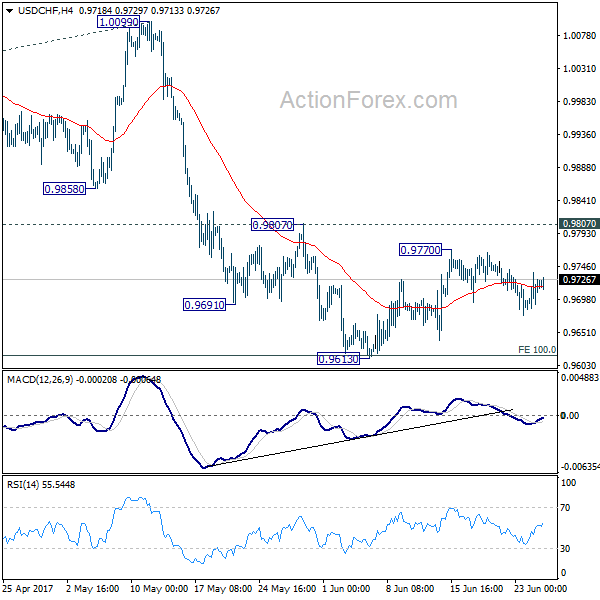

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9690; (P) 0.9714; (R1) 0.9748; More.....

No change in USD/CHF's outlook as the consolidation pattern from 0.9613 is still extending. Intraday bias stays neutral and another rise cannot be ruled out. But after all, near term outlook remains bearish as long as 0.9807 resistance holds. Break of 0.9613 will resume the decline from 1.0342 and target 0.9548 support and below. We'd start to look for bottoming signal again as it approaches 0.9443 key support level. On the upside, firm break of 0.9807 will indicate near term reversal and turn outlook bullish for 1.0099 resistance next.

In the bigger picture, USD/CHF is still bounded in medium term range of 0.9443/1.0342 for the moment. Consolidative trading would likely continue and medium term outlook remains neutral. Break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. Meanwhile, downside attempts should be contained by 0.9443 key support level. However, sustained break of 0.9443 will carry larger bearish implication and target 0.9 handle.

Market Update – Asian Session: China Premier Li Upbeat On Economic Prospects Amid Another Double-Digit Industrial Profit Growth

US Session Highlights

(US) Fed’s Dudley (dove, FOMC voter): Fed's taken very measured and careful approach to shrinking bond portfolio

(US) MAY PRELIMINARY DURABLE GOODS ORDERS: -1.1% V -0.6E (the largest drop in six months); DURABLES EX TRANSPORTATION: 0.1% V +0.4%E

(US) May Chicago Fed National Activity Index: -0.26 v +0.49 prior

(US) JUNE DALLAS FED MANUFACTURING ACTIVITY: 15.0 V 16.0E

Stocks opened the week on a positive note, spurred by a rally in Europe, as two Italian banks were saved from bankruptcy with public money and Nestle hit a new all-time high, gaining 4% on the day. Technology stocks fell out of favor, down 0.3%. Best performing sectors in the S&P were Utilities and Financials, gaining 0.8% and 0.5% respectively.

US markets on close: Dow +0.1%, S&P500 flat, Nasdaq -0.3%

Best Sector in S&P500: Utilities

Worst Sector in S&P500: Technology

Biggest gainers: FE +4.1%; EQT +3.8%; CVS +3.5%

Biggest losers: FTR -6.6%; ARNC -6.0%; QRVO -5.1%

At the close: VIX 9.9 (-0.1pts); Treasuries: 2-yr 1.36% (+1bps), 10-yr 2.14% (-1bps), 30-yr 2.70% (-2bps)

Politics

(US) Sen Collins (R-ME) to vote NO on motion to proceed on healthcare legislation - tweet

(US) CBO scores Senate Republican healthcare bill: 22 million more people uninsured by 2026

(BR) Brazil Prosecutor General Janot confirms to proceed with corruption charges against President Temer - Brazil press

Key economic data

(CN) CHINA MAY INDUSTRIAL PROFITS Y/Y: 16.7% V 14.0% PRIOR; YTD 22.7% V 24.4% PRIOR

(NZ) NEW ZEALAND MAY TRADE BALANCE (NZD): 103M (3rd straight surplus) V 419ME; 12-MONTH YTD: -3.75B V -3.39BE

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 111.8 v 112.4 prior

Asia Session Notable Observations

China Premier Li spoke at World Economic Forum, pleding to maintain policy settings amid steady growth expectations in Q2; Unemployment seen at 4.9%.

China profit growth accelerates to 16.7% from 14.0%, while Liabilities growth slows to 6.5% from 6.7% in May.

New Zealand posts 3rd straight trade surplus; Exports in line with estimates and Imports higher than expected; Shipments of Dairy spike over 40% y/y to NZ$1.2

Brazil Prosecutor confirms proceeding with corruption charges against Pres Temer.

White House notes signs of Syria preparing another chemical attack, warns Assad will pay heavy price if he proceeds.

Speakers and Press

China

(CN) China Premier Li: Economy maintaining steady growth and improving in Q2; To keep proactive fiscal policy and prudent monetary policy - World Economic Forum comments

(CN) PBOC said to be in talks with MoF on asset management tax plan

(CN) China May Lottery Sales CNY37.7B, +8.9% y/y

Japan

(JP) Japan Fin Min Aso: Takata bankruptcy may impact jobless rate; Will work with METI to gauge impact - press

(JP) Japan ruling Liberal Democratic Party lawmaker Shigeru Ishiba: Japan must keep its 2020 primary balance target; faith in currency is extremely important

(JP) Japan Q1 Household Assets ¥1,809T, +2.7% y/y

Korea

(KR) South Korea Pres Moon: Extra budget will help economy get back to 3% GDP growth - press

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.3%, Hang Seng +0.1%, Shanghai Composite -0.1%, ASX200 -0.1%, Kospi +0.3%

Equity Futures: S&P500 flat; Nasdaq +0.1%, Dax flat, FTSE100 flat

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1180-1.1195; JPY 111.80-112.10; AUD 0.7575-0.7605; NZD 0.7275-0.7300

Aug Gold flat at 1,246/oz; Aug Crude Oil +0.3% at $43.50/brl; July Copper -0.2% at $2.63/lb

SPDR Gold Trust ETF daily holdings rise 2.7 tonnes to 853.7 tonnes

Morgan Stanley lowers Q3 Iron Ore price forecast by 23% to $50/ton - press

(CN) PBOC SETS YUAN MID POINT AT 6.8292 V 6.8220 PRIOR; Weakest Yuan fix since May 31st

(CN) PBoC: To skip today's open market operation (OMO); 3rd straight skip

(JP) Japan MoF sells ¥1.77T v ¥2.2T indicated in 2-yr 0.1% JGBs; Avg yield: -0.103% v -0.162% prior; bid to cover: 6.79x v 5.06x prior

(AU) Australia (AOFM) sells A$150M in 2.5% 2030 indexed bonds; avg yield 0.6562%

Asia equities notable movers

Australia

QBE Insurance (QBE) +1.3%; Exec: Seeing higher claims in emerging markets - press

Blackmores Limited (BKL) -3.9%; CEO Christine Holgate to resign

Metcash (MTS) -4.1%; Cut at Credit Suisse

Japan

Nissan (7201) +0.7%; Targets 8% global market share as part of its next mid-term plan - press

Mitsubishi Motor (7211) +1.4%; Guides FY19 global vehicle production at least 1.5M units, +40% from last FY

Nikon (7731) +0.7%; Said to increase display device output for camera and TV products - Nikkei

Hong Kong

China Southern (1055) -3.5%; To raise up to $1.9B in share sale

Pioneer Global Group (224) +13.4%; Reports FY17 (HK$) Net loss 67.6M v loss 67.7M y/y; Rev 295.0M v 258.7M y/y

Bosideng International Holdings limited (3998) +5.1%; Reports FY (CNY) net 391.8M v 280.9M y/y, Rev 6.82B v 5.79B y/y

Candlesticks and Ichimoku Trade Ideas Performance Update

2 positions were entered among all 4 currency pairs with total loss of 30 points and the positions are listed below:

19 Jun : USD/CHF - Long at 0.9705, exited at 0.9690 (- 15 points)

21 Jun : GBP/USD - Short at 1.2695, exited at 1.2710 (- 15 points)

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr + 65 + 93 + 50 - 40

May - 65 - 35 + 100 -175

Jun - 65 -10 - 10 + 75

Jul

Aug

Sep

Oct

Nov

Dec

Y-T-D + 278 + 38 +200 -174

Silver Could Be About To Reverse Its Trajectory

Key Points:

- Short term bullish trend line evident.

- RSI Oscillator is nearing oversold whilst Stochastics indicate reversal imminent.

- Watch for a break higher towards the $17.00 handle and $17.582 in extension.

Silver has been relatively volatile over the past few weeks as the metal has reacted to a range of changing conditions, including risks from the Fed on interest rate hikes. However, despite the recent pullback from the high at $17.714, the precious metal could be setting up to turn the corner and rally again.

Currently, the precious metal is trading around the $16.533 mark,relatively close to a key support level. Subsequently, any further downside moves would need to surmount this level and convincingly push lower to maintain its momentum. However, the risks are abating and we might be relatively close to seeing a reversal for the precious metal.

In fact, a review of the daily chart shows a relatively clear short term, rising trend line which is likely to mean plenty of support for the metal in the coming days. In addition, the RSI Oscillator is nearing over sold levels, and given that the swing lows are getting higher, we are likely to see a rally in the coming days. The Stochastic Oscillator is also representing a potential reversal with a crossover, within oversold territory, having occurred in the past few days.

However, despite the upside biased technical factors, it should be noted that the derivatives market for Silver has seen plenty of manipulation on COMEX of late and this has strongly impacted ‘paper’ prices. Subsequently, it’s relatively difficult to predict the timing of potential breakouts given some of the opaque actors behind the scenes.

However, it is relatively clear that there is building pressure for an upside correction in the coming days. This is especially prescient given that price action is currently being squeezed between a rising trend line and the declining moving averages. Clearly, something must break and both of the oscillators seem to suggest that the upside is the probable direction.

Ultimately, Silver is likely to see some bullishness in the coming days as long as it can break through the declining moving average lines. If it can surmount this level we are likely to see a significant technical rally that, given the size of the recent range, could take it back towards the $17.582 mark. Even the fundamental perspective is positive with a range of worsening U.S. economic data clouding the risk of further Federal Reserve action in the months ahead. Also, physical and industrial demand for Silver remains buoyant further supporting the bullish contention.

Are Oil Prices On The Mend?

Key Points:

- Recent gains could be built on in the coming weeks.

- The shifting technical bias is indicating that gains could be quite substantial.

- A near-term peak is likely to be seen at the $47.69 handle.

Oil finally seems to have found a near-term bottom – much to the relief of OPEC – and this could set the commodity up for sizable recovery over the coming weeks. Of course, the overarching consensus that the cartel's efforts will be overshadowed by North American supply remains in place which will likely mean that we aren't destined to move back above that $50 mark. Nevertheless, there could still be some decent upside potential to capitalise on.

Primarily, it is the shifting technical bias that suggests that recent gains may be only the beginning of a much larger upswing for oil prices. This may come as somewhat of a surprise to some as, quite clearly, the EMA's are about as bearish as they can be and the long-term trend line is certainly in decline. However, upon closer inspection, there are actually numerous signs that the oil could be much more buoyant than is immediately apparent.

For one thing, the Parabolic SAR – typically a good indicator of trend direction – is barely one pip above price action. Effectively, this means that we could see the reading shift to bullish with even the most modest day of buying pressure. Additionally, the MACD and the signal line are well on the way to converging which could indicate that a shift in momentum is now in full swing. One final thing worth mentioning is just how close oil prices are to dipping back into oversold territory as this will be reinforcing support around the $43 handle and capping downside risks.

All things considered, there is a decent likelihood of us seeing gains extend moving ahead which now begs the question, where can we expect resistance to come back into play? As shown above, a key resistance level exists around the $46 mark which could prove to be a near-term peak for oil. Largely, this can be chalked up to the presence of both a historical reversal level and the 38.2% Fibonacci retracement around this price. However, this resistance level is by no means an unassailable barrier to the potential rally and we could instead see gains extend all the way up to the $47.69 handle. At this price, the influence of the 100 day moving average will also be adding to the overall selling pressure – perhaps sparking yet another reversal and resumption of the overarching downtrend.

Trump Consumer Euphoria Seems To Have Faded A Bit Tonight

Market movers today

Today is another quiet day in terms of data releases.

The Fed's Williams (non-voter, neutral) will speak this morning and later today it is time for US consumer confidence for June. We look for a small decline in line with what we have seen in the consumer survey from University of Michigan. The post -Trump consumer euphoria seems to have faded a bit . Tonight , more Fed speakers will be available (Kashkari and Harker).

In the Scandies, it is time for Swedish foreign trade and PPI data for May. Given the improvement in export indicators over the past few months, we would need to see some strong export numbers to remain positive on the out look for exports. Looking at seasonal patterns, we fear that net trade in May may have moved further into negative territory though.

Selected market news

Yesterday, German ifo expectations increased again in June to 106.8 from 106.5 in May (consensus: 106.4). This is the highest level since early 2014 and suggests a GDP above 1.0% q/q in Germany. The slightly higher ifo expectations were driven by the wholesale and retail sector expectations while manufacturing and construction sector expectations were unchanged compared with the levels in May. Note that despite the still solid ifo expectations and PMI figures, the euro area surprise index has declined during June.

In the US, core capex orders came out yesterday at -0.2% m/m in May, but were revised up in April from 0.1% to 0.2%. Orders have rebounded from previous lows but have stabilised recently, still at low levels. The figures suggest slower fixed investment growth in Q2 than in Q1.

It has been a calm session in global financial markets this morning. Asian stock markets have moved sideways mainly and in fixed income markets, changes in the US 10-year government benchmark bond yield have been quite muted since yesterday.

Aussie Dollar Extends Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.09% against the USD and closed at 0.7582.

LME Copper prices declined 0.05% or $3.0/MT to $5771.0/MT. Aluminium prices declined 0.7% or $13.0/MT to $1855.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7587, with the AUD trading 0.07% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7570, and a fall through could take it to the next support level of 0.7552. The pair is expected to find its first resistance at 0.7602, and a rise through could take it to the next resistance level of 0.7616.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Germany’s Ifo Business Confidence Surged To A Record High Level In June

For the 24 hours to 23:00 GMT, the EUR declined 0.13% against the USD and closed at 1.1180, after the European Central Bank's (ECB) President, Mario Draghi stated that there is no need to deviate from the ECB's policy path, adding that premature tightening would lead to a fresh recession and more inequality as low interest rates had helped create jobs and foster growth in the economy.

On the macro front, Germany's Ifo business climate index unexpectedly rose to a level of 115.1 in June, notching its highest level since 1991 and defying market expectations for a fall to a level of 114.5, suggesting that German business confidence is booming amid brighter growth prospects in the Euro-zone's largest economy. The index had recorded a level of 114.6 in the previous month.

Moreover, the nation's Ifo business expectations index registered an unexpected rise to a level of 106.8 in June, compared to a reading of 106.5 in the previous month, while markets were expecting the index to fall to a level of 106.4. Also, the nation's Ifo current assessment index surprisingly advanced to a level of 124.1 in June, compared to market expectations for the index to remain steady at a level of 123.3.

Macroeconomic data released in the US indicated that preliminary durable goods orders eased more-than-expected by 1.1% on a monthly basis in May, compared to market consensus for a drop of 0.6%. In the previous month, durable goods orders had dropped 0.8%. Additionally, the nation's Dallas Fed manufacturing business index declined more-than-anticipated to a level of 15.0 in June, compared to a reading of 17.2 in the prior month. Also, the nation's Chicago Fed national activity index dropped more-than-expected to a level of -0.26 in May, compared to a revised reading of 0.57 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1187, with the EUR trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1166, and a fall through could take it to the next support level of 1.1145. The pair is expected to find its first resistance at 1.1214, and a rise through could take it to the next resistance level of 1.1241.

With no major economic releases in the Euro-zone today, investors will look forward to the US consumer confidence index for June, slated to release later in the day. Also, market participants will draw their attention to a speech by the Federal Reserve (Fed) Chair, Janet Yellen, for clues on the timing of further rate hikes and plans to trim the Fed's balance sheet.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

UK’s BBA Mortgage Applications Declined To An 8-Month Low Level In May

For the 24 hours to 23:00 GMT, the GBP declined 0.24% against the USD and closed at 1.2719, after UK's BBA mortgage approvals fell to a level of 40.35K in May, hitting its lowest level since September 2016 and compared to a revised level of 40.69K in the previous month. Meanwhile, investors had envisaged for a drop to a level of 40.25K.

However, losses in the Pound were trimmed after the British Prime Minister, Theresa May's Conservatives struck a deal with the Democratic Unionist Party to support a minority government.

In the Asian session, at GMT0300, the pair is trading at 1.2719, with the GBP trading flat against the USD from yesterday's close.

The pair is expected to find support at 1.2697, and a fall through could take it to the next support level of 1.2674. The pair is expected to find its first resistance at 1.2751, and a rise through could take it to the next resistance level of 1.2782.

Ahead in the day, traders would closely monitor a speech by the Bank of England's (BoE) Governor, Mark Carney, and the BoE's financial stability report.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.