Sample Category Title

Commodities Diverge Ahead Of Trump’s Climate Accord Decision

Climate change will be the theme of the day, as the President tweets that He will announce his decision this afternoon, which could see a continuation of both oil and gold's overnight price action.

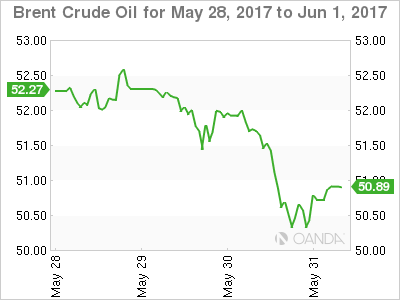

Oil's early week rally came to an abrupt end overnight as increasing Libyan and Nigerian production lit the fuse, and both Brent and WTI plunged nearly 4 percent at one stage. Both managed to rally on intra-day profit taking but still ended up around -2.2 percent for the New York session. Although OPEC cut exempt Libya and Nigeria may have been blamed, I suspect they are more the straws that have broken the camel's backs, with the technical picture on both contracts starting to look more like a technical consolidation of a bear market rather than a new dawn for bulls.

Traders will now look ahead nervously to this tonight's U.S. DOE Crude Inventory figures for solace with the market looking for a minus three million drawdown. A greater drawdown may see oil stabilise while a less than expected drawdown could see more downside pain. Ahead of this though President Trump's announcement on the United States' future in the Paris Climate Change Accord's at 3 PM ET in Washington D.C. A withdrawal may be construed as open season on new drilling which in itself may not bring bulls cheer.

Brent spot trades at 50.95 with support at 50.00. A daily close below this level is implying a potentially much deeper downside extension. Resistance is at 52.10.

WTI spot has support at 47.50 and then 47.20. It has resistance at 49.50 and then the magical 50.00 level where significantly, it failed at earlier this week.

Gold

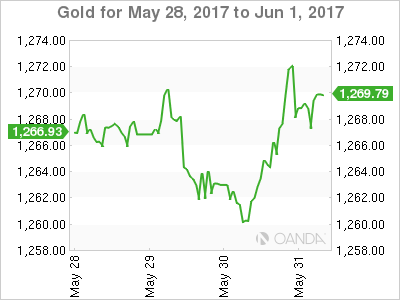

If the street needed a clear lesson on gold's pricing dynamics at the moment, as the geopolitical temperature gauge rose a few notches and gold rallied 15 dollars to 1274.50 at one stage, before settling at 1269.50 in early Asia trading after a very busy New York session. Investors around the world are seeking safe havens ahead of tomorrow's Non-Farm payrolls and into next weeks U.K. Elections which have gone from a one horse race to an emotionally close one if you believe the polls.

Before this, though we will have President Trump's announcement of the United States future within the Paris Climate Accords in Washington D.C. A withdrawal in itself shouldn't be bearish for the U.S. Dollar in isolation; rather it is the intent that it signals. In this case a more isolationist stance from literally, the rest of the world's view. This could see that geopolitical temperature gauge rise again, taking gold with it.

All of the above and running into the weekend should imply that gold remains bid, if not here than on any significant dips. Gold has a double bottom and ascending trend line support at 1259.00 with resistance at the overnight highs of 1274.50. A break above here may see more stop loss buying enter the market with the next resistance at 1278.50. Traders should expect intraday moves to be very headline driven over the next two days.

Running With The Yuan Bulls

Running with the Yuan Bulls

An extremely active month end as the dealing desk was abuzz digesting numerous conversations and themes.Currency markets were grappling with a sagging US dollar and falling US Treasury yields. While equity markets were a bit wobbly as oil prices remain slippery and investors are expressing concern that the market is looking a bit extended.

The US dollar continues to sour as the recent string of poor to middling US economic data weighs negatively on US rate hike expectations beyond June

The ever so slight wobble in equity markets could be a sign that investors are growing more cautious about the US economy amidst external concerns around Chinese growth and euro zone stability.

While numerous currency subplots unfold, unquestionably the headliner is the Chinese Yuan

Chinese Yuan

The Pboc has let the Yuan bulls loose in the China shop. Extremely hectic 24 hours on the CNH post after USDCNH toppled ten big figures. While some explanation behind the move can be offered up about funding cost impact, the weightiness of the move cannot be explained by funding alone and is probably linked to the start of an overall CNH and CNY policy shift

Needless to say, the market is a tad shell-shocked this morning while searching for some policy clarity from the Pboc

While there remains some politics in play after the Moody's downgrade, with numerous projects recently tabled through the one belt one road initiative, the stronger Yuan could be in China's best interest to promote yuan internationalisation and attract more investment

On a fundamental basis, PBoC's shift in interest rate policy could be adjusting investors expectations. While the Pboc rate hikes were interpreted as in lock step with the Federal Reserve Board tightening, beyond June, the Fed interest rate view remains extremely clouded, so the shifting differentials will most certainly ease capital outflows and lessen domestic demand for US dollar

Euro

Despite the mixed headlines, negative EUR inflation data, and a very cautious sounding Draghi, the EURUSD powered higher overnight as investors become more convinced the ECB will signal a shift in forward guidance. It was all aboard the Euro Express as fear of missing the boat mentality on changing ECB policy is far too beguiling for traders to pass up. While yesterday's Reuters 'sources' article stoked the EURO Bulls fire, investors went all in after ECB member Weidmann affirmed the markets ECB view.

Australian Dollar

Soft commodity prices continue to undermine the Aussie dollar which is struggling for momentum despite broader USD weakness. Iron ore prices remain at the heart of the matter amidst China growth concerns. But sliding oil prices have compounded the view putting pressure on all commodity-linked currencies.

China concerns are mounting despite the beat on yesterday PMI as the actual impact of higher funding cost have yet to be realised in the manufacturing and service sector.

Aussie appears to be hanging on by a thread, and if weren't for the dwindling Fed rate hike expectation beyond June, the Aussie could very be trading well below the .7400 handle.

Oil remains on a very slippery slope as traders continue to hammer prices lower in total defiance to OPEC production cuts. Speculators will continue to throw down the gauntlet amid concerns about the growing supply glut more so as US rigs continue to ramp up production.

API reported a draw of 8.67 million barrels of US crude oil and coming at a timely reprieve for prices.But given the market's current resolve it's more likely the knee-jerk is faded rather than extended as conversation around oil remains very bearish

While external drivers should remain dominant, these mornings CAPEX and Retail sales data could produce a limited rise, but the tail risk is most certainly for weaker prints with the Aussie precariously perched at.7425

Dollar Mixed Ahead Of Busy Economic Calendar

Private payrolls, unemployment claims, manufacturing data and oil inventories

The US dollar is mixed on Wednesday. The greenback is gaining against commodity currencies like the NZD, CAD and AUD but the current political turmoil has the CHF, EUR and CHF appreciating against the dollar. Added to the turbulence the Trump Administration is embroiled in regarding Russian connections, the ratings agency Fitch said today that the two pieces of legislation under review by Congress could limit the independence of the Fed and reduce the role of the dollar as the global reserve currency.

The ADP private payrolls employment change will be released on Thursday, June 1 at 8:15 am EDT. US unemployment claims will be published at 8:30 am EDT. The two US employment indicators will build the expectations for the U.S. non farm payrolls (NFP) due on Friday. The ADP is forecasted to show the US added another 181,000 jobs in May and the claims to be inline with previous weeks at around 230,000. The Institute for Supply Management will release the manufacturing purchasing manager index at 10:00 am EDT. The ISM manufacturing PMI has been deteriorating over the past months but is still expected at 54. A reading above 50 is considered an expansion.

Oil prices have been one of the biggest movers after doubts have risen regarding the ability of the Organization of the Petroleum Exporting Countries (OPEC) and other major producers to stabilize energy prices with their production cut agreement extension. The release of the US weekly inventories at 11:00 am EDT will bring more transparency to see the impact of their strategy, as it is being offset by rising US shale production and the end of the latest disruption to Libyan supply.

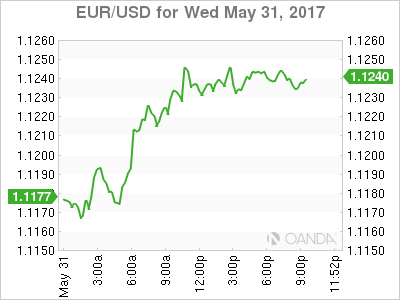

The EUR/USD gained 0.406 percent in the last 24 hours. The single pair is trading at 1.1235 after European data disappointed but the USD was unable to gain momentum as the chaos in Washington continues to impair the currency. German retails sales dropped by 0.2 percent and unemployment was reduced by less than expected to rattle confidence in the EU’s largest economy. Inflation data was soft, but close to forecasts which will be enough for the European Central Bank (ECB) to continue on the current path of balancing an end of negative rates, while tapering its stimulus program.

Dallas Fed Chief Robert Kaplan said yesterday that the 3 percent growth targets from the Trump administration are too aggressive and the US will probably growth at 2 percent. Fed Kaplan favours balance sheet reduction by this year with a gradual pace to take the process years to complete. Kaplan foresees two more rate hikes in 2017, in line with many of his colleagues and for the time being at least one more than the market is pricing in. The CME FedWatch tool has been slightly below 90 percent in probability of a June rate hike leaving the fed funds rate at 100 to 125 basis points. Political uncertainty and monetary policy are too evenly matched at this point and the dollar will need some clarity from economic data if its go give the monetary policy divergence edge to the greenback.

The ISM in Chicago offered a correction to its data release showing a better than expected 59.4 reading. The original report was a disappointing 55.2 reading. There will be some anxiety regarding the ISM release of the manufacturing PMI data given that no explanation was given on the erroneous data that stood for 93 minutes.

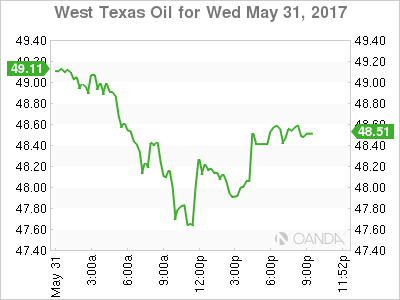

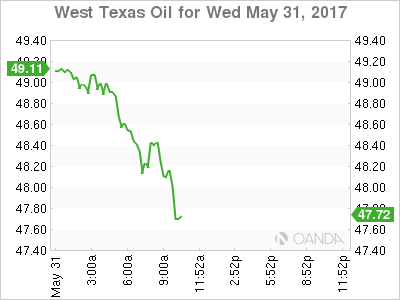

The price of oil fell 2.714 percent in the last 24 hours. The West Texas Intermediate is trading at $48.08 after the supply disruption in Libya has been sorted and the OPEC member nation is now reporting a daily production of 827,000 barrels, before the problems at the country’s biggest oilfield, El Sharara, had production at 794,000. Oil prices are at three week lows despite the efforts from the OPEC and other producers to cut production to stabilize prices.

With the meeting in Vienna on May 25 now in the past traders are not sure the OPEC is doing enough as it followed the script set by the dual press release form Saudi Arabia and Russia earlier in the month. US production is still on the rise and even the OPEC members outside of the deal are ramping up production giving traders concerns about how much of the glut can really be reduced, when the actual demand for energy has not increased.

Market events to watch this week:

Thursday, Jun 1

4:30 am GBP Manufacturing PMI

8:15 am USD ADP Non-Farm Employment Change

8:30 am USD Unemployment Claims

10:00 am USD ISM Manufacturing PMI

11:00 am USD Crude Oil Inventories

Friday, Jun 2

4:30 am GBP Construction PMI

8:30 am CAD Trade Balance

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

The Five Great Debates

No single theme is dominating markets right now so today we take a look at five fundamental drivers and where we stand. In May, the New Zealand dollar was the top performer while AUD lagged in a major antipodean divergence. 2 new Premium trades have been added; 1 in FX and 1 in a major European index.

The UK election debate scheduled for today is a dud. While the polls continue to drive GBP, we look at five bigger debates elsewhere.

1) The Fed debate

The market is juggling with three options: Here they are with the probabilities in parentheses: No hike on June 14 (10%). It would take a string of weak data between then and now; A hike with similarly hawkish bias (35%). Fed officials have begun to worry about the data; A hike with a dovish bias (55%). The market is shifting towards this option and that's what is weighing on the US dollar. It would be signaled by something in the statement indicating that the Fed will need to see stronger evidence of growth and inflation before continuing to remove stimulus.

2) The great inflation debate

This feeds into the first theme. Eurozone inflation at 1.4% y/y compared to 1.5% on Wednesday missed expectations. Central banks are divided on whether slightly better growth and a tighter jobs market will producer inflation. The latest buzz phrase in economics circles is 'global overcapacity' which is fancy way of saying that globalization, technology and offshoring can keep prices and wages down. The Fed is holding on tight to models that show a tight domestic economy will mean domestic inflation but they may one day have to rethink it.

3) The China mystery

Yesterday's PMIs were both slightly stronger than expected but the opacity of Chinese policy and the latest drop in metals prices has planted a deep seed of doubt. The latest move is rapid yuan strengthening. Skeptics say it's a government-orchestrated squeeze on shorts designed to improve stability. We're watching closely.

4) The ECB shift debate

A leak on Tuesday indicated the ECB could move to a neutral stance and take away references to doing more as soon as next week. That was followed by today's disappointing eurozone data slate. In the bigger picture, the suspicions is that Draghi wants to setup a September taper announcement but doesn't want to spark EUR/USD strength or excessive run-up in yields.

5) Oil's toils

More Libyan production sent oil sharply lower Wednesday but it bounced on tighter US inventories in the API report. Every oil authority talks about a great inventory balancing that's coming before year end while every analyst has doubts. Russia's deputy finance minister might have tipped his hand Wednesday, saying to expect $40-$50 oil for seven years with risks of prices falling below. We're left with the question: Who or what could boost crude right now?

Could NZD/USD Hold Above the 0.7100 Psychological Level?

NZD/USD has seen a noticeable 2.4% gain since May 22nd helped by outperforming New Zealand economic data.

On the daily chart Kiwi bulls have successfully breached the major downtrend line resistance on May 22. Since then Kiwi has been trading above the downside 10 SMA support.

The bulls further broke the next significant psychological resistance level at 0.7000 on May 23 with strong bullish momentum.

This morning NZD/USD broke the next significant psychological resistance level at 0.7100, touching a 3-month high of 0.7120, helped by the weakening of USD.

If the bulls can successfully hold above the level at 0.7100, we will likely see Kiwi continuing edging up.

Conversely, if the bulls fail to hold the level, we will likely see a correction.

The resistance level is at 0.7120 followed by 0.7150.

The support line is at 0.7100 followed by 0.7080 and 0.7050.

US pending home sales for April will be released at 15:00 BST this afternoon. Be aware that it will likely affect NZD/USD.

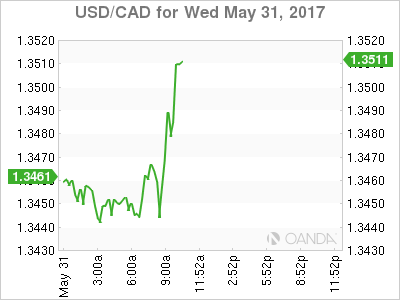

Canadian Dollar Lower After March GDP Beats Expectations but Oil Drops

The Canadian dollar is weaker against the US dollar o Wednesday despite an improvement of monthly GDP data in March. Oil prices continue to suffer from glut concerns as the efforts of the Organization of the Petroleum Exporting Countries (OPEC) and other producers to cut production are being offset by non members such as the US and even by members such as Libya who has ramped up production after a disruption in its largest oil field.

The Canadian economy great at a 3.7 percent pace in the first quarter of 2017. The annualized per quarter growth was lower than expected but the monthly figures for March beat estimates by showing a 0.5 percent growth when 0.2 was anticipated. The third and fourth quarters of last year were revised upwards with a final 4.2 percent for Q3 and 2.7 percent for Q4.

Mexico Economy Minister Ildefonso Guajardo said earlier today that he is seeking to finish NAFTA talks with US by December 15. The Trump administration has started the process that could start talks in late August. Guajardo is foreseeing negotiations to take place in the last quarter of the 2017. On May 11 the Mexican minister stated that he will send a delegation to China in September to seek other alternatives. Mr. Guajardo has also said that if duties are part of the agreement Mexico could walk out of the negotiations. The Conference Board of Canada said today that the US softwood lumber duties will have a $700 million impact to Canadian exports and a loss of 2,200 jobs. The negative impact to the Canadian economy of a bad renegotiation of NAFTA would be massive given the high percentage of exports that head south.

The USD/CAD lost 0.275 percent in the last 24 hours. The currency pair is trading at 1.3449 after the stronger than expected monthly GDP data was not enough to offset the trend that made the quarterly data came in below expectations. The growth of the Canadian economy in the last two quarters of 2016 was revised upward which makes the first quarter more solid than before, but the high correlation between oil prices and the loonie put downward pressure on the currency. US political turmoil has the dollar in a daze, not able to capitalize on the positive comments from voting Fed members.

Dallas Fed Chief Robert Kaplan said yesterday that the 3 percent growth targets from the Trump administration are too aggressive and the US will probably growth at 2 percent. Fed Kaplan favours balance sheet reduction by this year with a gradual pace to take the process years to complete. Kaplan foresees two more rate hikes in 2017, in line with many of his colleagues and for the time being at least one more than the market is pricing in. The CME FedWatch tool has been slightly below 90 percent in probability of a June rate hike leaving the fed funds rate at 100 to 125 basis points. Political uncertainty and monetary policy are too evenly matched at this point and the dollar will need some clarity from economic data if its go give the monetary policy divergence edge to the greenback.

The price of oil fell 1.675 percent in the last 24 hours. The West Texas Intermediate is trading at $48.36 after the supply disruption in Libya has been sorted and the OPEC member nation is now reporting a daily production of 827,000 barrels, before the problems at the country's biggest oilfield, El Sharara, had production at 794,000. Oil prices are at three week lows despite the efforts from the OPEC and other producers to cut production to stabilize prices.

With the meeting in Vienna on May 25 now in the past traders are not sure the OPEC is doing enough as it followed the script set by the dual press release form Saudi Arabia and Russia earlier in the month. US production is still on the rise and even the OPEC members outside of the deal are ramping up production giving traders concerns about how much of the glut can really be reduced, when the actual demand for energy has not increased.

Market events to watch this week:

Thursday, Jun 1

- 4:30 am GBP Manufacturing PMI

- 8:15 am USD ADP Non-Farm Employment Change

- 8:30 am USD Unemployment Claims

- 10:00 am USD ISM Manufacturing PMI

- 11:00 am USD Crude Oil Inventories

Friday, Jun 2

- 4:30 am GBP Construction PMI

- 8:30 am CAD Trade Balance

- 8:30 am USD Average Hourly Earnings m/m

- 8:30 am USD Non-Farm Employment Change

- 8:30 am USD Unemployment Rate

*All times EDT

Technical Outlook: GBPUSD Regained Traction and Bounced

Cable regained traction and bounced near Asian high at 1.2863 on bullish acceleration from European session low at 1.2768. Fresh strength emerged after a poll published on Wednesday showed an increase of the lead of Conservative party to 15 percentage points. The latest rally sidelined immediate downside risk, despite the pair cracked previous low at 1.2775, as the price remains well above pivotal support at 1.2786 (Fibo 38.2% of 1.2365/1.3047 rally and is on track for the fourth consecutive daily close above the support. However, the downside is expected to remain at risk, as formation of 10/20SMA and daily Tenkan-sen/Kijun-sen bear crosses is seen as bearish signal. Only sustained break above 1.2900/20 resistance zone would provide relief and signal stronger retracement of pullback from 1.3047 (18 May peak).

Res: 1.2866; 1.2887; 1.2909; 1.2920

Sup: 1.2823; 1.2809; 1.2786; 1.2768

EUR/GBP Returns Close to Recent Top

- Main European equity markets gain more than 0.5% in a news-thin trading session. US stock markets open mixed with Nasdaq outperforming (+0.25%).

- Dallas Fed Kaplan said that inflation is "sort of back on trend" and that he doesn't think there's a deteriorating trend in price pressures. He sees two more interest rate increases and an announcement of plans to reduce Fed's balance sheet this year.

- EMU CPI inflation slowed more than forecast in May, falling from 1.9% Y/Y to 1.4% Y/Y. Underlying core inflation decelerated from 1.2% Y/Y to 0.9% Y/Y, strengthening ECB Draghi's case to keep monetary policy ultra-easy. The EMU unemployment rate fell from 9.5% to 9.3%, its lowest level since March 2009.

- The Chicago PMI declined from 58.3 to 55.2 in May, while consensus only expected a drop to 57. However, given the volatile history of the Chicago PMI, this outcome didn't bother investors.

- US President Trump has decided to withdraw from the Paris climate accord, Axios reported, citing two unidentified sources with direct knowledge of the decision. Trump, who has previously called global warming a hoax, refused to endorse the landmark climate change accord at a summit of the G7 group of wealthy nations last Saturday

- A renewed pledge from Saudi Arabia and Russia, two of the world's biggest oil producers, to bring down surplus inventories failed to stem a decline on Wednesday in the price of crude oil. Brent crude declined from $52/barrel towards $50/barrel.

- Europe must stop stalling and agree on debt relief measures for Greece on June 15 to revive the only EMU economy still in recession, ECB Coeure said. He added that if the meeting agreed sufficiently clear measures, this would allow the ECB to consider including Greek bonds in its asset purchase programme.

Rates

Brent crude oil tests psychological $50/barrel mark

Global core bond investors remained side-lined today ahead of key US eco data tomorrow (ADP, manufacturing ISM) and Friday (payrolls). Both the Bund and US Note future traded again in a narrow sideways range. The impact from positive risk sentiment on European stock markets (>+0.5%) and weakness in oil prices ( drop from $52/barrel to $50/barrel) cancelled each other out. EMU eco data printed mixed with a bigger drop in EMU inflation, though anticipated after lower German/Spanish/French CPI readings and an unexpected decline in unemployment rate to the lowest level since March 2009. Dallas Fed Kaplan sounded less concerned about the recent setback in US inflation than Washington-based Fed governor Brainard yesterday and sticks with his rate call (2 more hikes this year). Markets shrugged their shoulders.

At the time of writing, changes on the German yield curve range between -0.1 bp (2-yr) and +0.3 bps (30-yr). Changes on the US yield curve vary between -0.2 bps (2-yr) and +0.7 bps (5-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrowed 1 to 4 bps with Portugal outperforming (-7 bps) and Greece underperforming (+3 bps).

Currencies

Euro erases early losses. Dollar fails to convince

The euro outperformed most other major currencies today. EMU inflation declined more than expected. At the same time, German and EMU unemployment beat market consensus. The combination of good growth, low inflation and the expectation of only very gradual ECB policy normalisation triggered some kind of European risk rally. EMU assets and the euro are outperforming. EUR/USD trades in the 1.1225 area. USD/JPY (110.85) again hardly profits from this risk rally.

Overnight, Asian markets showed a diffuse picture. Chinese equities opened strong, supported by better than expected China PMI's, but the gains evaporated. Japan underperformed. USD/JPY held in the 111 area. End-of-month USD buying from US importers is said to prevent a further decline, for now. EUR/USD traded with a slightly negative bias in a tight 1.1190/65 range.

Trading on most markets, including in the major FX cross rates, was confined to tight ranges during most of the morning session. EMU eco data were mixed. EMU headline inflation declined more than expected from 1.9% Y/Y to 1.4% Y/Y, supporting recent calls from ECB president Draghi that the EMU economy still needs ample monetary support. At the same time, the German unemployment rate dropped to 5.7%, a record low. The EMU unemployment rate also declined faster than expected to 9.3%, the lowest level since 2009. Initially, the data had hardly any impact on trading. Sentiment changed as US traders joined the action. Some kind of European risk-on trade kicked it with European equities and the euro outperforming. The combination of strong growth, benign inflation and expectations for only a gradual scaling back of ECB policy stimulation triggered a repositioning in favour of European assets, including the single currency. EUR/USD rebounded back above the 1.12 area. Remarkably, interest rate differentials between the US and Germany/EMU hardly changed. A sharp decline of oil didn't help the dollar. Other interesting remark: USD/JPY again didn't profit from the (European) risk rally. The pair even fails to hold north of 111 (currently 110.85). EUR./USD is changing hands around 1.1218, a combination of euro strength and USD softness. Later today, USD traders will keep an eye at the Fed Beige Book, preparing the June 13-14 meeting.

EUR/GBP returns close to recent top

Investors sold sterling this morning as a YouGov poll indicated that the Conservative party might fail to secure a majority in the June 08 election. Sterling was already under pressure in Asia and the pressure intensified early in Europe. Cable dropped temporary below 1.28 (even as the dollar wasn't in good shape either). EUR/GBP rebounded north of 0.87. The pressure on sterling eased later in the session, maybe as other polls still give quite a significant lead for the conservative party. Especially cable rebounded and trades again in the 1.2840/50 area, reversing most of the overnight loss. EUR/GBP (0.8735) holds near the recent highs as the euro remains well bid across the board.

Strong and More ‘Balanced’ Growth in Canada in Q1

Highlights:

- Canadian GDP jumped 3.7% in Q1 (at an annualized rate) to build on 2.7% and 4.2% increases in Q4 and Q3 of 2016, respectively.

- Household spending remained strong (consumer spending up 4.3%, residential investment up 15.7%) but, unlike earlier quarters, business investment was also a significant support to Q1 growth.

- Monthly GDP rose a stronger-than-expected 0.5% in March, pointing to strong momentum through the end of the quarter.

Our Take:

Strong economic growth in Canada is not really new. The 3.7% GDP jump in Q1 2017 marked a third consecutive gain above our estimate of the economy's 'potential' long-run growth rate and a third consecutive outperformance relative to the U.S. Perhaps the most important takeaway from the Q1 numbers was a strong gain in business investment. The 10.3% annualized quarterly increase was the largest in almost 5 years and followed two years of persistent declines. Business investment has been a missing ingredient from earlier improvements which were driven largely by stronger household expenditures.

Q1 growth was not significantly different than the Bank of Canada's 3.8% forecast and there are still plenty of risks to the outlook, particularly from potential U.S. trade disruptions. Growing evidence that business investment has begun to rise again, however, means those concerns will have to be balanced against firmer current economic conditions that argue that ultra-low levels of interest rates may otherwise no longer be needed. We expect the bank to maintain a very cautious tone in the near-term, reflecting uncertainties about the U.S. and the lack of evidence that consumer price inflation is strengthening, but assume that further economic growth will eventually prompt the central bank to begin hiking rates at a gradual pace by mid-2018.

Hot First Quarter Growth Marks a Canadian GDP ‘Three-Peat’

The Canadian economy roared ahead in the first quarter of the year, expanding 3.7% q/q annualized. Including price effects, nominal GDP growth was an impressive 8.9%.

Consumers were the star of the show as household spending rose 4.3% on the back of robust durables spending (+9.9%). It seemed that Canadians still can't shake their debt habit, as nominal household expenditures outpaced disposable income growth, resulting in a 1 percentage point drop in the household savings rate (to 4.3%).

The positive story was not confined to consumers. Business investment rebounded significantly (+10.3%) on strength in machinery and equipment investment (+25.3%), while investment in intellectual property products rose 6.3% supported by an eye-popping 67.1% rise in mineral exploration. On the residential investment side of things, a 15.7% gain in activity marked the strongest performance since 2012 on the back of strong construction activity and a significant increase in resale activity.

Net trade was a modest drag on growth as exports were effectively flat (-0.3%) and imports gained sharply (+13.7%), as the impacts of earlier one-offs worked their way out of the data. Of course, imports must go somewhere, and in the first quarter, they appear to have largely made their way into inventories, which rose $14.9 billion, adding 3.6 percentage points to first quarter growth.

The 0.5% expansion of monthly GDP in March was also encouraging, providing a healthy starting point for the second quarter. The goods-producing side of the economy led the way (+0.9%) on strong gains in utilities and manufacturing (both +1.6%). The service sector expanded at a still healthy 0.3% monthly pace, with gains in retail trade (+1.0%), finance and insurance (+0.8%), and wholesale trade (+0.7%) leading the way. Encouragingly, on an industry basis, the Canadian economy continues to demonstrate a breadth of expansion: 80% of Canadian industries, representing approximately 90% of output expanded in March, the best performance since May 2014.

Key Implications

Wasn't it America that was supposed to be made great again? And yet boring old Canada was a first quarter pace of growth that more than tripled what was seen for the U.S. Moreover, although helped by a post-wildfire recovery, the 2016Q3 to 2017Q1 'three-peat' marked the fastest three-quarter string of growth since the post-crisis recovery in early 2010. Beneath the surface however, there are reasons to expect a less exciting pace of expansion going forward.

To begin with, there is already evidence that key housing markets are beginning to cool off, suggesting that the robust pace of first quarter growth is not likely to be seen again any time soon. At the same time, the environment for business investment should remain supportive, but elevated uncertainty is likely to cap the pace of growth. Finally, consumers are likely to keep their wallets open, helped by past gains in housing wealth. But, it is again unlikely that the pace of first quarter growth, particularly for durable goods spending, can be maintained, and the credit-fueled nature of recent spending growth remains concerning.

It is not all bad news however - strong March figures provide a solid start to the second quarter, setting the Canadian economy up another quarter of well above-trend growth.

For the Bank of Canada, despite the March GDP figures, concerns about the durability of growth and still soft consumer price inflation will likely result in continued near-term caution. That said, we remain of the view that growth is likely to moderate but remain above-trend, supported by a continuation of the broad based growth trend that has emerged in recent months. This broad-based growth, alongside nascent inflationary pressures, should set the stage for the beginning of a gradual tightening cycle early next year.