Sample Category Title

US Data Expected to Be Mixed

Ascension Day meant many European traders were not at their desks on Thursday and that may have explained the lack of volatility. The US Dollar did strengthen a little and Sterling did slip a little, but it was all a bit….beige. It wasn't a lack of data that made the FX market boring, though.

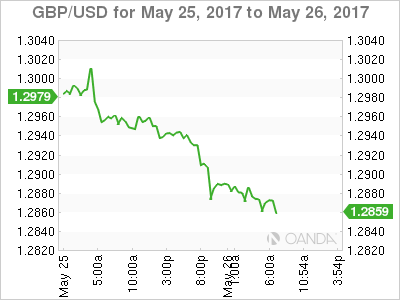

Britain's Q1 economic growth rate was downgraded to 0.2% from the previous estimate of 0.3%. That is sharply lower than the Q4 growth rate of 0.7% and that is a worry for the UK politicians, but Sterling didn't collapse. The lack of UK data today should leave Sterling to revolve around current levels, but there is a long weekend ahead in the UK and US, so traders may be tempted to remove some of their positions. As Sterling has slipped this week, there is scope for the Pound to recover somewhat before the 3-day break. Beware!

The little data we do have today comes from the US. The preliminary Q1 economic growth data is expected to show a rise to a quarterly 0.9% growth rate; up from Q4. If that is so, the US Dollar will strengthen, as a June US interest rate hike becomes more likely. That data doesn't have the spotlight to itself though; we will also see Durable Goods data (expected lower), the Michigan Consumer Sentiment Index (expected a little lower) and core Consumption and Expenditure data, for which the forecasts are very mixed. In other words, anything could happen. In such an unsettled environment, short-termism is a safe bet for currency risk management.

There isn't much more to report today. The G7 summit starts today, but there seem to be G7, or G8, or G20 meetings every few weeks these days. These guys do like to travel and they like to talk in summits so they can release meaningful communiques afterwards. Progress is always made and the meetings are always 'constructive'. Change, though, is a little scarcer. Sorry for being such a cynic.

Next week is very light on heavy data… if you catch my drift. There is a lot of it, though, and we have a change of month, plus a shortened week for UK and US traders – and we have the US Employment report next Friday. All in all, there is a lot to anticipate.

And there are reports that, in Germany, a four-mile-long pipeline is being built to transport beer to an upcoming festival. The volume it is able to handle means festival-goers will be able to buy beer poured at a rate of six pints in every six seconds. This is always assuming the pipeline isn't tapped by anyone else, of course.

Have a great extended weekend, one and all. I'm online now looking for tickets to Germany and a plumbing kit.

Drink up – it's a Bank Holiday weekend!

"The hard part about being a bartender is figuring out who is drunk and who is just stupid." Anon

"When I read about the evils of drinking, I gave up . . . reading." Henry Youngman

"In the Bowling Alley of Tomorrow, there will even be machines that wear rental shoes and throw the ball for you. Your sole function will be to drink beer." Dave Barry

"Actually, it only takes one drink to get me loaded. Trouble is, I can't remember if it's the thirteenth or fourteenth." George Burns

"An intelligent man is sometimes forced to be drunk to spend time with fools." Ernest Hemmingway

"If your doctor warns that you have to watch your drinking, find a bar with a mirror." John Mooney

"I can't die until the government finds a safe place to bury my liver." Phil Harris

"I told the stewardess liquor for three." - "Who are the other two?" - "Oh, there are no other two." James Bond

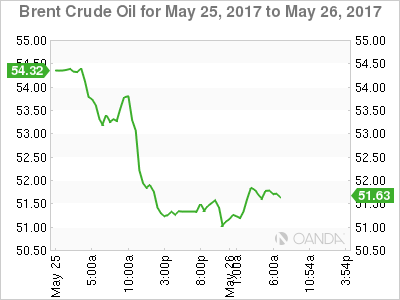

Oil Bears Inspired By OPEC Disappointment

A strong sense of disappointment had a punishing effect on oil markets on Thursday with prices tumbling 5% after OPEC underwhelmed participants by renewing an agreement to cap output by 1.8 million barrels a day until March 2018. With the resurgence of U.S Shale obstructing OPEC's efforts to quell the oversupply woes this year, most investors were hoping for deeper cuts to effectively rebalance the saturated markets.

There is now a growing threat of the nine-month supply cut extension leaving oil prices at the mercy of inventories and U.S Shale likely to exploit this well-presented opportunity to seize more market share from OPEC members. With the oil glut potentially returning with a vengeance once the OPEC deal expires in nine months, oil weakness may be destined to become a dominant theme in the medium to longer-term.

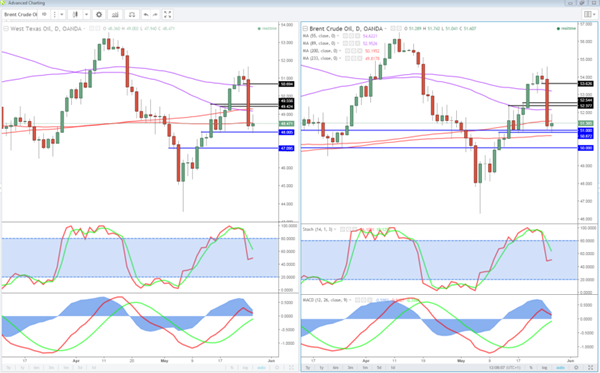

The price action seen in oil suggests that markets are clearly not impressed with OPEC's decision and further weakness should be expected as the oversupply fears bite. From a technical standpoint, WTI Crude is heavily depressed on the daily charts. A breakdown below $48 should provide encouragement for bears to challenge $46.

Sterling gripped by political uncertainty

Sterling found itself vulnerable to heavy losses on Friday after a poll showed a narrowing lead for Conservatives against the Labour opposition ahead of next month's general election. The threat of Theresa May failing to secure a landslide election victory should weigh heavy on Sterling moving forward as anxiety heightens over her ability to strengthen her hand in the Brexit negotiations. With political uncertainty likely to heighten ahead of the UK general election on June 8, Sterling could become even more attractive to bears.

Focusing away from politics, sentiment towards the UK economy took a hit on Thursday following reports showing GDP growth decelerating more than the initial estimate in the first quarter of 2017. The visible deceleration in economic growth is a clear sign of Brexit negatively impacting the UK as rising inflation and tepid wage growth drains consumer confidence. Sentiment is turning increasingly bearish towards the Pound with further downside expected as sellers exploit the Brexit anxiety to attack. From a technical standpoint, the GBPUSD is under selling pressure on the daily charts. A decisive break down below 1.2850 may open a path towards 1.2775.

Dollar remains vulnerable to losses

The Greenback has been on the back foot for the most part of this week with upside gains limited following May's Federal Reserve meeting minutes which was dished with a dovish undertone. With U.S economic data following a mixed pattern and Trump uncertainty still a dominant theme, there is a layer of uncertainty over the longer-term hiking path. As the Federal Reserve is set to maintain a defensive stance until the U.S economy displays signs of stability, there will be an increasing focus on hard economic data. With U.S economic data in focus, much attention will be directed towards the pending US GDP report on Friday which has the ability to empower the Dollar bears if GDP fails to meet expectations.

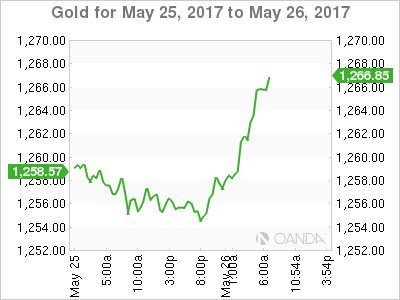

Gold bulls breach $1260

Gold was firm on Friday with prices breaking above $1260 as investors mulled over the tone of caution in May's Federal Reserve meeting minutes. Although expectations are high that there will be a U.S interest rate increase in June, the longer-term hiking path remains uncertain consequently weakening the Greenback. With uncertainty over Trump likely to impact the Fed and pressure the Dollar further, Gold should remain buoyed moving forward. From a technical standpoint, the yellow metal is regaining momentum on the daily charts with bulls pressuring the $1260 resistance. A breakout and daily close above $1260 should encourage a further incline higher towards $1275.

Oil Stops The Bleed, Sterling Pounded By Polls

Battered oil prices have stopped the bleeding for now as the market seems to be looking past the disappointment that yesterday's OPEC meeting did not expand on production cuts, instead of extending.

Global equities too are under pressure following crude oil's -5% loss yesterday; the loss seems to have undermined sentiment towards risk assets in general.

The pound has slid on a poll showing PM Theresa May's Conservatives' lead shrinking, two weeks before an election. According to the latest YouGov/Times poll, the Conservatives lead Labour by +43% to +38% ahead of June 8th election.

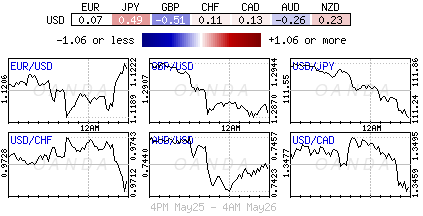

Comments from the St. Louis Fed President Bullard (dove) in Tokyo this morning are weighing on the 'mighty' dollar as he noted 'prices are deviating noticeably from the Fed's +2% inflation path' and called market expectations of 'two more rate hikes this year as too aggressive.'

1. Stocks lose some appeal on risk attitude

In Asian overnight, regional bourses traded mostly mixed despite the continued bullish momentum stateside, where the sixth consecutive positive session Thursday took U.S indices to new record highs.

In Japan, the Nikkei share average extended its losses (-0.6%) as the yen's gains (¥111.03) outright accelerated - the benchmark index still managed to cap off a winning week (+0.5%). The broader Topix fell -0.6%.

In Hong Kong, stocks broke a five-day winning streak, as gains in air carriers were offset by weakness in energy shares. The Hang Seng index was unchanged, while the China Enterprises Index gained +0.1%. For the week, both Hang Seng and HSCE gained +1.8%.

In China, stocks have ended the week higher with state-led buying offsetting the midweek Moody's downgrade. The blue-chip CSI300 index fell -0.2%, while the Shanghai Composite Index added +0.1%. For the week, CSI300 advanced +2.3%, while the SSEC gained +0.6%.

In Europe, regional indices trading mostly lower led by the FTSE MIB and French CAC, with the FTSE100 outperforming having traded new all time highs, mostly supported by a weaker pound (£1.2860).

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.7% at 3559, FTSE +0.1% at 7524, DAX -0.4% at 12568, CAC-40 -0.7% at 5298, IBEX-35 -1.0% at 10831, FTSE MIB -1.0% at 21083, SMI -0.2% at 9019, S&P 500 Futures -0.1%.

2. Oil stops the bleed for now, gold shines

Oil prices have edged higher ahead of the U.S open, but remain on the back foot after plummeting -5% in yesterday's session when OPEC and some non-OPEC producers agreed to extend a pledge to cut around -1.8m bpd until the end of the Q1 2018. The market was pricing in 'longer or larger curbs.'

Brent crude futures are at +$51.80 per barrel, up +0.66% from Thursday's close. They are still set to end today's session with a weekly loss of more than -3%. U.S West Texas Intermediate (WTI) crude futures continues to trade below the psychological +$50 handle, at +$49.15, though still up +16c from yesterdays close.

A weaker dollar coupled with a pullback in investor risk appetite is supporting gold. In the overnight session, spot gold has rallied +0.5% to +$1,261 an ounce, and is poised for a +0.5% gain for the week.

3. Global yields fall on risk attitude

It's not just a calm tone in equities, the bond market's volatility index has fallen to its lowest level in nearly three years this week as the Fed minutes further reduce risk of a big rise in yields.

Note: A lower reading suggests that investors expect smaller price swings or a relatively tight trading band for yields.

Currently, fixed income dealers expect the U.S 10-year Treasury yield to continue to trade between +2.20% and +2.50% in the near-term. Ahead of the open stateside, U.S 10's have backed up +1 bps to +2.24%.

In Europe, the bond market is being supported by muted expectations of a rapid turnaround in the ECB's policy. French (OAT's) 10-year yields are little changed, while German Bunds have dropped -1 bps to +0.36%.

In Japan, 10-year JGB yield declined -0.01 bps to +0.035% on disappointing CPI data overnight (see below).

4. 'Big' dollar remains under pressure

The pound has been one of the big movers with sterling falling to a new two-month low against EUR at €0.8724 after a YouGov opinion poll showed the lead for PM Theresa May's Conservative Party falling by -5 points ahead of the June 8 election. Outright, GBP/USD has dropped -0.5% to a two-week low of £1.2861, easily extending Thursday's fall after data revealed an unexpected downward revision to U.K Q1 GDP.

The EUR/USD (€1.1227) continues to hover atop of the psychological €1.12 handle. Many expect the 'single' unit pullbacks to be brief and shallow. The 'bulls' believe the EUR is in the process of going higher - the prospect of the ECB announcing a path to more tapering of its asset-purchase program at the June ECB meeting, improving eurozone economic activity, and rising eurozone capital inflows is expected to support the currency towards €1.1275 -1.13.

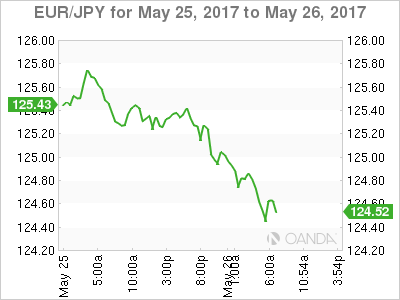

JPY (¥110.98) currency is firmer in the aftermath of Japan's April CPI data.

5. Japan's inflation recovers

Rising energy prices in April are finally making a dent in 'disinflationary' forces in Japan, as headline CPI hit a three-month high while Core-CPI (ex-food) hit a two-year high.

Japan National CPI rose for the fourth consecutive month - y/y +0.4% vs. +0.4%e; Core-CPI +0.3% vs. +0.4%e.

Overall, despite the uptick, the data remains well below the BoJ's target. However, the consensus continues to expect higher inflation in Japan in coming months due to a tightening labor market and a recovery in energy prices.

Soft End To The Week As Oil Drags

As the week draws to a close, risk appetite appears to be drying up, not helped of course by recent moves in oil which is dragging on global benchmarks.

Oil Bounces But Losses Weigh on Indices

Oil has been one of the standout performers throughout May as traders banked on an extension to the deal between a number of OPEC and non-OPEC producers that came into effect earlier this year. The deal – which will see the 1.8 million barrel a day cut extended from the middle of this year to the first quarter of 2018 – was agreed between participating producers on Thursday, prompted a sudden and sharp sell-off in oil.

The reason for the sell-off was simple. There had been so much reported on the agreement in the weeks leading up to the meeting that it had been fully priced in. Once speculation became reality, there was no more gains to be had, not in the near-term anyway. Should we see full compliance and evidence that inventories are falling back towards their five year average, as intended, the prices may well creep higher once again. The result for now though has been a correction in oil prices which is weighing on energy stocks and therefore indices, particularly those with heavy exposure.

FTSE Makes Small Gains as GBP Weakness Offsets Oil Moves

The FTSE 100, which ordinarily would be feeling the pain of this, is actually trading a little higher this morning. A second day of selling in the pound – this time driven by the latest poll numbers which show the gap between the Conservatives and Labour has shrunk to only five points from around 20 a couple of weeks ago – is more than compensating for the weakness in energy stocks and therefore helping to support the index.

Could Gold Be Headed Towards $1,300?

Gold is benefiting from the more risk averse sentiment in the markets today, as well as the weakness in the US dollar which is off by around one fifth of one percent. Gold is currently trying to push its way through $1,265 which has been a tricky level for the yellow metal over the last few months. A move above here could see it test its 2017 highs just shy of $1,300.

It's been a relatively quiet morning on the newsflow and data side, with no numbers from Europe leaving traders looking to the US releases as we close out the week. A first revision of Q1 GDP will certainly be of interest as the Fed considers its second rate hike of the year at its next meeting in June. Policy makers have shown a clear desire to see evidence that the first quarter weakness was only transitory and an upward revision here may provide them with more comfort. Of course, the opposite is also true. We'll also get durable goods orders and consumer surveys from UoM this afternoon, while the leaders of the G7 are also due to meet in Italy.

Daily Technical Analysis: GBP/USD Bearish Divergence Could Bring The Pair Lower

The GBP/USD is still in uptrend on 4h but it is showing a bearish divergence that could tank the price lower. 1.2830 is support and if the support breaks, the pair could head towards 1.2785. In case of retracement, we might see 1.2900-1.2915 the POC zone (inner trend line, ATR pivot, W4, EMA89). The POC zone could also reject the price towards 1.2830 and 1.2785. At this point the interim resistance is 23.6 fib - 1.2886 so short term traders could possibly reject the price from that level in the form of short term momentum trades.

Oil Prices Drop On A ‘Buy The Rumor, Sell The Fact’ Trade

Yesterday, OPEC and non-OPEC producers concluded their meeting in Vienna, agreeing to extend the duration of the November output-cut deal by 9 months at the previous volume of 1.8 mbpd. However, even though the producers reached an accord, oil prices dropped in the aftermath of the event, which in our view reflects a 'buy the rumor, sell the fact' reaction. An extension of 9 months was widely anticipated by markets, suggesting that all of the good news may have already been priced in. Thus, some investors that were looking for a longer extension or deeper cuts in production may have been left disappointed, which caused WTI prices to drop.

WTI fell below two support (now turned into resistance) levels in a row and the longer-term upside support line taken from the low of the 5th of April 2016. The decline was halted near the 48.40 (S1) support level. Even though the price structure on the 4-hour chart suggests the near-term outlook is cautiously negative, in order for us to get confident on further declines, we would like to see a decisive break below the 44.00 zone. Such a break would signal a forthcoming lower low on the 4-hour chart, and may set the stage for further downside extensions.

As for the bigger picture, we stick to our view that a long-term healthy uptrend in oil prices is still unlikely. The continued increase in US production – evident by the recent EIA data as well as the recovery in the Baker Hughes oil rig count – is likely to keep a lid on any significant gains in the precious liquid’s price. In addition, there is also the risk that the nations which are exempted from the production cuts, Libya and Nigeria, raise their output notably in the future, thereby offsetting some of the cuts from the other producers.

Sterling takes a hit from an election opinion poll

The British pound dipped overnight, following the release of a UK election opinion poll by YouGov. The poll showed that although the Conservatives are still ahead, Labour is catching up, with the two parties expected to secure 43% and 38% respectively. Considering that the FT’s rolling average of polls currently shows the two parties at 46% and 33%, this poll likely triggered speculation that this election race may actually be closer than previously anticipated.

In our view, fresh polls showing that the gap between these two parties continues to narrow could prove negative for sterling, on concerns that Theresa May and the Conservatives may not secure the strong majority they are seeking in Parliament. Finally, we believe that the British pound could become increasingly more sensitive to incoming polls as we approach Election Day, given that polls released just a few days ahead of the event may capture voters’ sentiment more accurately and thereby, carry more importance for investors.

GBP/USD fell overnight, breaking below the support (now turned into resistance) level of 1.2900 (R1). During the early European morning Friday, the pair looks to be headed for a test near the crossroad of the 1.2850 (S1) key support zone and a short-term uptrend line taken from the low of the 14th of March. New polls that show the Labour party catching up even further could trigger further declines in Cable. If the bears manage to overcome the aforementioned crossroad, they could initially aim for the next support hurdle at 1.2770 (S2).

Today’s highlights:

The European morning is relatively quiet, with no major indicators due to be released. The only event that could attract some attention is the G7 summit in Italy. We think that market focus will be on the language the G7 use about free trade, considering that after US President Trump got elected, the G20 dropped their commitment to 'resist all kinds of protectionism'.

In the US, durable goods orders for April are due out. The forecast is for the headline print to have declined, while the core figure is expected to have risen, a rebound from previously. We share the view for a decline in the headline print, considering the slowdown in civilian aircraft orders in April, while we see the risks surrounding the core forecast as skewed to the downside. We base this view on the nation’s ISM manufacturing PMI, which showed that new orders slowed down notably during the month. Soft durable goods orders could bring USD under renewed selling interest.

As for the rest of the US data, we also get the 2nd estimate of GDP for Q1. Expectations are for economic growth to have been revised upwards, albeit slightly. However, we doubt that it will have a significant market impact, given that the Fed has already pointed that it considers the soft growth in Q1 as transitory. As a result, we expect investors to pay more attention to incoming US data for Q2 (such as durable goods orders), as well as the Atlanta Fed GDPNow model, in order to get a better picture of whether economic growth has rebounded.

We have one speaker on the agenda: ECB Executive Board member Benoit Coeure.

WTI

Support: 48.40 (S1), 47.50 (S2), 46.00 (S3)

Resistance: 49.90 (R1), 50.60 (R2), 52.00 (R3)

GBP/USD

Support: 1.2850 (S1), 1.2770 (S2), 1.2700 (S3)

Resistance: 1.2900 (R1), 1.2950 (R2), 1.3000 (R3)

Euro Listless Ahead Of US GDP

The euro has been drifting this week, and continues to stay close to the 1.12 level. Currently, EUR/USD is trading at 1.1220. For a second straight day, there are no releases in the eurozone. It’s a busy day in the US, highlighted by Second Estimate GDP, which is expected to post a gain of 0.9%, better than the initial GDP report of 0.7%. This will be followed by Core Durable Goods Orders and UoM Consumer Sentiment. Leaders of the G7 are gathered in Sicily for a two-day meeting, with the response to global terror high on the agenda, especially in light of the Manchester bombing earlier this week.

German indicators continue to point upwards, and German business confidence hit a record high in May. The Ifo Business Climate Index improved to 114.6, its highest level since Germany was reunified in 1991. The election of Emmanuel Macron as the French president has boosted business confidence, as the German corporate sector is optimistic that Berlin and Paris can work together to improve the eurozone economy. France is Germany’s second largest trading partner and Macron underscored the importance he attaches to Franco-German relations when he visited German chancellor Angela Merkel within days of winning the presidency. The Brexit vote and Donald Trump’s “America first” agenda present serious challenges to the EU, and Merkel and Macron will have no problem seeing eye-to-eye in their desire to deepen European integration.

Federal Reserve policymakers find themselves in a quandary, as the US economy has been sending conflicting signals with regard to inflation and employment. The labor market remains red hot, as the unemployment rate fell to 4.4 percent in April, its lowest level since 2007. Problem is, inflation hasn’t kept up, and remains below the Fed target of 2 percent. The Fed minutes stated that the central bank plans to raise rates “soon”, and the odds of a June hike remain at about 78%, unchanged by the minutes. At the same time, the Fed has provided itself some wiggle room, and could opt to delay a hike until the second quarter if inflation or consumer indicators take an unexpected nosedive. As for additional hikes in 2017, the markets remain skeptical. The odds for a September rate stand at just 37%, with the markets unclear on whether the Fed will make further moves this year if inflation remains below the Fed target. Even if soft first quarter data was a blip, the markets (and possibly Fed policymakers) are concerned that President Trump, who is facing congressional investigations over his connections with the Russian government, may not be able to pass his agenda of cutting taxes and reigning in government spending. Gone are the heady days at the end of 2016, when a red-hot US economy had analysts predicting four rate hikes in 2017.

Soft End To The Week As Oil Drags

- Oil Bounces But Losses Weigh on Indices;

- FTSE Makes Small Gains as GBP Weakness Offsets Oil Moves;

- Could Gold Be Headed Towards $1,300?

- US GDP Data Eyed as Fed Seeks Reassurances on Q1.

As the week draws to a close, risk appetite appears to be drying up, not helped of course by recent moves in oil which is dragging on global benchmarks.

Oil has been one of the standout performers throughout May as traders banked on an extension to the deal between a number of OPEC and non-OPEC producers that came into effect earlier this year. The deal - which will see the 1.8 million barrel a day cut extended from the middle of this year to the first quarter of 2018 – was agreed between participating producers on Thursday, prompted a sudden and sharp sell-off in oil.

The reason for the sell-off was simple. There had been so much reported on the agreement in the weeks leading up to the meeting that it had been fully priced in. Once speculation became reality, there was no more gains to be had, not in the near-term anyway. Should we see full compliance and evidence that inventories are falling back towards their five year average, as intended, the prices may well creep higher once again. The result for now though has been a correction in oil prices which is weighing on energy stocks and therefore indices, particularly those with heavy exposure.

The FTSE 100, which ordinarily would be feeling the pain of this, is actually trading a little higher this morning. A second day of selling in the pound - this time driven by the latest poll numbers which show the gap between the Conservatives and Labour has shrunk to only five points from around 20 a couple of weeks ago – is more than compensating for the weakness in energy stocks and therefore helping to support the index.

Gold is benefiting from the more risk averse sentiment in the markets today, as well as the weakness in the US dollar which is off by around one fifth of one percent. Gold is currently trying to push its way through $1,265 which has been a tricky level for the yellow metal over the last few months. A move above here could see it test its 2017 highs just shy of $1,300.

It's been a relatively quiet morning on the newsflow and data side, with no numbers from Europe leaving traders looking to the US releases as we close out the week. A first revision of Q1 GDP will certainly be of interest as the Fed considers its second rate hike of the year at its next meeting in June. Policy makers have shown a clear desire to see evidence that the first quarter weakness was only transitory and an upward revision here may provide them with more comfort. Of course, the opposite is also true. We'll also get durable goods orders and consumer surveys from UoM this afternoon, while the leaders of the G7 are also due to meet in Italy.

Technical Outlook: Spot Gold Probes Above Multi-Day Congestion Tops At $1265

Spot Gold is probing above key $1265 barrier (Fibo 61.8% of $1295/$1214/multiple upside rejections/weekly cloud top) on fresh bullish recovery on Friday, in attempt to finally break above $1245/$1265 congestion that extends into seventh straight day.

Strong bullish setup of daily MA's is supportive for further advance, as 55SMA contained recent dips at $1247, guarding key support at $1245 (daily cloud base) and rising 10SMA that formed bull-cross with 55SMA, continues to underpin the action.

Fresh weakness of the dollar kept gold price on the front foot, with sustained break and close above $1265 pivot, expected to open next targets at $1270 (late Apr lower platform) and $1276 (Fibo 76.4% retracement.

The yellow metal is on track for the third consecutive bullish weekly close that supports scenario.

Broke daily cloud top at $1258 now acts as initial support ahead of rising 10SMA/daily Kijun-sen at $1251.

Res: 1267, 1270, 1276, 1280

Sup: 1262, 1258, 1253, 1251

Technical Outlook: USDJPY Falls Sharply On Fresh Risk Aversion

The pair was sharply down on Friday, driven increased risk aversion after President Trump’s comments on North Korea.

Fresh bears extended below 111.00 handle and touched Fibo 61.8% of 110.23/112.12 support, signaling that recovery phase off 110.23 (18 May low) may be over.

Repeated failures to break and close above daily cloud top (111.80) resulted in fresh weakness, as recovery rally stalled here, despite brief upticks above 112.00 barrier.

Daily studies are turning into bearish setup on latest weakness and signal increased risk of further easing which may result in full retracement of 110.23/112.12 corrective upleg and test of psychological 110.00 support, reinforced by 200SMA.

Corrective upticks on oversold near-term studies should be capped by broken daily Kijun-sen at 110.62 which guards daily cloud top barrier.

Res: 111.30, 111.62, 111.80, 112.12

Sup: 110.90, 110.50, 110.23, 110.00