Sample Category Title

Where Are The Hawks?

Where are the hawks?

With few hawkish surprises in the FOMC minutes, other than some more extensive than expected discussion around the balance sheet, the US dollar sold off as pre-event USD supportive positioning unwound

The Fed continued to downplay the listless Q1 US economic activity and softer inflation metrics as transitory which now accentuates the importance of next week's economic calendar.While, the market continues to view the Federal Reserve on track for a June lift off, but this decision may come down to the wire, with next Friday's payrolls, and specifically the wages growth component, providing a gentle nudge one way or another. While we maintain our base case for a June hike, the picture is a bit murky down the road and could continue to weigh negatively on the Greenback. There's still much ground to be covered, and despite the increased chance of a September balance sheet broadcast, but if the Feds can't convincingly guide us to an interest rate hike one month before the market event, one can only imagine the indecisions and market gyrations leading up to a possible taper.

In the meantime, price action remains 'passive' and 'stable' amidst growing ' uncertainty', words we seldom use in the same sentence when describing the market, but such is the reality of the current market conditions.

The China downgrade has had a minimal initial impact on the markets, as it wasn't too unexpected given the burdening debt load and in reality, China has negligible vulnerability or exposure to foreign investors, so the market quickly shrugged off the downgrade.

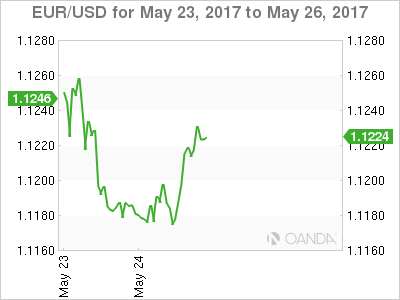

Euro

The Euro moved higher despite passive comments from ECB' members this week, which brings into question the recent build-up of short-term Euro longs to post the French election. However, it's more likely the market views the solid performance in Eurozone economic activity as speaking louder than words at this stage, and the EUR tone remains guardedly confident on expectations of shifting ECB language. While we're seeing an early buy into the Euro this morning, if the ECB headlines continue to reinforce a dovish stance, long positioning could evaporate quickly.

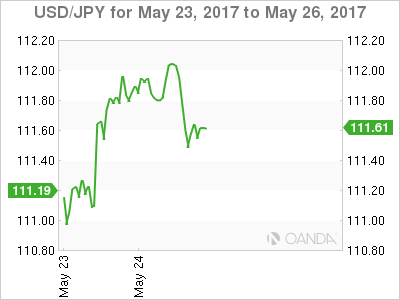

Japanese Yen

Dollar-yen movements are suggestive of position overhang from the near term short dollar view on the back of US political uncertainty and geopolitical risk in the Korean peninsula. The market may be stretched long JPY as a guard against a potential escalation of event risk, and now dealers find themselves reluctant to add to those positions and at the same time remain pessimistic on the USD.

With few catalysts to buy dollars from the Fed minutes, dealers remain in a state of limbo, eyeing headline risk on one screen while tracking US bond yields on the other.

While USDJPY has recovered well from the 111.00 level as US yields continue to provide surprising motivation as US yields rose following a soft Treasury Bill auction, but without the needed kick from the Feds or a rebound in sagging US economic data, the pair will continue to struggle above 112.00

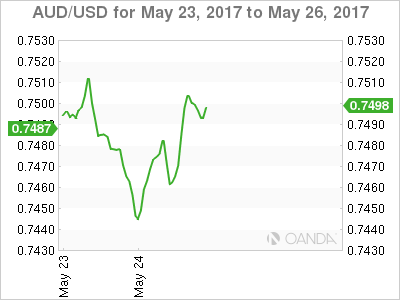

Australian dollar

Aussie came temporarily unhinged on the China downgrade as G10 dealers use AUD as a proxy for China risk, but the move was really all about the drop in Iron ore prices. Iron ore futures are struggling amidst report that mainland steelmakers are retooling to make better use of Scrap and when combined with iron ore inventories rising at 45 Chinese ports the current view for iron ore prices doesn't present a rosy picture.

Aussie has rebounded on less hawkish Fed minutes and a bounce in WTI as we approach the OPEC meeting.But will likely struggle, as it has so often of late, to gain any momentum above the .7500 handle more so as the iron or glut remains in focus.

Asia FX

Following up on relatively quiet Asia session yesterday when outside the PHP which broke the 50.00 level in the NDF markets on aggressive buying after the martial law declaration, trading was dead. However, overnight activity saw decent dollar selling interest on USDKRW and USDTWD, in part driven by exporter flow but magnified by a less hawkish Fed retort.

The Ringgit broke through the critical 4.29 level as oil prices continue to move higher ahead of the OPEC meeting. The bullish momentum keeps the MYR in favour for a catch-up play to regional currencies.

FOMC Minutes: Fed Outlines QT Principles And Expects To Hike ‘Soon’

On the rate hike outlook, 'most participants' (both covering voting and non-voting FOMC members) think a rate hike will be appropriate 'soon'. As mentioned in the statement, the FOMC members were not worried about the weak GDP growth in Q1, which they think is transitory and partly reflecting negative residual seasonality. The members also noted that the unemployment rate had dropped further below the Fed's NAIRU estimate of 4.7%. That said, 'a few participants' think it is a 'concern' that the progress on the inflation goal has slowed (and remember the meeting took place before the CPI data for April). Overall, the Fed admits it is in a difficult position. On the one hand the Fed should likely hike rates as it has met its employment objective; on the other, the Fed should be more cautious as it has missed its inflation target for eight years (except for a few months). Since the meeting, the problem has only worsened for the Fed. The jobs report for April showed the unemployment rate dipped to 4.4% (the lowest in a decade) while the CPI data for April surprised on the downside, as CPI core inflation dipped to 1.9% .

While consensus is that the Fed will hike at the June meeting, we are still more sceptical, because of both the weaker economic data and still too low inflation. However, we just think the Fed will wait until July, so it is not a given it should lead to a major reaction in the financial markets. Thus, it will not be a major surprise for us if the Fed decides to hike in June anyway, also given the current market pricing. By waiting until July, the Fed gets some more data points to ensure that inflation does not continue to surprise on the downside and that growth has rebounded in Q2 after the weak Q1. The reason why we think the Fed will still hike relatively soon is that it puts more weight on labour market data than inflation rates. Also, if the Fed hikes in June, it would indicate a hiking pace of four hikes per year (every other meeting), which is more than the Fed projected both in December and March (3 hikes per year). We expect the third hike this year to be in December.

Next year we now expect the Fed to hike three times (previously 3-4 times) due to a combination of the Fed's desire to shrink its balance sheet soon (see section below and the next page) and Trump's inability to deliver on Trumponomics (see analysis here).

Looking at the market pricing, we still think it is too the soft side. While the June hike is priced in by 80%, the markets have priced one and half hikes for the rest of the year and a total of 2.7 hikes from now until year-end 2018.

Fed outlines quantitative tightening principles

Before the release, we said we would look for any comments on the Fed's desire to reduce the size of its balance sheet (quantitative tightening) and we were not left disappointed. 'Nearly all' FOMC members think it would be appropriate to begin quantitative tightening later this year (most have indicated in speech end-2017 is most likely).

The minutes state that quantitative tightening will be conducted 'in a gradual and predictable manner'. The staff proposes that the FOMC announces a set of gradually increasing caps/limits on the dollar amounts of bonds that will be allowed to run off each month and only reinvest the amounts that exceeded the caps each month. The caps will be set at low levels and then raised every three months (corresponding to every other meeting, although the Fed will likely not vote on this every month, as many FOMC members have argued it should run in the background). When the final values of the caps are reached, the caps will be maintained and the balance sheet will continue to shrink until the target is reached.

The minutes also say that the FOMC members agreed to amend Committee's Policy Normalization Principles and Plans “soon”. We are still missing the triggers for actually starting quantitative tightening (based on the minutes from the March meeting, 'several participants' prefer a quantitative threshold, which could be either a certain Fed funds target range or an economic variable (unemployment rate or inflation) like the previous Evans's rule), caps sizes and increases and target for the future level of the balance sheet. The FOMC members agreed to continue the discussions at the June meeting.

We think this supports our view that the Fed will come with the big announcement of the triggers for starting quantitative tightening in connection with the June meeting. Although the Fed strongly signals the beginning of quantitative tightening this year, we hold onto our long-held view that it will actually start in Q1 18 for now. We expect the Fed to begin very gradually by a smaller amount than what the Fed bought per month under the QE1 programme (USD30bn per month) but with the idea of increasing caps the amount may rise above this threshold during the reduction phase. In an optimistic scenario the Fed can reduce its balance sheet by USD1,700bn, in our view.

We have written extensively about the QT theme this year: Fed's Quantitative Tightening: Fixed Income Implications (6 April), FOMC Minutes: Quantitative tightening is moving closer (5 April) and Research US: Fed's regulatory hurdle for starting quantitative tightening (13 March).

Recent US research

- Research US: Trump's budget dead on arrival in Congress – do not expect too much of Trumponomics (24 May)

- FOMC review: Fed thinks weak GDP growth in Q1 was transitory (3 May)

- Fed's Quantitative Tightening: Fixed Income Implications (6 April)

- FOMC Minutes: Quantitative tightening is moving closer (5 April)

- Research US: Fed's regulatory hurdle for starting quantitative tightening (13 March)

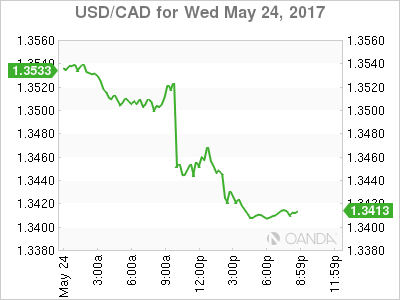

USD/CAD Canadian Dollar Higher After Central Bank Holds Rate

The Bank of Canada kept rates unchanged but statement was not all dovish

The Canadian dollar is higher against the US dollar after the Bank of Canada (BoC) kept rates unchanged at 0.50 percent. The release of minutes from the Fed’s May meeting was full of surprises, but still felt short of the market expectations which are pricing in a rate hike in the upcoming June 13/14 Federal Open Market Committee (FOMC) meeting.

The BoC managed to balance its dovish assessment of the economy with the potential opportunity as there is still excess capacity. The housing market remains a concern as it is too early to tell if the latest moves by the provincial government in Ontario after following the lead of British Columbia and the problems at Home Capital Trust have had a real impact on prices. The central bank has put rate cuts off the table since earlier this year, but there are no real possibilities of a rate hike until 2018. Trade will remain a challenge as the US has begun the 90 day period before holding a renegotiation meeting with Canada and Mexico.

The Fed Minutes released today brought insights about the central bank’s next steps on rate policy and its balance sheet reduction plans. Fed members discussed that a rate hike would be appropriate soon. The market agrees, already pricing in a 83.1 percent probability of a rate hike in the upcoming June FOMC meeting, although through to its cautious nature the Fed did add that it would have to be dependant on strong economic data. Central bank officials are calling the slowdown in the first quarter as transitory and expect the US economy to recover. The Fed surprised with a lot of details on their plans to shrinks their balance sheet. A three month increasing cap seems to be the plan going forward until reaching normalization.

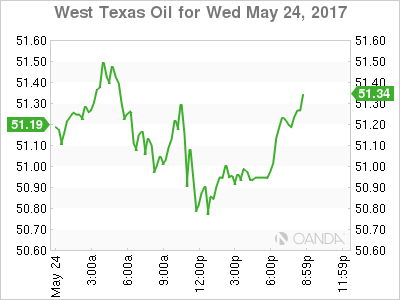

Oil prices had initially risen with the combination of the bigger than expected drawdown in US weekly inventories and the upcoming meeting between Organization of the Petroleum Exporting Countries (OPEC) and other major producers in Vienna to discuss the extension to the production cut agreement put in place in January of this year. The agreement has stabilized prices but rising US production has kept crude at around current levels which is why an extension and a possible further decrease in supply might be needed.

The USD/CAD lost 0.436 percent in the last 24 hours. The currency pair is trading at 1.3437 after the decision from the Bank of Canada (BoC) to leave benchmark rates untouched at record low 0.50 percent. The price of oil also boosted the loonie against the US dollar with the bigger than expected drawdown of 4.4 million barrels. The minutes form the U.S. Federal Reserve meeting in May were also released today, but although they kept the June rate hike on the table did not sway the market who has already priced in that decision by the central bank.

The price of oil lost 0.227 percent on Wednesday. The West Texas Intermediate is trading at $50.97 after the US weekly inventories were even lower than expected ahead of the Organization of the Petroleum Exporting Countries (OPEC) meeting on Thursday. The producers appear to be ready to extend by 6 to 9 months their historic deal to cut 1.8 million barrels per day but deeper cuts are still not ruled out as the final decision is yet to reached according to reports from Vienna.

Market events to watch this week:

Thursday, May 25

- 4:30 am GBP Second Estimate GDP q/q

- All Day ALL OPEC Meetings

- 8:30 am USD Unemployment Claims

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

Gold Flat as Federal Reserve Minutes Loom

Gold is showing little movement in the Wednesday session. In North American trade, spot gold is trading at $1251.36 an ounce. On the economic front, Existing Home Sales dropped sharply to 5.57 million, short of the forecast of 5.65 million. Later in the day, the Federal Reserve will release the minutes of its May policy meeting. On Thursday, the US will publish unemployment claims.

All eyes are on the Fed minutes, with the markets hoping to glean some clues about the timing of future rate moves. The Federal Reserve raised rates back in March, and the markets expect the Fed to press the rate trigger at the June policy meeting. The odds of a rate hike have increased to 83%, according to the CME Group. Just last week, the likelihood of a rate increase stood at 73%. Despite the market speculation, Fed policymakers are keeping their cards close to their chest, at least in their public appearances. On Tuesday, Philadelphia Fed President Patrick Harker said that a June move was a "distinct possibility", but cautioned that a weak inflation report could delay a rate hike. Earlier in the week, Robert Kaplan, President of the Dallas Fed, stated that three interest increases in 2017 was "appropriate". The Fed minutes are expected to underscore support for a June move, but may not shed much light on what happens after that. Still any clues about the Fed's rate plans could shake up the currency markets.

The markets are keeping a close eye on the Federal Reserve, which will release the minutes of the May policy meeting. June has been circled as the next rate move, although Fed policymakers have kept their cards close to their vests. On Tuesday, Philadelphia Fed President Patrick Harker said that a June move was a "distinct possibility", but cautioned that a weak inflation report could delay a rate hike. Earlier in the week, Robert Kaplan, President of the Dallas Fed, stated that three interest increases in 2017 was "appropriate". The minutes are unlikely to contain any major surprises, but could underscore support for a June move. Gold prices move inversely to interest rate moves, so any clues about further rate hikes this year could send gold to lower levels.

On Tuesday, the White House presented President Trump's 2018 budget proposal to Congress. Trump has promised to slash government spending, and the budget proposes major cuts to the Medicaid health program, disability benefits and food stamps. Trump has outlined an ambitious program to cut government spending by $3.6 trillion in the next 10 years and achieving a balanced budget by 2020. The budget also includes $25 billion for paid leave after childbirth and some $200 billion for infrastructure programs. It's a safe bet that Trump's budget will face tough opposition on Capitol Hill, with both Democrats and Republicans unlikely to go along with such deep cuts to social assistance programs. Still, with the Trump administration beset by Congressional investigations, the White House can point to the budget as a step forward in his agenda to cut government spending.

Pound Stays Close to 1.30, Markets Eye British GDP

GBP/USD has inched lower in the Wednesday session. In the North American session, the pair is trading at 1.2950. On the release front, there are no British events on the schedule. In the US, Existing Home Sales dropped sharply to 5.57 million, short of the forecast of 5.65 million. Later on, the Federal Reserve will release the minutes of its May policy meeting. On Thursday, the UK releases Second Estimate GDP, while the US will publish unemployment claims.

The British pound is having an uneventful week, but the situation in the UK is anything but quiet. The country is badly shaken after a horrific bombing at a Manchester rock concert killed 22 and injured 120 people. It was the worst terrorist attack on British soil since a bombing in London in 2005. The British government raised the terror threat level to "critical", the highest level. This move has raised speculation that another terror attack could be imminent on British soil. The attack has led to the suspension of the election campaign, with just 15 days to go before the vote. Prime Minister Theresa May is expected to win the election, but further attacks could rattle confidence in the government and shrink May's lead in the polls.

All eyes are on the Fed minutes, with the markets hoping to glean some clues about the timing of future rate moves. The Federal Reserve raised rates back in March, and the markets expect the Fed to press the rate trigger at the June policy meeting. The odds of a rate hike have increased to 83%, according to the CME Group. Just last week, the likelihood of a rate increase stood at 73%. Despite the market speculation, Fed policymakers are keeping their cards close to their chest, at least in their public appearances. On Tuesday, Philadelphia Fed President Patrick Harker said that a June move was a "distinct possibility", but cautioned that a weak inflation report could delay a rate hike. Earlier in the week, Robert Kaplan, President of the Dallas Fed, stated that three interest increases in 2017 was "appropriate". The Fed minutes are expected to underscore support for a June move, but may not shed much light on what happens after that. Still any clues about the Fed's rate plans could shake up the currency markets.

With President Trump still overseas on his first presidential trip, the White House presented Trump's 2018 budget proposal to Congress on Tuesday. Trump has promised to slash government spending, and the budget proposes major cuts to the Medicaid health program, disability benefits and food stamps. Trump has outlined an ambitious program to cut government spending by $3.6 trillion in the next 10 years and achieving a balanced budget by 2020. The budget also includes $25 billion for paid leave after childbirth and some $200 billion for infrastructure programs. It's a safe bet that Trump's budget will face tough opposition on Capitol Hill, with both Democrats and Republicans unlikely to go along with such deep cuts to social assistance programs. Still, with the Trump administration beset by Congressional investigations, the White House can point to the budget as a step forward in his agenda to cut government spending.

Bank of Canada: Policy Appropriate “At Present”

Our Take

The Bank made a subtle change in today's statement having maintained the overnight rate at 0.5% but stipulating that the degree of policy support remains appropriate "at present".

The tone of the Bank's assessment appears to be more upbeat as policymakers gave a nod to both global and domestic conditions having improved with the Bank anticipating "very strong growth in the first quarter". Moderating this enthusiasm was the persistence of subdued wage growth and core infla- tion measures remaining below 2%.

There have signs that the economy built a good head of steam over recent quarters and that the hand off to the second quarter was solid. Hours worked recovered in April and an alternative measure of wag- es showed growth averaged closer to 2% in recent months. Our monitoring of the data points to growth in the economy having strengthened with real GDP growth topping 4% in the first quarter driven by on- going household spending strength and a recovery in business investment.

While current conditions were viewed more positively, the Bank continues to be concerned about the uncertainties associated with US economic policy and specifically cited competitiveness challenges faced by Canadian exporters. The Bank said recent regulatory changes have not yet resulted in a "substantial cooling" in housing market activity. We expect that the rule changes to be sufficient to slow housing market activity but as long as expectations for rates to remain low persist, the risks is that hot markets will stay on a slow burn and do not expect consumer spending growth to weaken significantly. With business investment picking up in the first quarter, the opportunity for the Bank to shift the drivers of growth away from the financially extended consumer may be in the offing. The Bank acknowledged that the current degree of monetary policy support is needed today, however should the economy continue along this stronger growth path, we think it likely the Bank will shift away from its neutral stance and maintain our view that the Bank will be in position to raise the overnight rate in the first half of next year.

Technical Outlook: USDCAD Fell Sharply after BoC

The pair fell sharply after Bank of Canada left interest rates unchanged at 0.50% as expected, but the greenback came under increased pressure after downbeat US Housing data in April.

Loonie hit fresh one-month high against the greenback at 3.3430, which lies near strong support provided by Fibo 61.8% of 1.3222/1.3793 rally.

Weakening daily studies suggest further downside which requires close below 1.3440 Fibo 61.8% support for bearish signal and may extend towards 1.3345/1.3300 (100 / SMA's respectively).

FOMC minutes are next event that may further impact pair's near-term performance.

Res: 1.3482; 1.3527; 1.3540; 1.3575

Sup: 1.3430; 1.3410; 1.3345; 1.3300

Bank of Canada Poloz Holds the Line with a Neutral Statement

As was universally expected, the Bank of Canada maintained its key policy interest rate at 0.50%. The short statement accompanying the decision struck a neutral tone.

The statement highlighted a number of perceived positives: a global economy that "continues to gain traction" and an expected rebound in U.S. economic growth after a weak first quarter. Domestically, the adjustment to lower oil prices is seen as largely in the rear view, and recent economic data is seen as encouraging, helped by improvements in labour markets that are broadening.

Balancing the positives are subdued wage and price growth, which are viewed as consistent with ongoing excess capacity in the economy. The uncertainties highlighted in the Bank's April Monetary Policy Report remain in place, and export growth remains modest in the face of "ongoing competitiveness pressures". Finally, macroprudential measures are expected to contribute to more sustainable debt profiles, but are not seen to have had any meaningful cooling effect to date.

Key Implications

Canadian growth may be coming in hot, but the Bank of Canada is not. Despite signs of still robust economic growth in Canada, Governor Poloz chose to once again strike a cautious, if balanced, tone.

The short statement accompanying today's decision covered both sides of the ledger, acknowledging the positive tone of recent Canadian data, but also highlighting areas of concern. The risks posed by the housing sector remain tangible given the lagged impacts of macroprudential policies, and crucially, price pressures, whether in terms of wages or inflation, are largely nonexistent at the moment.

Indeed, the Bank's core mandate is to control inflation over the medium term. Healthy economic growth of late has yet to translate into meaningful price pressures with several of the Bank of Canada's preferred measures actually softening in recent months. This should not be surprising, given significant economic setbacks in recent years and the lags between economic growth and inflation. As we move into early 2018, the strong economic growth of recent quarters should begin translating into inflationary pressures, motivating the start of a gradual tightening cycle.

Dollar Stays Off Recent Lows, But No Further Gains

- European equities traded sideways and are currently marginally down, while US equities open marginally higher and are a whisker away from all -time highs.

- U.S. home sales fell more than expected in April, weighed down by a shortage of houses on the market. Existing home sales declined 2.3 percent to a seasonally adjusted annual rate of 5.57 million units. Despite the decline, April's sales pace was the fourth highest over the past 12 months.

- Sweden's central bank is once again ramping up the pressure on the government to do more to address the country's rapidly-rising debt levels, warning that the issue poses "a serious threat to financial and macroeconomic stability

- The reliance of the eurozone's financial system on the policies of its central bank have been laid bare in the European Central Bank's latest financial stability review, which highlights the risks posed by attempts to rein in extraordinary monetary stimulus.

- The Bank of Canada as expected kept its policy rate unchanged at 0.5%. The Bank still sees current monetary stimulus as appropriate. The bank sees recent economic data as encouraging, but the uncertainties flagged in April are still clouding the outlook.

Listless bond trading awaiting FOMC minutes.

In a news-poor session, core bonds traded quietly. US yields are very little changed while German yields are modestly lower. US Treasuries hovered listless in a very tight 4/32 range, awaiting the FOMC Minutes. The Bund opened a little lower, but soon went higher. However, gains were limited and in the afternoon the Bund faded, losing most of the small morning gains. Comments of ECB Praet and Draghi were interesting (see below), but unable to impact markets. At the time of writing, US yields barely moved and yield changes vary from +0.6 bp (2-yr) to -1.4 bp (30-yr). German yields fell between 1.2 and 2.3 bps, flattening the curve.

In EMU bond markets 10-yr yield spreads narrowed about 3 bps across the board with Portugal (+6 bps) and Greece (+20 bps) underperforming. In case of Portugal, it might be due to news that it wants to pay back IMF loans. Markets expect more supply. Greece is still reeling from the absence of an agreement between its creditors.

ECB Praet sounded optimistic on growth as he sees an increasingly solid recovery which is remarkable resilient to external shocks. He wants to see the good surveys translated in hard data. Q1 was already strong, but we think that Praet wants a confirmation from Q2 GDP. He sees the output gap closing in 2019 when price pressures will increase and the ECB objective will be fulfilled. He added that underlying inflation is still low. "It's a debate for the coming weeks, coming months to say to what extent we have confidence in" the projected path of inflation and "to what extent --if you start withdrawing accommodation -- this inflation path is sustained" So, now even the very dovish and influential ECB member is ready to question short term the path the ECB will follow in his policy.

Draghi said "Asset purchases are inevitably more difficult to calibrate, more complex to implement, and more likely to produce side-effects than other instruments, including moderately negative rates" He clearly restates the sequence of the exit policy: First ending QE, later reversing negative rates.

Dollar stays off recent lows, but no further gains

Today, the dollar maintained most of yesterday's late session gains, but there was no news to inspire additional follow-through gains. EUR/USD stabilizes in the high 1.11 area. USD/JPY is changing hands around 111.80. The FOMC minutes to be published later on will probably decide the fate.

Overnight, Asian equities showed a mixed picture. USD/JPY traded in the high 111 area going into the European open. The China rating downgrade put temporary pressure on the Aussie dollar. AUD/USD dropped to the 0.7450 area, but the Asian losses were reversed later in the session. EUR/USD held a tight range in the 1.1180 area after yesterday's setback.

There was hardly any news to guide trading in the major FX cross rates in Europe. European equities held a sideways trading pattern near yesterday's closing levels. The dollar maintained yesterday's gains against the euro and the yen. USD/JPY tried a shy attempt to regain the 112 mark, but failed. ECB Praet's Praet suggested that the ECB might reconsider some elements of its ultra-easy in the near future. However, the euro hardly reacted.

There were also no US data releases. US equities opened marginally higher, near the highs, but the moves in equities, yields and FX remain very limited. EUR/USD trades in the 1.12 area. USD/JPY is seen in the d 111.75/85 area. The FOMC minutes later this evening might decide if there is room for a USD rebound.

EUR/GBP rebound takes a breather

Today, there were no eco data or other events with market moving potential in the UK. Technical considerations and the price moves in the euro and the dollar drove sterling trading. The terror warning had hardly any impact on the UK currency. Early this morning, yesterday's EUR/GBP correction went a bit further, but new buying interest already kicked in just north of the 0.86 big figure. An intraday bottoming out in the EUR/USD also prevented further EUR/GBP losses. The pair is again trading in the 0.8640/50 area. So, the EUR/GBP uptrend isn't broken yet. Cable again tried to regain the 1.30 barrier after yesterday's setback, but the attempt failed again as the dollar was in (slightly) better shape compared to of late. Cable trades again in the 1.2950 area.

PRE FOMC Coverage: EUR/USD Bearish Head and Shoulders For Possible Drop

On hawkish FOMC, the EUR/USD could drop from POC and POC2. POC 1.1180-1.1200 (D H3, Top of Left Shoulder, ATR Pivot) could reject the price lower towards 1.1150 and 1.1080. In the case of deeper retracement (less hawkish FOMC or dovish FOMC) the POC2 1.1220-30 (D H4, ATR Pivot) could reject the price down IF the price stays below 1.1270. Above 1.1270, 1.1300 should be exposed.