Sample Category Title

EURUSD May Be In For A Reversal

On the 4h chart of EUR/USD, we can see that price made a sharp structure from around the 1.0604 region which is now viewed as wave C) of Y. That said this whole correction since December of last year that is in motion is known as a double zig-zag, which may be trading in final stages as we already see sub-wave C) unfolding a minor five wave move within itself. As such a reversal to the downside may be around the corner, ideally around the Fibonacci ratio of 100.0

EURUSD, 4H

The ECB’s Bank Lending Survey Is Due For Release

Market movers today

The ECB's Bank Lending Survey is due for release. The latestreport from January showed that loan growth continued to be supported by increasing demand across all loan categories, while creditst andards (i.e. banks' internal guidelines or loan approval criteria) for loans to enterprises tightened somewhatin net terms due to banks' lower willingness to tolerate risk.

Rate decision in Hungary. We expect the National Bank of Hungary (NBH) to keep its base rate unchanged at 0.9% today. The inflation rate rose to 2.9% y/y in February, near the central bank target of 3%. However, the rise in inflation so far is driven mainly by a base effect of energy prices, and thus no imminent pressure for higher interestrates.

In the US, Conference Board for April is due. The indicator is at very high levels and although we do notexpect to see a significant decline, we would also not be surprised to see a small decline given the historically high levels. In general, we have seen a divergence between 'hard' and 'soft ' data in recent months, when soft data has been strong and hard data weak. Softdata indicates growth in the region of 1.5-2.0%, while the Fed At lanta GDP nowcastshows growth in Q1 of 0.5% q/q AR.

In Sweden, unemployment figures are due . For more on the Scandi region, see p.2.

Selected market news

The very strong risk relief rally in Europe yesterday post the firstround of the French presidential election continued in the US session with Dow Jones and S&P500 closing 1% higher, and markets in Asia are also trading higher this morning. In fixed income markets, yields on German government bonds rose some 9-11bp across the curve while the 5Y OAT -Bund spread tightened 25bp and is now back at a level last observed at the end of last year, meaning any French political risk premium is gone.

The election outcome was in line with prior opinion polls, and yesterday's strong risk rally could indicate thatinvestors were caught on the wrong foot and/or markets now see Macron winning the presidency as a done deal. New polls released yesterday confirmed a solid 60% to 40% lead for Macron versus Le Pen in the second run-off on 7 May, and comments in the media also suggest that most political commentators see Macron winning in the second round.

However, while the risk rally could continue in the coming days, we still see a risk of volatility rising again driven by profit taking and risk reduction going into the second round on 7 May. Moreover, our equity strategy team still holds the view thatequity markets will soon be back focusing on growth.

With political uncertainty related to the French presidential election cleared (for now at least ), focus is likely to turn to the US, where President Trump has announced that he will present his tax plans on Wednesday. According to the media, Trump will call for cutting taxes for individuals and lowering the corporate rate to 15%. Moreover, the Trump administration yesterday said it will impose new tariffs on imports of Canadian softwood lumber. This marks the latestexample of the new administration taking a tougher stance on trade practices that the US considers unfair. Last and not least , the mostrecent government funding bill expires on Friday 28 April. If both chambers fail to approve a new funding bill before midnight on Friday 28 April, the government would run out of money to pay its bill and a shutdown would begin.

Market Update – Asian Session: Trump Keeps The Pressure On North Korea

Asia Mid-Session Market Update: Trump keeps the pressure on North Korea, defers on border wall funding;  CAD under pressure as US protectionism looks north

US Session Highlights

(US) Mar Chicago Fed National Activity Index: 0.08 v 0.50e

(US) APR DALLAS FED MANUFACTURING ACTIVITY: 16.8 V 17.0E; New order growth rate: 5.1 v 3.2 prior

US and EU stocks were given a boost of confidence today after yesterday's first round of French presidential elections put mainstream candidate (and likely eventual winner) Macron into the second round. Investors returned to risk in a big way, sending the Dow to jump 176 points at the open. Financials were the outperforming sector for the S&P, gaining 2.27%. Fixed income continued to pay the price, as the 10-yield rose back above 2.30%.

US markets on close: Dow +1.1%, S&P500 +1.1%, Nasdaq +1.2%

Best Sector in S&P500: Financials

Worst Sector in S&P500: Real Estate

Biggest gainers: BCR +19.5%; HAS +5.7%; XLNX +3.0%

Biggest losers: BDX -4.4%; KIM -2.9%; MU -2.8%

At the close: VIX 10.8 (-3.8pts); Treasuries: 2-yr 1.23% (+4.5bps), 10-yr 2.27% (+3.7bps), 30-yr 2.93% (+3.2bps)

US movers afterhours

UIS Reports Q1 $0.30 v $0.11 y/y, R$664.5M v $626Me (1 est)- Affirms FY17 R$2.65-2.75B v $2.70Be, FCF $130-170M (prior R$2.65-2.75B, FCF $130-170M); +12.6% afterhours

LLNW Reports Q1 $0.02 v $0.00e, R$44.7M v $43.4Me; +11.6% afterhours

HUM Pre-announces Q1 $2.75 v $2.43e, R$13.5B v $13.6Be; Raises FY17 guidance; +2.8% afterhours

WHR Reports Q1 $2.50 v $2.67e, R$4.79B v $4.76Be; Cuts FY17 GAAP guidance; -1.8% afterhours

ABX Reports Q1 $0.14 v $0.24e, R$1.99B v $2.18Be; -3.6% afterhours

ESRX Reports Q1 $1.33 v $1.32e, R$24.7B v $25.0Be; discloses Anthem intends to move its business when the current contract expires in 2019; -14.9% afterhours

Politics

(US) Pres Trump believes he can get funding for the border wall either now or in Sept - One America News Network

Key economic data

(JP) JAPAN MAR PPI SERVICES Y/Y: 0.8% V 0.7%E

(KR) South Korea Mar Consumer Confidence: 101.2 v 96.7 prior (6-month high)

Asia Session Notable Observations, Speakers and Press

Asian indices continued to trend higher, tracking outsized rally on Wall St on the heels of market-friendly French presidential elections Round 1 results. Hang Seng is up nearly 1% with banks leading the way, while Nikkei225 remains supported by softer JPY. Japanese Telecoms are particularly soft on speculation of discounting due to competition in the sector, and industrials are performing strongly. Australia is on holiday for Anzac day.

In FX, EUR and AUD were rangebound against the greenback, while NZD retreated below $0.70. Kiwi weakness partially attributed to trade protectionism stateside, as US Commerce Ministry determined that Canada softwood lumber exporters get subsidies, applying a 20% tariff, also warning it may put an import tax on Canadian dairy products. USD/CAD spiked up over 50pips above 1.3550 - highest level since late December on the protectionist posturing, just as Canada govt ministers Freeland (Foreign Affairs) and Carr (Natural Resources) condemn "unfair and punitive" dutes on softwood lumber.

US political risk of govt shutdown was dialed down to a simmer, with US President Trump claiming he could wait on funding the southern border wall to avert an impasse with Congress. Geopolitics on the Korean peninsula remain tense however as US administration officials will hold a session with the full Senate abouth the North Korea threat on Wednesday.

China

(CN) China said to have indicted former Stats Bureau head Wang on bribery - Chinese press

(CN) China issues plan for medium and long term auto sector development

Japan

(JP) Japan Fin Min Aso: Economy has prospered due to benefits of free trade

(JP) BOJ Dep Gov Iwata: Doing internal simulations of exit from QE; Too early to discuss exit externally

Korea

(US) President Trump has called on the UN Security Council to be prepared to impose additional sanctions against North Korea’s nuclear and ballistic missile programs; Says now is the time to solve the problem of North Korea - financial press

(KR) South Korea Nuclear Envoy Chief: Discussed with US, Japan counterparts ways to gain cooperation from China and Russia on North Korea

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.8%, Hang Seng +0.9%, Shanghai Composite +0.4%, ASX200 closed, Kospi +0.5%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.2%, FTSE100 +0.3%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0850-1.0870; JPY 109.60-110.20; AUD 0.7550-0.7570; NZD 0.6985-0.7015

June Gold -0.2% at 1,275/oz; June Crude Oil +0.5% at $49.46/brl; July Copper +0.7% at $2.58/lb

SPDR Gold Trust ETF daily holdings rise 1.5 tonnes to 860.2 tonnes; 2nd straight increase

Goldman Sachs continues to expect pressure in Gold prices with 3-month target of $1,200/oz; Medium term target remains at $1,250/oz - press

(CN) PBOC SETS YUAN MID POINT AT 6.8833 V 6.8673 PRIOR; Weakest Yuan fix since Apr 18th; biggest margin of weakness since Mar 7th

(CN) PBOC to inject combined CNY80B v CNY30B prior in 7-day, 14-day and 28-day reverse repos, 6th straight injection

Asia equities / Notables / movers by sector

Japan

JSR (4185) +0.9%; FY16/17 results

NEC (6701) +3.8%; FY16/17 results

Lixil (5938) -4.3%; FY16/17 results

Kose (4922) +1.2%; FY16/17 results

NTT Docomo (9437) -2.1%; FY17 results speculation

Mazda (7261) +1.8%' FY17 result speculation

Hong Kong

AAG Energy (2686) -1.6%; Q1 results

Northeast Electric Development (42) +0.9%; Q1 results

Korea

Korea Zinc (010130) +2.3%; Q1 results

SK Innovation (096770) +3.0%; Q1 results

SK Hynix (000660) -0.8%; Q1 results

Aussie Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the AUD rose 0.19% against the USD and closed at 0.7567.

On the economic front, in China, Australia's largest trading partner, the leading economic index rose 0.9% on a monthly basis in March. In the previous month, the index had climbed by a revised 1.3%.

LME Copper prices rose 0.2% or $11.0/MT to $5612.0/MT. Aluminium prices declined 0.2% or $4.5/MT to $1928.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7559, with the AUD trading 0.11% lower against the USD from yesterday's close.

The pair is expected to find support at 0.7541, and a fall through could take it to the next support level of 0.7522. The pair is expected to find its first resistance at 0.7581, and a rise through could take it to the next resistance level of 0.7602.

Moving ahead, traders would keep a close watch on a speech by the Reserve Bank of Australia's (RBA) Governor, Philip Lowe along with the release of Australia's consumer price index for 1Q, both due tomorrow.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

German Business Confidence Climbed To Its Highest Level Since July 2011 In April

For the 24 hours to 23:00 GMT, the EUR rose 0.26% against the USD and closed at 1.0867, after Germany’s Ifo business climate index surprisingly jumped to a level of 112.9 in April, strengthening to its highest level in nearly 6 years, indicating that businesses are brushing off concerns about the threat of rising protectionism and uncertainties linked to Brexit as well as major European elections. The index registered a revised reading of 112.4 in the prior month, while markets expected for a steady reading.

Additionally, the nation’s Ifo current assessment index unexpectedly rose to a level of 121.1 in April, defying market expectations of a fall to a level of 119.2 and following a revised level of 119.5 in the previous month. On the other hand, the Ifo business expectations index unexpectedly eased to a level of 105.2 in April, contradicting market consensus for a rise to a level of 105.9, thus suggesting that firms remained cautious about the nation’s future economic outlook. The index recorded a level of 105.7 in the previous month.

Separately, the German Bundesbank indicated in its monthly report that high industrial orders, exceptionally optimistic manufacturing sentiment and a rebound in exports supported German economic growth during the first quarter. However, the bank warned that German GDP potential is likely to fall to 0.75% per year by 2025 from around 1.25% at present due to the nation’s aging labour force.

In economic news, the US Chicago Fed national activity index unexpectedly declined to a level of 0.08 in March, compared to a revised level of 0.27 in the previous month. Investors had envisaged for an advance to a level of 0.50. Further, the nation’s Dallas Fed manufacturing business index surprisingly dropped to a level of 16.8 in April, compared to market expectations of an advance to a level of 17.0. In the previous month, the had registered a reading of 16.9.

In the Asian session, at GMT0300, the pair is trading at 1.0861, with the EUR trading 0.06% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.0828, and a fall through could take it to the next support level of 1.0794. The pair is expected to find its first resistance at 1.0886, and a rise through could take it to the next resistance level of 1.0910.

With no major economic releases in the Euro-zone today, investors will look forward to the US consumer confidence index for April, new home sales for March and house price index for February, all slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the GBP declined 0.08% against the USD and closed at 1.2785.

On the economic front, UK’s CBI industrial trends total orders decreased more-than-anticipated to a level of 4.0 in April, from a reading of 8.0 in the previous month and compared to market expectations of a drop to a level of 5.0.

In the Asian session, at GMT0300, the pair is trading at 1.2780, with the GBP trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2755, and a fall through could take it to the next support level of 1.2731. The pair is expected to find its first resistance at 1.2818, and a rise through could take it to the next resistance level of 1.2857.

Going ahead market participants will focus on UK’s public sector net borrowing data for March, scheduled to release in a few hours.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.18% against the JPY and closed at 109.81.

Macroeconomic data indicated that Japan's final leading economic index fell less than initially estimated to a level of 104.8 in February, compared to a drop to a level of 104.7 in the preliminary print and following a reading of 104.9 in the prior month. Also, the nation's final coincident index was revised higher to a level of 115.3 in February, compared to revised level of 113.3 in the flash estimate. In the previous month, the index had recorded a level of 115.1.

In the Asian session, at GMT0300, the pair is trading at 110.07, with the USD trading 0.24% higher against the JPY from yesterday's close.

The pair is expected to find support at 109.65, and a fall through could take it to the next support level of 109.22. The pair is expected to find its first resistance at 110.42, and a rise through could take it to the next resistance level of 110.76.

Looking ahead, Japan's small business confidence index for April and all industry activity index for February, both set to release tomorrow, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

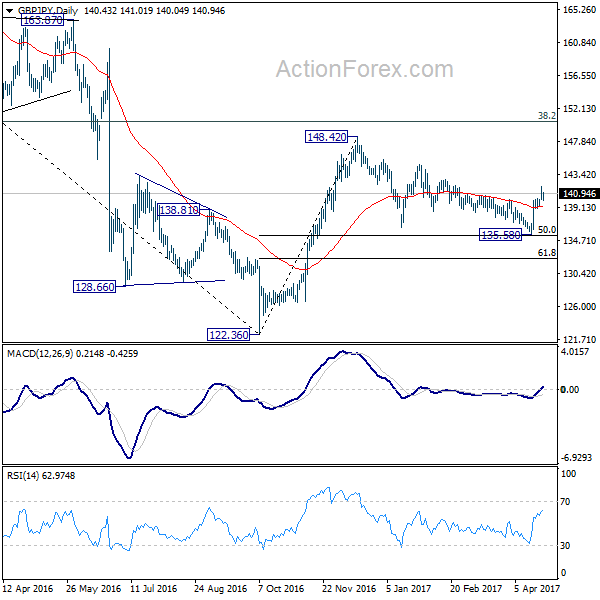

GBP/JPY Daily Outlook

Daily Pivots: (S1) 139.72; (P) 140.88; (R1) 141.58; More....

With 139.19 minor support intact, intraday bias in GBP/JPY remains on the upside for 144.77 resistance. Consolidation pattern from 148.42 should have completed three waves down to 135.58, after hitting 135.39 fibonacci level. Break of 144.77 should extend whole rise from 122.36 through 148.42. On the downside, break of 139.19 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.

Swiss Franc Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the USD slightly declined against the CHF and closed at 0.9958.

In economic news, Switzerland’s total sight deposits rose to a level of CHF569.1 billion in the week ended 21 April, from a level of CHF567.1 billion in the previous week.

In the Asian session, at GMT0300, the pair is trading at 0.9961, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9933, and a fall through could take it to the next support level of 0.9904. The pair is expected to find its first resistance at 0.9985, and a rise through could take it to the next resistance level of 1.0008.

With no economic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

US To Impose 20.0% Duties On Canadian Softwood Lumber

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the CAD and closed at 1.3514. The Canadian Dollar lost ground after the US announced its first batch of duties on imported wood from Canada.

The US Commerce Secretary, Wilbur Ross, stated that his agency will impose new anti-subsidy tariffs averaging 20.0% on Canadian softwood lumber imports, thus intensifying the long-running trade dispute between the two nations.

In the Asian session, at GMT0300, the pair is trading at 1.3549, with the USD trading 0.26% higher against the CAD from yesterday’s close.

The pair is expected to find support at 1.3452, and a fall through could take it to the next support level of 1.3354. The pair is expected to find its first resistance at 1.3603, and a rise through could take it to the next resistance level of 1.3656.

In absence of any major economic releases in Canada today, trading trend in the CAD is expected to be determined by global macroeconomic events.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.