Sample Category Title

GOLD – Bearish, Risk Turns Lower On Correctiongold

GOLD - The commodity weakened after failing to strengthen further on Wednesday. On the downside, support comes in at the 1,270.00 level where a break will turn attention to the 1,260.00 level. Further down, a cut through here will open the door for a move lower towards the 1,250.00 level. Below here if seen could trigger further downside pressure targeting the 1,240.00 level. Conversely, resistance resides at the 1,290.00 level where a break will aim at the 1,300.00 level. A turn above there will expose the 1,310.00 level. Further out, resistance stands at the 1,320.00 level. All in all, GOLD looks to weaken further.

Elliott Wave View: INDU More Downside

Short term Elliott Wave view in INDU ( Dow) suggest that instrument is showing 5 swings sequence from 3/03 peak (21018) favoring more downside. From 3/03 peak INDU is following a Double three Elliott wave Structure , where Minor wave W ended at 20579 low and Minor wave X ended at 20887 peak. Index has since broken below the 20412 low, suggesting the next leg lower in Minor wave Y has started already. The Internal Subdivision of Minor wave Y is also unfolding as Double three Elliott wave structure where Minute wave ((w)) ended at 20453 and Minute wave ((x)) ended at 20645 peak. Below from there, index is following another double three Elliott wave structure in Minute wave ((y)) lower, where Minutte wave (w) is expected to end in between 20378-20315 area then should see a bounce in Minutte wave (x) before further downside is seen. Near term, while bounces stays below 20645 peak and more importantly below 20887 peak index has scope to extend lower 1 more leg lower at least. we don’t like selling the index.

Dow 1 hour Elliott Wave Chart

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD,AUDUSD, GBPCAD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EURUSD pair eased from Tuesday's fresh nearly three-week high at 1.0735 which was retested on Wednesday, but strong barrier, shaped in daily Kijun-sen line, kept gains limited for now. Consolidation phase remained above broken 1.0700 barrier, reinforced by 20SMA at 1.0689 that keep in play fresh bullish momentum, gained on Tuesday's rally, for fresh attempts higher.

Slightly stronger dollar kept the Euro's near-term action at the back foot, however, dollar's gains were limited due to persisting geopolitical tensions and June rate expectations edging lower on weaker than expected US economic data and softer US economic growth expectations, as Trump administration no longer expects to complete tax reforms by August, as initially planned.

The Euro is expected to attempt above current highs and resume bull-leg from 1.0601 trough, after completing consolidation phase, which may extend below 1.0700/1.0689 support zone, but should not exceed next strong support and lower pivot at 1.0653 (daily Tenkan-sen / Fibonacci 61.8% retracement of 1.0601/1.0735 upleg).

Support: 1.0700, 1.0685, 1.0653, 1.0636

Resistance: 1.0738, 1.0777, 1.0800, 1.0826

USD/JPY

USD JPY managed to hold above two-day low at 108.32 on Wednesday, but remained under 200SMA barrier at 108.85, after repeated probes above it failed. Another close below 200SMA will maintain negative near-term tone, as overall structure remains bearish. The dollar stays under pressure on rising tensions over North Korea that triggered strong migration from riskier assets into safe haven yen.

The price is expected to stay in extended consolidation above fresh five-month low at 108.11, signalled by reversal of slow stochastic from oversold zone on daily chart. Upside was so far limited at 109.20, ahead of pivotal 109.43 barrier (Fibonacci 38.2% of 111.57/108.11 downleg) and next strong barrier at 109.84 (daily Tenkan-sen) which is expected to cap extended upticks.

Larger bear-leg from 115.50, which also marks the third wave of five-wave cycle from 118.65, is looking for eventual close below its 100% Fibonacci expansion at 108.48, for attack at immediate target at 107.86 (Fibonacci 61.8% retracement of 101.18/118.65 rally).

The wave could travel to its FE 123.6% at 106.82 on break of the latter.

Alternatively, bounce above daily Tenkan-sen barrier would sideline immediate bearish threats for stronger correction of the downleg from 111.57.

Support: 108.32, 108.11, 107.86, 107.00

Resistance: 108.94, 109.22, 109.43, 109.84

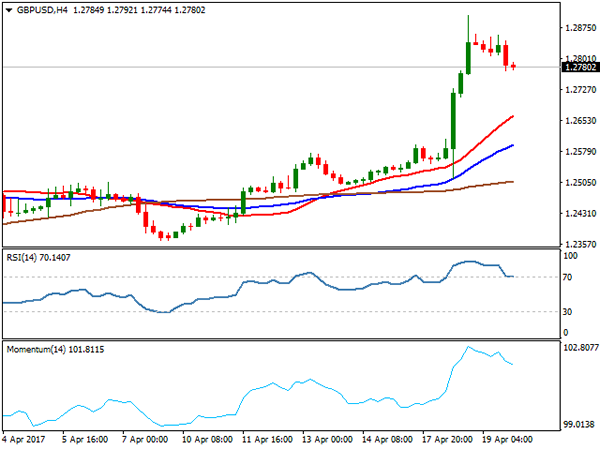

GBP/USD

British pound extended pullback from fresh high at 1.2905 (the highest since 03 Oct) posted after strong rally on Wednesday. Corrective easing was triggered by overbought studies and profit-taking Wednesday's strong rally, when the pair gained 2.2%.

However, decision for early election in the UK was welcomed by markets, as yesterday's rally of pound showed and fresh bullish sentiment has been established, keeping focus at the upside.

Fresh bulls are expected to attempt again at 1.2904 barrier, with possible extension towards psychological 1.3000 target, after markets fully digest the latest news.

Pullback's extension below 1.2800 handle faces solid support at 1.2755 (Fibonacci 38.2% of Wednesday's rally) ahead of 1.2700 and 1.2635 (daily Tenkan-sen) where extended downticks are expected to find ground.

Support: 1.2771, 1.2755, 1.2704, 1.2663

Resistance: 1.2859, 1.2905, 1.2950, 1.3000

AUDUSD

The Aussie dollar remained firmly in red on Wednesday and extended pullback from recovery high at 0.7610 (posted on Apr 17). Fresh weakness has eventually taken out strong supports at 0.7550 (200SMA) and 0.7519 (100SMA) and also broke below round-figure support at 0.7500, signalling full retracement of 0.7472/0.7610 upleg on final push towards key supports at 0.7472/60 (Apr 10/12 base / daily Ichimoku cloud base).

Daily technicals in firm bearish mode are supportive for further downside action on break below thick daily Ichimoku cloud and extension towards 0.7453 (50% retracement of 0.7158/0.7749, Jan/Mar rally.

Broken Daily Tenkan-sen and 200SMA at 0.7541/51 are expected to keep the upside protected.

Support: 0.7491, 0.7472, 0.7460, 0.7384

Resistance: 0.7519, 0.7541, 0.7551, 0.7576

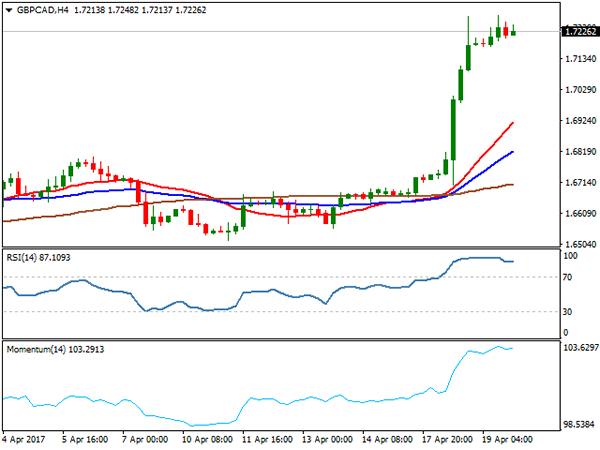

GBPCAD

The GBPCAD cross remained well supported on Wednesday and attempted higher again after narrow consolidation, posting fresh marginally higher multi-month high at 1.7280. Firm bullish sentiment is so far ignoring strongly overbought conditions of daily studies and continuing to aim higher.

Strong bullish acceleration was underpinned by double-bottom pattern formed on weekly chart at 1.5740 zone, which also marks the bottom of larger bear-trend from Jan 2016 high at 2.0918. The pair is focusing targets at 1.7524/42 (Sep 15 / Aug 03 highs) after pivots at 1.7037/1.7119 (Fibonacci 38.2% of 1.9127/1.5745 descend / Nov 11 highs) were taken out.

These levels now act as initial supports and guard significant point at 1.6988 (Fibonacci 38.2% of 1.6515/1.7280 rally), which is expected to contain deeper pullbacks.

Support: 1.7176, 1.7119, 1.7100, 1.7037

Resistance: 1.7280, 1.7454, 1.7524, 1.7542

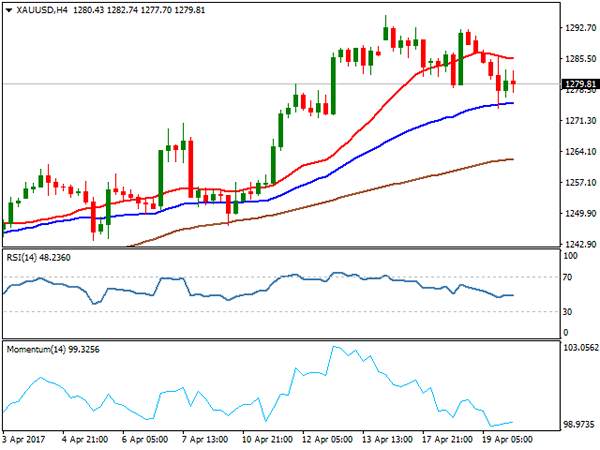

GOLD

Spot Gold ended in red on Wednesday and extended pullback from fresh high at $1295 to briefly probe below $1275 (Fibonacci 38.2% of $1243/$1295 upleg). Quick bounce above $1275 pivot signalled that downside remains limited for now, as technical correction on overbought daily studies faces strong headwinds on Gold's safe haven buying on rising tensions around Korean peninsula.

However, technical studies show more room for extension of pullback from $1295. Rising daily Tenkan-sen line (currently at $1271) acts as good support, where extended easing should be ideally contained, before bulls regain control.

Near-term focus remains at $1295/$1300 targets, with break of the latter (which is seen very likely on rising uncertainty in the markets), expected to expose next barriers at $1307/15 (Nov 2 high / Sep 1 low).

Support: 1275, 1271, 1269, 1263

Resistance: 1283, 1290, 1292, 1295

WTI CRUDE OIL

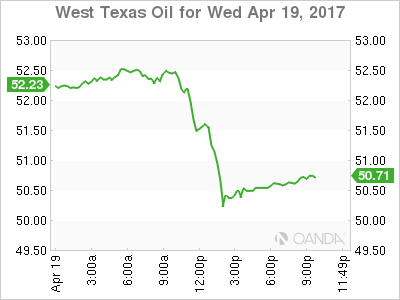

WTI oil accelerated strongly lower on Wednesday, extending pullback from $53.74 peak to hit lows ticks ahead of psychological $50.00 support. Strong bearish acceleration broke below important supports at $51.75/62 (100/55SMA's), $51.19 (Fibonacci 38.2% of $47.07/$53.74) and 20SMA at $50.73. Oil prices dropped nearly 4% on Wednesday, on the biggest one-day loss since early March, after bearish U.S. inventories data, raised concerns that the increasing levels of U.S. shale oil production could weigh on OPEC's efforts to reduce output and support oil prices.

EIA report showed that crude oil inventories fell by 1 million barrels compared to forecast for nearly 1.5 million barrels draw in the week ending Apr 12.

The report had negative impact on oil price that dropped into dangerous territory near $50.00 pivot, loss of which would drag the price down to 200SMA at $48.92.

Wednesday's long bearish candle is expected to weigh on near-term action.

Recent bearish acceleration may take a breather on oversold daily slow stochastic, however, firmer bullish signal is awaited.

Support: 50.41, 50.00, 49.62, 48.92

Resistance: 51.19, 51.58, 51.75, 52.24

DJIA

Dow Jones remained under pressure on Wednesday and extended below daily Ichimoku cloud base which offered solid support during past few sessions. Daily close below the cloud will be seen as bearish signal for extension towards next significant supports at 20266 (Fibonacci 61.8% retracement of 19713/21160 upleg) and 20197 (rising 100SMA).

Daily technicals are establishing in firm bearish mode and maintain downside pressure, as overall sentiment for stocks is negative.

Broken cloud base now acts as solid resistance, which should ideally limit the upside and guard next pivotal barrier at 0500 (falling daily Tenkan-sen line).

Support: 20310, 20266, 20197, 20054

Resistance: 20385, 20437, 20500, 20580

FTSE100

FTSE index stayed under pressure and extended losses on Wednesday, to hit new low at 7032, on the way towards target at 7024 (Feb 2 low). Full retracement of 7024/7444 rally will be seen as strong bearish signal for extension of larger bear-phase from fresh all-time high at 7444 (posted on Mar16) towards psychological 7000 support and 6969 (Fibonacci 61.8% retracement of larger 6675/7444 rally.

Broken daily Ichimoku cloud which will start turning lower next week, now marks strong barrier. Cloud base at 7192, reinforced by falling daily Tenkan-sen line is expected to cap stronger upside attempts.

Support: 7032, 7024, 7000, 6969

Resistance: 7091, 7144, 7192, 7235

DAX

DAX remained in red on Wednesday, as price action entered consolidation phase above Tuesday's fresh low at 11979, after bears cracked psychological 12000 support. Larger bear-phase off 12410 (Apr 03 peak) which currently rides on the third wave is signalling extension towards key support at 11878 (Mar 22 trough / top of rising daily Ichimoku cloud), for full retracement of 11878/12410 rally.

Strong bearish sentiment that dominates in the stock markets and bearish momentum building on daily studies are supportive for final attack at 11878 target.

Broken 20SMA at 12158 marks strong resistance which is expected to limit extended corrective upticks.

Support: 11979, 11943, 11878, 11718

Resistance: 12062, 12144, 12158, 1245

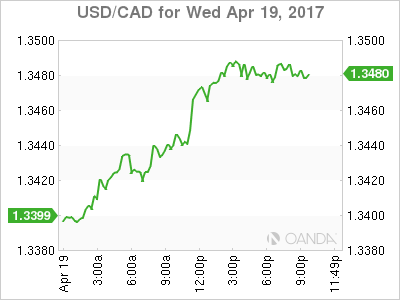

CAD in the Crosshairs

A drop in oil prices and reports that Canadian officials will try to tame the housing market sent USD/CAD close to 1.35 on Wednesday. The US dollar was the top performer while the Australian dollar lagged. New Zealand CPI and Japanese trade balance are up next. The Premium short in the DOW30 was closed for 205-pt gain, leaving another index trade open. There are 2 CAD trades in progress.

The Canadian dollar has been a challenge for traders this year. A series of headfakes, central bank mixed signals and false breakouts have kept the pair confined in a rough 1.30 to 1.35 range. Economic data has been extremely strong lately but the BOC has warned it's a mirage.

Meanwhile, two other factors threaten to break the range: Oil and housing.

Crude fell nearly $2 on Wednesday after the US reported an unexpected build in gasoline supplies, low demand and another rise in production. That final factor will irk OPEC and could scuttle a quota extension at the May 25 meeting.

If that's the case, crude and the Canadian dollar would swan dive in synch. The assumption is that Saudis will suck it up until after the Aramco IPO but that's a dangerous bet.

For the loonie, the wild card is housing. Tomorrow Ontario provincial government - where Toronto is located - will reportedly unveil 10 measures aimed at cooling the housing market. Leaks sound like they could be drastic as they include rent controls, taxes on foreign buyers, levies on speculators and more. Prices around Toronto have risen more than 30% in the past year and have tripled since 2000 so a correction is long overdue but heavy-handed government intervention could turn it into a rout.

The consumer has long been a major driver of Canadian economic strength but if housing wealth evaporates, so will spending (and CAD).

Technically, 1.3500 offered some tough resistance Wednesday even as oil prices were plunging. Beyond that, the March high of 1.3536 and the late-December, no liquidity high of 1.3599 are resistance. Also note that CAD/JPY is at the lowest since November and GBP/CAD is at the highest since September.

The loonie isn't the only commodity currency that's wilting; AUD and NZD are also nearing the lows of the year. A big factor in whether the kiwi gets there will be the Q1 CPI report due at 2245 GMT. The consensus is for a 0.8% q/q rise. That would be a healthy inflation boost and get prices up to 2.0% y/y.

At 2350 GMT, we'll be watching Japanese trade balance. The consensus is for a 608B yen surplus but more important will be trade growth. Exports are forecast to rise 6.2% and imports up 10.0%.

Fed Beige Book: Economic Activity Progressed at a Decent Clip to Cap off the First-Quarter

The most recent Beige Book notes that economic activity continued to expand at a modest-to-moderate pace throughout the country during the period of mid-February to the end of March, with half of the districts reporting moderate gains. The notion that weather effects may have contributed to a slowdown in economic activity during the first-quarter were not emphasized in the report.

Labor markets tightened further, with some contacts noting the potential for labor shortages. High-skilled IT workers, which were already reported to be in short supply in past rounds, are becoming more scarce with some employers noting worries around visa issuance regulations. Moreover, employers noted rising difficulty filling low-skilled positions.

Wages increased modestly, but have been blamed for restraining growth in some sectors, including manufacturing, transportation, and construction. Employers increasingly quoted rising turnover rates and indicated that they would raise wages moderately the coming months.

Low inventory levels have constrained sales activity despite strong demand for housing. This resulted in upward pressure on home prices across the country, a trend likely to be most detrimental to first-time homebuyers. Overall, in spite of higher mortgage rates demand for housing is strengthening as a consequence of income gains and an improving labor market.

Price increases were seen as only modest by businesses and were broadly little changed from the previous report. Small increases in selling prices were noted by manufacturers while restauranteurs only raised menu prices slightly as declines in grocery store prices only partly offset labor cost increases at restaurants.

The manufacturing sector continued to exhibit strength despite a slowdown in the pace of freight shipment growth. Lingering policy uncertainty around trade deals is likely still causing delays in investment, with most capital outlies related to maintaining existing equipment and less so for adding capacity.

Key Implications

Despite economic data pointing to a slowdown in economic activity through the end of March, businesses remained largely optimistic through the end of March supported by solid demand in several segments including manufacturing, IT, and restaurants.

Although business contacts across several industries cited policy uncertainty as worrisome, this Beige Book corroborates the sanguine attitude reported by other business sentiment readings March, such as the NFIB and ISM manufacturing indices.

All told, this Beige Book provides further confirmation that the economy is continuing to expand at a decent clip and suggests continued, albeit moderate, economic improvement - something that's likely enough to motivate the Fed to pursue its gradual rate-raising path.

Latest Beige Book Reinforces Gradual Tightening Despite Slower Q1 Growth

Highlights:

- Economic activity once again increased in all twelve districts over the reporting period (mid-February to end of March) with half reporting "modest" growth while the other half saw "moderate" gains.

- A pickup in activity was evident across all sectors, though to varying degrees.

- Reports on consumer spending varied with strong auto sales but somewhat softer growth in other areas of retail spending. Services industries generally saw steady expansion and manufacturing recorded modest to moderate gains.

- Employment expanded across districts and labour markets "remained tight"; wage growth (though modest) broadened while turnover and labour shortages increased. Moderate employment growth and modest wage growth are expected to continue.

- Prices rose modestly with stronger increases in input than output prices (although retail prices generally rose moderately).

Our Take:

Today's Beige Book report can be added to the list of surveys and other 'soft' indicators that point to an improving economic backdrop in the first quarter even as 'hard' data have been less impressive. This reinforces our view that an expected moderation in Q1 GDP growth (to 1.5%, largely reflecting softer consumer spending) will prove temporary. The FOMC expressed a similar sentiment in March with minutes from their policy meeting largely attributing slower Q1 activity to temporary factors. And while growth has faltered, labour market conditions clearly continued to tighten early this year, supporting some Committee members' views that their maximum employment objective has more or less been met. The Fed is not expected to alter monetary policy following their upcoming meetings on May 2-3, but we expect the statement to reiterate that a gradual withdrawal of accommodation remains appropriate, notwithstanding softer Q1 growth. A less-than-dovish policy statement might provide some pushback against recent paring of market expectations for tightening this year. Current pricing implies slightly more than a single rate hike over the remainder of 2017 compared with the two further moves that we and the Fed see as more likely.

EUR/GBP Support. Here We Go Again!

Here we go again!

If you're a regular reader of the blog, you know we've been trading the same EUR/GBP support level for what seems like forever now.

After breaking out of resistance back in June on the back of Brexit, price has continued to use that breakout level, this time as support, as it ranges sideways. Yes, exactly the same as the GBP/USD range that we talked about yesterday.

Now onto the charts:

EUR/GBP Daily:

The daily shows the higher time frame support level that the entire trade idea is based around. So long as the higher time frame support level holds, then we will always be looking for long entries.

EUR/GBP Hourly:

Now zooming into the hourly chart, you get a better feel for price action. In this case, you can see that price has bounced up off the level and come back to retest the short term resistance as support. Textbook technical behaviour for a bullish trending market where price steps up between support/resistance levels.

So now you have both a higher time frame support level as well as a short term bullish trend looking to establish itself. Confirmation!

Where you place your stop from here is up to you and your tolerance for risk. The obvious place is below the higher time frame support level but in putting it all the way down there, you are sacrificing some risk:reward units if the short term level holds and price immediately goes your way.

Unwind Of The Unwind Continues

Unwind of the Unwind Continues

Not unexpectedly, price action is suggesting that both the G10 and EM FX complex are paring back bets heading into the weekend. While a pre-weekend position cull has been in vogue for weeks, we’re seeing a greater propensity for position unwind this week due to the high level of investor anxiety over the French election narrative. Also, geopolitical angst, a faltering US economy and the UK snap election are consuming investors mindsets. With so many uncertainties offering few incentives for investors to re-engage risk exposure, clearly there is little market bravado as dealers appear to be disposed to participate after the fact, rather than play the post-election knee-jerk.

In the markets, a cutting move lower in crude was the primary catalyst for price action overnight, weighing on US equity markets after the Dow and S&P initially rallied on some positive earnings results. WTI prices fell after an unanticipated jump in US gasoline inventories and smaller than expected purge in US Oil stocks.

Fed Front

The Fed’s Beige Book reported the common middling expansionary theme, which had little impact on the dollar, but indicates that the Feds are remaining guardedly optimistic. However, with deepening concerns about the state of the US economy and risks that the Trump Administration policies could underwhelm, notwithstanding the absence of fiscal commitments, we could be in for further USD misfortunes in the near term. Dogged concerns on the Korean peninsula and French election this weekend will be the name of the game as we close the week out.

Euro

The French election is the dominant narrative for the euro. Despite the recent move above 1.0700, which was primarily driven by position overhang, a further extension of the current euro rally will need to include centrist Emmanuel Macron in round two run off, as his margin of victory going head to head against the other candidates looks decisive. But the closeness of the polling numbers for all four candidates entering round one increases the likelihood for a surprise, as it would take little in the way of undecided swing vote to turn the tables for any one candidate. Given the unquantifiable risks entering the weekend, markets have become lukewarm in the EURUSD trade, which has barely broken a sweat overnight, with volumes running well below average.

Australian Dollar

The least surprising trade overnight was the Aussie dollar which has continued to trade poorly over the past 24 hours. The AUD feels the headwinds of geopolitical risk, lower commodity prices and a more dovish tilt from this week’s RBA minutes, as the Central Bank is emphatically not in any rush to change their neutral policy stance.

The overnight drop in Crude prices weighed on the commodity bloc of currencies, but the AUD is the Bloc’s near term whipping boy, coming in as G10’s worst performer overnight.

However , as with most of the G-10 currencies , I would expect some paring back of positions overhang entering the weekend and the AUD could find some decent support ahead of the critical .7475 level

Japanese Yen

USDJPY has established a short-term base around 108.25 as UST’s come of their low yields and as geopolitical concerns calm. I view positioning as light overall but with an overhang of freshly minted dollar shorts on geopolitical risk and weaker US economic narrative. We could see the market cut shorts ahead of the weekend, along with a USDJPY squeeze higher, which is not out of the question and even more so as liquidity peels back.

USDASIA

The local markets are muted as this pre-French election position squaring event unfolds. Most of the local currency positions were tapered when the Korean Peninsula risk came to the fore so not expecting much movement heading into the weekend provided the geopolitical ticker tape remains dormant.

USD/CAD Loonie Lower After Gasoline Stocks Cause Oil Price Drop

The Canadian dollar is weaker against major currencies after a lower drawdown than expected in weekly crude inventories and a higher buildup of gasoline stock pushed down oil prices. American energy production is ramping up and will further pressure crude prices even as the Organization of the Petroleum Exporting Countries (OPEC) is due to meet this weekend with an extension of the production cut deal sure to be in the agenda.

The OPEC has complied with the agreed cuts, and other non-OPEC nations that joined deal have also done their part. Russia has been the outlier yet to hit the expected goals, but Saudi Arabia has cut more than their share to keep the supply levels low. The OPEC cuts and other disruptions to supplies due to geopolitical or weather related issues have kept the price of energy stable, but as more of the non-OPEC producers start ramping up production there could be another free fall of crude prices. The upcoming meeting in Vienna for the Group will no doubt focus on what they plans are going forward after the original six month timeline for the production deal ends in June.

The surprise announcement in the UK to call for a snap election has added another election process to an already crowded European calendar. This weekend French citizens will head to the polls for the first round of the presidential elections. The polls are showing a race that is too close to call and four candidates are splitting the vote with only two qualifying for a second round. Scandals and independent candidates have added uncertainty to a decisive leadership change in France.

Risk aversion has not favoured the CAD and with oil facing challenges from rising US production the loonie is not on sure footing despite a strong economic performance in the first quarter of the year.

The USD/CAD rose 0.583 percent in the last 24 hours. The pair is trading at 1.3475 as the USD is recovering from a downtrend in previous sessions. The greenback has been hit by comments from President Donald Trump about it being too strong. Treasury Secretary Steve Mnuchin has walked back some of those comments adding that Trump is not talking down the dollar. Goldman Sachs is advising clients to rethink their earlier comments on a strong dollar reaching parity with the euro.

The price of energy fell 2.28 percent on the Wednesday trading session. The price of West Texas is trading near lows of $51.18 as despite the efforts of the OPEC supplies in North America are higher as production ramps up in particular from shale producers. The biggest factor in the drop in oil prices was the gasoline stocks buildup of 1.5 million barrels ahead of the driving season.

US data will be front and center on Thursday as the Philly Fed Manufacturing Index and weekly unemployment claims are released at 8:30 am EDT. Treasury Secretary Steve Mnuchin will speak at the Institute of International Finance Policy Summit, in Washington DC. Mnuchin is hitting his stride as his profile becomes more established and is the biggest advocate of the tax reform package that had the reflation trade going earlier in the year.

Market events to watch this week:

Thursday, April 20

8:30am USD Philly Fed Manufacturing Index

8:30am USD Unemployment Claims

11:30am GBP BOE Gov Carney Speaks

12:30pm GBP BOE Gov Carney Speaks

1:15pm USD Treasury Sec Mnuchin Speaks

Friday, April 21

4:30am GBP Retail Sales m/m

8:30am CAD CPI m/m

Saturday, April 22

All Day OPEC Meeting

Sunday, April 23

All Day French Elections

Possible Scenarios for French Presidential Election

This Sunday's French Presidential race is a massive event for the EUR, and the significance has not been lost on capital markets with German Bund yields' trading atop of this year lows.

This latest Ifop poll puts Macron and Le Pen each on +23%, just +3% ahead of Fillon and the far-left Melenchon.

The spread between French and German 10-year bond yields - another indicator of market worries - is +0.72 bps. In November, the spread was as little as +0.22 bps.

This tight four horse race has thrown various scenarios into play:

Le Pen vs. Macron

This is the baseline scenario that has been dominant for many weeks since Fillon got into trouble. Polls show that these very different candidates are neck and neck.

In the second round on May 7, Le Pen is unlikely to significantly increase her support beyond her base, and voters of the moderate left and right are expected to merge around Macron.

Current polls show him winning by margins of around +25%.

This is probably the markets preferred outcome, which should be a plus for the EUR (€1.1000'ish) and have Bund yields unwinding the past months risk premium rather quickly.

Le Pen vs. Fillon

This two horse race was probably the punters ideal scenario at the beginning of February.

Until Fillon got into trouble, he was expected to beat Le Pen in round two by a good margin. He would still be expected to win, but by a much slimmer majority of around +13-15%.

If voters do happen to stay away in protest of Fillon's previous antics it will make for an interesting time for Euro capital markets. The extreme-left will still prefer Le Pen, similar to events in the U.K and the U.S.

Expect markets to be very much on edge for this outcome. The EUR will take a hit, as it's not a foregone conclusion that a "market-friendly" candidate will indeed win.

The EUR will be expected to gravitate towards its 15-year low rather quickly (€1.0340'ish).

Le Pen vs. Melenchon

Quelle surprise and a potential disaster for the Eurozone - if you thought Brexit was a massive issue, this will be a European nightmare scenario.

To many, both are deemed destructive - Le Pen to the E.U and integration, and Melenchon to opening the "unyielding" French economy.

There is no form on this two horse race, and few opinion polls are putting these extreme candidates against each other.

Never forget, the impossible can become a reality - President Trump in the U.S and U.K's Brexit.

This outcome would be extremely negative for the EUR. The possibility of penetrating parity with some zeal is a reality.

Le Pen falling at the first hurdle

That would be a massive shock. It has always been touted as a race in which she makes it to the finish line on May 7, but loses.

Handicappers believe that a Macron vs. Fillon would be the most market-friendly sub-scenario.

In second place, capital markets would tolerate Melenchon against one of the centrists. However, either Macron or Fillon are expected to easily beat Melenchon.

Eliminating the most contentious candidate in round one would be a massive win for the EUR. Those 'single' unit bears will have no cover to hide - EUR to €1.1200+