Sample Category Title

Market Update – Asian Session: Treasury Prices Dropped Along With Gold, And The USD/JPY has rebounded

US Session Highlights

(US) DOE CRUDE: -1.0M V -1ME; GASOLINE: +1.5M V -2ME; DISTILLATE: -2.0M V -1ME

(BR) Brazil Apr IGP-M Inflation (2nd Preview): -1.0% v -0.7%e

(US) MBA MORTGAGE APPLICATIONS W/E APR 14TH: -1.8% V 1.5% PRIOR

US equities opened the morning higher, though trading remained somewhat muted ahead of the weekend French election and a continued dearth of news out of DC. Risk-on flows largely returned to global markets, as Treasury prices dropped along with gold, and the USD/JPY has rebounded. As the session wore on, stocks weakened modestly and crude sold off after a smaller-than-expected inventory draw, but healthcare and industrials held onto tepid gains, while energy, consumer staples, and utilities declined.

US markets on close: Dow -0.6%, S&P500 -0.2%, Nasdaq +0.2%

Best Sector in S&P500: Healthcare

Worst Sector in S&P500: Energy

Biggest gainers: LRCX +6.9%; ISRG +6.4%; WRK +4.5%

Biggest losers: IBM -4.9%; MRO -4.3%; NFX -3.5%

At the close: VIX 14.9 (+0.5pts); Treasuries: 2-yr 1.18% (+1bps), 10-yr 2.22% (flat), 30-yr 2.87% (+3bps)

US movers afterhours

SCSS Reports Q1 $0.56 v $0.46e, R$393.3M v $370Me; Raises FY17 Rev $1.25-1.50 v $1.31e; +13.2% afterhours

QCOM Reports Q2 $1.34 v $1.20e, R$6.0B v $5.88Be; Guides Q3 $0.90-1.15 v $1.09e; +2.4% afterhours

CSX Reports Q1 $0.51 v $0.43e, R$2.87B v $2.73Be; +2.7% afterhours

EBAY Reports Q1 $0.49 v $0.48e, R$2.22B v $2.21Be; Guides Q2 $0.43-0.45 v $0.48e; R$2.28-2.32B v $2.32Be; Non-GAAP op margin 30.0% v 33.4% y/y; -1.9% afterhours

URI Reports Q1 $1.63 v $1.57e, R$1.36B v $1.34Be; Adj EBITDA margin 43.6% v 44.6% y/y; -6.3% afterhours

Key economic data

(NZ) NEW ZEALAND Q1 CPI Q/Q: 1.0% (1-year high) V 0.8%E; Y/Y: 2.2% (highest since Q3 of 2011) V 2.0%E

(AU) AUSTRALIA Q1 NAB BUSINESS CONFIDENCE: 6 V 5 PRIOR

(JP) JAPAN MAR TRADE BALANCE: ¥614.7B V ¥608BE; ADJ TRADE BALANCE: ¥172.2B V ¥172BE

(CN) China Mar FX Net Client Settlements (CNY): -48.3B v -69.2B prior

Asia Session Notable Observations, Speakers and Press

Asia indices trading mixed tracking heavy tone on Wall St, where slumping oil prices weighed on the Energy sector while low-beta Utilities/Staples also stumbled. Traders are starting to square positions going into the French elections this weekend, though there is little evidence of continued momentum behind the wild-card Melenchon in the first round after a recent surge. New Zealand Q1 CPI was the most notable datapoint of the session, rising to 5-year high annualized where Tradable prices increased 1.6%, while prices for non-tradables increased 2.5%, prompting some analysts to adjust their RBNZ tightening outlook forward. NZD/USD spiked some 40pips on the result and held its gains. Japan Trade numbers were also notable but less market moving, with surplus just above consensus, imports growth at a 3-year high, and exports at a 2-year high.

China

(CN) China State Administration of Foreign Exchange (SAFE) spokesperson: Pressure on capital outflows eased significantly in Q1 - press

(CN) China state planner NDRC said to release a 2nd batch of public-private projects - Chinese press

(CN) Former China State Administration of Foreign Exchange (SAFE) Official Guan Tao: Non-financial institutions and other participants should be allowed into the bank-dominated onshore yuan market to boost liquidity and price discovery

Australia

(AU) According to the latest property industry survey by ANZ and the Property Council of Australia, property firms and investors are most optimistic about outlook for property prices since 2014 - AFR

(AU) CBA: Australia inflation is skewed much lower because land prices are not included in the CPI basket - AFR

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.2%, Hang Seng +0.4%, Shanghai Composite -0.1%, ASX200 +0.2%, Kospi +0.4%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.2%, FTSE100 +0.2%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0707-1.0721; JPY 108.80-109.10; AUD 0.7490-0.7510; NZD 0.7000-0.7045

June Gold -0.2% at 1,281/oz; June Crude Oil +0.6% at $51.14/brl; May Copper -0.6% at $2.51/lb

SPDR Gold Trust ETF daily holdings rise 11.8 tonnes to 860.8 tonnes; 4th straight increase; highest since Dec 7th

iShares Silver Trust ETF daily holdings fall to 10,149 tonnes from 10,178 tonnes prior

(JP) Japan's MoF sells ¥0.9T in 0.7% (0.7% prior) 20-year JGBs; Avg yield: 0.562% v 0.673% prior; bid-to-cover: 4.06x (highest since 2014) v 3.78x prior

(CN) PBOC to inject combined CNY100B v CNY80B prior in 7-day, 14-day and 28-day reverse repos

(CN) PBOC SETS YUAN MID POINT AT 6.8792 V 6.8664 PRIOR; biggest margin of weakness in 3 weeks

(NZ) New Zealand sells NZ$150M in 2.75% 2025 bonds; avg yield 2.889%

Asia equities/Notables /movers by sector

Australia:

Rio Tinto (RIO) +0.3%; Q1 production

Iluka (ILU) +11.0%; Q1 results

Santos (STO) -2.9%: Q1 results

Woodside Petroleum (WPL) -1.5%; Q1 results

Hong Kong:

Ajisen (538) +0.3%; Q1 SSS

Qingdao Port International (6198) +0.7%; FY16 results

Yanzhou Coal Mining -0.2%; Guides Q1

CNOOC and PetroChina -1.0% on lower oil prices

Japan:

Toshiba (6502) +4.7%; Hon Hai/Amazon or Dell joint bid for chip unit speculation

Canon (7751) +3.1%; Q1 results speculation

Sumitomo Heavy (6302) +1.0%; FY17 results speculation

AUDJPY Demonstrating Significant Confluence

Key Points:

- AUDJPY demonstrating confluence.

- RSI Oscillator within oversold territory.

- Watch for a move higher to complete the D leg around the 84.83 mark.

The AUDJPY currency pair has convincingly trended lower over the past few months as the air has steadily leaked from the balloon that is the Australian economy. Subsequently, the market has seen price action falling from its high above the 87.00 handle, to the present close at 81.79. This is a significant depreciation but there are some signs that the pair might finally have hit rock bottom.

In particular, there is plenty of confluence being exhibited around the 81.50 mark which suggests that we are nearing a relatively big move. At this level, price action is likely to form a bullish crab pattern, as well as the C point of two bearish 5-0 patterns. In addition, the RSI Oscillator is starting to rise out of oversold levels in another indication that a turnaround is on the cards.

Further adding to the bullish contention is the appearance of ABCD pattern on the 4-hour timeframe that is now nearing completion. In fact, the C leg should complete right around the key 81.50 level which would suggest that the full pattern completion would finish at 84.83. Subsequently, there is plenty of scope for a retracement sharply higher.

Fundamentally, the Australian economy has suffered a fairly protracted decline which largely mirrors the fall in world commodity prices and the end of the super cycle. In fact, just this past month has seen the price of iron ore slump by around 30% as China pulls back their future steel purchases. However, the Aussie Dollar has largely rejected the negative pressures due to the already steep decline. Subsequently from a mean reversion point of view, the pair might have already plumbed its current depths.

Ultimately, the AUDJPY is likely to find plenty of support at its present level around the 81.50 mark given that both the ADX and RSI Oscillators are signalling oversold levels. In addition, strong confluence and the completion of a C leg hints at the validity of the bullish contention. Subsequently, the most likely scenario is one where price action consolidates around the 81.50-70 mark before commencing a relatively strong rally back towards 84.83 thereby completing the ABCD pattern.

Long-Term Australia Dollar Forecast Remains Intact Despite Recent Bullishness

Key Points:

- The double top remains intact despite the recent hiccup.

- Neckline is currently being challenged.

- Fundamental and technical biases are in agreement.

The Aussie Dollar's long-term technical forecast was in danger of being upset last week but the pair's recent tumble back to support has revived the bear's hopes for a major downtrend taking hold. What's more, the broader argument for ongoing losses is looking stronger than ever which could see the neckline of the overarching chart pattern broken over the coming days, even in the absence of a major fundamental shift in sentiment.

First and foremost, let's identify exactly what the above mentioned overarching structure is and what it could mean moving forward. As illustrated below, the pattern we have been tracking recently is a fairly well defined double top with peaks around the 0.7735 level and a neckline evident around the 0.7490 handle. This neckline has come into focus over the past 24 hours given that it is once again being challenged and looking just about ready to yield to selling pressure.

As for what this means in the medium to long-term, a breakout now could bring us into a period of fairly sizable losses. Indeed, if the retracements of the double top are any guide, the AUDUSD could plunge back to even the 0.7150 mark by June. However, we have had a similar bias only recently so it may warrant taking a closer look at some of the other technical indicators to gauge whether we are truly going to see a breakout and subsequent decline for the pair.

Firstly, as was the case previously, the EMA configuration is highly bearish and the two shorter period averages are on the cusp of completing a crossover with the 100 day EMA. However, unlike last time, the MACD has just returned to bearish and the stochastics are much less oversold which will see downside risk increase substantially. In fact, one of the only impediments to a breakout comes from the Parabolic SAR which is currently bullish. Regardless, this shouldn't present much of a real impasse given that it is also on the verge of inverting back to bearish if we have even a modest sell-off moving forward.

Ultimately, despite some recent doubt being cast on the long-term forecast, there is still a fairly strong argument for the decline suggested above. Moreover, this technical bias fits rather well with the broader fundamental case for continued losses as a result of crumbling demand for Australian iron ore. Due to this, it's worth monitoring that neckline closely as, once it breaks, the bears are likely to swiftly seize control of the pair.

Australia’s NAB Business Confidence Remained Steady In The First Quarter Of 2017

For the 24 hours to 23:00 GMT, the AUD declined 0.71% against the USD and closed at 0.7499.

LME Copper prices declined 0.4% or $20.0/MT to $5600.5/MT. Aluminium prices declined 1.0% or $20.0/MT to $1895.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7509, with the AUD trading 0.13% higher against the USD from yesterday's close.

Early morning data indicated that Australia's NAB business confidence index remained unchanged at 6.0 in 1Q 2017.

The pair is expected to find support at 0.7486, and a fall through could take it to the next support level of 0.7463. The pair is expected to find its first resistance at 0.7534, and a rise through could take it to the next resistance level of 0.7559.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro-Zone’s Annual Consumer Price Inflation Advanced 1.5% In March

For the 24 hours to 23:00 GMT, the EUR declined 0.13% against the USD and closed at 1.0715.

On the economic front, the Euro-zone's final consumer price index (CPI) climbed 1.5% on an annual basis in March, in line with market expectations and confirming the preliminary print. In the previous month, the CPI had recorded a rise of 2.0%. Moreover, the region's seasonally adjusted trade surplus widened more-than-anticipated to a level of €19.2 billion in February, from a trade surplus of €15.7 billion in the previous month, while markets expected the region to post a trade surplus of €18.0 billion.

In the US, the Federal Reserve (Fed) Beige Book revealed that the US economy expanded at a modest-to-moderate pace during mid-February to the end of March as a tighter labour market helped broaden wage gains, but inflation pressures remained modest. Moreover, a large number of firms reported high turnover rates and challenges in retaining staff.

On the data front, the US MBA mortgage applications dropped 1.8% in the week ended 14 April 2017, following a rise of 1.5% in the prior week.

In the Asian session, at GMT0300, the pair is trading at 1.0714, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.0696, and a fall through could take it to the next support level of 1.0678. The pair is expected to find its first resistance at 1.0734, and a rise through could take it to the next resistance level of 1.0754.

Moving ahead, market participants await the release of the flash consumer confidence index for April and construction output data for February from the Euro-zone, both slated to release in a few hours. Moreover, the US leading indicators for March, Philadelphia Fed business outlook index for April and weekly jobless claims data, all slated to release later in the day, would keep investors on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

GBP/USD: Pound Trading A Tad Higher, Ahead Of The BoE Governor’s Speech

For the 24 hours to 23:00 GMT, the GBP declined 0.48% against the USD and closed at 1.2781.

Meanwhile, UK's lawmakers assented to Prime Minister, Theresa May's plan to hold an early general election on 8th June.

In the Asian session, at GMT0300, the pair is trading at 1.2783, with the GBP trading marginally higher from yesterday's close.

The pair is expected to find support at 1.2747, and a fall through could take it to the next support level of 1.2710. The pair is expected to find its first resistance at 1.2839, and a rise through could take it to the next resistance level of 1.2894.

Looking ahead, market participants will draw their attention to a speech by the Bank of England (BoE) Governor, Mark Carney, due later today.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Japan’s Imports Jumped To A 3-Year High Level In March, While Exports Grew The Most In 2 Years In...

For the 24 hours to 23:00 GMT, the USD rose 0.42% against the JPY and closed at 108.89.

In the Asian session, at GMT0300, the pair is trading at 108.90, with the USD trading a tad higher against the JPY from yesterday's close.

Overnight data revealed that Japan's adjusted merchandise trade surplus narrowed less-than-anticipated to a level of ¥172.2 billion in March, as growth in imports outpaced exports. The nation registered a revised surplus of ¥609.0 billion in the previous month. Additionally, the nation's exports grew at the fastest pace in more than two years, after it jumped more-than-expected by 12.0% on an annual basis in March, compared to an advance of 11.3% in the prior month. Moreover, annual imports climbed 15.8% in March, against a rise of 1.2% in the previous month.

The pair is expected to find support at 108.50, and a fall through could take it to the next support level of 108.09. The pair is expected to find its first resistance at 109.24, and a rise through could take it to the next resistance level of 109.57.

Going ahead, traders would focus on Japan's flash Nikkei manufacturing PMI for April, and tertiary industry index for February, slated to release in the early hours of tomorrow.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Marginally Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.16% against the CHF and closed at 0.9977.

In the Asian session, at GMT0300, the pair is trading at 0.9980, with the USD trading slightly higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9959, and a fall through could take it to the next support level of 0.9937. The pair is expected to find its first resistance at 0.9997, and a rise through could take it to the next resistance level of 1.0013.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Loonie Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.71% against the CAD and closed at 1.3478.

In the Asian session, at GMT0300, the pair is trading at 1.3477, with the USD trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3415, and a fall through could take it to the next support level of 1.3354. The pair is expected to find its first resistance at 1.3514, and a rise through could take it to the next resistance level of 1.3552.

Amid a lack of economic releases in Canada today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

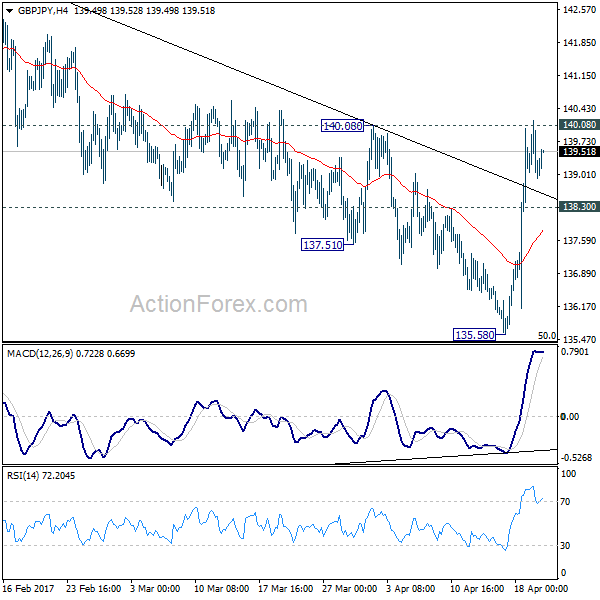

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.61; (P) 139.40; (R1) 139.88; More...

Intraday bias in GBP/JPY remains on the upside with cautiously bullish outlook. Current developments argues that consolidation pattern from 148.42 is possibly completed at 135.58, just ahead of 135.39 fibonacci level. Decisive break of 140.08 resistance will affirm this case. GBP/JPY should then target a test on 148.42 key resistance level. Meanwhile, this bullish case will be favored as long as 138.30 minor support holds, in case of retreat.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. As long as 50% retracement of 122.36 to 148.42 at 135.39 holds, another rising leg would be seen to 38.2% retracement of 195.86 to 122.36 at 150.42 and possibly above. However, firm break of 135.39 will bring retest of 122.36, with prospect of resuming the larger down trend from 195.86.