Sample Category Title

Spot Gold Skyrockets On Political Turmoil

'Recently a degree of uncertainty has found its way into previously seemingly bulletproof financial markets.' – ANZ (based on Reuters)

Pair's Outlook

The US and Russian tensions over Syria and North Korean nuclear threats are the driving force behind the surge in the value of the yellow metal. Due to the combined effect of the global political turmoil a run to safety has caused the bullion's price to jump and touch the 1,280 level on Wednesday morning, which is a two percent increase, if compared to Tuesday's opening price. It is most likely that the fundamentals will continue to dictate the fluctuations in the commodity price, as technical analysis has become impaired on the daily chart.

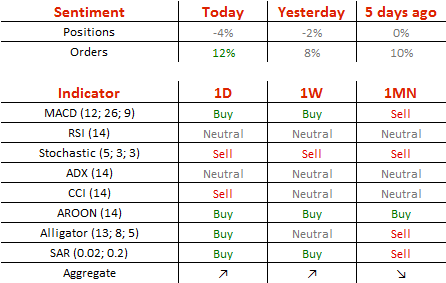

Traders' Sentiment

SWFX traders are neutral bearish, as 52% of open positions are short. However, 56% of trader set up orders are to buy the yellow metal.

(UK) British Inflation Holds Steady In March Amid Later Easter Holidays

'The recent run of escalating inflation may have paused for now, but that has more to do with the timing of Easter than any change in the strong upward pressure on prices.' - Stephen Clarke, Resolution Foundation

British inflation remained unchanged in March compared to the prior month due to this year's later Easter and a slight fall in oil prices. The Office for National Statistics reported on Tuesday consumer prices rose 2.3% on an annualised basis last month, while market analysts anticipated a 2.2% increase. The sharp fall in the value of the British Pound paired with the recent rebound in oil prices boosted inflation across Britain. Furthermore, a combination of subdued wage growth and surging inflation started putting significant pressure on households' pockets, raising concerns over growth prospects as consumer spending accounts for about 60% of the British economy. Tuesday's data also showed that food prices climbed 1.2% on an annualised basis in March, the largest gain since 2014. However, the Bank of England said at its latest monetary policy meeting that there was no rush to raise interest rates and it was prepared to tolerate inflation above the 2% target. The main driver behind March's unchanged reading was a drop in airfares, which, in turn, was triggered by the later timing of this year's Easter holidays. Analysts suggest that consumer prices will continue surging until inflation hits 3% due to the weak Sterling and higher oil prices.

German Investor Sentiment Hits Highest Since 2015 In April

'The financial market experts expect this positive development to continue.' - Achim Wambach, ZEW

The mood among German investors improved markedly in April amid strong economic growth in the Q1 and easing concerns over the US President Donald Trump's protectionist policies. The Mannheim-based ZEW Institute reported on Tuesday that its Economic Sentiment Index jumped to 19.5, the highest level since August 2015, from 12.8 points seen in March, while analysts anticipated a slight increase to 13.2. Despite Trump's latest border tax threats, the German car industry reported that it started the year with solid growth. Moreover, figures released last week showed that both German industrial production and trade surplus soared in February. The assessment of the current economic situation in Germany climbed to 80.1 points in April, compared to the previous month's 77.3, whereas markets expected a modest increase to 77.7 during the reported period. Many analysts revised up its growth projections for the German economy. Thus, the Euro zone's largest economy is set to expand 1.5% in 2017 and 1.8% in 2018. Tuesday's strong figures provided support to the current German Chancellor Angela Merkel's government ahead of the September parliamentary elections. After the release, the EUR/USD pair rose above 1.0600.

US Employers Post 5.7M Open Job Positions In February

'The fact that we've got a lot of jobs is a good thing - we wanted that. But the fact that you could create that many jobs in the context of growth that is so low points to a significant problem, and the problem is productivity growth is very low.' - Janet Yellen, Federal Reserve

US employers posted more open job positions in the second month of the year, official figures revealed on Tuesday. According to the Job Openings and Labor Turnover survey published by the Labour Department, job openings advanced 2.1% to a seasonally adjusted 5.7M during the reported period, following the preceding month's 5.6M and surpassing market analysts' expectations for a decrease to 5.59M. That marked the highest level since July 2016. February's gain boosted the jobs opening rate to 3.8% after it remained steady at 3.7% for four consecutive months. Nevertheless, hiring fell to 5.3M in February, compared to 5.4M registered in the preceding month. Therefore, the hiring rate dropped to 3.6% from 3.7% in January. Analysts stated that the US labour market is at or close to full employment, with the unemployment rate at a near 10-year low of 4.5%. Monthly job openings are closely followed by the Federal Reserve Chair Janet Yellen, as it is considered as a key barometer of economic conditions and the labour market trends. On Monday, the Fed Chair hinted at two more rate hikes this year, and some analysts suggested that the Fed might want to pull the trigger in June. After the release, the USD/JPY pair dropped to 100.58, its lowest level since November 18.

Technical Outlook: GBPUSD – Near-Term Bulls Look For Extension Above 1.2500 Pivot, UK Jobs Data Eyed

Strong two-day rally that broke above narrowing daily cloud and closed well above daily Tenkan-sen (1.2458) has shifted near-term focus higher. Tuesday's strong bullish acceleration extended briefly in early Wednesday and pressuring psychological 1.2500 barrier and 06 Apr high at 1.2504. Break here is needed to expose next target at 1.2553 (03 Apr high) and open way towards key near-term barrier at 1.2613 (27 Mar peak). Daily MA's and Tenkan-sen/Kijun-sen lines in bullish setup are supportive for further advance, as the pair is awaiting UK jobs data for firmer signals. UK jobless claims are expected to rise in March, according to forecast at -3.0K vs -11.3K in Feb, while Unemployment rate and Average Earnings are expected to stay unchanged at 4.7% and 2.2% respectively. Broken daily Tenkan-sen/20SMA offer solid support at 1.2455 zone, which is expected to hold dips and guard lower pivot at 1.2415 (100SMA).

Res: 1.2505, 1.2518, 1.2553, 1.2594

Sup: 1.2478, 1.2455, 1.2415, 1.2374

AUD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 13 Mar 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Bearish engulfing pattern

• Time of formation: 16 Feb 2017

• Trend bias: Near term down

The Australian dollar did meet renewed selling interest at 85.75 (we recommended in our previous update to sell aussie at 85.70 and a short position was entered) and has dropped in line with our bearish expectation, our short position met downside target at 83.70 with 200 points profit, as this anticipated selloff has kept the pair under pressure, bearishness remains for recent decline from 88.15 top to extend further weakness to 82.00 and possibly towards support at 81.10-15, however, near term oversold condition should limit downside and reckon 80.00 psychological support would hold from here, bring rebound later.

On the upside, whilst initial recovery to 83.00-10 cannot be ruled out, reckon the Tenkan-Sen (now at 83.83) would limit upside and bring another decline to aforesaid downside targets. Only a daily close above the Kijun-Sen (now at 84.70) would abort and suggest low is formed instead, risk a stronger rebound to 85.00-10 but said resistance at 85.75 should remain intact, bring another decline later this month.

Recommendation: Our short position entered at 85.70 met target at 83.70 with 200 points profit and would sell again at 83.65 for 81.65 with stop above 84.65.

On the weekly chart, the pair has continued heading south throughout since the beginning of last week and broke below support art 83.75, adding credence to our view that top has been formed at 88.15 and consolidation with downside bias remains for the retreat from there to extend weakness to the upper Kumo (now at 81.61), then towards support at 81.10-15, however, a weekly close below latter level is needed to retain bearishness and suggest the rise from 72.50 has ended, then further fall to 80.50 and possibly psychological support at 80.00 would follow but the lower Kumo (now at 78.65) should remain intact.

On the upside, although recovery to 83.00-10 is likely, reckon upside would be limited to 83.60-70 and bring another decline. Above 83.70 would risk a stronger rebound towards 85.05 (last week’s high and current level of the Tenkan-Sen), however, only a weekly close above resistance at 85.75 would abort and signal low is formed instead, bring further subsequent gain to 86.00 and then 86.50-60, however, price should falter below resistance at 87.50.

Market Update – Asian Session: China Inflation Still Weighed Down By Food Prices

Asia Mid-Session Market Update: China inflation still weighed down by food prices; BOJ's Kuroda steps up jawboning of exchange rate as Yen rises to fresh 2017 highs

US Session Highlights

(US) Mar NFIB Small Business Optimism: 104.7 v 104.7e

(US) FEB JOLTS JOB OPENINGS: 5.743M V 5.65ME

(US) President Trump tweets: “I explained to the President of China that a trade deal with the U.S. will be far better for them if they solve the North Korean problem! North Korea is looking for trouble. If China decides to help, that would be great. If not, we will solve the problem without them! U.S.A.”

(US) Fed's Williams (moderate, non-voter): we need to bring rates back to normal this year and next year; Reiterates there could be three or four rate hikes this year - press interview

US markets on close: Dow flat, S&P500 -0.1%, Nasdaq -0.2%

Best Sector in S&P500: Real Estate

Worst Sector in S&P500: Technology

Biggest gainers: AAL +3.8%; STX +3.1%; JWN +2.6%

Biggest losers: ADS -3.8%; SWN -3.1%; RCL -2.7%

At the close: VIX 15.1 (+1.0pts); Treasuries: 2-yr 1.24% (-2bps), 10-yr 2.30% (-6bps), 30-yr 2.93% (-6bps)

US movers afterhours

NBIX: FDA approves INGREZZA (valbenazine) capsules as the first and only approved treatment for adults with tardive dyskinesia (TD); +19.3% afterhours

DRYS: Declares dividend of $2.5 million (1% of market cap); dividend per share amount to be paid by the Company to be determined later; +6.9% afterhours

TSCO: Guides Q1 $0.45-0.46 v $0.53e, R$1.56B v $1.58Be; SSS -2.2%; -3.5% afterhours

ONVO: Announces CEO transition; -6.6% afterhours

NS: Agrees to acquire Navigator Energy Services, LLC for $1.48B; -6.8% afterhours

Politics

(US) President Trump: US sending a very powerful armada to North Korea - Fox interview

(US) House Fin Services Chairman Hensarling (R-TX): will unveil Dodd-Frank overhaul bill by the end of the month

(US) John Sullivan nominated by Pres Trump as Deputy State Secretary - press

Key economic data

(CN) CHINA MAR CPI M/M: -0.3% (2nd straight decline) v -0.2% PRIOR; Y/Y: 0.9% V 1.0%E

(CN) CHINA MAR PPI Y/Y: 7.6% V 7.5%E; 7th consecutive increase

(AU) AUSTRALIA APR WESTPAC CONSUMER CONFIDENCE INDEX: 99.0 V 99.7 PRIOR, M/M: -0.7% (first decline in 4 months) V +0.1% PRIOR

(JP) JAPAN FEB CORE MACHINE ORDERS M/M: 1.5% V +3.6%E; Y/Y: 5.6% V +2.5%E

(JP) JAPAN MAR PPI (CGPI) M/M: 0.2% V 0.3%E; Y/Y: 1.4% V 1.4%E

(KR) South Korea Mar Unemployment Rate: 3.7% v 3.8%e; 466K new jobs created, biggest gain since Dec 2015

Asia Session Notable Observations, Speakers and Press

Safehaven flows remain the prevalent theme in Asian trade as geopolitical risks related to conflicts in Syria and saber-rattling by North Korea are not abating. Ahead of his arrival in Moscow, US State Sec Tillerson is calling on Putin to denounce his support for Syria's Assad, just as Kremlin continues to hint that chemical attacks were actually done by the rebels to garner international sympathy. US President Trump has also tweeted that "North Korea is looking for trouble" and added today that US is "sending a powerful armada", while Pyongyang warned of a nuclear attack on the US at any sign of American aggression. Vix has spiked up to a 2-week high, US benchmark Treasury yield is testing a key long-term support of 2.30%, and Nikkei225 is the worst performing major index on Yen strength (both Nikkei and USD/JPY are at lowest levels since mid-Nov). Gold prices have also extended their gains on safehaven demand, while Dalian Iron Ore price decline is weighing on the high-beta Aussie Dollar currency. AUD/USD has fallen back below $0.75 near its 2 1/2 month lows going into tomorrow's critical Australia employment data.

China consumer inflation remained underwhelming in March, as m/m CPI fell for the 2nd straight month and y/y was near its 2-year lows below 1%. Food CPI component fell again by over 4%, while non-food rose slightly by 2.3% v 2.2% prior. Recall China has a formal 2017 CPI target of 3%. Conversely, rising input costs have continued to prop up wholesale inflation, with PPI up for the 7th straight month at +7.6% - close to consensus.

Ahead of tomorrow's employment data, Australia Westpac Consumer Confidence index registered its first decline in 4 months to 99.0 from 99.7 - implying contracting conditions. Westpac economist still remarked that confidence is holding up well media attention over housing affordability and growing geopolitical tensions globally.

China

(CN) China Banking Regulatory Commission (CBRC) urges banks to reduce exposure

(CN) China Insurance Regulatory Commission (CIRC) vice chairman Chen Wenhui: Insurance industry exposed to solvency, liquidity, corporate governance, and external risks - press

Japan

(JP) BOJ Gov Kuroda: BOJ easing not aimed at FX level; Further weakening in Yen would help to meet CPI target sooner

(JP) Japan Fin Min Aso: Drafting free trade rules is a key goal for US-Japan dialogue

(JP) US said to be planning to talk about trade deficit with Japan - Nikkei

Australia/New Zealand

(NZ) New Zealand's Aon Hewitt: 1-year inflation expectations unchanged at 1.7%; 4-year unchanged at 2.0%

Korea

(US) President Trump: US sending a very powerful armada to North Korea - Fox interview

(KR) South Korea presidential frontrunner Jae-In Moon: to draft extra budget immediately if getting elected

(KR) Japan Foreign Ministry issues short-term alert on South Korea travel due to North Korea nuclear tests

Asian Equity Indices/Futures (23:30ET)

Nikkei -1.2%, Hang Seng -0.1%, Shanghai Composite -0.3%, ASX200 flat, Kospi +0.1%

Equity Futures: S&P500 -0.2%; Nasdaq -0.2%, Dax -0.2%, FTSE100 -0.3%

FX ranges/Commodities/Fixed Income (23:30ET)

EUR 1.0595-1.0615; JPY 109.25-109.75; AUD 0.7485-0.7510; NZD 0.6930-0.6960

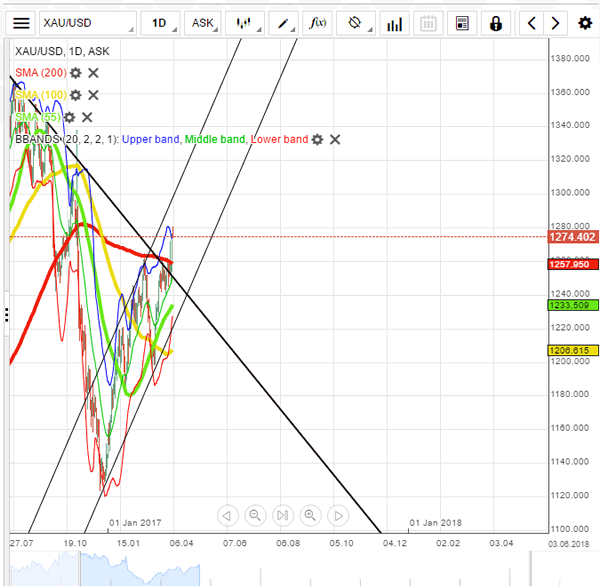

June Gold +0.2% at 1,277/oz; May Crude Oil +0.3% at $53.54/brl; May Copper -0.3% at $2.60/lb

(US) Weekly API Oil Inventories: Crude: -1.3M v -1.8M prior; second straight draw

SPDR Gold Trust ETF daily holdings rise 4.1 tonnes to 842.4 tonnes; highest since Mar 2nd

iShares Silver Trust ETF daily holdings rise to 10,208 tonnes from 9,862 tonnes prior; First rise since Mar 20th

(CN) PBOC SETS YUAN MID POINT AT 6.8940 V 6.8957 PRIOR; 2nd straight firmer fix

(CN) PBoC skips open market operations for 13th straight session; drains net CNY40B

(CN) China MoF sells 5-yr Govt bonds at 3.1264% v 3.12%e; bid-to-cover 1.62x

(AU) Australia MoF (AOFM) sells A$800M in 1.75% 2020 Bonds; avg yield: 1.8675%; bid-to-cover: 3.74x

(JP) BOJ announces amounts to buy in upcoming QE operation: cuts 3-5yr to ¥350B (prior ¥380B)

Asia equities / Notables / movers

Australia

NST.AU Northern Star +2.1%, SAR.AU Saracen +4.9%, RSG.AU Resolute Mining +1.8% (gold price gains)

SPK.NZ Spark NZ +2.6% (offer to buy TeamTalk has lapsed)

TLS.AU Telstra -6.8% (TPG plans rival Australian mobile network)

SFR.AU Sandfire Resources -2.4% (Morgans Financial downgrade)

Japan

8028.JP FamilyMart Uny -4.5% (annual result)

6502.JP Toshiba Corporation -1.5% (may need govt support, 9-month result)

7752.JP Ricoh Co +1.6% (to shrink camera business)

6796.JP Clarion Co -6.4- (annual result speculation)

6146.JP Disco Corp -3.4% (annual result speculation)

2726.JP Pal Co +5.4% (annual result)

7649.JP Sugi Holdings % (annual result)

9948.JP Arcs Co -3.7% (annual result)

2670.JP ABC-MART -5.5% (annual result)

Hong Kong

2009.HK BBMG Corp +0.2% (guidance)

6837.HK Haitong Securities -0.9% (Mar result)

6030.HK CITIC Securities -0.6% (Mar result)

1888.HK Kingboard Laminates Holdings -5.3% (shareholder placement)

China

000507.CN 600185.CN Gree Real Estate +10.0% (SMBC upgrade)

600340.CN China Fortune Land Development +2.2% (Xiongan new district)

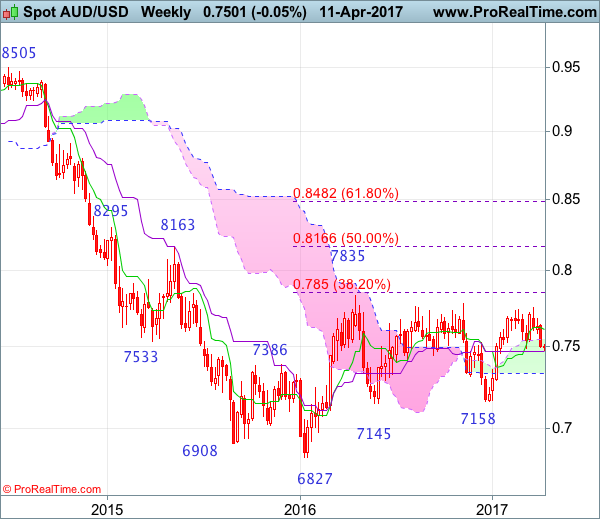

AUD/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting doji

• Time of formation: 20 Feb 2017

• Trend bias: Sideways

Daily

• Last Candlesticks pattern: Bearish engulfing pattern

• Time of formation: 21 Mar 2017

• Trend bias: Near term down

Aussie has dropped quite sharply last week and broke below indicated support at 0.7491, dampening our bullishness and suggesting top has been formed at 0.7750 last month, hence consolidation with downside bias is seen for this fall from 0.7750 to bring at least a strong retracement of the rise from 0.7158 and further decline to 0.7450-55 (50% Fibonacci retracement of 0.7158-0.7750), then towards 0.7380-85 (61.8% Fibonacci retracement), however, reckon downside would be limited to 0.7300-10 and bring rebound later.

On the upside, whilst initial recovery to 0.7540-50 cannot be ruled out, reckon the Tenkan-Sen (now at 0.7569) would limit upside and bring another decline later. Only a daily close above the Kijun-Sen (now at 0.7612) would abort and signal first leg of decline from 0.7750 has ended, bring a stronger rebound to 0,7640-50 but resistance at 0.7680 should cap upside, price should falter below 0.7700-10, bring another decline later.

Recommendation: Sell at 0.7570 for 0.7390 with stop above 0.7670.

On the weekly chart, last week’s selloff below support at 0.7491 formed a black candlestick with price closing near the week’s low, signaling top has been formed at 0.7750 and consolidation with downside bias is seen, a weekly close below the Kijun-Sen (now at 0.7468) would add credence our view that the rebound from 0.7158 has ended at 0.7750, then further choppy trading below previous resistance at 0.7778 would take place with mild downside bias for further fall towards 0.7380-85 (61.8% Fibonacci retracement of 0.7158-0.7750), however, reckon downside would be limited to 0.7290-00, bring recovery later.

On the upside, expect recovery to be limited to 0.7565-70 and the Tenkan-Sen (now at 0.7612) should hold, bring another decline later. Above last week’s high at 0.7641 would risk test of resistance at 0.7680 but only a sustained breach above this level would signal the retreat from 0.7750 has ended instead, bring another bounce towards this level. Looking ahead, only break of 0.7778 resistance would suggest a possible upside break of early established broad range, bring further rise to 2016 high at 0.7835, above there would confirm and encourage for headway to 0.7900 and later towards psychological level at 0.8000.

Technical Outlook: EURUSD – Plethora Of Strong Barriers Likely To Limit Repeated Recovery Attempts

The Euro remains at the front foot on Wednesday and probes again above daily cloud top (1.0613) for renewed attack at next significant barrier at 1.0622 (100SMA), following Wednesday's spike to 1.0628.

Strong upside rejection on Wednesday that left daily candle with long upper shadow is expected to weigh on near-term action, as daily studies remain in bearish setup.

The pair faces a cluster of barriers between 1.0613 and 1.0635 (cloud top/100SMA and daily Tenkan-sen in steep descend) which is seen as strong obstacle for the euro to extend near-term recovery leg from 1.0570 low.

Also, growing fears about the outcome of French elections keeps traders cautious and may limit recovery attempts.

Near-term action is also pressured by falling thick 4-hr Ichimoku cloud (spanned between 1.0664/1.0769), base of which should cap extended upticks.

Res: 1.0622, 1.0635, 1.0650, 1.0664

Sup: 1.0593, 1.0577, 1.0568, 1.0524

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 10612

The intraday bias is slightly positive after 1.0567 low and initial resistance lies at 1.0640. Crucial on the downside is 1.0580 support and a break through that low will challenge 1.0490 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0640 | 1.0828 | 1.0580 | 1.0490 |

| 1.0700 | 1.0904 | 1.0490 | 1.0340 |

USD/JPY

Current level - 109.52

Yesterday's break through 110.10 lows signals a completion of the prolonged consolidation pattern and the bias is bearish, for a slide towards 108.50 area. Major resistance lies at 110.10.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.50 | 113.50 | 110.10 | 110.10 |

| 112.26 | 115.65 | 110.10 | 107.80 |

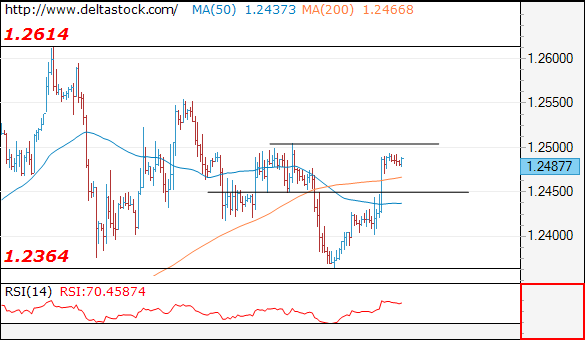

GBP/USD

Current level - 1.2487

The intraday bias is positive after the break through 1.2450, as the pair is currently testing 1.2500 resistance area. A violation of the latter will challenge 1.2500 and 1.2620.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2500 | 1.2620 | 1.2450 | 1.2230 |

| 1.2620 | 1.2705 | 1.2364 | 1.2107 |