Sample Category Title

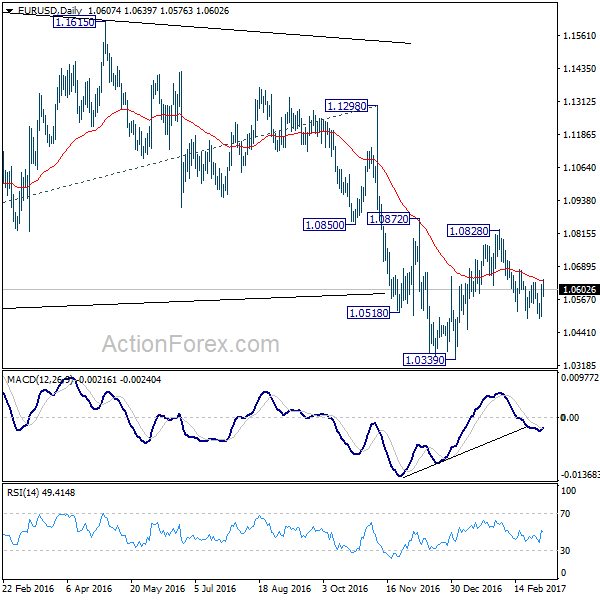

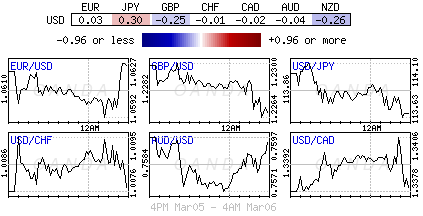

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0537; (P) 1.0580 (R1) 1.0663; More.....

EUR/USD breached 1.0630 minor resistance today but fails to sustain so far. Intraday bias remains neutral first. On the upside, firm break of 1.0630 resistance will argue that pull back from 1.0828 is completed. Also, rise from 1.0339 could possibly be resuming. In that case, intraday bias will be turned back to the upside for 1.0828 resistance and above. On the downside, below 1.0493 support will affirm the case that fall from 1.0828 is resuming the larger down trend. In that case, intraday bias will be back to the downside for resting 1.0339 low.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

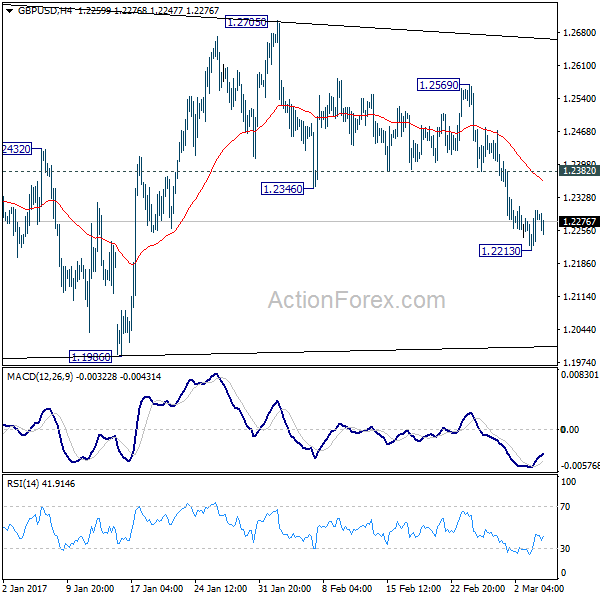

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2236; (P) 1.2268; (R1) 1.2322; More...

Intraday bias in GBP/USD remains neutral for consolidation above 1.2213 temporary low. We're still maintaining a bearish view on the pair. That is, consolidation pattern from 1.1946 should have completed with three waves to 1.2705 already. Hence, current recovery should be limited by 1.2382 support resistance and bring another decline. On the downside, break of 1.2213 will target 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view and resume the larger down trend. Nonetheless, on the upside, above 1.2382 minor resistance will delay the bearish case and turn bias back to the upside for 1.2569.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Trade Idea Update: USD/JPY – Sell at 114.35

USD/JPY - 113.82

Original strategy :

Sell at 114.35, Target: 113.35, Stop: 114.70

Position : -

Target : -

Stop : -

New strategy :

Sell at 114.35, Target: 113.35, Stop: 114.70

Position : -

Target : -

Stop : -

Although the greenback rose briefly to 114.75, the subsequent sharp retreat suggests top is possibly formed there on Friday, hence consolidation with mild downside bias is seen for retracement of last week’s rise to 111.69, hence weakness to 113.47 support is likely, below there would bring further fall to 113.20-25 (50% Fibonacci retracement of 111.69-114.75), however, downside would be limited to 113.00 and 112.84-86 (previous resistance and 61.8% Fibonacci retracement), bring rebound later.

In view of this, we are looking to sell dollar on recovery for such move as 114.40-50 should limit upside, bring another decline. Only above said resistance at 114.75 would abort and signal the rise from 111.69 has resumed and extend gain to 114.96 (previous resistance) but price should falter well below resistance at 115.38.

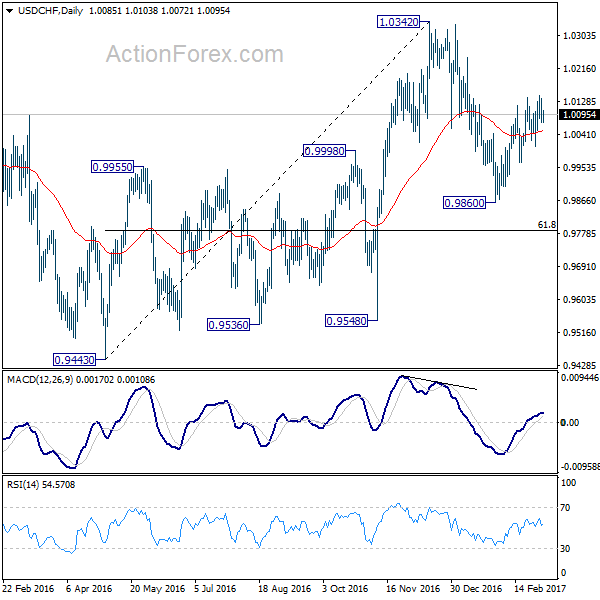

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0052; (P) 1.0094; (R1) 1.0116; More.....

USD/CHF is staying in consolidation below 1.0145 temporary top and intraday bias stays neutral first. The lost of momentum after hitting 1.0145 is dampening the bullish case a bit. But still, as 1.0008 minor support holds, further rise is mildly in favor in the pair. Above 1.0145 will target a test on 1.0342 key resistance. Based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. On the downside, break of 1.0008, however, will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

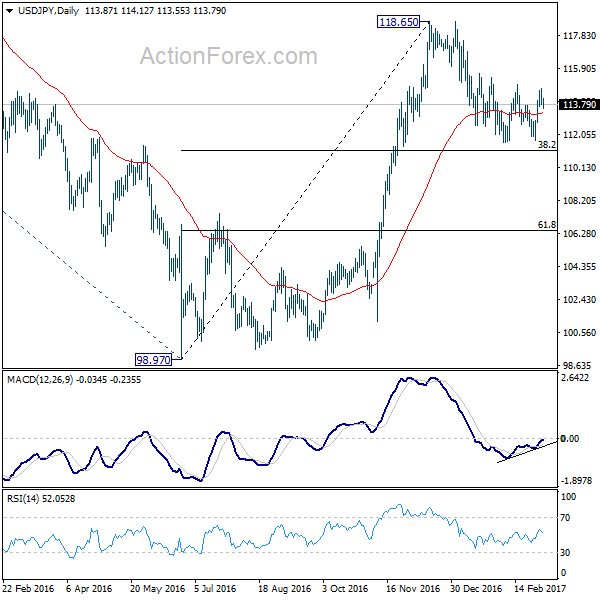

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.61; (P) 114.18; (R1) 114.56; More...

USD/JPY weakens today but loss is limited so far. It's holding above 55 hour EMA and stays well in range of 111.58/114.94. Intraday bias remains neutral first. The corrective fall from 118.65 might not be completed yet. But still, in case of another fall, we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound. On the upside, decisive break of 114.94 will indicate that it's completed with a double bottom pattern (111.58, 111.68). In such case, intraday bias will be turned to the upside for retesting 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Yen Maintain Gains, Followed by Dollar, Politics Prevail Economics for Now

The markets trade in mild risk aversion today and the sentiments sent Yen broadly higher. Meanwhile, Dollar regains some ground from Friday's profit taking pull back. The greenback stays supported by firm expectation of a March Fed hike. Nonetheless, the moves in the forex markets are relatively limited. Politics has been a stronger drive in the forex markets, as well as others since late last year. This view is shared by the BIS too as seen in it's quarterly report. For the moment, US fiscal policies, French elections, Brexit negotiations, as well as some geopolitical development like North Korea's firing of missiles will stay as important market drivers. Dollar will look into Friday's job report for sealing the case for a Fed hike.

BIS: Politics tightened its grip over financial markets

The Bank for International Settlements said in its quarterly report published today that "politics tightened its grip over financial markets in the past quarter, reasserting its supremacy over economics." The report touched on the political uncertainties in Europe with elections in France, Germany and the Netherlands. Meanwhile, it also pointed out reflation trades triggered by US president Donald Trump. Emerging markets are see as " caught between a rock and a hard place, the rock being the prospect of a tightening of U.S. monetary policy (even if gradual), an appreciating dollar and their FX currency debt, and the hard place the threat of rising protectionism."

UK treasury Hammond to deliver tax hike

In UK, Chancellor of the Exchequer Philip Hammond will deliver his first budget statement to Parliament on Wednesday. Hammond said during the weekend that UK has "got enough in the tank" so buffer the impact of Brexit. But he still emphasized the need to keep a tight rein on public finance. There are talks that Hammon would announce tax hike to counter the need to additional borrowing. Meanwhile, he talked hard regarding the negotiation with EU on Brexit terms. He vowed to "fight back" if UK and EU "don't continue to work closely together". And UK will "forge new trade deals around the world".

Eurozone Sentix investor confidence hit near 10 year high

Eurozone Sentix investor confidence rose to 20.7 in March, up from 17.4 and beat expectation of 18.5. That's also the highest level in more than 10 years, since August 2007. Sentix noted that "all the expectation components for the global economic regions rose and cast the decline of last month in a new light". And, "therefore the potential threat of a sudden halt to the economic recovery is off the table." Also, "in addition to the main regions, the positive economic momentum for emerging markets is retained." Also from Eurozone, retail PMI dropped to 49.9 in February.

EU to increase defense cooperation

European Union defense ministers are meeting in Brussels today for setting up a centralized command structure for certain military operations. That is seen by analysts as a response to doubtful commitment from US on NATO. EU foreign policy chief Federica Mogherini said the plan is a "major step forwards" that enables "more unified, more rational, more efficient approach to existing training missions." On the other hand, the exiting member UK's defense secretary Michael Fallon urged EU to "cooperate more closely with NATO, to avoid unnecessary duplication and structures and to work together on new threats."

Yen jumps as North Korea fires ballistic missiles

The Japanese Yen jumps broadly in Asian session today on risk aversion as North Korea fired four ballistic missiles into nearby waters. Some analysts pointed out that the missile tests reminded the markets of the unpredictably of Kim Jong Un leadership. Japan prime minister Shinzo Abe warned that the missile launches "clearly show that this is a new level of threat" from North Korea".

China to target 6.5% growth this year

In China, Premier Li Keqiang suggested at the National People's Congress that the government's GDP growth target for this year is "around 6.5%, or higher if possible", down from 2016's 6.5-7.0%. Inflation target stays at around 3% and a fiscal deficit at around 3% of GDP. The growth target of money supply M2 has been lowered, by -1 percentage point, to 12%. As suggested in the Work Report, the RMB exchange rate will "be further liberalized, and the currency's stable position in the global monetary system will be maintained". A number of Chinese macroeconomic data would be released including trade balance and inflation.

RBA to stand pat

Australia TD securities inflation dropped -0.3% mom in February. Australia retail sales rose 0.4% mom in January, in line with consensus. RBA will announce rate decision tomorrow and it's widely expected to stand pat.

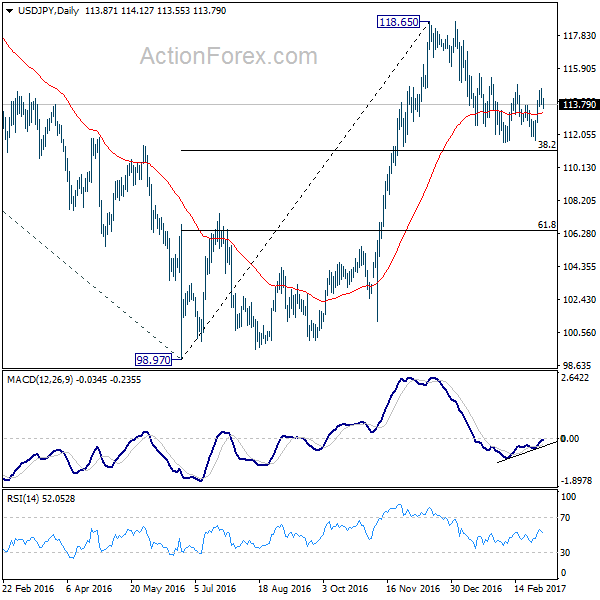

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.61; (P) 114.18; (R1) 114.56; More...

USD/JPY weakens today but loss is limited so far. It's holding above 55 hour EMA and stays well in range of 111.58/114.94. Intraday bias remains neutral first. The corrective fall from 118.65 might not be completed yet. But still, in case of another fall, we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound. On the upside, decisive break of 114.94 will indicate that it's completed with a double bottom pattern (111.58, 111.68). In such case, intraday bias will be turned to the upside for retesting 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | TD Securities Inflation M/M Feb | -0.30% | 0.60% | ||

| 0:30 | AUD | Retail Sales M/M Jan | 0.40% | 0.40% | -0.10% | |

| 9:10 | EUR | Eurozone Retail PMI Feb | 49.9 | 50.1 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Mar | 20.7 | 18.5 | 17.4 | |

| 15:00 | USD | Factory Orders Jan | 1.00% | 1.30% |

Markets Gripped by Monday Jitters

Global stocks were vulnerable to losses during early trading on Monday with investors on edge as the heightened geopolitical tensions in East Asia weighed on risk sentiment. Asian shares traded mostly mixed amid the jitters while risk aversion exposed European equities to downside shocks. With the overall trading mood subdued and market participants treading cautiously, gains on Wall Street could be limited this evening.

It should be kept in mind that the rising optimism over Trump's fiscal policies boosting US growth has attributed to the highly impressive stock market rally this quarter. A situation where the anticipated policies fall below expectations could still result in a sharp selloff across the board.

Greenback on standby

The lack of buying incentives for fresh Dollar purchases coupled with profit taking has placed the Greenback on standby during Monday's trading session. Although Janet Yellen's hawkish remarks last Friday have heightened speculations of a March rate hike, Dollar bullish investors may still be seeking further inspiration elsewhere. Much attention will be directed towards Friday's NFP which could offer some insight on how the U.S labour force has fared in the New Year. A strong NFP should cement expectations of a March rate hike with bullish investors exploiting the optimism to elevate the Dollar Index back above 102.00.

Sterling bears eye 1.2200

The growing anxiety ahead of the Article 50 invoke this month has exposed Sterling to noticeable losses during Monday's trading session. Uncertainty has made Sterling fundamentally bearish with investors likely to exploit the Brexit developments to drag the currency much lower this quarter. From a technical standpoint, the GBPUSD is tilted to the downside on the daily charts as there have been consistently lower lows and lower highs. Previous support around 1.2300 could transform into a dynamic resistance that encourages a further decline back towards 1.2200.

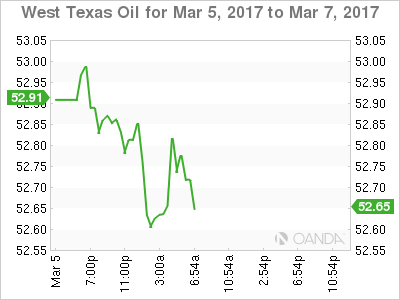

WTI Crude losing upside momentum

WTI Crude was under pressure during Monday's trading session as fears of lower growth targets in China sparked discussions of the nation cutting oil demand. The selling pressure was fuelled by the ongoing concerns over Russia's compliance with the global output cut which revived some oversupply anxieties. With U.S inventories rising incessantly and the Dollar set to strengthen from the prospects of higher US rates, oil markets could be poised to trade lower moving forward. From a technical standpoint, WTI Crude is pressured on the daily charts and a breakdown below $52.50 could encourage a further decline towards $51.50.

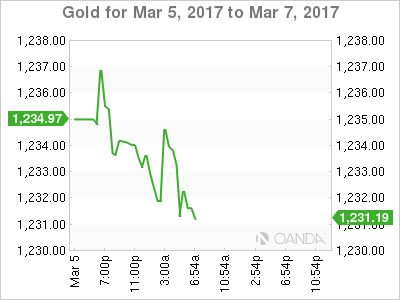

Commodity spotlight - Gold

The rising optimism over the Federal Reserve raising US interest rates in March has encouraged sellers to repeatedly attack Gold. Although risk aversion from geopolitical tensions in East Asia may provide some support for the zero-yielding metal, prices are looking increasingly pressured on the daily charts. A solid NFP this Friday combined with a strengthening Dollar could provide enough downside momentum for bears to conquer $1220. From a technical standpoint, a breakdown below $1220 may open a path lower towards $1200.

Deutsche Bank Capital Raise Sends DAX Lower

The DAX Index closed the week above the 12,000 level, but has dropped lower at the start of the new trading week. In the Monday session, The DAX is trading at 11,981.89 points. On the release front, Eurozone retail sales were stable in February, as Retail PMI came in at 49.1, down slightly from 50.1 a month earlier. Eurozone Sentix Investor Confidence report improved to 20.7, beating the estimate of 18.8 points. On Tuesday, Germany releases Factory Orders, with the markets bracing for a sharp decline of 2.5%.

European stocks are broadly lower in the Monday session, as a capital raise by Germany's Deutsche Bank as reduced investors' appetite for risk. The bank decided on a major reorganization on Sunday, which includes raising EUR 8 billion by issuing 687.5 million shares on March 21. Deutsche Bank has hit rough waters, and it seemed only a matter of time before it was forced took some drastic measures to right the boat. In December, the bank reached a $7.2 billion settlement with the U.S. Department of Justice for selling toxic mortgage-backed securities. Deutsche had a dismal 2016, with losses of EUR 1.4 billion. This capital hike is the fourth since 2010, and it remains to be seen if this move will attract investors and help set the bank in the right direction. Deutsche Bank shares are down about 1.0% on Monday, which has weighed on the DAX in the Monday session.

The euro dropped below the 1.05 line on Thursday, as EUR/USD dropped close to 7-week lows. Investors seized the opportunity and locked in profits on Friday, which helped boost the sagging euro. The pair gained 1.0% on Friday, marking its strongest 1-day gain since January 5. German Retail Sales disappointed, but this didn't impede the euro's rebound. Retail Sales declined 0.8%, well off the forecast of +0.2%. This marked a fifth decline of six releases, pointing to weakness in German consumer spending. Meanwhile, Eurozone inflation levels pointed higher in February. German Preliminary CPI rebounded posted a strong gain of 0.6%, matching the estimate. The Eurozone CPI Flash Estimate rose to 2.0%, hitting the ECB inflation target. Policymakers are now faced with a concern that they haven't experienced in years – will inflation rise too fast, too quickly? The central bank could curb inflation by tightening monetary policy, but will be hesitant to tinker with interest rates or its asset-purchase program unless growth and inflation indicators heat up significant

With the US economy continuing to perform well, market sentiment has heated up regarding a Fed rate hike. Federal Reserve policymakers continue to sound hawkish about a rate move on March 15, when the Fed next meets for a policy meeting. Last week, FOMC members William Dudley and John Williams both hinted at an imminent hike by the Fed. Dudley said the case for a hike is compelling, while Williams noted that a rate increase will be up for "serious consideration" at the March policy meeting. The markets are taking these statements at face value, as the odds of a March move have increased dramatically. The likelihood of a rate this month has jumped to 80%, compared to 33% just a week ago. Why the huge jump in odds? One reason is that policymakers are now saying they won't wait for Donald Trump to outline tax reform or other economic packages before making a monetary move. This is a significant departure from a few weeks ago, when the Fed sent out signals that it would stay on the sidelines until it had a clearer picture of the economic stance of the new administration.

Lower China Growth Spooks Markets

Monday March 6: Five things the markets are talking about

With geopolitical risk dominating early trading – North Korea fired four ballistic missiles into nearby waters – this is another busy economic event week that see's an RBA (Monday 10:30pm EST) and an ECB (Thursday 7:45am EST) rate decision and an U.S non-farm payroll print (Fri. 8:30am).

Expect ECB's Draghi to come under some pressure after last month's flash-CPI data printing +2% on the year thanks largely to increases in energy and food prices.

With Fed Chair Yellen almost assuring a Fed rate hike this month (Mar 14-15) after her statements last week, this Friday's U.S jobs report is anticipated to make that decision a slam-dunk. U.S Employers are expected to add around +190k workers to payrolls, in line with the average over the past six-month.

Elsewhere, Japan will posts its second estimate of Q4 growth, while China will release both consumer and producer prices. Canada's labor force data for Feb. will be released on top of NFP.

1. Mixed results for global stocks

Asian bourses saw some mixed results in overnight trading.

In Japan, shares fell in thin trade as the yen (¥113.75) firmed and as global geopolitical tensions rose after North Korea fired four missiles. The Nikkei share average fell -0.5% while the broader Topix shed -0.2%.

In Hong King, stocks gained as China optimism offset concerns on U.S rates and N. Korea. The Hang Seng index rose +0.2%, while the China Enterprises Index gained +0.3%.

In Europe, equity indices are trading generally lower. Shares of Deutsche Bank is the notable laggard in the Eurostoxx after confirming plans to raise +€8B through a rights issue. Commodity and mining stocks are weighing on the FTSE 100 as copper prices trades sharply lower intraday

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.2% at 3,396, FTSE -0.3% at 7,354, DAX -0.3% at 11,993, CAC-40 -0.3% at 4,982, IBEX-35 +0.1% at 9,811, FTSE MIB -0.4% at 19,592, SMI -0.1% at 8,661, S&P 500 Futures -0.2%

2. Oil falls on lower China growth targets

Oil prices are under pressure, wiping out most of Friday's gains; amid worries that lower growth targets in China (see below) could cut oil demand and ongoing concern over Russia's compliance with a global deal to cut oil output.

Brent crude futures have dropped -47c, or -0.8%, to +$55.43 a barrel, while U.S West Texas Intermediate (WTI) crude futures fell -47c, or -0.9%, to +$52.86 a barrel.

Note: Russia's energy ministry released figures last week that showed February oil output was unchanged from January at +11.11m bpd – this is casting doubt on Russia's moves to rein in output as part of a pact with OPEC.

The markets remains range bound and expect dealers to take their cue from the dollars direction.

Ahead of the U.S open, gold (+0.1% to +$1,233.18) is little changed, supported by safe haven interest amid rising geopolitical tensions over North Korea and a weaker dollar. On Friday, the yellow metal hit +$1,222.51, the lowest since Feb. 15, on signals of a hike in U.S interest rates this month.

Note: Data Friday showed that both hedge funds and money managers boosted their net long position in COMEX gold to the highest in over three-months.

3. Rate differentials to dominate

The probability of a Fed rate hike this month has jumped from +35% at the beginning of last week to currently over +80% after a spate of hawkish commentary from Fed officials supporting the notion of a 'live' FOMC meeting on March 14-15. Expect Friday's NFP print to determine whether FI dealers have priced their curves correctly. Yields on 10-year Treasuries fell one -1bps to +2.47%.

This week, the ECB is likely to keep policy unchanged this week, even after eurozone inflation hit the key desired +2% mark last month. Expect ECB's Draghi to likely stress the four criteria for fighting low inflation that he outlined in January. To date, none of the four criteria have been met so far. The market expects some tweaks to the ECB's take on the regions economy and rate guidance may be less 'dovish.'

Note: 10-year Bund yields have been rising from a low of +0.18% in late February to a high of +0.36% last week, driven by increasing expectations of an interest rate increase by the Fed in March.

Down-under, fixed income markets are pricing in about a +20% chance of an RBA rate hike before the end of 2017 and also see about +50% chance of a hike by the end of Q1 of 2018. The RBA meets today (10.30pm EST). Aussie 10-year bonds are little changed at +2.80%.

4. 'Big' dollars mixed results

The USD trades mixed ahead of the U.S open. The world's reserve currency of choice is trying to consolidate its gains from last weeks Fed-inspired rally where Ms. Yellen virtually confirmed the Fed's intentions to raise rates this month.

The EUR (€1.0592) is finding some support on the back of France's political center looking less fragmented – Juppe (Conservative) confirmed he would not run for President – and with the ECB meeting this week to be "less" dovish because of stronger global inflation and calmer peripheral sovereign spread markets.

The Pound (£1.2227) continues to hover atop of its two month low outright after weak U.K data from last week. For sterling traders, the focus will be on Chancellor of the Exchequer Hammond's budget statement on Wednesday (7:30am EST).

USD/JPY (¥113.85) is softer on Korean Peninsula jitters. North Korea said to have fired 4 missiles into eastern Japanese sea.

5. China lowers 2017 GDP, M2, and Retail Sales targets

At the National People's Congress (NPC) this weekend, China adjusted its economic target for 2017. They expect a GDP target of "around +6.5% or higher if possible" vs. +6.5-7.0% in 2016. Leaders also lowered M2 money supply to +12% from +13% and retail sales to +10% from +11%. However, authorities have kept its CPI target and Fiscal Budget deficit to GDP ratios unchanged at +3% each. The PBoC has pledged to pursue "prudent, neutral monetary policy in 2017." The Defense Ministry's 2017 growth was set at +7%, down from +7.6% last year and the lowest in a decade.

Leaders also expressed a continued commitment to reducing pollution, with that in mind, regulators also announced cuts in steel capacity by another -50M tons and coal output by over -150M tons.

Premier Li has dropped a pledge he had made in similar speeches in the past three-years to ensure that the yuan "remains generally stable at an appropriate and balanced level". This suggests China's government is ready to tolerate further declines in the yuan value against the dollar.

USDJPY: Remains Vulnerable But With Caution

USDJPY: The pair still faces downside pressure though closing higher the past week. On the downside, support comes in at the 114.00 level where a break if seen will aim at the 113.50 level. A cut through here will turn focus to the 113.00 level and possibly lower towards the 112.50 level. Its daily RSI is bearish and pointing lower suggesting further weakness. On the upside, resistance resides at the 114.50 level. Further out, we envisage a possible move towards the 115.00 level. Further out, resistance resides at the 115.50 level with a turn above here aiming at the 116.00 level. On the whole, USDJPY looks to weaken in the nearer term.