Sample Category Title

Weekly Focus: Will the US Job Report Confirm a Near-Term Fed Hike?

Market movers ahead

- The US labour market report for February will be scrutinised intensively following the recent speculation about the prospect of a Fed hike in March. We estimate a non-farm payroll of 190,000 and some reversal in average hourly earnings after weakness in wages in financial activities dragged them down in January.

- In the euro area, the ECB meeting will reveal whether the rise in inflation to the ECB's 2.0% target has resulted in a more hawkish monetary policy stance. Despite the higher inflation, there are still no signs of an upward trend in underlying prices. Hence, we expect the ECB to stick to its dovish communication.

- In China, the National People's Congress this weekend will reveal the new economic targets for growth and inflation for this year.

- In Scandinavia, focus is on the Norwegian regional survey, which is Norges Bank's preferred economic indicator and particularly important as it is forward looking.

Global macro and market themes

- Reflation, Trump and European populism remain the dominant drivers of markets.

- The USD and US yields should head higher near term.

- German yields have bottomed and should rise in coming months.

- We remain bullish on US equities as Donald Trump's policy agenda is growth supportive despite all the noise.

Trade Idea: USD/CAD – Buy at 1.3300

USD/CAD - 1.3404

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Buy at 1.3255, Target: 1.3425, Stop: 1.3195

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3300, Target: 1.3450, Stop: 1.3240

Position: -

Target: -

Stop:-

The greenback has continued edging higher and near term upside risk remains for the rise from 1.2969 low to extend further gain to resistance t 1.3461, however, loss of near term upward momentum should prevent sharp move beyond 1.3500-10 and price should falter well below 1.3558, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy on pullback as 1.3300-10 should limit downside and bring another rise later. Below 1.3250 would defer and risk correction to indicated previous resistance at 1.3212 (now support) but only break there would suggest top is formed, bring weakness to 1.3165 first.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Pound Slides Continues on Soft Services PMI

GBP/USD has posted losses in Friday trade. Currently GBP/USD is trading at 1.2220. On the release front, British Services PMI dipped to 53.3, short of the estimate of 54.4 points. In the US, today's highlight is ISM Manufacturing PMI, which is forecast to remain unchanged at 56.5 points. The markets will be listening closely as four FOMC members deliver remarks on Friday, including Federal Reserve Chair Janet Yellen.

Market sentiment continues to heat up regarding a Fed rate hike. Federal Reserve policymakers continue to sound hawkish about a rate move on March 15, when the Fed next meets for a policy meeting. Earlier in the week, FOMC members William Dudley and John Williams both hinted at an imminent hike by the Fed. Dudley said the case for a hike is compelling, while Williams noted that a rate increase will be up for "serious consideration" at the March policy meeting. The markets are taking these statements at face value, as the odds of a March move have increased dramatically. The likelihood of a rate move has soared to 80%, compared to 33% just a few days ago. Why the huge jump in odds? One reason is that policymakers are now saying they don't need to wait for Donald Trump to outline tax reform or other economic packages before making a monetary move. This is a significant departure from a few weeks ago, when the Fed sent out signals that it would stay on the sidelines until it had a clearer picture of the economic stance of the new administration.

The pound's troubles continue, as the currency has fallen 1.4 percent this week. Earlier on Friday, GBP/USD dropped to a low of 1.2214, marking its lowest level since January 17. The pound has responded negatively to this week's key PMI reports. Manufacturing and Services PMIs both missed expectations, and Construction PMI continues to point to weak expansion. The softer Services PMI reflects more cautious spending by British consumers, who remain concerned about the ramifications of Brexit on the economy and their pocketbooks.

Canadian Dollar Slips to 8-Week Low on US Rate Expectations

USD/CAD continues to head lower in the Friday session. Currently, the pair is trading at 1.3420. On the release front, there are no Canadian releases on the schedule. In the US, today's highlight is ISM Manufacturing PMI, which is forecast to remain unchanged at 56.5 points. The markets will be listening closely as four FOMC members deliver remarks on Friday, including Federal Reserve Chair Janet Yellen.

It's been a week to forget for the Canadian dollar this week, as USD/CAD has gained 2.2 percent. The pair has punched above the 1.34 line, as the Canadian dollar has slipped to its lowest level since January 4. Market sentiment continues to heat up regarding a Fed rate hike. Federal Reserve policymakers continue to sound hawkish about a rate move on March 15, when the Fed next meets for a policy meeting. Earlier in the week, FOMC members William Dudley and John Williams both hinted at an imminent hike by the Fed. Dudley said the case for a hike is compelling, while Williams noted that a rate increase will be up for "serious consideration" at the March policy meeting. The markets are taking these statements at face value, as the odds of a March move have increased dramatically. The likelihood of a rate move has soared to 80%, compared to 33% just a few days ago. Why the huge jump in odds? One reason is that policymakers are now saying they don't plan to wait for Donald Trump to outline tax reform or other economic packages before making a monetary move. This is a significant departure from a few weeks ago, when the Fed sent out signals that it would stay on the sidelines until it had a clearer picture of the economic stance of the new administration.

There were no surprises from the Bank of Canada this week, which held rates at 0.50%, where they have been pegged since July 2015. However, the rate statement expressed concern, stating that the economy faces "significant uncertainties", including a lack of clarity over Donald Trump's economic agenda. Trump has called for the NAFTA trade agreement to be scrapped, although he has since backtracked and said that he only wanted to "tweak" the provisions that affect Canada-US trade. Still, Trump's protectionist leanings could hurt the Canadian economy, which sends 80% of its exports to its southern border. Even if NAFTA is left alone, the US could slap import duties on Canadian products, which would have negative ramifications for the Canadian economy.

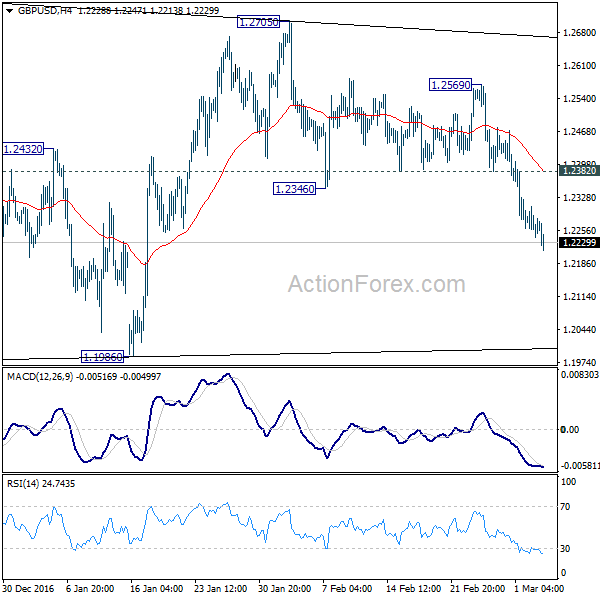

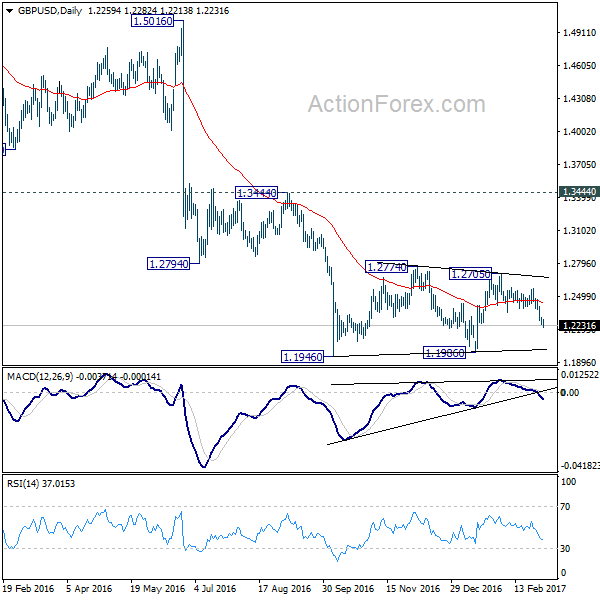

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2235; (P) 1.2271; (R1) 1.2301; More...

GBP/USD's fall from 1.2705 is still in progress and intraday bias remains on the downside for 1.1946/86 support zone. The consolidation pattern from 1.1946 has possibly completed at 1.2705. Break of 1.1946 will confirm our bearish view and resume the larger down trend. Nonetheless, on the upside, above 1.2382 minor resistance will delay the bearish case and turn bias neutral first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

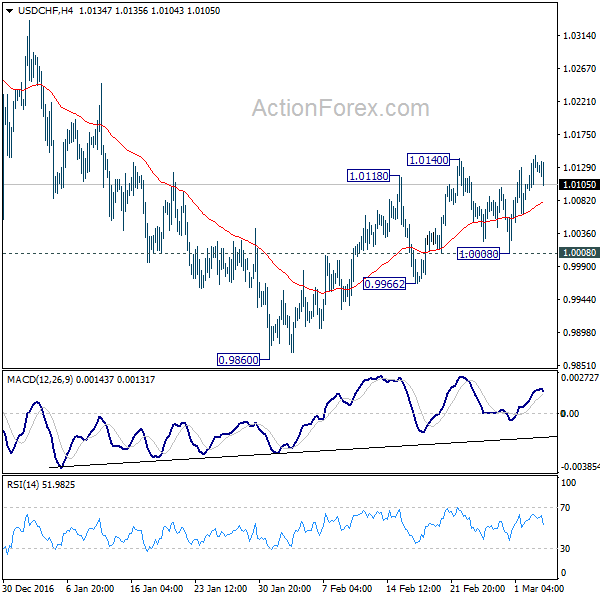

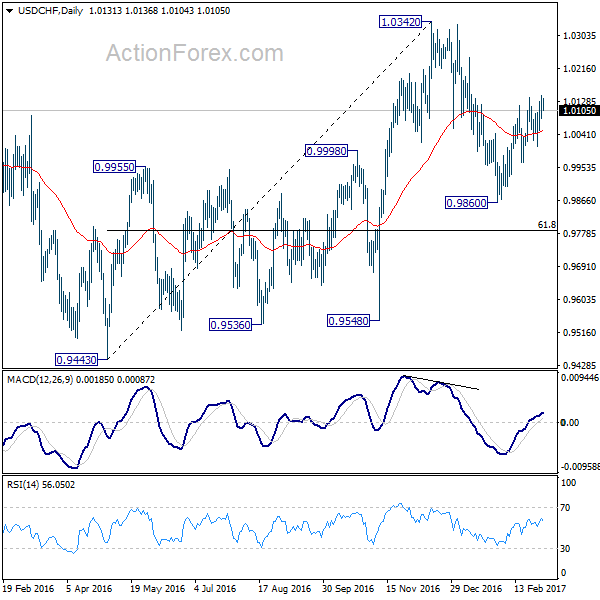

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0094; (P) 1.0120; (R1) 1.0157; More.....

Intraday bias in USD/CHF remains cautiously on the upside for the moment. Rebound from 0.9860 is resuming and would target a test on 1.0342 high. Based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. On the downside, break of 1.0008, however, will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.86; (P) 114.22; (R1) 114.77; More...

USD/JPY is still bounded below 114.94 resistance and intraday bias stays neutral first. Outlook is unchanged. Price actions from 118.65 are viewed as a corrective move. Firm break of 114.94 resistance will indicate that it's completed, on a double bottom pattern (111.58, 111.68). In such case, intraday bias will be turned to the upside for retesting 118.65. Also, the whole rise from 98.97 is likely resuming. On the downside, in case of another fall, we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Pound Slides Continues on Soft Services PMI

GBP/USD has posted losses in Friday trade. Currently GBP/USD is trading at 1.2220. On the release front, British Services PMI dipped to 53.3, short of the estimate of 54.4 points. In the US, today's highlight is ISM Manufacturing PMI, which is forecast to remain unchanged at 56.5 points. The markets will be listening closely as four FOMC members deliver remarks on Friday, including Federal Reserve Chair Janet Yellen.

Market sentiment continues to heat up regarding a Fed rate hike. Federal Reserve policymakers continue to sound hawkish about a rate move on March 15, when the Fed next meets for a policy meeting. Earlier in the week, FOMC members William Dudley and John Williams both hinted at an imminent hike by the Fed. Dudley said the case for a hike is compelling, while Williams noted that a rate increase will be up for "serious consideration" at the March policy meeting. The markets are taking these statements at face value, as the odds of a March move have increased dramatically. The Fed Rate Monitor Tool (Investing.com) is currently pricing a move at 82%, compared to 18% just a week ago. Why the huge jump in odds? One reason is that policymakers are now saying they don't need to wait for Donald Trump to outline tax reform or other economic packages before making a monetary move. This is a significant departure from a few weeks ago, when the Fed sent out signals that it would stay on the sidelines until it had a clearer picture of the economic stance of the new administration.

The pound's troubles continue, as the currency has fallen 1.4 percent this week. Earlier on Friday, GBP/USD dropped to a low of 1.2214, marking its lowest level since January 17. The pound has responded negatively to this week's key PMI reports. Manufacturing and Services PMIs both missed expectations, and Construction PMI continues to point to weak expansion. The softer Services PMI reflects more cautious spending by British consumers, who remain concerned about the ramifications of Brexit on the economy and their pocketbooks.

Global Stocks Dip ahead of Yellen’s Speech

Global stocks were pressured during Friday's trading session, as scepticism over the sustainability of the Trump-fuelled market rally and a sense of caution ahead of Yellen's speech kept investors on edge. Asian equity markets swiftly surrendered gains, while European shares descended into red territory as participants re-evaluated the likelihood of higher US interest rates. The bearish domino effect from Europe, coupled with risk aversion may limit gains on Wall Street later today.

Although the stock market rally has been phenomenal this quarter, investors should remain vigilant as the bearish attributes for a selloff still linger in the background. The political risks in Europe, Brexit woes and ongoing Trump uncertainties could still trigger a wave of risk aversion. While the upside momentum may continue to elevate global stocks to gravity-defying levels, an unexpected catalyst could trigger a selloff that brings an end to the overextended market rally.

Sterling slides to seven-week low

Sterling bears were unleashed on Friday following the unexpected decline in UK services in February, rekindling concerns that ongoing Brexit woes are negatively impacting the economy. The visible slowdown in UK services which fell to 53.3 has added to the cocktail of soft economic releases this week that continue to pressure Sterling. With sentiment towards Sterling firmly bearish, further downsides may be expected as anxiety heightens ahead of the Article 50 invocation this month. From a technical standpoint, the GBPUSD is heavily bearish on the daily charts and a breakdown below 1.2200 could encourage a further selloff lower towards 1.2050.

Janet Yellen in focus

The Greenback has been explosively bullish this trading week as expectations mount over the Federal Reserve raising US interest rates in March. The hawkish chorus of Fed officials suggesting an imminent US rate increase has made the Dollar king, while positive US economic data continues to ensure the currency remains buoyed. Much attention will be directed towards Yellen's speech this evening, which could cement expectations of a March rate hike if she reiterates a similarly hawkish mantra as other Fed officials.

Technical traders may pay attention to how the Dollar Index reacts around the 102.00 regions. There is a possibility that previous resistance at 102.00 could transform into a dynamic support, which in turn encourages a further incline higher towards 102.50.

Gold under fresh selling pressure

The growing speculation of the Federal Reserve raising US interest rates in March has exposed Gold to downside shocks, with the metal booking its biggest one-day loss of 2017 during Thursday's trading session. Sellers have exploited the repeated hawkish comments from Fed officials to pressure the yellow metal, while a strengthening Dollar continues to cap upside gains. A scenario where the Greenback continues to appreciate amid the improving sentiment towards the US economy could leave Gold vulnerable to further losses. Although the concerns over political risks in Europe, Brexit woes and Trump developments attract investors to safe haven assets in the medium to longer term, bears currently remain in control on the daily charts. From a technical standpoint, further weakness below $1220 could encourage a selloff lower towards $1200.

Commodity spotlight - WTI Crude

Oil markets were vulnerable to losses on Thursday following reports that Russian crude production remained unchanged in February, rekindling concerns of weak compliance in the global output cut deal. The sharp selloff was fuelled by US government data showing that domestic crude inventories ascended to record highs last week. Oil prices may come under increased pressure from the combination of oversupply fears resurfacing, US shale pumping oil incessantly and a strengthening Dollar. From a technical standpoint, the breakdown below $53 on WTI Crude may open a path lower towards $52.

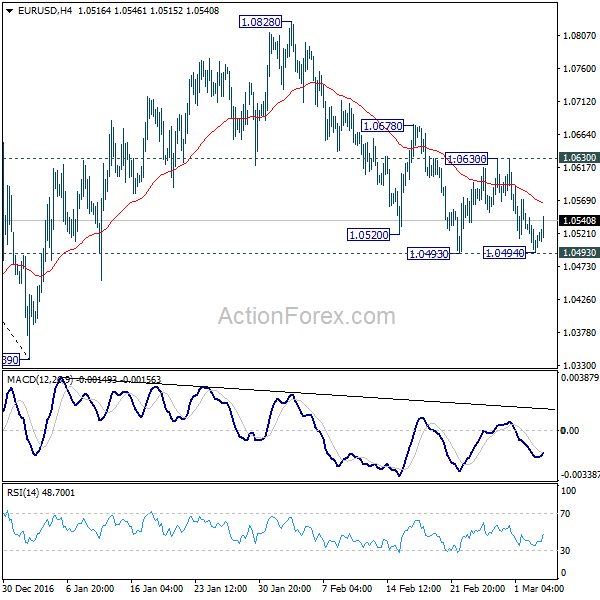

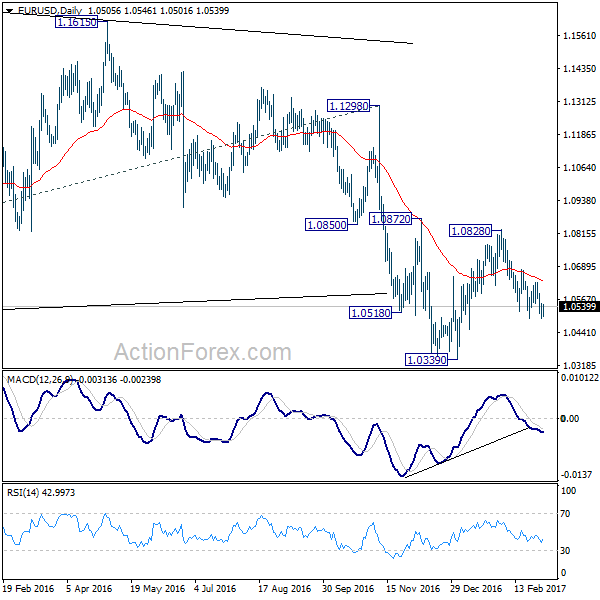

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0550; (P) 1.0590 (R1) 1.0616; More.....

EUR/USD recovers ahead of 1.0493 after forming a temporary low at 1.0494. Intraday bias remains neutral as the pair is still bounded in range of 1.0493/0630. Overall near term outlook stays bearish with 1.0630 resistance intact. Downside breakout is expected sooner or later. Fall from 1.0828 is resuming the larger down trend. Below 1.0493 will target 1.0339 low first. Break will confirm our bearish view and target parity. However, break of 1.0630 will dampen our view and turn focus back to 1.0828 resistance instead.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.