Sample Category Title

Fed’s Goolsbee expects extended series of rate cuts as economy normalizes

Chicago Fed President Austan Goolsbee highlighted Fed's outlook for an extended period of monetary easing in an interview with FOX Business overnight.

He noted, "this is a process over a year or more that we're trying to get the rates down to normal."

He also pointed out that the Fed's latest forecasts suggest "a lot of cuts" ahead, with policymakers aligned on this approach.

Fed has already begun easing, cutting its policy rate by 50bps at last meeting, bringing it to the 4.75%-5.00%.

Goolsbee refrained from committing to a specific rate cut size at the upcoming November meeting, stressing that the overall process of returning rates to more "normal" levels is the focus.

Additionally, Goolsbee noted cautionary signals in the labor market, though he remarked that the current unemployment rate of 4.2% appears to be at a sustainable level.

Fed’s Bostic sees gradual easing, possible dramatic cuts if job growth falter

In an interview with Reuters overnight, Atlanta Fed President Raphael Bostic outlined his expectations for a gradual, "orderly" easing of monetary policy over the next 15 months. His baseline scenario sees policy rate falling to a range of 3.00% to 3.25% by the end of 2025, a level he considers neutral for the economy.

However, Bostic cautioned that a "much weaker" labor market could accelerate the pace of rate cuts. He emphasized that significant job market deterioration would "add urgency" to Fed's easing process, prompting another "dramatic move" such as the 50bps rate cut enacted in September.

Bostic also noted his close attention to job growth, stating that as long as the economy continues to produce net jobs and monthly job creation stays above 100,000, the labor market will likely remain on stable footing. This threshold, in Bostic’s view, is the minimum needed to absorb new entrants into the labor force.

Gold (XAU/USD) Prices Slide as Q3 Draws to a Close

- Gold prices fell due to a stronger dollar and end-of-quarter flows, despite being on track for the best quarter since Q1 2016.

- The market is awaiting US jobs data on Friday, which could impact rate cut expectations and the US dollar.

- Gold remains extremely overbought at present, will the NFP report inspire a deeper correction?

Gold prices slid this morning as a slightly stronger dollar and end of quarter flows weigh on the precious metal. Despite the drop off, Gold remains on course for its best quarter since Q1 of 2016, which recorded gains of 16% +.

Gold continues to find support as safe haven appeal and incoming rate cuts keep bulls interested. However, the drop to start the week could be down to a number of overlapping factors such as profit taking, repositioning and the recent rally in Chinese equities and emerging markets.

The stimulus announced by the PBoC is the gift that keeps on giving where China is concerned. The rally in Chinese equities could be impacting Gold as well, given the higher yield on offer. Gold remains in extremely overbought territory and thus further upside may also prove a challenge.

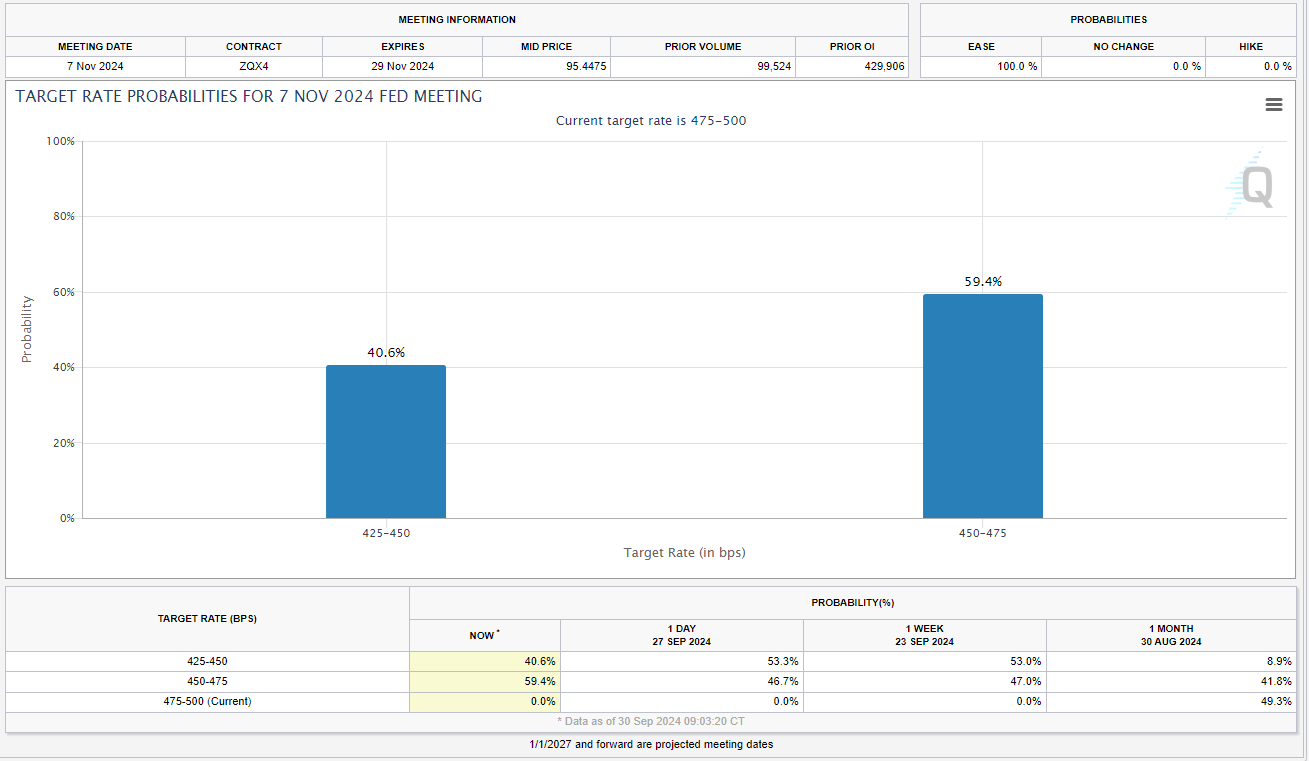

As things stand, markets could continue to range ahead of the jobs data on Friday. Any increase in rate cut expectations could lead to USD weakness. Current expectations have a 50 basis point cut in November at around 40%, down from 53% a day ago and could be partially responsible for the drop in the price of the precious metal.

Source: CME FedWatch Tool (click to enlarge)

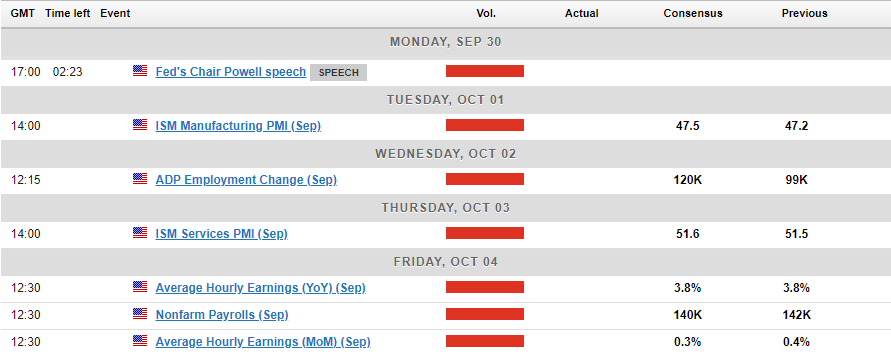

Economic Data Ahead

Gold prices face many challenges at the moment, both positive and negative. Safe haven appeal for now appears to be waning yet a weaker US Dollar as we are seeing today does have the potential to keep gold prices on the front foot.

There is a host of US data this week including services data, however the biggest volatility and potential for a change will come on Friday when the US jobs report is released. Signs of improving jobs numbers and a drop in the unemployment rate could push the precious metal lower.

Later in the day we do have a speech from Fed Chair Jerome Powell which could stoke volatility if the Fed President touches on rate cut expectations moving forward.

Technical Analysis Gold (XAU/USD)

From a technical analysis standpoint, Gold is tough to read at the minute particularly where areas of resistance is concerned. As we continue to print fresh all time highs it makes it difficult due to the lack of historical price data to analyze.

To put things into perspective, the RSI on the daily, weekly and monthly timeframe are all in overbought territory. However, as we know an instrument can languish weeks and sometimes months in overbought territory on the larger timeframes so this seems to be irrelevant at present.

The psychological 2650 mark is the most immediate area of resistance i would keep an eye on A break beyond that could open up a retest of last weeks and the all-time high print around 2685.50 before the 2700 comes into focus.

Looking at support and the 2625 area has been key over the last couple of days and could still serve as a base for gold prices. This may be a level worth monitoring moving forward.

GOLD (XAU/USD) Four-Hour (H4) Chart, September 30, 2024

Source: TradingView (click to enlarge)

Support

- 2625

- 2600

- 2585

Resistance

- 2650

- 2675

- 3000

How is Gold Prepping for NFP?

Gold prices are holding steady near $2,650 in Asian trading on Monday, despite positive market sentiment from China's new stimulus measures. Traders are hesitant to make any big moves before the speech from US Federal Reserve (Fed) Chairman Jerome Powell later today. Powell didn’t touch on the economy or monetary policy in his last speech, so investors are looking forward to hearing any clues on the possible interest rate cut in November.

Currently, the market sees a 52% chance of the Fed cutting rates by 50 basis points in November, according to the CME Group’s FedWatch Tool, slightly up from last week’s 50% odds. The recent US inflation data, especially the core Personal Consumption Expenditures (PCE) price index, hasn’t changed expectations. While the annual core PCE rate moved closer to the Fed's 2% target, Gold still pulled back from last week’s high of $2,686 as traders took profits ahead of key US employment data. Despite ongoing geopolitical tensions in the Middle East and fresh Chinese stimulus, Gold prices continue to face downward pressure Today.

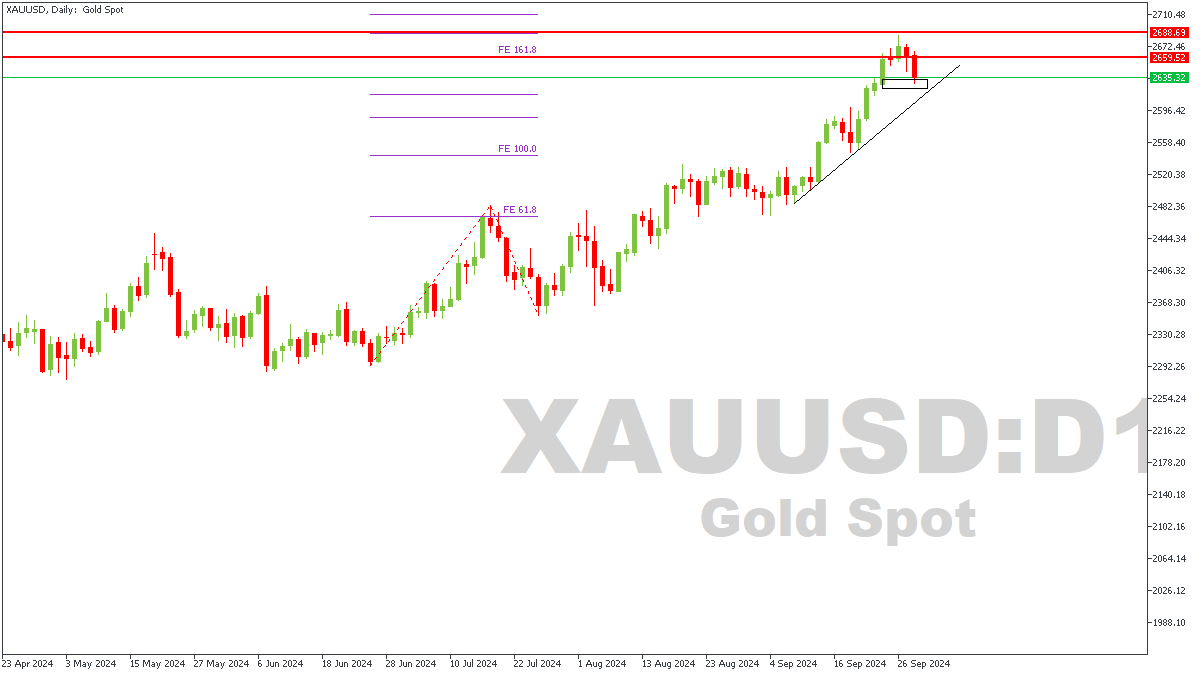

XAUUSD – D1 Timeframe

The two horizontal red lines you’re seeing on this daily timeframe chart of XAUUSD represent the pivots based on the Fibonacci expansion tool. Now, the fact that Gold is at an All-Time-High (ATH) necessitated the use of the Fibonacci expansion tool to figure out future pivots. We have also seen an initial rejection from this area, leading me to vote in favor of the ‘Bears.’

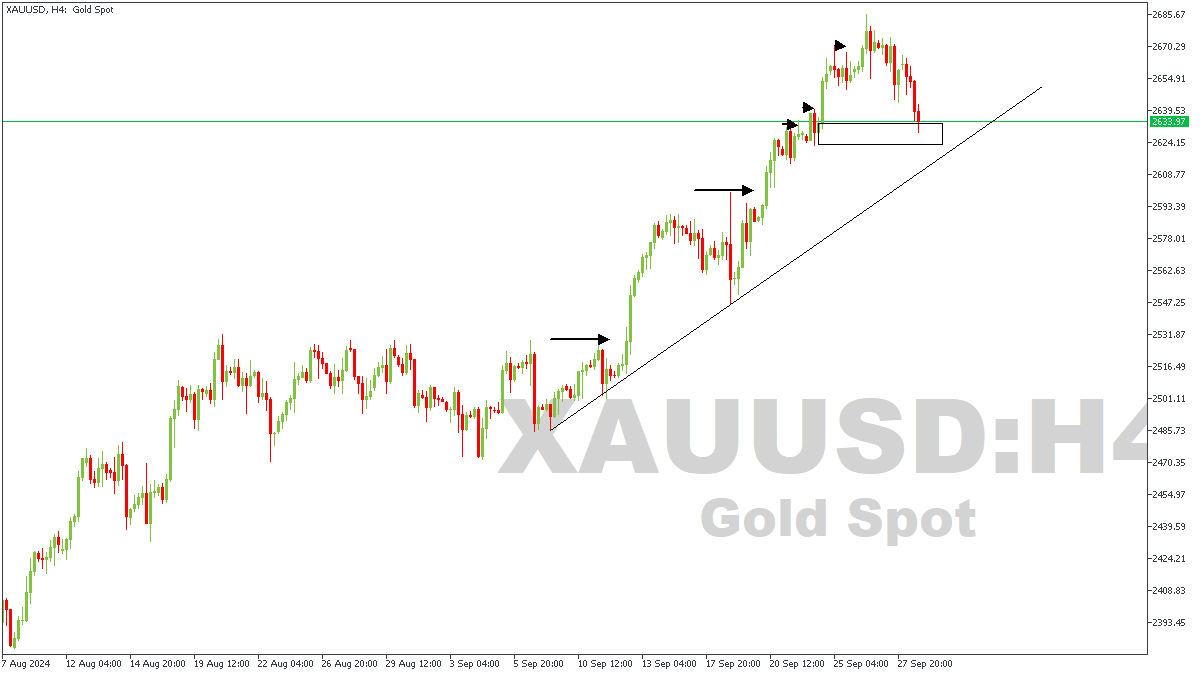

XAUUSD – H4 Timeframe

The 4-hour timeframe sheds more light into the criteria required for the confirmation of the bearish sentiment. The decider in this case being the break below the trendline support and the highlighted demand zone. Patience is advised, since a retest of the broken demand zone will provide a much safer point of entry than the aggressive approach.

Analyst’s Expectations:

- Direction: Bearish

- Target: $2,541.13

- Invalidation: $2,675.85

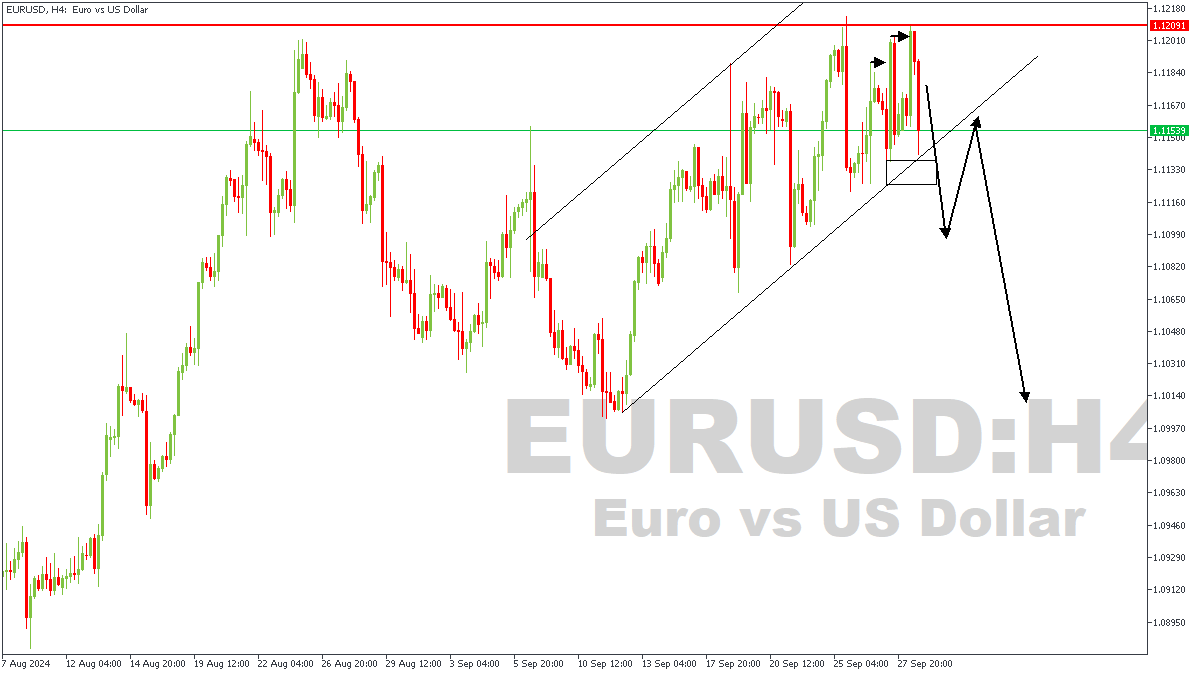

GBPUSD & EURUSD Outlook

The US Dollar (USD) is struggling to gain strength as it begins the last trading day of the third quarter. Investors are closely watching for inflation data from Germany and speeches from key Federal Reserve officials, including Chairman Jerome Powell, later in the day. On Friday, the USD Index fell to its lowest point in over a year, hitting 100.15, before slightly recovering. Early Monday, the USD Index is still under pressure, staying below 100.50. Meanwhile, US stock index futures are trading slightly lower.

In China, economic data showed a decline in both the manufacturing and services sectors, putting more pressure on the country’s already struggling economy. However, the Australian dollar (AUD) has benefited from positive business confidence data, pushing AUDUSD to its highest level since February 2023. In the UK, revised GDP data showed slower growth than initially reported, but GBPUSD remains steady just below 1.3400.

EURUSD– H4 Timeframe

The price on the 4-hour timeframe of EURUSD has recently come under heavy rejection from the daily timeframe pivot, leading to a suspicion that a bearish shift in market structure could be underway. The outcome is however going to depend on the ability of the momentum to break below the confluence region of the trendline support and the demand zone. What I mean is that if price can successfully break below the trendline and the demand zone, we would have confirmation of the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.10460

- Invalidation: 1.12033

GBPUSD – H4 Timeframe

Price action on the 4-hour timeframe of GBPUSD closely mirrors what we have on the same timeframe chart of EURUSD. In the case of GBPUSD though, the rejection is coming from a pivot some within an area of imbalance on the weekly timeframe. The expected outcome is however the same. I’m looking forward to a break in the market structure, as well as the trendline as the requisite confluence for the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.32176

- Invalidation: 1.34414

Euro Steady as Germany’s CPI lower Than Expected

The euro is steady at the start of the trading week. EUR/USD is trading at 1.1170 in the North American session at the time of writing, up 0.06% on the day.

Germany’s CPI eases to 1.6%

Inflation in Germany slowed to 1.6% y/y in September, down from 1.9% in August and shy of the market estimate of 1.6%. This was the lowest level since February 2021 and was driven by a sharp drop in energy costs. Monthly, inflation was flat, up from -0.1% in August and below the market estimate of 0.1%. Core inflation dropped to 2.7%, down from 2.8% in August and its lowest level since January 2022.

The decline in inflation in the eurozone’s largest economy is typical of what is happening across the bloc. Eurozone inflation will be released on Tuesday with a market estimate of 1.9%, compared to 2.2% in August, which was a three-year low. An inflation reading below the 2% target would be highly symbolic and increase the pressure on the ECB to continue to trim rates in order to kick-start the weak economy.

The ECB remains cautious about rate cuts as services inflation and wage growth remain high. Policy makers are likely to stay on the sidelines in October in order to monitor key data and wait until December before making any rate moves.

US Core PCE Index drops to 0.1%

The Fed appears to have inflation under control and the US Core PCE Price Index, the Fed’s preferred inflation indicator, was within expectations on Friday. The index rose 0.1% m/m in August, a three-month low. This was down from 0.2% in July and below the market estimate of 0.2%. Yearly, Core PCE ticked up to 2.7%, after three consecutive months at 2.6% and in line with expectations.

EUR/USD Technical

- EUR/USD is testing resistance at 1.1164. Above, there is resistance at 1.1202

- 1.1124 and 1.1086 are providing support

Sunset Market Commentary

Markets

With national German (and Italian) inflation data, an appearance of ECB present Christine Lagarde before the EU Parliament and Fed Chair Powell speaking before the National Association of Business Economics conference (Nashville), investors today already receive quite some interesting input to challenge their positioning regarding the outcome of the next ECB (Oct 17, unchanged or frontloading to 25 bps cut) and Fed meetings (Nov 7, 25 bps or 50 bps). German headline HICP eased further to -0.1% M/M and 1.8% Y/Y (from -0.2% M/M and 2.0% last month), but contrary to Spanish and French data on Friday didn’t bring a big downside surprise. German national data (headline 0.0% and 1.6%) released by the statistical office showed ongoing disinflation in goods (-0.3% Y/Y) with energy prices declining 7.6%% Y/Y. However, the slowdown in core inflation (2.7% from 2.8%) and services inflation (3.8% from 3.9%) proceeds only at a very gradual pace. With markets this morning discounting a 75% chance of an October ECB rate cut, some investors turned a bit more cautious. 2-y German yields intraday added 5 bps ahead the speeches of ECB’s Lagarde and Fed’s Powell. The US 2-y even added about 6 bps. At the hearing before the European Parliament, Lagarde acknowledged that Europe’s recovery is facing headwinds and saw disinflation accelerating. It might rise again due to base effects in Q4. Still, the ECB will take into account the increased confidence of taming inflation in October. With core inflation still sticky, this is no outright commitment to cut. Even so, it is no formal dismissal either. The issue might lead to an interesting (public) debate between hawks and doves that might already openly start in the coming days. EMU yields reversed most of the intraday uptick (German 2-y yield +1.0 bp, 30-y -1.0 bp). Understandably, the intraday setback in the US is much more modest. The US 2-y yield adds 5.0 bps. The 30-y +0.5 bps. Will Powell be as ‘clement’ as his European counterpart this evening? On other markets, the ongoing, stimulus-driven China equity rally doesn’t provide further spill-overs to European and/or US equity markets anymore. The Eurostoxx 50 cedes 1.0 %. US indices area easing modestly after the Dow (-0.5%) closed at a record level last Friday. Lagarde keeping the door open to at least to assess the merits of an October cut and as such a widening of the US-EMU interest rate differentials again has remarkably little impact on the euro (or the dollar). After again filling offers north 1.12 (and near the YTD top) EUR/USD currently eases only modestly to 1.1175. DXY still struggles to avoid further losses (little changed at 100.4).

News & Views

The Swiss KOF Economic barometer continued to rise in September, albeit only very slightly. It increased from 105 in August (upwardly revised from 101.6) to 105.5, the second best level since October 2021, suggesting that the Swiss economy is slowly working its way out of the trough. Details showed that almost all indicator bundles for the economic sectors point to a more favourable outlook than before with producing industries (manufacturing & construction) standing out. General business situation, export opportunities and intermediate input purchases are increasingly pointing to improvement. On the demand side, indicators for consumer demand were unchanged (slightly above average) while indicator for future foreign demand are weakening. The Swiss franc loses some ground today, but that’s not related to the data. Rising core bond yields even outweigh risk-off market sentiment, putting CHF in the defensive. EUR/CHF rises from 0.9390 to 0.9440.

September Polish inflation figures printed exactly in line with consensus, sticking with the 0.1% M/M pace from August to rise from 4.3% Y/Y to 4.9% Y/Y and further away from the National Bank of Poland’s 2.5% inflation target (with a +-1 ppt tolerance band). It’s the sixth consecutive Y/Y-increase lifting inflation to its highest level YTD. Details showed fuel prices dropping by 3.4% M/M while prices for food and non-alcoholic drinks and for electricity, gas and others both rise by 0.2% M/M. Core inflation will only be published on October 16, but the current breakdown suggests a new acceleration likely bringing core CPI back above 4% (from 3.7% in September) in Y/Y terms. Inflation developments defend the current NBP approach of sticking to the 5.75% policy rate for now and holding back from a protracted cutting cycle like local peers (eg CNB and MNB). The NBP meets on Wednesday, but the November meeting (including updated growth and inflation forecasts) will be more interesting. EUR/PLN holds near multi-year strongest levels for PLN at 4.28.

Graphs

EUR/PLN: rising inflation suggest zloty won’t lose interest rate support anytime soon.

EUR/CHF: improving growth outlook might make it less evident for SNB to reduce policy rate. CHF is holding strong.

EMU 2-y swap: Lagarde acknowledging faster disinflation and poor growth keeps EMU short-term yields under pressure.

Iron ore: propelled higher on China stimulus.

ECB’s Lagarde signals growing confidence in disinflation but economic recovery faces obstacles

During a hearing before the Committee on Economic and Monetary Affairs of the European Parliament today, ECB President Christine Lagarde indicated that inflation might "temporarily increase" in Q4, largely due to the previous sharp declines in energy prices dropping out of the annual inflation rate calculations.

However, she added that "the latest developments strengthen our confidence that inflation will return to target in a timely manner". ECB will factor these dynamics into its next monetary policy meeting scheduled for October.

On the topic of economic growth, Lagarde acknowledged that the "suppressed level of some survey indicators" points to the challenges the recovery is facing. Nonetheless, she anticipates that the recovery will strengthen over time, as rising real incomes are expected to boost household consumption.

Lagarde reiterated ECB's data-dependent approach and emphasized that ECB is "not pre-committing to a particular rate path".

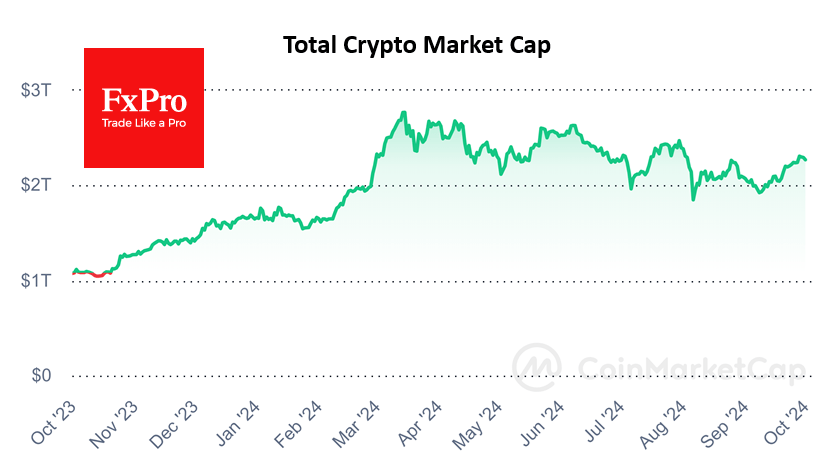

Crypto Market Takes Defence

Market Picture

The cryptocurrency market starts the week on the defensive, losing 1.2% of its capitalisation in 24 hours to $2.27 trillion, although it is still up 3% from a week ago. This drawdown looks like short-term profit-taking from the recent wave of gains amid the risks of the upcoming jobs report and Powell’s comments.

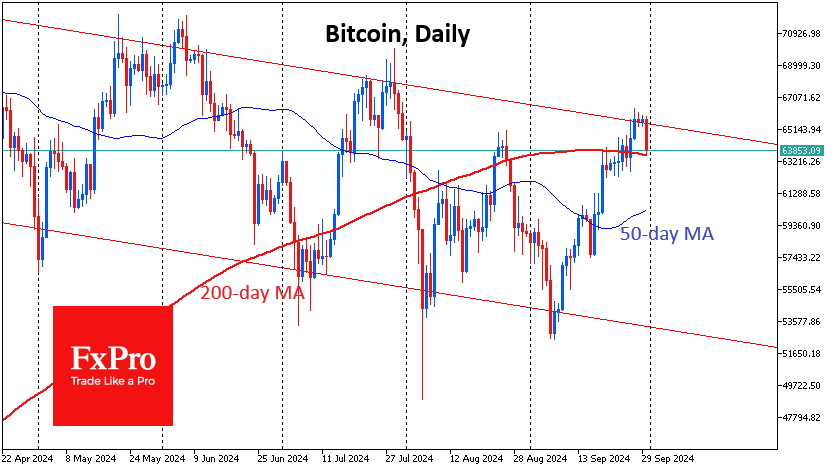

The first cryptocurrency is down 2.6% on Monday, retreating to $64.0K. On the technical side, bitcoin has come under pressure near the upper border of a multi-month downtrend. However, we see this as having more of an emotional component, as we believe that the break above the previous highs and the 200-day moving average served as an important signal of bullish dominance.

Bitcoin is on the verge of its best September since 2012. BTC has gained more than 11% since the beginning of the month, in stark contrast to the typical decline this month. The altcoin index is up more than 20% after easing financial conditions amid a global wave of interest rate cuts by the Fed, ECB and PBC.

Bitcoin closed higher for the third week, hitting its highest level since late July on Friday at around $66,500. The positive momentum in US spot bitcoin ETFs continued through all five trading sessions of the week.

News Background

According to SoSoValue, inflows into US spot bitcoin ETFs totalled $1.11 billion last week, the largest in 10 weeks, including inflows of $494.3 million. Cumulative inflows since the launch of BTC ETFs in January rose to $18.80 billion (+6.3% for the week). The Ethereum ETF turned positive after six weeks of outflows, with net inflows of $84.5 million.

Prices for 90% of altcoins traded on Binance have crossed above the 50 DMA, notes GoaSymmetric. Altcoins are ‘waking up’. ‘This is nothing compared to what we will see in the next six months,’ said Michael van de Poppe, founder of MN Trading.

Grayscale has updated its list of 20 cryptocurrencies that could outperform the market in Q4. As a result of the next rebalancing, SUI, TAO, OP, HNT, CELO, and UMA will be added to the ‘model portfolio’. RENDER, MNT, RUNE, PENDLE, ILV and RAY were removed.

CCData calculates that the companies behind the top five stable coins by market capitalisation will lose about $625m in annual revenue after the Fed’s 50bp rate cut in September. US Treasuries account for 80.2% of stablecoin issuers’ reserves. Cumulatively, they hold around $125bn of the country’s national debt.